AAPL - The Fed's Latest Rate Decision: What Should Investors Watch Going Forward?

2023-05-10 07:00:00 ET

Summary

- The Fed raised rates by 25 basis points in its May decision, matching expectations.

- Fed Chair Jerome Powell focused on maintaining tight monetary conditions and provided an inflation assessment contrary to the market's dovish expectations.

- While the market anticipates a pause in rate hikes, Powell avoided committing to it. The summit of rate hikes is apparently shrouded by fog.

- The market expects Fed policy to lead the economy into a recession but notable earnings from the likes of Apple still avoid such assessments.

- As a result, financial markets are in a kind of comfort zone although policy from global central banks provide wildcard outcomes from currency movements.

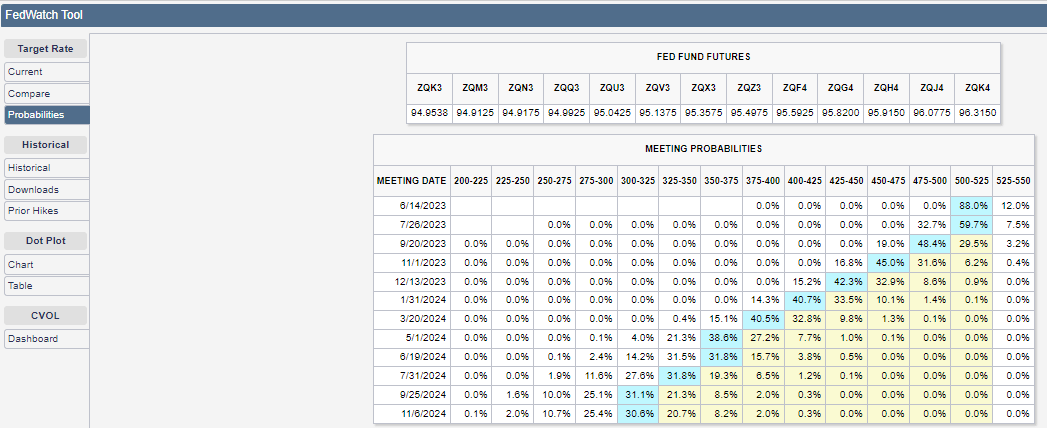

The May decision on monetary policy from the Federal Reserve felt anti-climactic. The Fed raised rates by 25 basis points as expected. Fed Chair Jerome Powell activated the “data dependent”, meeting-to-meeting rule to lay out the plan for the near-term future of monetary policy. He downplayed the potential for lingering economic risks from weakening regional banks. Finally, Powell reminded the audience that inflation remains too high to warrant rate cuts anytime soon, a recurring theme for months that contradicts the dovish expectations expressed in the Fed fund futures . The futures project the first rate cut to come in September.

The blue boxes highlight the most likely outcome for rates according to betting on futures. (CME Fed Watch Tool)

{kind=link}

Powell’s commentary on inflation during Q&A illustrates stubborn hawkishness on inflation even with the current prospect of a pause in rate hikes:

“So we — on the Committee, have a view that inflation is going to come down, not so quickly, but it’ll take some time. And in that world, if that forecast is broadly right, it would not be appropriate to cut rates, and we won’t cut rates. If you have a different forecast and, you know, markets — or have been from time to time pricing in, you know, quite rapid reductions in inflation, you know, we’d factor that in. But that’s not our forecast …if you look at non-housing services, it really, really hasn’t moved much. And it’s quite stable….again, in that world, it wouldn’t be — it wouldn’t be appropriate for us to cut rates.”

In other words, Powell and the Fed remain laser focused on achieving and maintaining tight monetary conditions. They have no interest in climbing the mountain only to turn right back around. They want to enjoy the view from the interest rate summit…and conceptually, they are still not even quite at the top.

