ASAN - The Lurking Cost Problems At Asana That Keep Us Away

Summary

- Asana is burning through cash to acquire customers.

- The company's costs appear to be growing faster than its top-line revenue.

- We cannot see how the company will succeed in the long run unless it reins in its cost structure.

Thesis

The landscape of enterprise cross-team communication and project management software is crowded. Project managers have a dizzying array of platforms to choose from, monday.com ( MNDY ), ClickUp, Confluence -- the list goes on. Add to that list Asana ( ASAN ), a project management software firm founded and headed by Dustin Moskovitz, a billionaire whose name investors may recognize as one of the co-founders of Facebook ( META ).

Incorporated in 2008 and headquartered in San Francisco, the company offers both free and paid services. Unfortunately, these services come with no discernible competitive moat to speak of, and problematic cost issues that we think should leave investors looking elsewhere.

Revenue Growth?

There's an old saying in the practice of law that goes something like this: "If the law isn't on your side, argue the facts. If the facts aren't on your side, argue the law. If neither are on your side, attack the opposition."

The saying has considerable merit both in the court when crafting a defense and in the market when approaching a company with a critical eye--keeping in mind that management will likely try to put its best foot forward in its presentations is typically a bit of edge investors can use to better assess the state of a company.

In Asana's case, management seems to highlight revenue metrics the most. The company's most recent press release for its FY 2023 Q3 revenues references the word "revenue" 36 times, while the word "profit" makes an appearance only 6 times (and most of these times it is only referring to gross profit).

This helps to point us in the right direction for how to view Asana the way that management views the company--as one that is largely focused on growing revenue and not particularly worried about generating profit (at least for now).

