SLB - The Energy Rebound - SLB Seems Way Too Cheap

2023-10-30 15:54:22 ET

Summary

- SLB is one of the largest providers of fossil fuel production services, offering valuable insights into the industry.

- The company is attractively valued and poised to benefit from rebounding investment activity and higher-margin operations.

- The energy sector continues to trade at a significant discount, with a lack of investments impacting the industry as a whole.

Introduction

SLB ( SLB ) , formerly known as Schlumberger, is a fascinating company for a number of reasons. It's one of the world's biggest providers of fossil fuel production services, which means the company's comments and numbers tell us a lot about this industry.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Well Construction | ||||

| 8,706 | ||||

| 38.0 % | ||||

| 11,397 | ||||

| 40.6 % | ||||

| Production Systems | ||||

| 6,710 | ||||

| 29.3 % | ||||

| 7,862 | ||||

| 28.0 % | ||||

| Reservoir Performance | ||||

| 4,599 | ||||

| 20.1 % | ||||

| 5,553 | ||||

| 19.8 % | ||||

| Digital & Integration | ||||

| 3,290 | ||||

| 14.3 % | ||||

| 3,725 | ||||

| 13.3 % | ||||

| Eliminations & Other | ||||

| -376 | ||||

| -1.6 % | ||||

| -446 | ||||

| -1.6 % |

Furthermore, it so happens that the company is very attractively valued, as it not only benefits from rebounding investment activity in the industry but also from its ability to shift to higher-margin operations.

On July 17, I wrote an article titled Schlumberger Stock: A Buy Going Into Q2 Earnings .

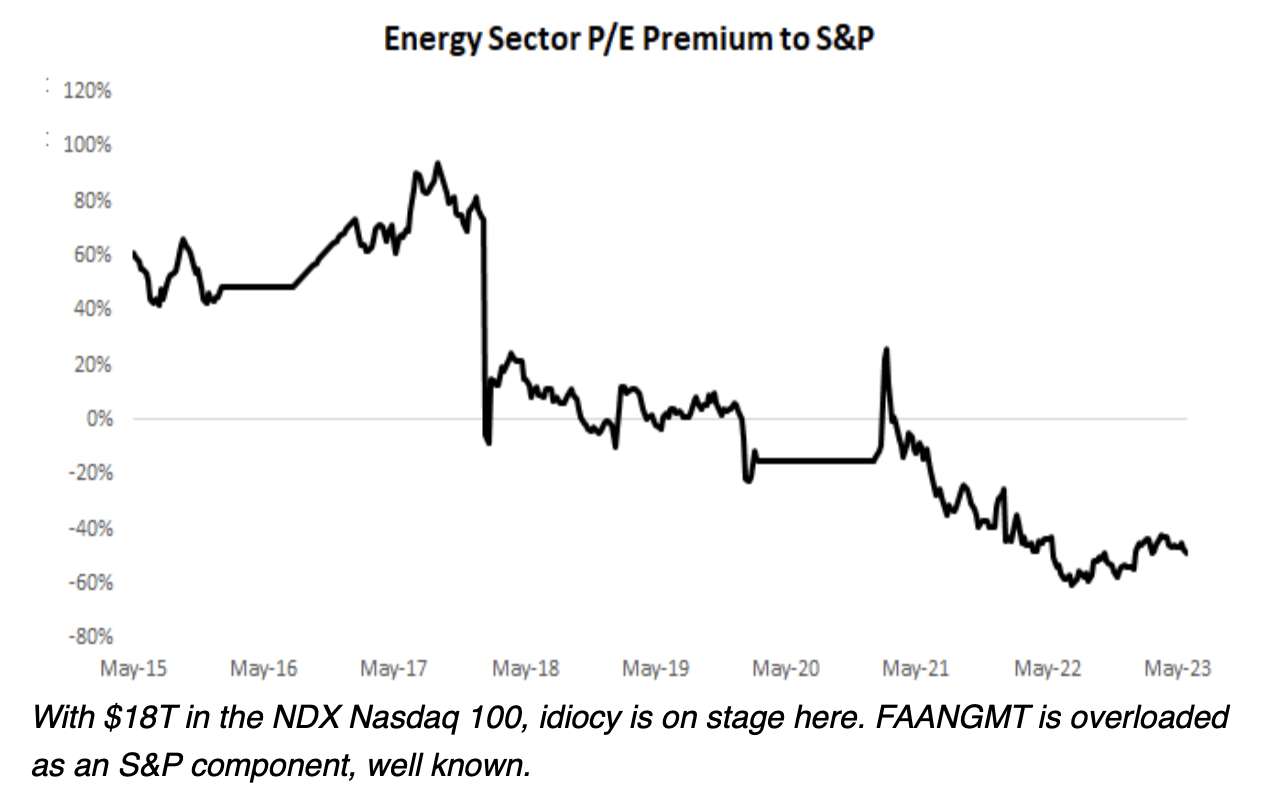

In that article, I mentioned the attractiveness of the energy sector, which is currently one of my biggest investment sectors. Back then, the energy sector traded at a significant discount, which is still the case.