In response to a question on whether monetary policy is now sufficiently restrictive, Powell gave a monetary shrug of the shoulders:

“That’s going to be an ongoing assessment. We’re going to need data to accumulate on that. Not an assessment that we’ve made that would mean we think we’ve reached that point. And I just think it’s not possible to say that with confidence now.”

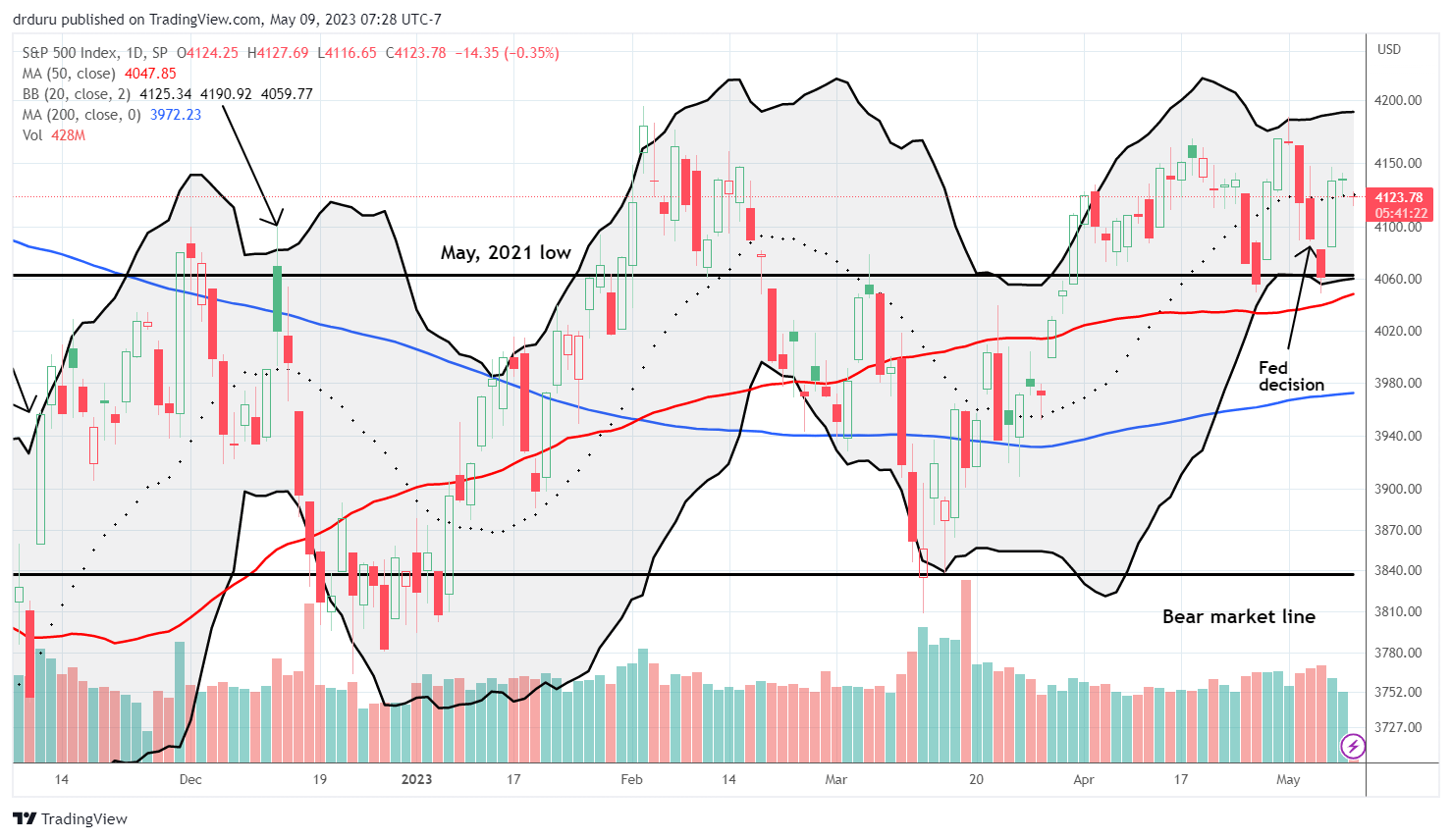

The stock market effectively got nothing that it wanted. So it made sense that the S&P 500 ( SPY ) closed the day lower and selling followed through the next day. If not for the strong reaction to Apple’s earnings results , the index may have come into this week teetering on an important technical breakdown with yet another strong jobs report validating the Fed’s risk management approach to monetary policy.