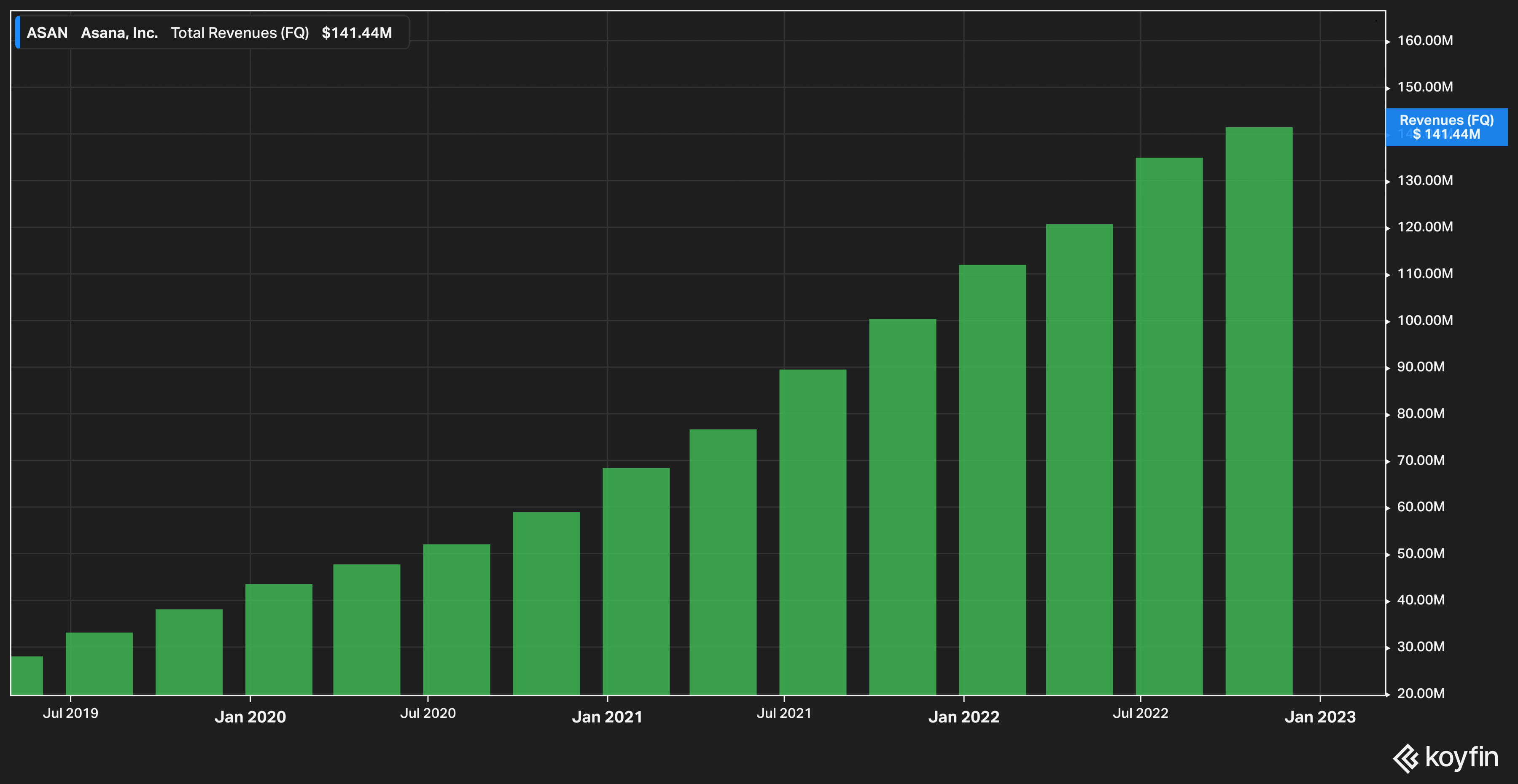

To be sure, generating revenue has not seemed to be the company's problem over the last several years.

{kind=link}

The above chart is indeed a corporate model of revenue growth--consistently up and to the right.