{kind=link}

Bear Traps Report

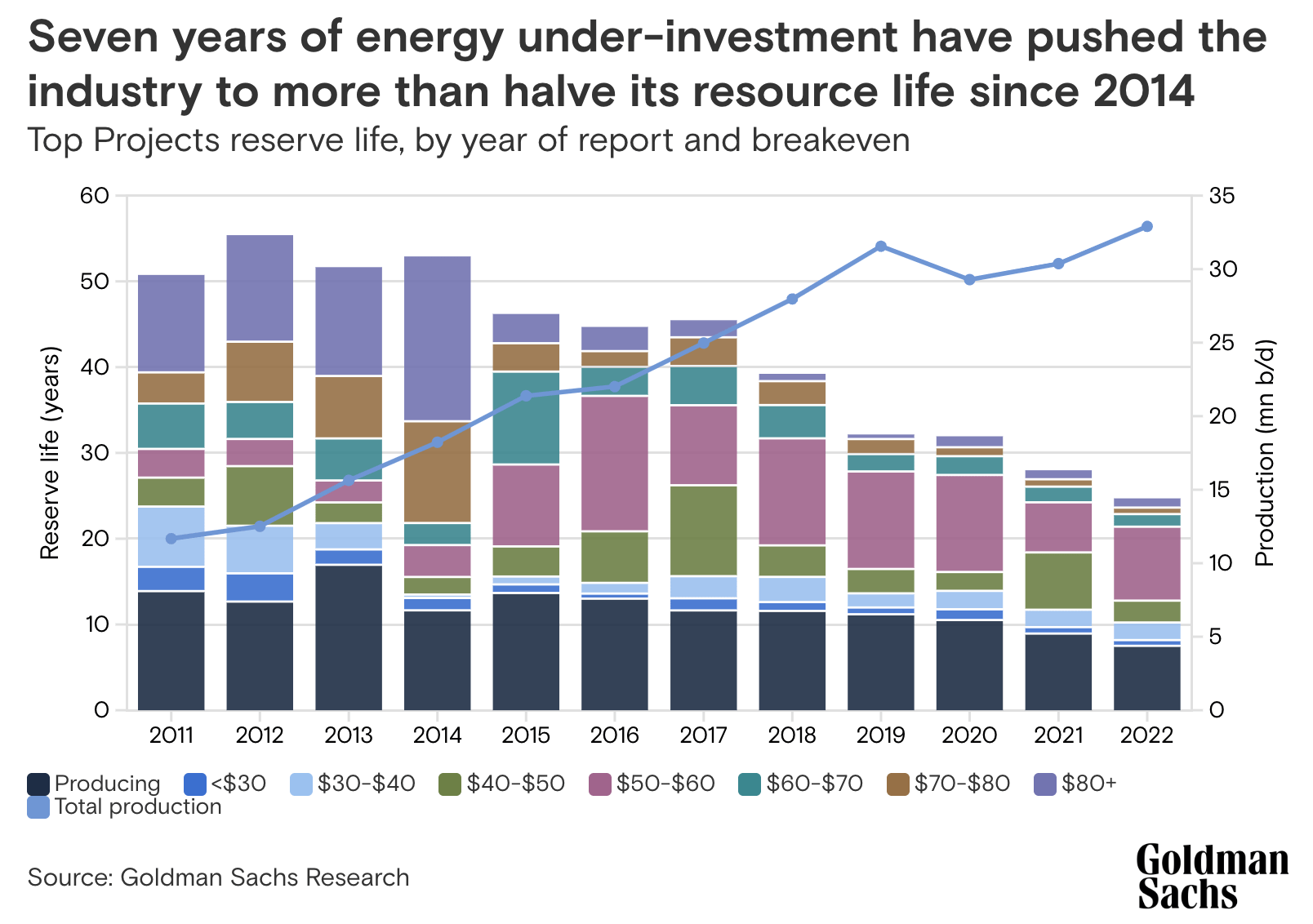

Furthermore, Goldman Sachs reported that the entire industry is suffering from a lack of investments, which has multiple reasons, including a focus on free cash flow instead of production growth and resource protection.

{kind=link}

Goldman Sachs

In light of the strong SLB numbers we're about to see in this article, we need to be aware that this is in an environment of subdued investments.

It’s fascinating, and you can read many charts in this report in that way. Capex is coming back from the trough, but again, it’s well below what it used to be in the 2010 to 2013 period. We need to remind ourselves that even with the growth, we are still well below what we used to do, the investment we used to have, just a decade ago. And demand has now again crossed the pre-Covid level and is reaching new historic highs. - Goldman Sachs

In other words, even if we see a slight shift in CapEx, it could have a tremendous impact on companies like SLB.

Which brings me to the core of this article.