The S&P 500 is floating above double support from its 50DMA and the September, 2021 low. (TradingView.com)

{kind=link}

Why Did The Fed Raise Rates Again?

A reporter in the audience of the conference call asked a key question on so many minds: “if the whole point of slowing down the pace was to see the effects of your moves, and now you’ve for the last two meetings been seeing the effects of those moves, why did the Committee feel it was necessary to keep moving?” This reporter was referring to the Fed’s earlier reasoning for slowing down the pace of rate hikes. Powell’s response was boilerplate, including this familiar reference to balancing risks:

“We always have to balance the risk of not doing enough and not getting inflation under control against the risk of maybe slowing down economic activity too much. And we thought that this rate hike, along with the meaningful change in our policy statement, was the right way to balance that.”

The subtext to this commentary is that the labor market still gives the Fed room to push rates as high as it dares to reach the summit of restrictive levels. Powell’s introductory comments included a reference to the strength in employment: “The labor market remains very tight….overall, labor demand still substantially exceeds the supply of available workers.” In between those bookends Powell did provide the caveats of a growing participation rate, a decline in job vacancies, and some easing in wage growth. Yet, even taken together these factors were insufficient to dissuade the Fed from hiking again.

The April jobs report released two days after the Fed announcement further reinforced the Fed’s assessment. The unemployment rate went DOWN last month, the participation rate increased, wage growth remained healthy. For a Fed in risk management mode on inflation, these economic data are sufficient to stay the course. The Fed cannot hear the protests of those who, over the past year or so, have dismissed the jobs report as a lagging indicator because the din of inflation machinery just continues buzzing.

A Non-Pause

Powell was very careful to avoid committing to a pause in the rate hikes even as a pause is the most likely next step. The Fed needs its optionality. However, during the Q&A he did point out a key change from the previous statement on monetary policy:

“A decision on a pause was not made today. You will have noticed that, in the statement from March , we had a sentence that said the Committee anticipates that some additional policy firming may be appropriate. That sentence is not in the statement anymore. We took that out and, instead, we’re saying that, in determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account certain factors. So that’s a meaningful change that we’re no longer saying that we anticipate…so we’ll be driven by incoming data meeting by meeting.”

Powell wanted to make sure everyone understands the change was very purposeful. The era of persistent rate hikes has ended. Yet, the Fed is not technically pausing. The summit is still shrouded in fog. If the Fed does indeed keep rates steady in June, Powell may need to double down on the “meeting-to-meeting” rhetoric to cap a potential stock buying euphoria that celebrates the end of rate hikes.

The Central Bank Chorus

The Fed’s peers have taken different approaches to the imminent end of rate hikes. The divergence means the end of the synchronized fight against global inflation, thus increasing the potential for upside inflation surprises somewhere in the world. The wildcard for these effects is the varying paces of quantitative tightening across major central banks.