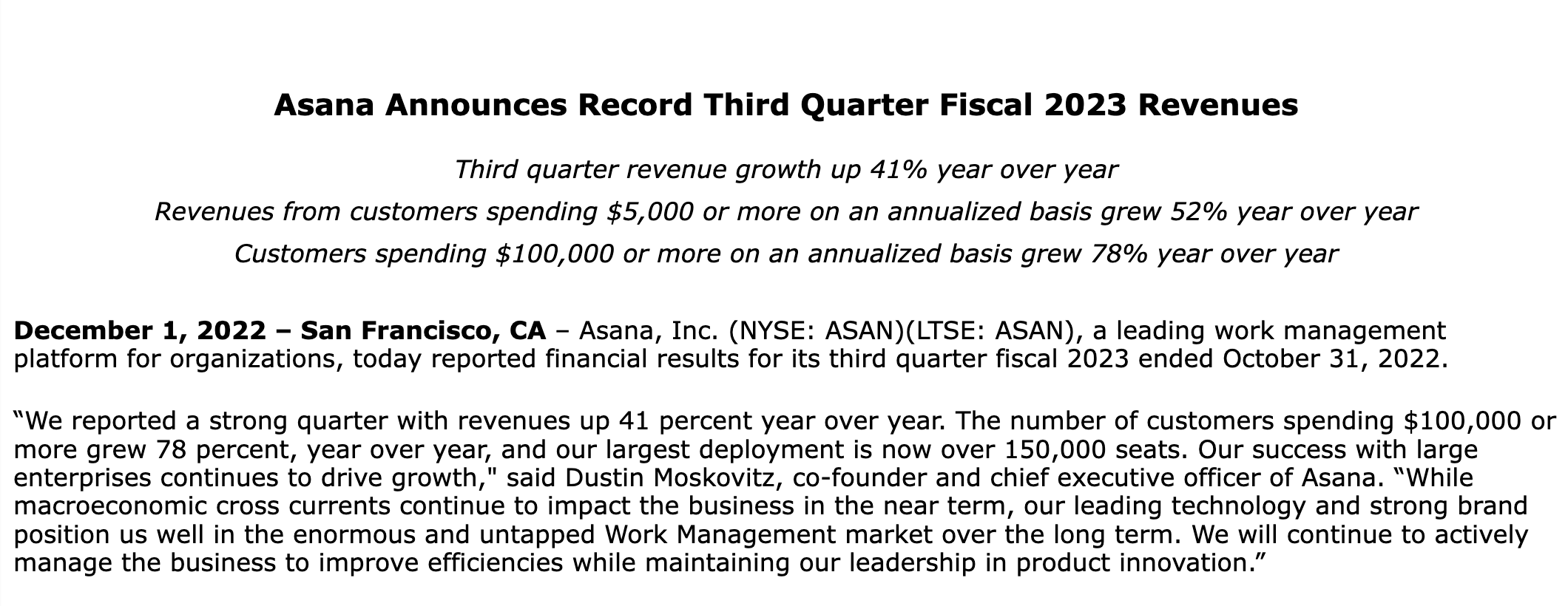

To illustrate this point, observe the headline of the company's most recent earnings press release:

{kind=link}

Naturally, these points highlight what management sees as the best part of the business--one with an expanding customer base and growing revenue. Investors, however, cannot afford to live by the top line alone; everything that comes afterwards matters quite a bit to them.