SLB Is Back On Track

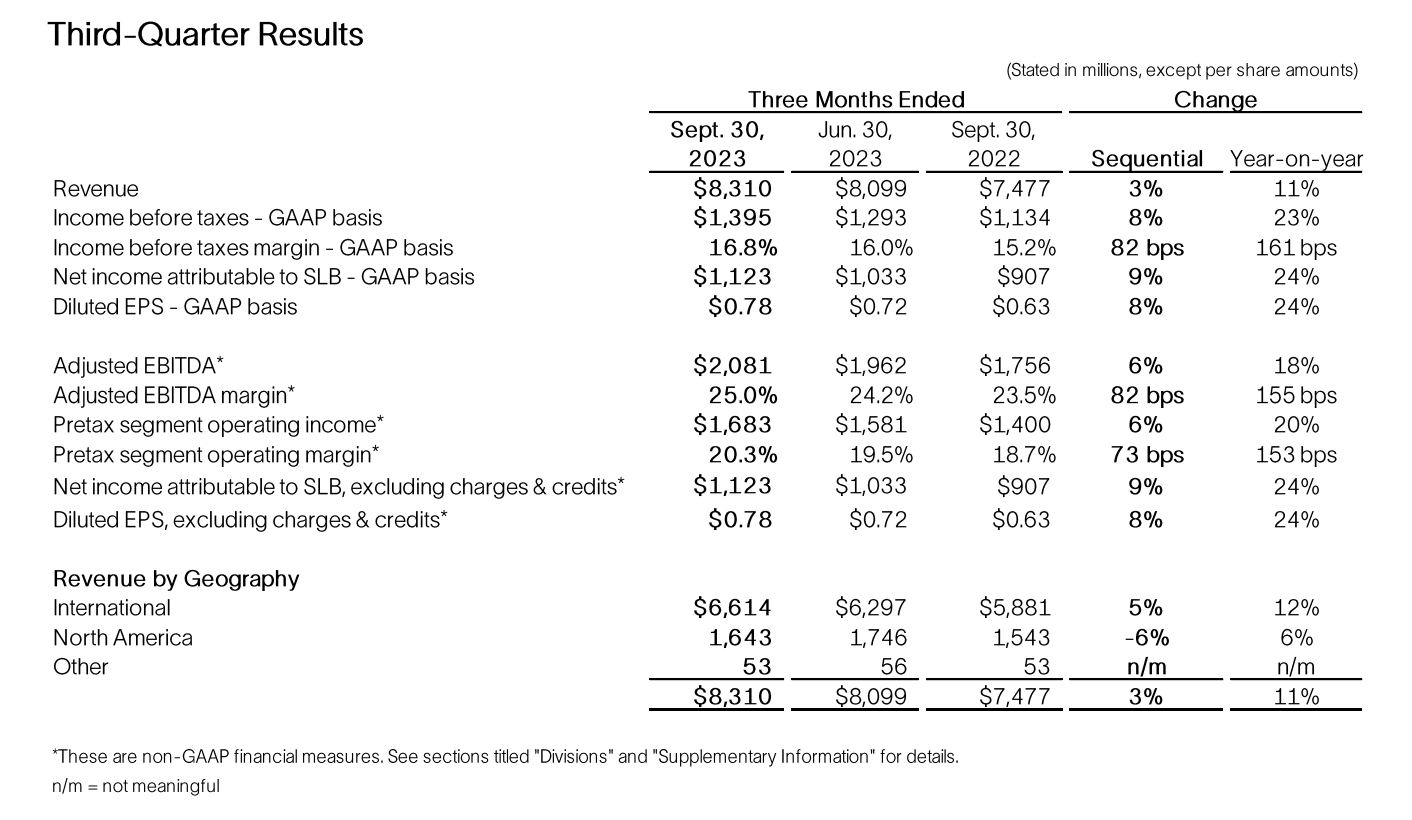

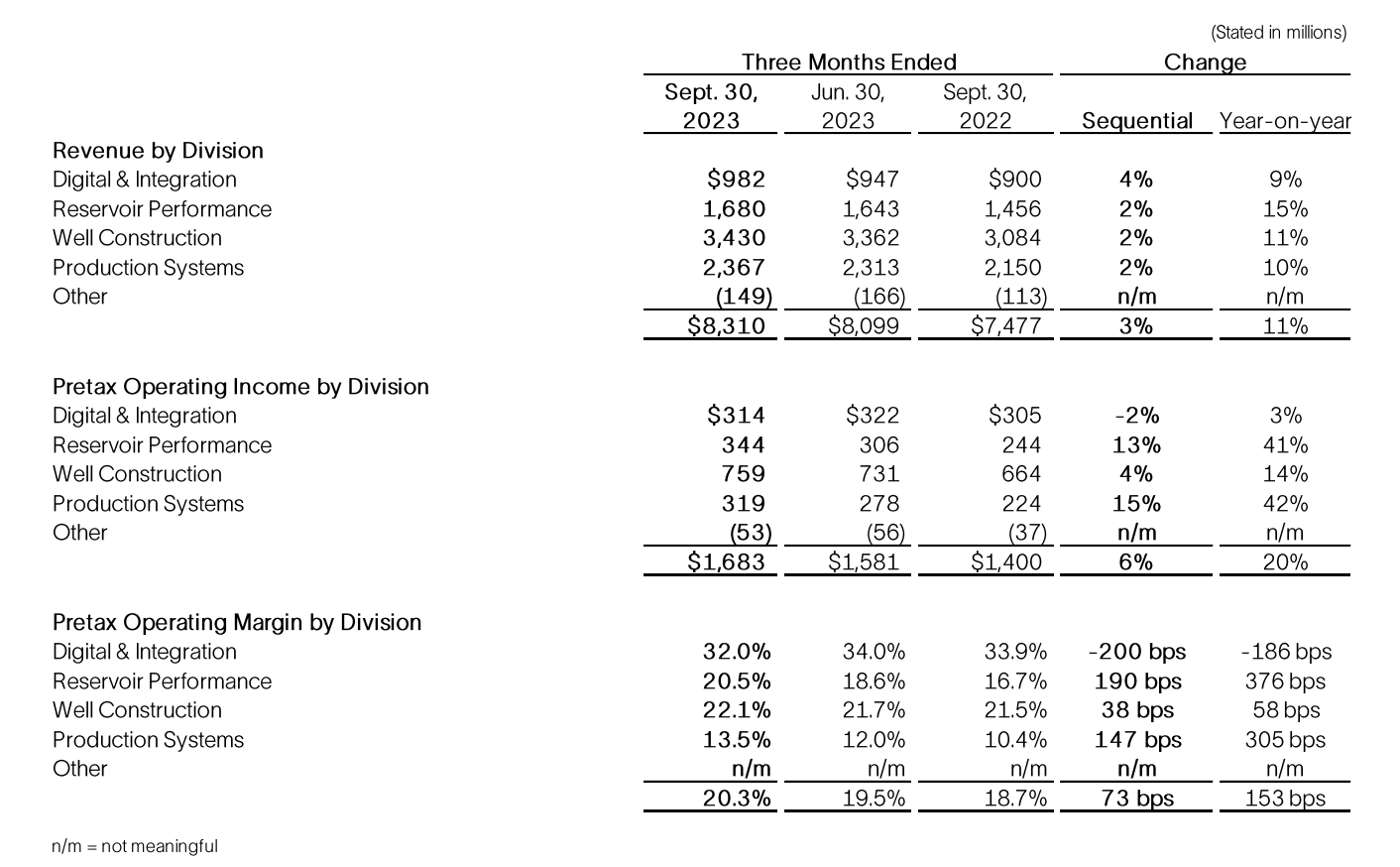

In the third quarter, SLB reported earnings per share of $0.78, showing a sequential increase of $0.06 and a year-on-year increase of $0.15.

Third-quarter revenue was $8.3 billion, reflecting a 3% sequential increase.