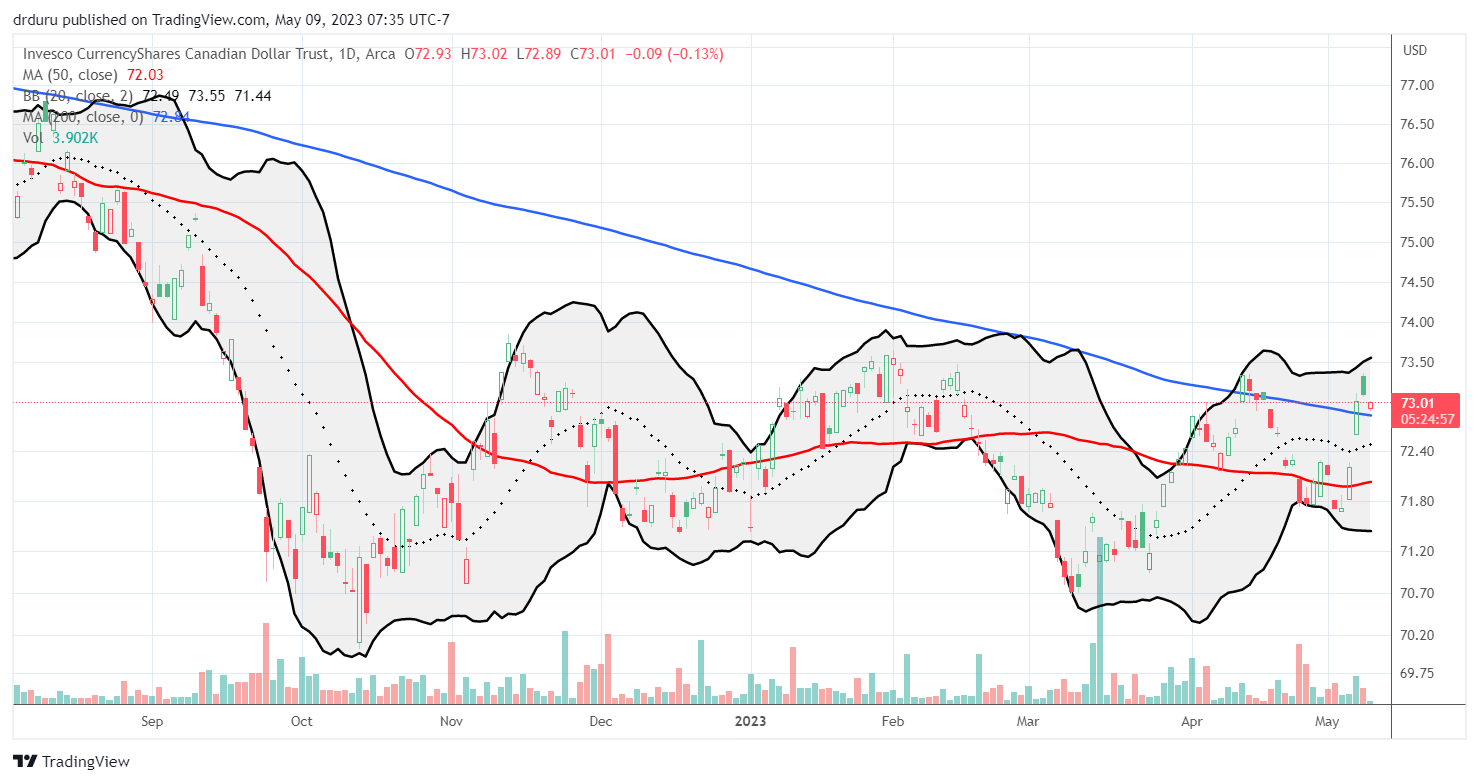

The Bank of Canada ((BOC)) projected a goldilocks scenario with inflation rapidly returning to target without a major economic slowdown. Governor Tim Macklem cited a litany of upside risks to inflation in an effort to dissuade a market that, much like the U.S., expects the Bank of Canada to quickly make a 180 degree turn and start cutting rates. The Bank of Canada announced an official pause in March and is now trying to keep the market on notice that it can hike rates at any time if the data require it : “Governing Council continues to assess whether monetary policy is sufficiently restrictive to relieve price pressures and remains prepared to raise the policy rate further if needed to return inflation to the 2% target.” Interestingly, the Canadian dollar (Invesco CurrencyShares Canadian Dollar Trust ( FXC )) bottomed against the U.S. dollar after the March pause.

