SMR - The Bear Nucleus: Skepticism Over NuScale

2023-11-08 13:43:49 ET

Summary

- NuScale Power Corporation is rated as a STRONG SELL due to its high cash burn and non-competitive technology.

- The company specializes in small modular reactors (SMRs) but faces challenges in terms of cost and competitiveness compared to other energy sources.

- Existing contracts with clients are unlikely to be successful, raising doubts about the company's future prospects.

In recent months I have published many analyses on stocks related to the climate transition, focusing especially on small companies with disruptive technologies. Continuing on this path, in recent days I have focused my attention on NuScale Power Corporation ( SMR ).

After a careful analysis of the company, its financials, its technology, and its future prospects, my rating is a firm STRONG SELL. Not only is it a company that is burning a worrying amount of cash in the short term, but I also believe that in the long term it is developing a non-competitive technology with little potential.

My investment thesis is also supported by data from a recent short-seller report by Iceberg Research , which highlights significant issues related to the few existing contracts of NuScale.

Business Model

NuScale specializes in small modular reactors (SMRs). The company has created a 77 MW reactor, called the NuScale Power Module, which can be assembled into power plants with four, six, or twelve reactors.

The advantage of these reactors is supposed to be that they can provide a high amount of power in a small space compared to other energy sources. A VOYGR-12 plant with 12 reactors occupies just 0.05 square miles, but is capable of delivering 924 MW of power to the grid. And as always with nuclear energy, it does so without emitting greenhouse gases into the atmosphere.

The company began production of the first components in April, after many years of development that led to the approval of the reactor design by the US Nuclear Regulatory Commission.

The company has two major contracts underway:

- The largest is with Standard Power , a company that deals with data centers for cryptocurrency mining. This is a contract for 1.8 GW valued at an estimated $37 billion. Delivery is expected by 2029;

- The longest ongoing project is the Carbon Free Power Project (CFPP), which proposes 4 reactors from the Utah Associated Municipal Power Systems funded with over $1 billion from the Department of Energy. It is expected to start producing energy in 2029 and reach full operational capacity by 2030.

3D Rendering of a 12-module VOYGR plant (NuScale)

Financials and Valuation

At the moment, NuScale is essentially a pre-revenue company, since the only revenues come from the secondary business unit related to training, testing, and engineering services on the company's nuclear products. Below I present the main financial data recorded by NuScale in recent years (in $ millions, source Seeking Alpha).

| Dec 2019 |

| Dec 2020 |

| Dec 2021 |

| Dec 2022 |

| TTM |

| Revenue |

| 0.4 |

| 0.6 |

| 2.9 |

| 11.8 |

| 17.9 |

| Operating income |

| -127.6 |

| -158.8 |

| -174.3 |

| -230 |

| -245.1 |

| EBITDA |

| -125 |

| -156.8 |

| -172.1 |

| -227.3 |

| -242.4 |

| Net income |

| -71.1 |

| -88.4 |

| -102.5 |

| -141.6 |

| -162.2 |

| Cash from operations |

| -66.4 |

| -47.2 |

| -99.2 |

| -148.6 |

| -166.9 |

| Cash & Equivalents |

| 17.1 |

| 4.9 |

| 77.1 |

| 217.7 |

| 154.4 |

| Total debt |

| 16.8 |

| 36.9 |

| 15.4 |

| 4.4 |

| 3.7 |

The aspect I want to focus on is the fact that the company has less cash on hand than what it has burned over the past 12 months, and at the same time, it will be another 6 years before the first project becomes operational. I also have many doubts about the realization of these contracts. Consequently, I have no doubt that the company will have to significantly dilute the ownership shares of the shareholders before selling the first plants and the first kilowatts of energy.

Being the only publicly traded company dedicated to SMRs, it is difficult to find terms of comparison for the valuation of the company. Moreover, being a pre-revenue company, we cannot even rely on the growth rate and much less on elements such as DCF or sum-of-the-parts.

Currently, the company's market cap is $790 million, a valuation that I find very difficult to justify given that:

- In my view, the contracts with clients are very unlikely to be successful, as I will explain better shortly;

- The company's business model has fundamental problems, which make it very difficult for NuScale to ever become a major energy producer.