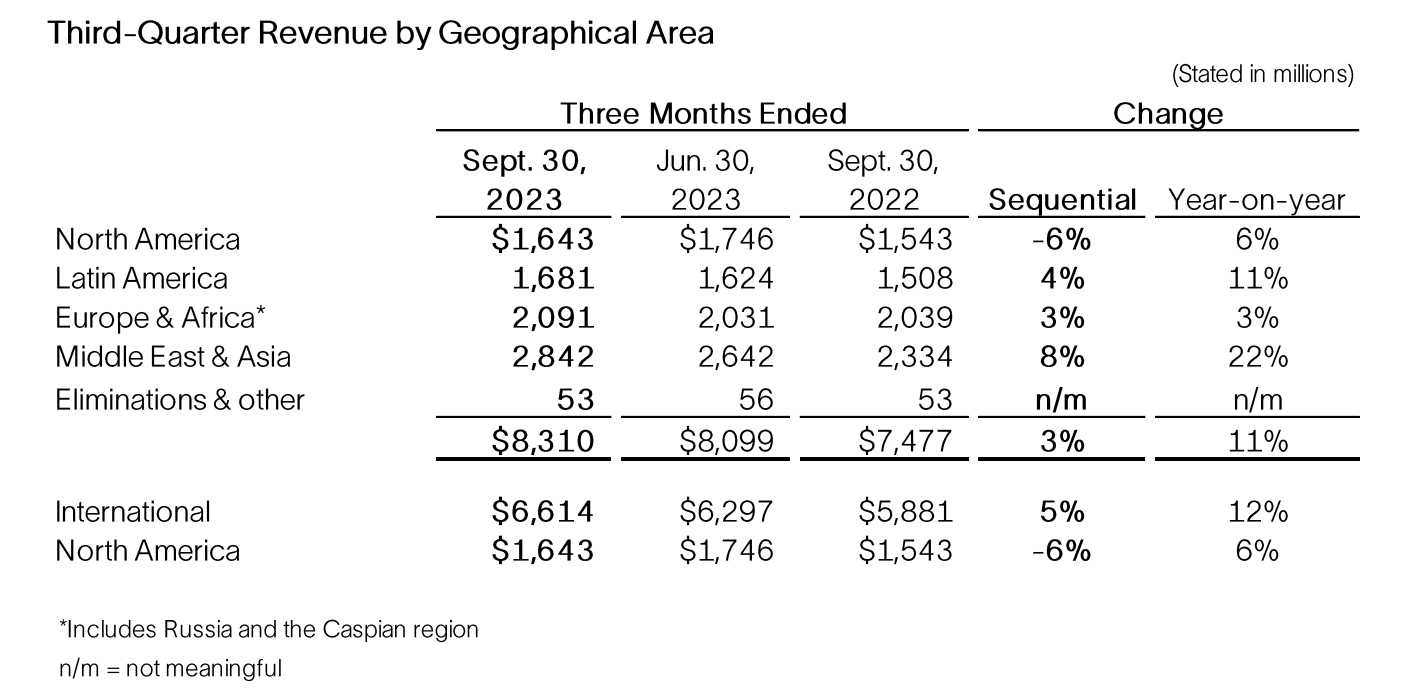

International revenue growth of 5%, led by the Middle East and Asia (8% increase), partially offset by a 6% decrease in North America.

{kind=link}

SLB

According to the company, it has built upon the positive momentum from the first half of the year, achieving sequential and year-on-year growth in both revenue and adjusted EBITDA. Adjusted EBITDA rose by 6% sequentially and 18% year-over-year.

The company-wide adjusted EBITDA margin reached 25%, the highest level since 2015. Year-on-year, third-quarter revenue increased by 11%, with international revenue growing by 12% and North American revenue increasing by 6%.

{kind=link}

SLB

Taking a closer look at the performance per segment, we see strength across the board, with outperforming growth where it matters most.

- Digital and Integration Division : Third-quarter revenue was $982 million, with a 4% sequential increase. Margins decreased by two percentage points to 32% due to lower profitability in APS offsetting improved digital margins.

- Reservoir Performance Division : Revenue was $1.7 billion, up 2% sequentially, with margins improving by 190 basis points to 20.5%. This growth was driven by strong international performance, a favorable technology mix, and improved pricing.

- Production Systems Division : Revenue was $2.4 billion, increasing by 2% sequentially. International revenue increased by 7%, while North American revenue decreased by 8% due to lower subsea activity. Margins expanded by 147 basis points to 13.5%.

{kind=link}

SLB

Furthermore, during the quarter, SLB generated $1.7 billion in cash flow from operations and just over $1 billion in free cash flow, reducing net debt sequentially by $731 million to $9.4 billion.

The net debt to trailing 12-month EBITDA leverage ratio was 1.2x, the lowest level since 2015. The company has an A-rated balance sheet (S&P Global rating).

The company also repurchased 2.6 million shares of stock during the quarter for $151 million and aims to return $2 billion to shareholders in dividends and stock buybacks for the year.

This would translate to 2.5% of its market cap. SLB's dividend currently yields 1.7%.

What's Next?

If you think the prior part was a bit boring, I agree. Essentially, SLB's numbers confirm a gradual recovery in drilling demand, with certain one-off events causing differences between regions.

What matters more is the outlook. That's where it gets exciting - at least for me.

Going forward, SLB expects high single-digit sequential revenue growth in the fourth quarter, with pretax margins remaining at the third-quarter level.

This outlook includes the contribution of the recently acquired Aker Subsea business, which is expected to add roughly $400 to $500 million in incremental revenue in the fourth quarter with pretax operating margins in the low teens.

OneSubsea now comprises SLB’s and Aker Solutions’ subsea businesses, which include an extensive complementary subsea production and processing technology portfolio, world-class manufacturing scale and capacity, access to industry-leading reservoir and digital domain expertise, unique pore-to-process integration capabilities and strengthened R&D capabilities. - SLB

Aker Subsea

Furthermore, what I found fascinating is the company's four (three, as offshore is part of its core business) engines of growth, which I listed below. These tell us a lot about where SLB believes its industry is headed and how it expects to capitalize on it.