The Canadian dollar is at the top of an extended trading range against the U.S. dollar. (TradingView.com)

{kind=link}

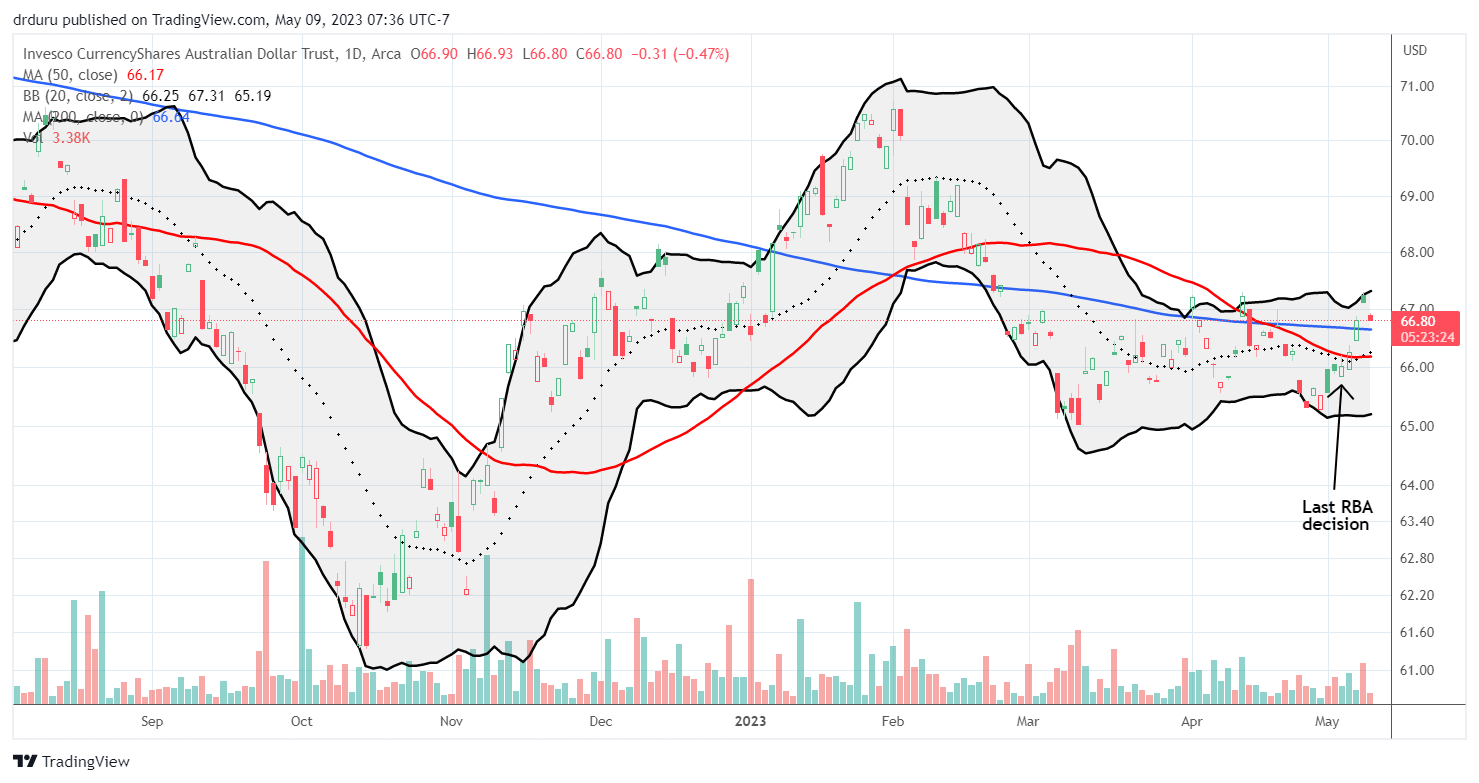

The Reserve Bank of Australia paused and then resumed interest rate hikes . The resumption of rate hikes caught the market completely by surprise. It seems inflation remains a serious problem in Australia, and the RBA did not like the on-going inflation trends after the pause. I think the Fed will be as skittish as the RBA. The Australian dollar, Invesco CurrencyShares Australian Dollar Trust ( FXA ), is still floating higher against the U.S. dollar since the surprise announcement. I expect the Australian dollar to be a major beneficiary of the end of rate hikes in the U.S.

The Australian dollar remains well off its high of the year against the U.S. dollar. (TradingView.com)