Why I am Bearish on NuScale

My investment thesis is based on two essential points:

- I consider NuScale's SMRs and more generally this energy source to be uncompetitive;

- The low probability of successful outcomes for the two existing contracts.

I will explain these two points in detail below.

1. In my opinion, SMRs are not competitive in the energy arena

I think the numbers speak for themselves: comparing the installation and energy production costs of NuScale against the main market alternatives, it is an extremely non-competitive solution.

Taking the CFPP contract as a reference, in January 2023, the construction cost estimates and terms for the sale of energy were updated :

- The estimated realization cost has increased from $5.3 billion to $9.3 billion;

- The energy selling price was renegotiated from $58/MWh to $89/MWh. If it was not competitive to start with, it is now absolutely out of the market.

Let's remember that this is a 462 MW project. Let's now look at the cost of the main alternatives:

- The current cost to install wind turbines is about $800-950 per KW . A 462 MW project therefore requires an initial investment of approximately $369-439 million. Considering the midpoint between these two values, this means that currently, SMRs are 23 times more expensive than wind energy;

- The price for the installation of photovoltaic panels is currently around an average of $876 per KW . This means that currently installing 1 KW of power from photovoltaic panels is 22 times less expensive compared to installing 1 KW of power from NuScale's SMRs.

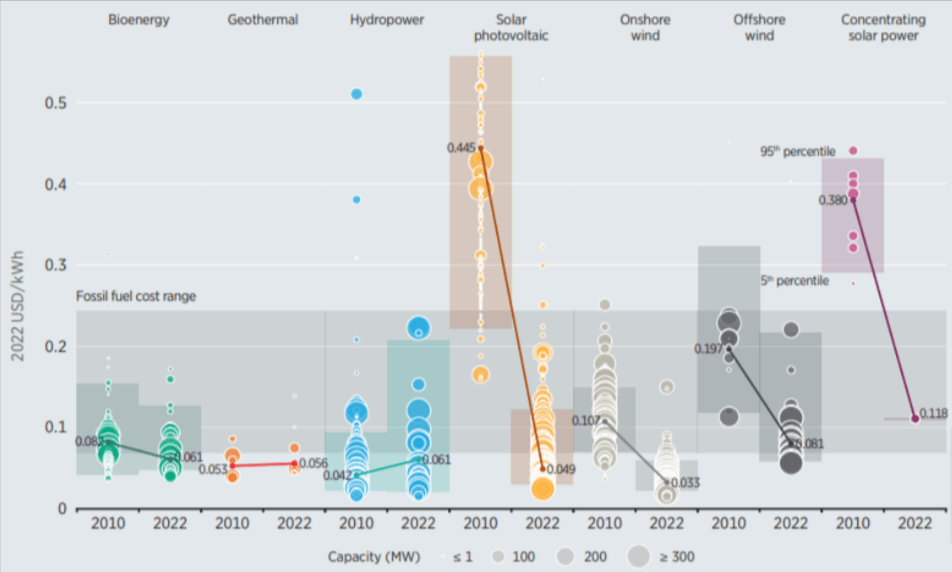

Moving on to the production cost, here I report a chart from the 2022 annual report of the International Renewable Energy Agency (IRENA).

{kind=link}

According to this data, the current cost of producing renewable energy per MWh is:

- $56 for geothermal energy.

- $33 for onshore wind energy.

- $81 for offshore wind energy.

- $49 for photovoltaic energy.

- $61 for hydroelectric energy.

Even excluding further increases in production prices projected by NuScale, with its price of $89 per MWh, the energy produced from SMRs is already far more expensive compared to all the main alternatives.

We are therefore faced with a system that is significantly more capital intensive compared to existing technologies, which promises higher costs for the energy produced as well as the need to manage stocks of spent nuclear fuel: a lose-lose-lose situation, which does not leave me hopeful for the future of NuScale.

Serious Doubts About Ongoing Contracts

Here is an excerpt from the short-seller report that I find particularly important:

"NuScale, a developer of small modular nuclear reactors, recently disclosed a huge contract with blockchain datacenter service provider Standard Power. The deal aims for a projected capacity of 1,848 MWe that we estimate is worth ~$37bn. This contract has zero chance of being executed as Standard Power clearly does not have the means to support contracts of this size.