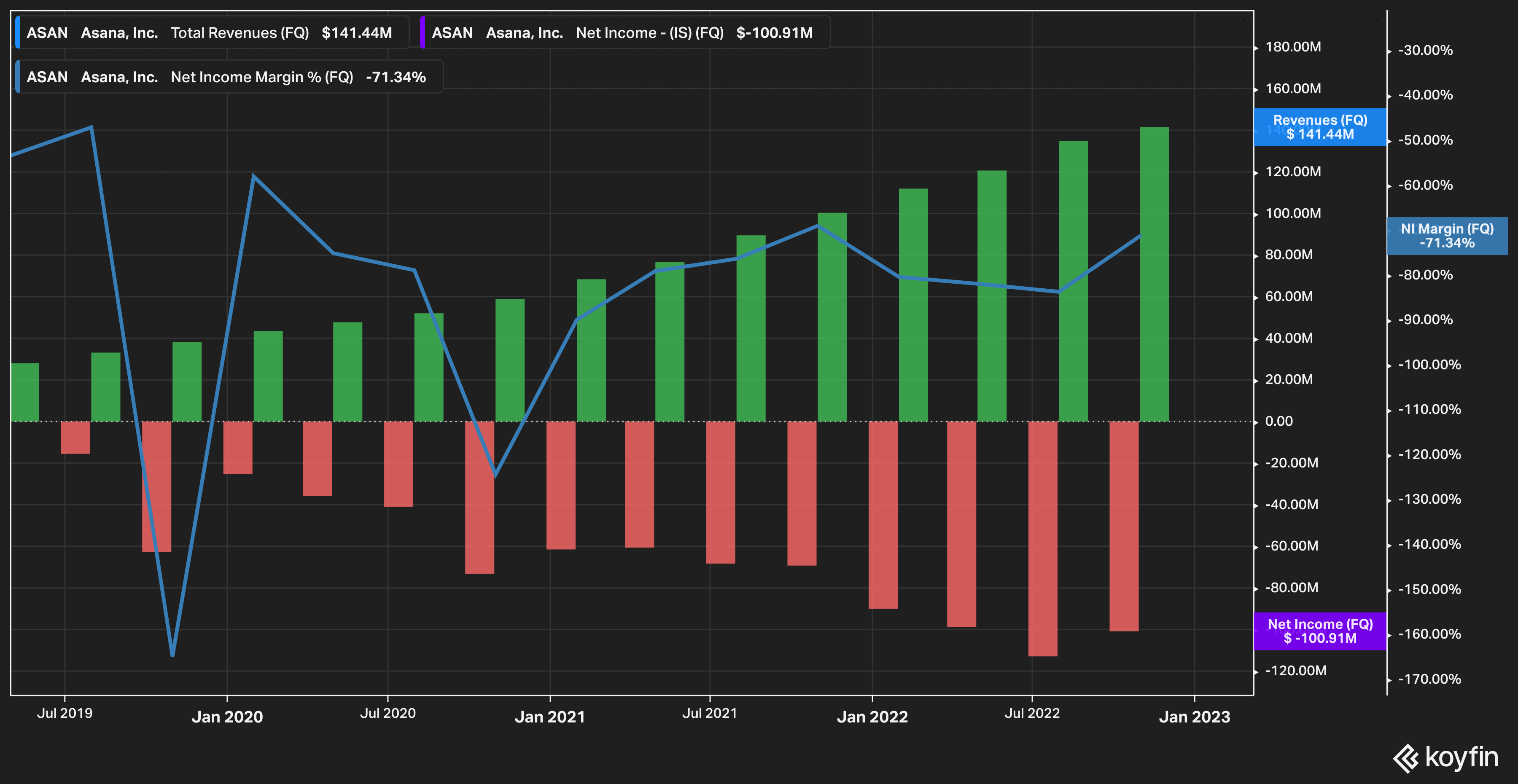

With that in mind, consider Asana's reported net income and net income margin over the same time frame referenced in the first chart in this article.

{kind=link}

Asana's net income losses have grown in near lockstep with revenue since the company's public debut in 2019. Net profit margins, to wit, have remained quite negative, with the latest quarter's net profit margin clocking in at just over -70%.

Cost Growth

Naturally, management has an answer for this. They point out in the most recent earnings release that, "dollar-based net retention rate for customers with $100,000 or more in annualized spend in Q3 was over 140%."

Naturally, this figure is meant to inspire confidence among investors--after all, what else could be concluded from growing business spend from your largest customers? We conclude, however, that the company's spending to acquire new customers is unfortunately outpacing this growth.

