PST - The End Of Rate Hikes: Are We There Yet?

2023-08-09 11:30:00 ET

Summary

- The disinflationary trend continues, and core inflation appears to be in retreat across Western economies.

- Global central banks continued to raise interest rates, despite what looks to be clear disinflation evidence.

- Whether or not central banks keep hiking, we believe interest rate structures across most developed markets offer value.

As the market patiently waits for global central banks to wind down their rate hiking cycles, we wonder, is the journey really this long or have we gotten lost along the way?

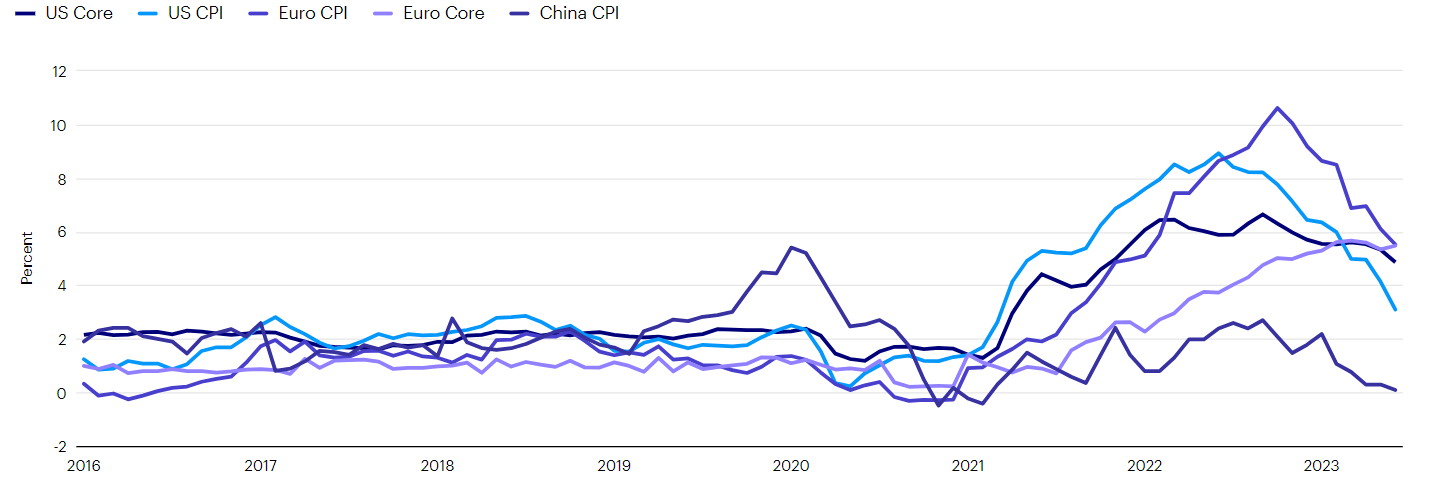

Recent economic data have been favorable for markets. The disinflationary trend that’s been in place for several quarters continues, and core inflation appears to be in retreat across Western economies. Even China is showing signs of deflation, with recent reports of falling producer prices and steady consumer prices compared to a year ago. It would appear to be time to put fears of rising inflation to rest.

Inflation is declining around the globe

Consumer Price Index (CPI) And Core Inflation - US, Europe And China (Macrobond. Data from January 1, 2016 to June 30, 2023)

{kind=link}

On the other hand, global growth is progressing at an unexciting but non-recessionary pace, near our estimates for potential growth. We believe slow positive growth and disinflation is a good backdrop for market risk takers and should be generally associated with strong risky asset performance. Recent market performance is most likely related to investors’ growing confidence in the slow growth, disinflationary environment and their positioning accordingly.

Central banks hew to their inflation fight

The doubters continue to be led by global central banks, which have continued to raise interest rates despite what looks to be clear evidence of disinflation. Inflation proved to be higher and more persistent than central banks anticipated coming out of the pandemic lockdowns, and their reaction to this miscalculation seems to be to consciously err on the side of caution now. While the disinflationary trend has been clear, and central banks could plausibly pause to observe the impact of significant rate increases, they’ve continued to hike rates. Central banks also are signaling that rates will likely stay elevated for an extended period. If rates stay high, while inflation continues to decline, the chances of a policy overshoot increase. This could arise through lower-than-desired inflation or a recession. Either of these outcomes would likely damage the current favorable investing environment.