NuScale has a more credible contract with the Carbon Free Power Project ("CFPP") for the Utah Associated Municipal Power Systems ("UAMPS"). CFPP participants have been supportive of the project despite contracted energy prices that never seem to stop rising, from $55/MWh in 2016, to $89/MWh at the start of this year. What many have missed is that NuScale has been given till around January 2024 to raise project commitments to 80% or 370 MWe, from the existing 26% or 120 MWe, or risk termination. Crucially, when the participants agreed to this timeline, they were assured refunds for project costs if it were terminated, which creates an incentive for them to drop out. We are three months to the deadline and subscriptions have not moved an inch."

NuScale has replied with a press release that states the following:

"Standard Power is a private entity backed by U.S.-based ultra-high net worth family offices and financial institutions, with data center projects in development requiring approximately four gigawatts of power. Standard Power is led by Chairman Douglas Wurth, who served for nearly 20 years as a senior executive member of J.P. Morgan and formerly practiced law at New York-based multinational firm Skadden, Arps, Slate, Meagher & Flom LLP. Contrary to what was reported, Adam Swickle has not worked with Standard Power since May 2020.

[...]

While the CFPP being developed by Utah Associated Municipal Power Systems has its own project challenges not attributable to NuScale's SMR technology, the work we have completed to date has advanced our nuclear power modules to the point that utilities, governments and industrials can rely on a proven SMR technology that has regulatory approval, is in active production and is ready for commercial deployment"

Standard Power currently operates only this 50MW data center in Ohio with plans to scale capacity to 1,23 GW in the next two years (Standard Power)

{kind=link}

After verifying all the issues in question, Iceberg Research seems to have hit the mark with their bearish report. Indeed, Standard Power is still a very small company. It is not directly supported by UHNW (Ultra-High Net Worth) families, but by "US-based UHNW family offices and financial institutions with access to capital in excess of $10 billion". This means that some family offices and private equity funds have invested in this company, and collectively these financiers have an AUM (Assets Under Management) of over $10 billion. It's quite different from saying that these institutions have promised investments of billions of dollars in the capital of Standard Power. And not even with all the $10 billion available, in any case, could a project 4 times larger than the CFPP be financed.

Beyond this dispute, in my opinion, simple logic is enough to notice the incongruity of this contract. Companies that deal with blockchain, mining, and data centers are rightly obsessed with the price of energy, one of the most important variable costs for their business. It would make no sense to develop data centers powered by the most expensive energy source currently in circulation. And we're not talking about a small pilot project, but a project that, if realized, would see the size of Standard Power multiply in a few years.

Regarding the second response, that concerning the CFPP, I think it speaks for itself: the company has only commented that it believes it has learned a lot from the project. I'm sensing that it's almost like management assumes that it will not be able to reach the necessary subscription quota to move the project forward. The quota is addressed in the revision of the contract , on page 2.

Conclusions and final thoughts

I can't remember a time when I was more certain to state a STRONG SELL rating. In my opinion, NuScale's rate of cash burn, lack of price competitiveness, and short-term challenges related to the only two existing contracts are enough to recommend to those who have the stock in their portfolio to sell it. Over the next few days, I will also consider buying put options, but first, I will let the quarterly data presentation pass to make sure there are no big unexpected announcements.

I honestly do not see how, in today's competitive arena and considering the very high interest rates, serious clients interested in purchasing SMRs from NuScale could come forward. Without drastically reducing installation and production costs, I believe this technology will never be competitive.

Upside Risks

While I am very confident in my investment thesis, it also presents risks:

- Standard Power may actually be able to find the necessary funding sources to proceed with the purchase of nuclear reactors;

- NuScale could succeed in completing the CFPP project;

- The company could manage to develop new technologies to reach more competitive price levels compared to those projected in current contracts.

Nevertheless, I believe the likelihood of these events is low, and therefore not sufficient to change my rating.

For further details see:

The Bear Nucleus: Skepticism Over NuScale