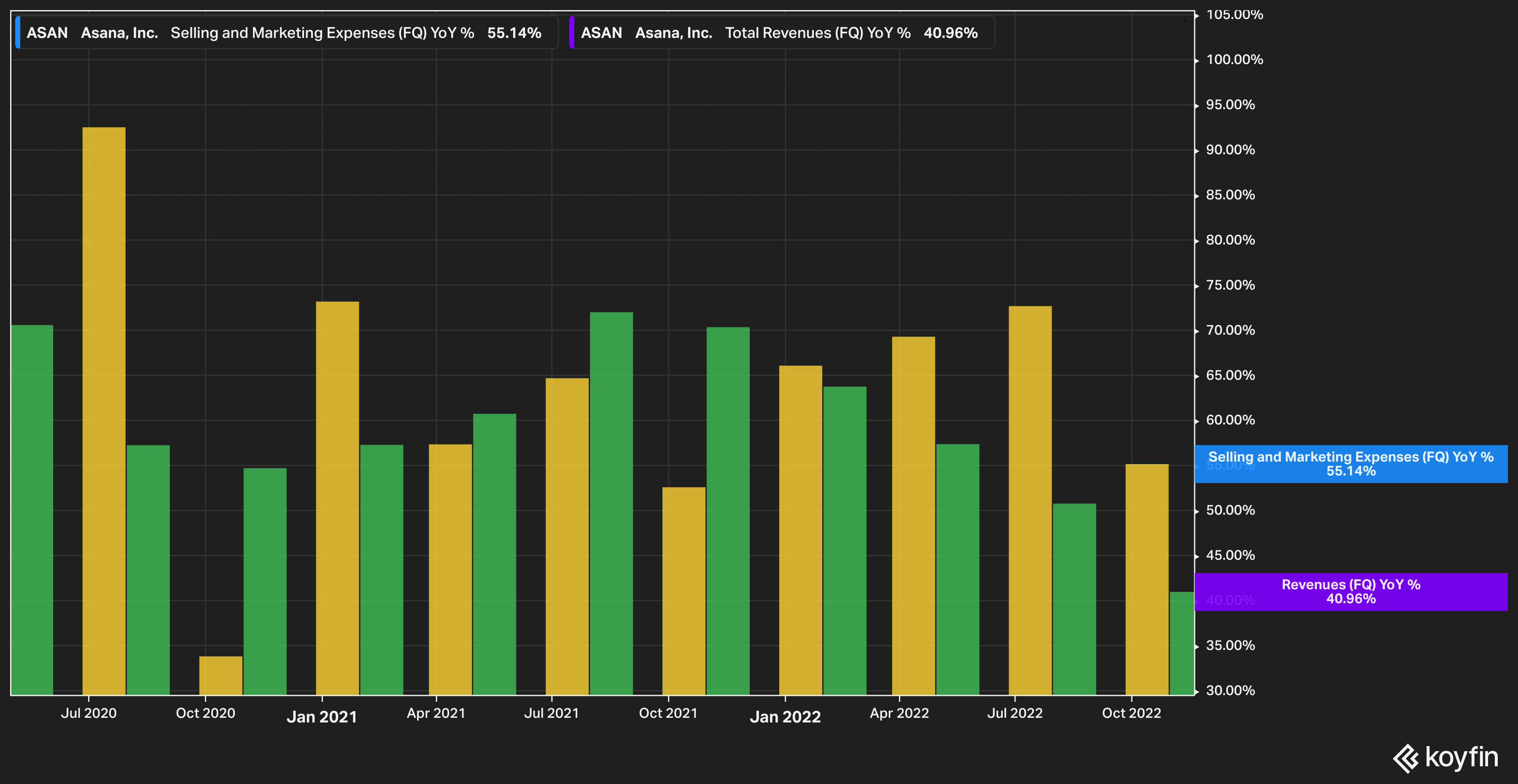

Consider, for a moment, that over the last four quarters Asana's selling and marketing expenses have outpaced revenue growth. This tells us that while the company has been busy touting its customer growth, it has simultaneously cost the company more to bring on each client (otherwise known as customer acquisition cost).

{kind=link}

In the nine months ended October 31st 2022, the company spent $320 million in sales and marketing costs against roughly $396 million in revenues. (And no, we have not excluded stock-based compensation, which was $43 million for the sales and marketing line item, since stock-based compensation directly impacts investor dilution.)

This means that for every $1 of generated revenue for the first nine months of 2022, Asana spent an astounding $0.80 cents in marketing to earn that dollar. It's perhaps no surprise then that, given the enormous expense of onboarding new customers, that the company would have a tough time reducing its margin of net income losses.

Those with a more positive view will counter that the lifetime value of the customer relationship outweighs this expensive upfront price. We would counter with:

- A multi-year timeframe to break even with a customer relationship on a platform that has relatively low switching hurdles is not a great model, and

- we can't be sure exactly what the company's average customer lifetime value is because the company doesn't seem to publish that data.

What we do know from Asana latest press release (click here and view the company's "supplemental information" for Q3, FY 2023) is that as the company expands its customer base, it continues to burn more and more cash. From the company's own recent figures, Asana had 135,000 paying customers. Only 18,700 of those customers paid more than $5,000 per year (just 13% of the paying customer base).

The result of all of this is scaling in the wrong direction--Asana reported negative free cash flow of $48 million on $141 million in revenue. In the previous quarter, free cash flow was a negative $42 million on $134 million in revenue.

The Bottom Line

We are open to the possibility that Asana may truly have best in class software for project and team management--but unfortunately the company's finances and current cost structure keep us away. Combine this with the fact that (even if we assume they operate as the best in their field) Asana is in a no-moat business with excessively high customer acquisition costs, and we must take a pass on the stock today.

For further details see:

The Lurking Cost Problems At Asana That Keep Us Away