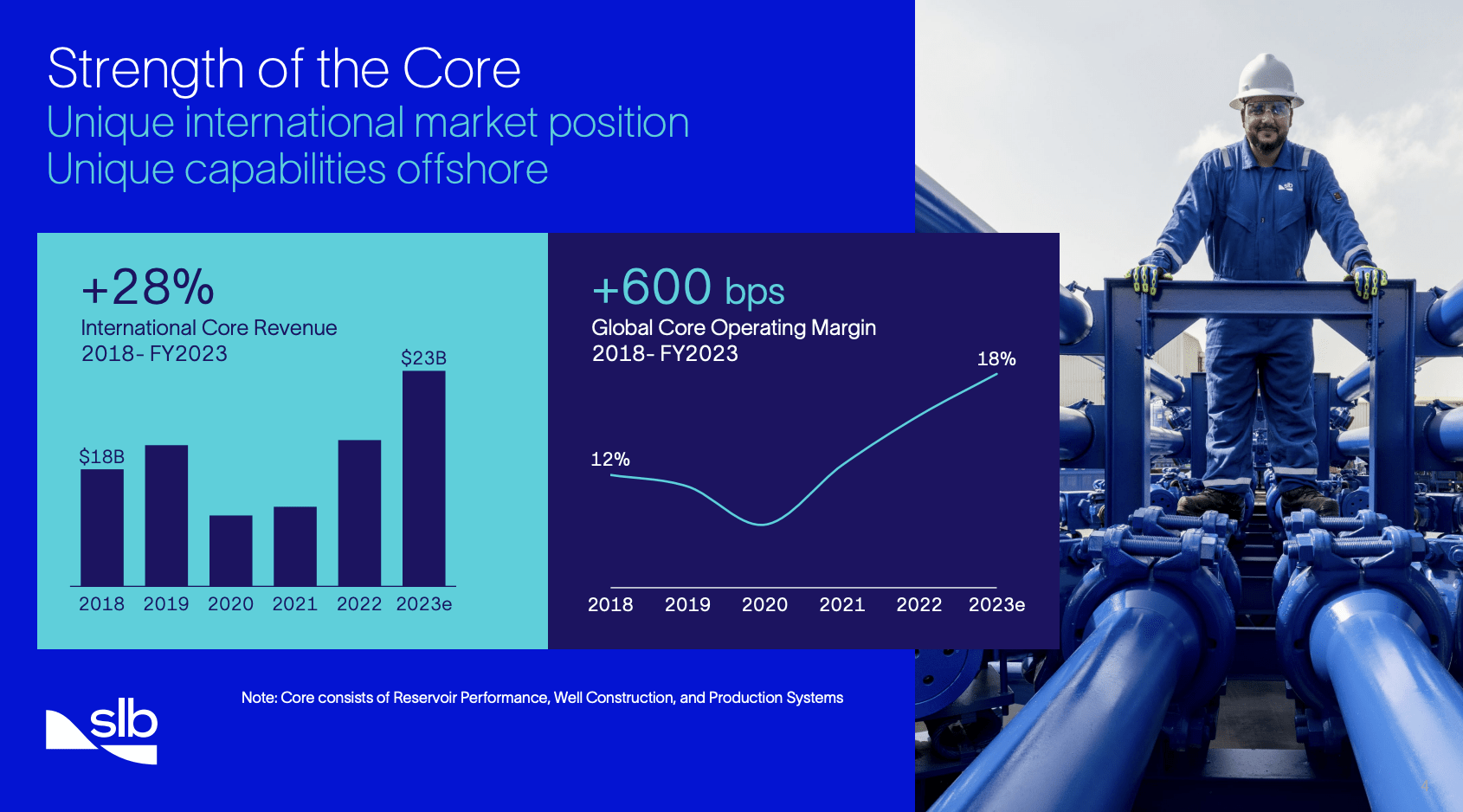

- Core Business: SLB benefits from a durable and resilient material growth cycle in the oil and gas sector, supported by long-cycle developments, production capacity expansions, exploration appraisal, and energy transition. Their core business has grown 22% year-to-date, driven by portfolio diversity, industry-leading technology, and unique integration capabilities. Reservoir Performance, Production Systems, and Construction all achieved exceptional results in this quarter.

{kind=link}

SLB

- Offshore Opportunities: According to the company, there are opportunities in offshore markets, with FIDs (final investment decisions) extending well beyond 2025. The recent OneSubsea joint venture with Aker Solutions and Subsea7 enhances SLB's capabilities in the subsea sector and will likely drive meaningful changes to subsea asset performance.