{kind=link}

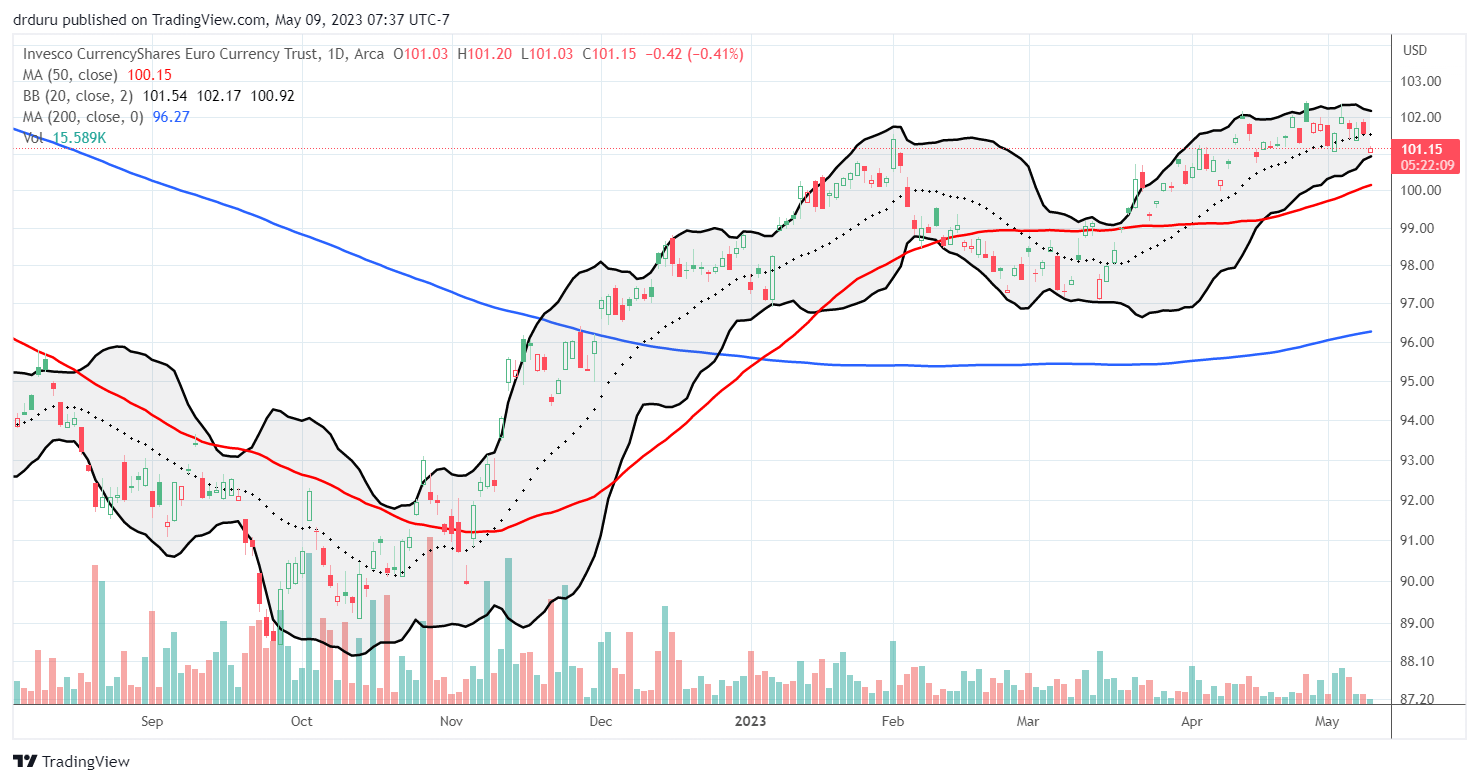

The European Central Bank (ECB) is trying to catch up to the Fed as it points out that “ the inflation outlook continues to be too high for too long .” Similar to the U.S., on-going tightness in the labor market is confounding policy makers. Still, the ECB announced it is slowing the pace of rate hikes; it is not ready to pause. The euro, Invesco CurrencyShares Euro Currency Trust ( FXE ) , is up 15% against the U.S. dollar since the September low. It may have the most to lose of the major currencies after the ECB finally reaches its rate hike summit.

The euro is starting to look a little toppy against the U.S. dollar. A pullback could negatively impact U.S. stocks. (TradingView.com)

{kind=link}

How May The Rate Increase Impact The Economy?

We already know the Fed needs a slowdown in economic activity to achieve its inflation goals. The tightening in credit accompanying the crisis in regional banks will add a drag to the economy. Yet despite consistent predictions of a recession from a host of pundits since the beginning of 2022, the economy is chugging along. The surprising resilience leaves the market to interpret the economy’s prospects through the lenses of the latest major earnings report. Apple Inc ( AAPL ) is a case in point.

The following quote from the Apple earnings conference call symbolizes the conundrum of solid corporate results existing alongside slowing economic conditions (from Seeking Alpha transcripts ) (emphasis mine):

“Moving to Services, we reached a new all-time revenue record of $20.9 billion. And in addition to the all-time records Tim mentioned earlier, we set March quarter records for advertising Apple Care and Video. Despite these records, as we saw in recent quarters, certain services offerings such as digital advertising and mobile gaming continue to be affected by the current macroeconomic environment…

we got the issue around the macroeconomic environment, particularly in advertising and in mobile gaming, but outside of those areas the behavior of customers continues to be pretty consistent .”

Apple sees no recession from its summit.

Apple’s forward guidance further highlights resilient revenue generation despite “macroeconomic headwinds”:

“We expect our June quarter year-over-year revenue performance to be similar to the March quarter, assuming that the macroeconomic outlook does not worsen from what we are projecting today for the current quarter…For Services, we expect our June quarter year-over-year revenue growth to be similar to the March quarter, while continuing to face macroeconomic headwinds in areas such as digital advertising and mobile gaming.”