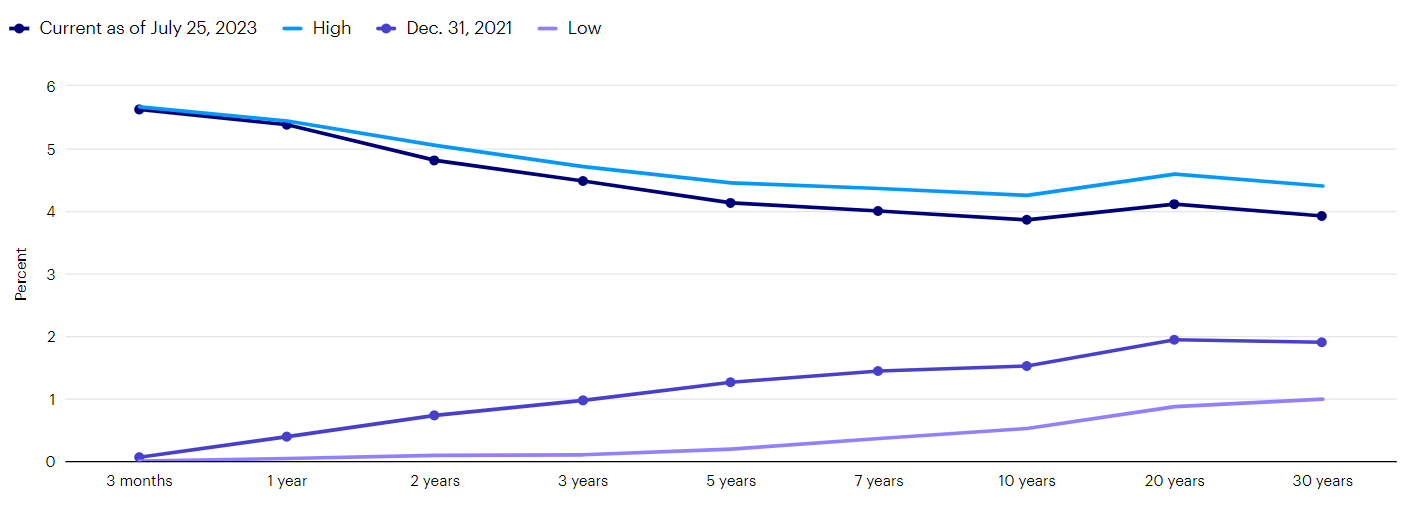

US interest rates across the yield curve are close to cyclical highs

Ten-Year Range Of US Treasury Yield Curve (Macrobond. Data from July 25, 2013 to July 25, 2023)

{kind=link}

Rate cuts could be a long way off

The question is, how will central banks manage going forward? If evidence of disinflation continues to build, as we expect it will, how will central banks respond? As the risk of lower-than-desired inflation builds, rate cuts would appear to become more appropriate. On the other hand, central bank rhetoric and expectations implied by markets argue that rate cuts may be a long time coming. Higher-than-necessary interest rates will likely increase downside risks in the coming quarters, which is something we as investors will need to pay attention to.

An opportunity in bonds

Either way, we conclude that interest rate structures across most developed markets offer value. With interest rates across yield curves close to cyclical highs, disinflation well-established, and central banks leaning very hawkishly, we believe investors have a very compelling opportunity in bonds. With the risk of an inflationary spiral off the table, we believe both the base case and risk cases involve solid potential total returns in bonds.

Important information

NA3038184

Header image: Thomas Winz / Getty

Past performance is not a guarantee of future results.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer's credit rating.

The Consumer Price Index (CPI) measures changes in consumer prices. Core CPI excludes food and energy prices.

An investment cannot be made directly in an index.

Tightening monetary policy includes actions by a central bank to curb inflation.

The yield curve plots interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates to project future interest rate changes and economic activity.

The opinions referenced above are those of the author as of July 17, 2023. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

©2023 Invesco Ltd. All rights reserved.

The end of rate hikes: Are we there yet? by Invesco US

For further details see:

The End Of Rate Hikes: Are We There Yet?