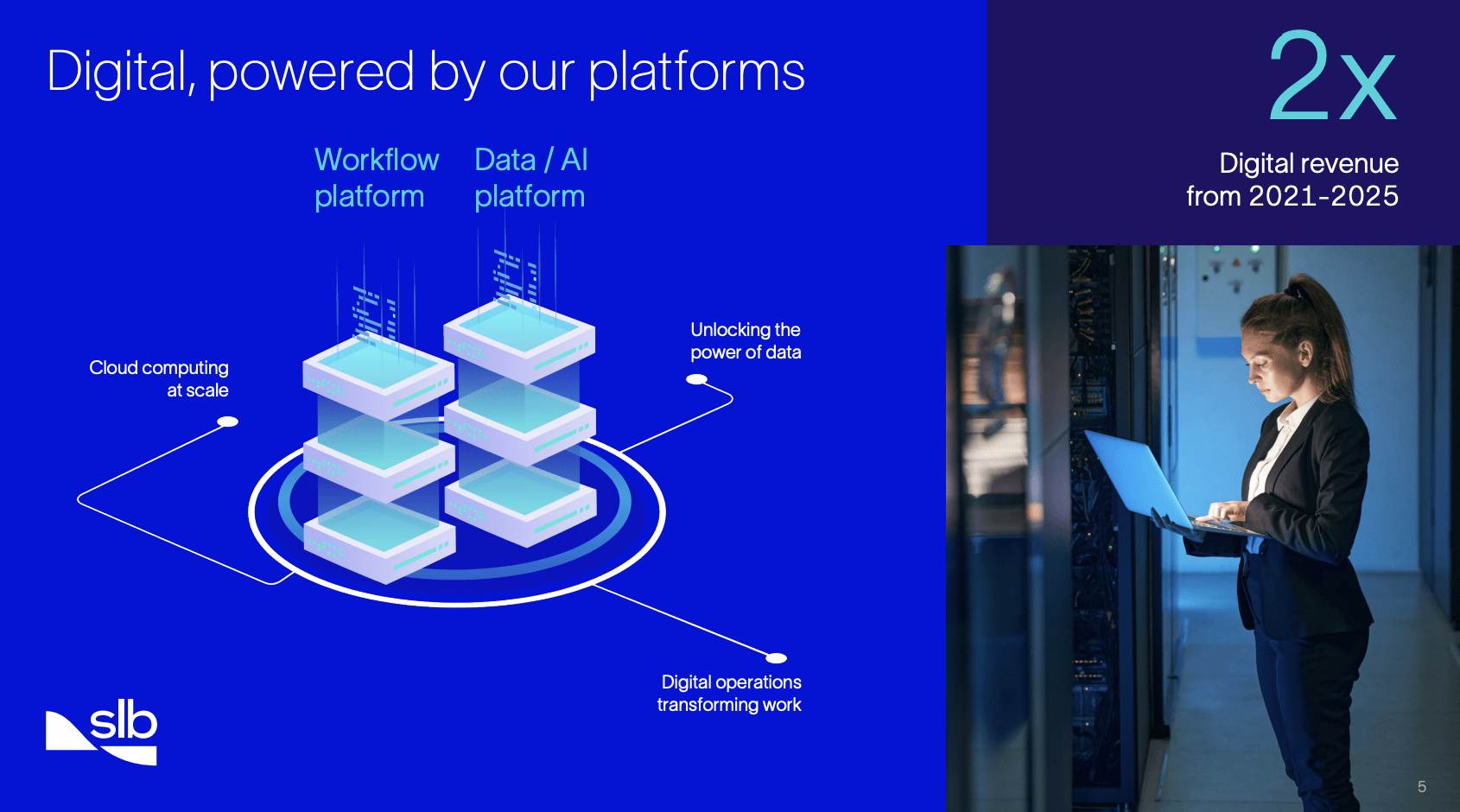

- Digital Growth: SLB is capitalizing on digital trends in the industry, including cloud computing, data, and AI. Delfi, their digital platform, saw significant year-over-year growth in users and compute hours. Customers are adopting connected and autonomous drilling solutions. SLB's digital technology offering is growing at a CAGR of about 60%. Shell-AWS collaborative agreement and the Kuwait Energy Basra Limited digital feed contract are examples of customers choosing SLB's digital technology.

{kind=link}

SLB

- New Energy: As the industry addresses the energy dilemma, SLB is focused on decarbonizing operations by reducing methane emissions and scaling carbon capture, utilization, and storage ("CCUS") solutions. They have launched IoT-enabled methane monitoring solutions and are actively involved in over 20 CCUS projects globally, partnering with TDA Research. SLB is confident that its New Energy business will create a new avenue for diversified long-term growth.

In May, I highlighted the company's environmental capabilities. Its focus on these new trends is also why it changed its name to SLB.

Essentially, the company aims to strike a balance between energy affordability, security, and sustainability by promoting innovation and decarbonization in the oil and gas industry, as well as advancing clean energy solutions. SLB's new identity symbolizes its commitment to addressing current energy needs while leading the way in the energy transition.

In other words, the company seems to be in an increasingly favorable environment, boosted by recovering demand in traditional industries and accelerating demand in renewables and tech-enabled activities.

What does this mean for its valuation?

Valuation

SLB shares are up 4.4% year-to-date, 10% below their 52-week high and 31% above their 52-week low.