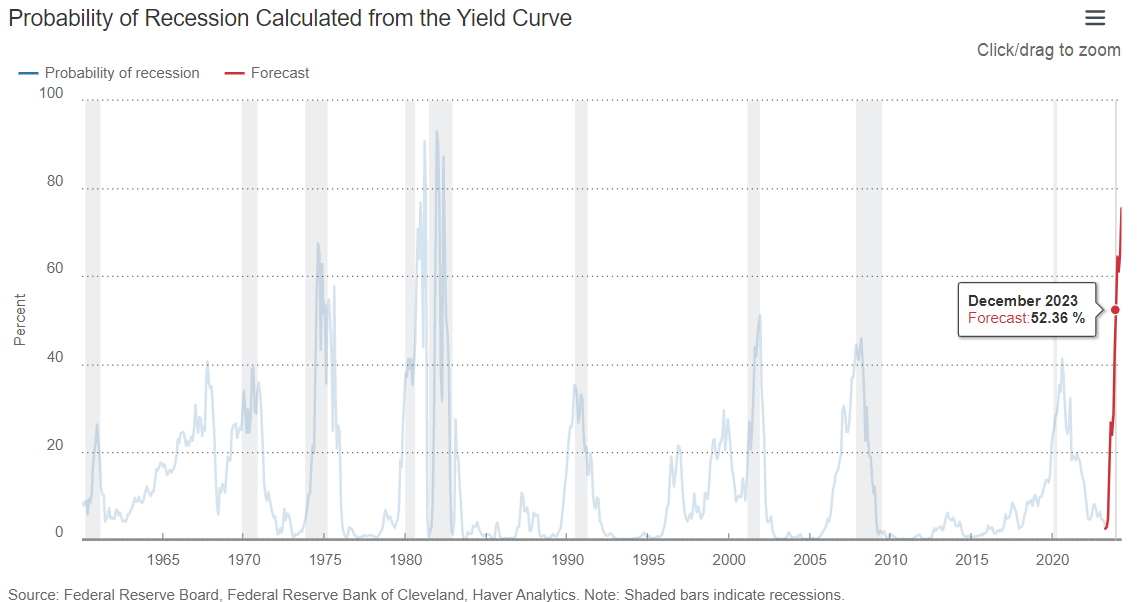

Apple never mentioned or referenced a recession during the conference call. Thus, the impact of the rate increase on the economy is anyone’s guess. The Cleveland Fed’s indicator still has a recession scheduled for December, 2023. The Fed fund futures are thus expecting signs of a recession to be obvious several months before the hit to the economy happens.

The bond market continues to price in a December start for a recession. (Federal Reserve Bank of Cleveland)

{kind=link}

How May The Rate Increase Impact The Stock Market

Given the S&P 500 has been stuck in a trading range for about a year, the impact of rate hikes on trading is not clear beyond the brief trigger-finger reactions to meetings. The October bottom in the index is practically a distant memory. Rate hikes would need to create a sell-off that challenges those lows to create a meaningful impact. AAPL’s post-earnings surge further boosted the S&P 500’s ability to avoid slipping into a retest. Perhaps the Fed is even becoming less relevant at this point in the cycle. Instead, there are plenty of other macroeconomic and geopolitical drivers for the market to worry about (or celebrate) in coming months.

From a technical perspective, the 50-day moving average ((DMA)) is pointing upward and has done so all year. Presumably, this pattern creates an upward bias for the price action. Still, I only see two main potential positive catalysts in the near-term: 1) a broader, permanent guarantee on bank deposits, especially for regional banks, and/or 2) the first rate cut from the Fed (or even a whiff of one). Of course, the first rate cut may be in response to the next economic calamity…so be careful of what you wish for.

Bottom Line

The Federal Reserve has not reached the summit for rate hikes, but the market will act like the summit is here absent strong evidence otherwise. Still, as long as the labor market remains tight, the odds for more rate hikes will be non-zero (10 basis points anyone?). With the market lined up for a steady diet of rate cuts for the last months of the year and beyond, any move the Fed makes to hike rates again could cause a mild pullback. The current pattern of fades of the volatility index ( VIX ) suggest sell-offs will continue to be shallow and brief.

In a kind of circular fashion, each rate hike from here brings the Fed to the doorstop of what must be the imminent end of rate hikes. So the market is likely to insist on predicting imminent rate cuts unless inflation delivers consecutive major upside surprises. The stock market decided to shelve the inflation narrative at the bottom last October. The impact of quantitative easing remains a wildcard.

The tension will continue between those who strain their gaze ahead for the tombstones of inflation and the policy makers still skittish about missing some fresh spark of inflationary pressures. In the middle is a stock market increasingly comfortable with current conditions. Rate hikes are not disturbing this comfort in any material way. Bulls and bears can find opportunity in such conditions: negative surprises will reward intrepid bets against low volatility while plowing the ground for the next dip to buy.

For further details see:

The Fed's Latest Rate Decision: What Should Investors Watch Going Forward?