FINVIZ

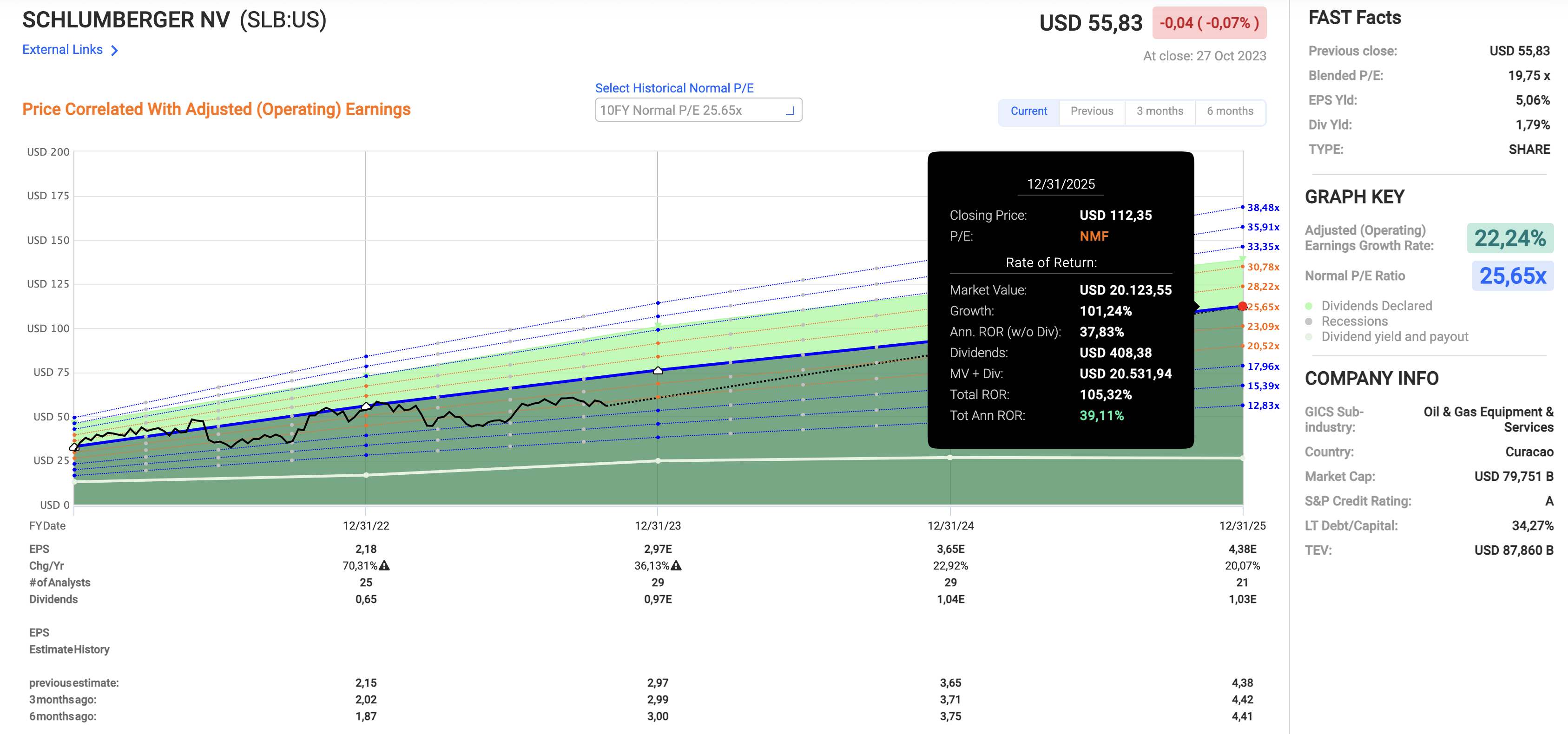

Currently, SLB is trading at a blended P/E ratio of 19.8x. The 10-year average valuation is 25.7x earnings, which includes multiple oil cycles.

- This year, the company is expected to grow EPS by 36%.

- In 2024 and 2025, EPS is expected to grow by 23% and 20%, respectively.

When incorporating expected growth rates and a return to its normal valuation multiple, we get a potential annual return of more than 39% through 2025.

{kind=link}

FAST Graphs

In other words, SLB could double without having to incorporate a nonsensical valuation multiple or abnormal and unrealistic EPS growth expectations.

The current consensus price target is $70, which is 25% above the current price.

The company has received targets as high as $81 in recent weeks, according to my data.

I believe an $80 target is fair. It incorporates growth potential in an economy that is dealing with significant demand risks caused by elevated inflation, elevated rates, and weakening growth in Europe, China, and other regions.

Over the next three to four years, I would not be surprised if SLB's stock price were to double.

Takeaway

SLB's impressive third-quarter performance reflects its ability to thrive in a challenging environment of subdued investments. What's particularly exciting is SLB's forward-looking outlook, with expectations of high single-digit sequential revenue growth and the addition of the Aker Subsea business.

Unless we enter a deep recession, SLB is poised for growth in its core business, offshore opportunities, digital technology, and new energy ventures.

Moreover, the stock's valuation presents a compelling opportunity.

With a current P/E ratio well below its historical average, combined with strong expected earnings growth, SLB could potentially offer substantial longer-term returns.

For further details see:

The Energy Rebound - SLB Seems Way Too Cheap