TLT - The Near Perfect High-Yield Retirement Portfolio

2023-05-05 08:30:00 ET

Summary

- After prolonged discussions with readers and countless requests, I decided to finally write a retirement-focused article.

- In this article, I present a model portfolio consisting of ETFs that come with high income and stability, which is key when it comes to achieving satisfying long-term returns.

- As individual requirements vary, the ETFs can be viewed as "building blocks" to enhance existing portfolios, depending on income and risk requirements.

Introduction

While I have always received requests to do a retirement-focused article, my recent article covering a potential portfolio for starting investors ended up in so many requests that I couldn't put it off any longer.

Since then, I have collected data and talked to retirees who shared their ideas and strategies with me. In this article, I will present an ETF model portfolio and potential portfolio picks for investors who prioritize income over capital gains.

However, I am still incorporating capital growth, which is achieved by adding dividend growth and (low-volatility) stock market exposure to the portfolio.

Income is enhanced by adding low-risk income vehicles.

Furthermore, my goal was to present a number of ETFs that can be used to improve existing portfolios, as I believe that most retirees already have existing portfolios.

So, without further ado, let's dive into it!

Things To Consider - Including The Initial Investment Volume

I often make the case that covering portfolio ideas is tricky. It's like cooking a five-course meal for a large group of people. Everyone has different tastes, dietary preferences, or even allergies.

When dealing with retired investors, it becomes even more complicated.

Here are a few things that have gone through my mind when I was working on this article:

- Retired investors usually don't start with an empty portfolio . Everyone I talked to had decades of investing experience and built a portfolio that came with high yields on cost. So, presenting a new portfolio idea isn't always the way to go. If anything, investors look for investments to refine their portfolios by making small adjustments. Hence, I also tried to show interesting ETFs in this article that could add value to existing portfolios.

- Discussing the incorporation of dividend growth stocks is tricky . The emphasis here is on growth. I have talked to 90-year-olds who were still buying stocks with high growth. I have also talked to 70-year-olds who only wanted stocks with high yields. The worst part is that this discussion incorporates the fact that we won't live forever. Some people work on big portfolios for their children or grandchildren. Other people told me they aim to spend as much money as possible before they reach an age where enjoying the fruits of their investments becomes harder.

- There are significant differences in required yields . Some people only need a 3% yield to retire. Others need 10-15% to generate enough cash to cover recurring costs and unexpected expenses. After all, some people are very wealthy, while others aren't. Finding a balance is tricky.

- Risk tolerance is an issue. Just like non-retired investors, retired investors aren't equal when it comes to the risks they tolerate. Some want to incorporate at least 40% bonds into their portfolio (like the 60/40 portfolio), while others buy loads of high-risk investments like mortgage REITs.

- As most of my regular readers know, investments with high yields (like >10% yields) make me extremely nervous . More often than not, these yields come with tremendous risks and a total return picture that barely defeats inflation. The chart below shows the long-term total return of mortgage REITs, which is absolutely terrible. However, for some, it works as an income vehicle. In this article, I incorporated high yields that, I believe, come with a decent risk reward.

Related to the list above, how much cash do we need to retire? If you sit on a $5 million nest egg, you will be able to retire in every major city of the world without having to take significant financial risks like buying 10%-yielding investments.

{kind=link}

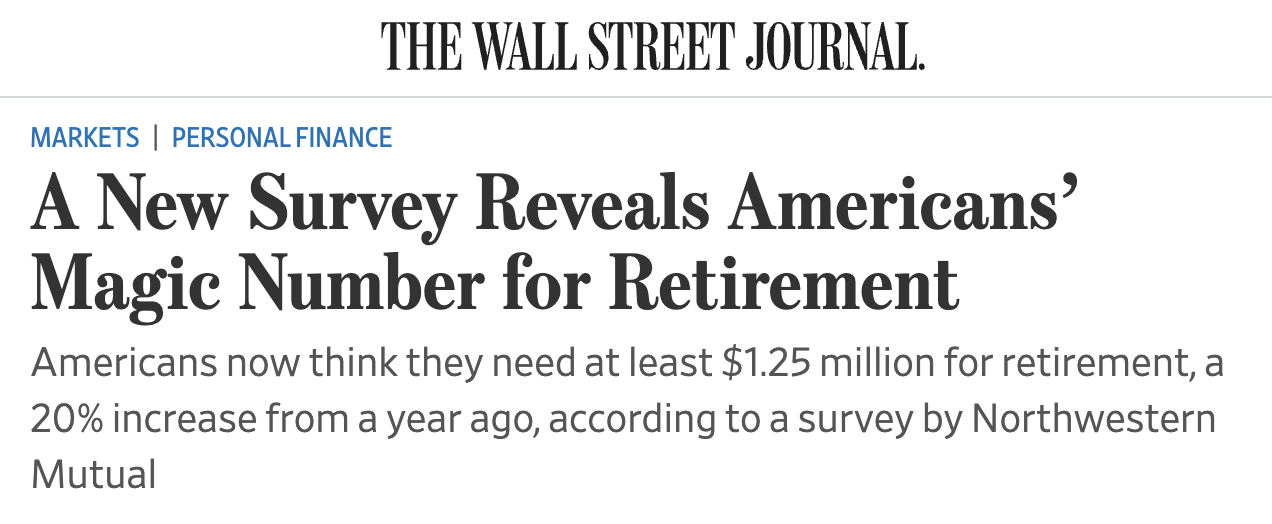

According to a Wall Street Journal report from 2022 (which is still valid), Americans believe their household needs at least $1.25 million to retire COMFORTABLY. Please note that I wrote "comfortably" in all caps. After all, we can all aggressively cut costs. However, that would often lead to a reduction in the quality of life, and that's not what retirement should be about.

Unfortunately, but not unexpectedly, Americans are far from reaching these goals.

According to the journal (emphasis added):

While Americans say they will need more money after they retire, the average amount in a retirement savings account has dropped this year to $86,869 , an 11% decline from 2021, the survey said.

The expected retirement age also ticked up to 64 years of age , compared with 62.6 last year.

[...] The survey, which polled 2,381 American adults in February, comes as consumers have been squeezed by rising inflation . That has put pressure on their spending power and their ability to save.

[...] About one in four people said they now plan to retire later because of the pandemic , the survey said. Of those who are putting off retirement, 59% said they wanted to work more to save money. And 45% said they were worried about rising healthcare costs or had unexpected medical costs.

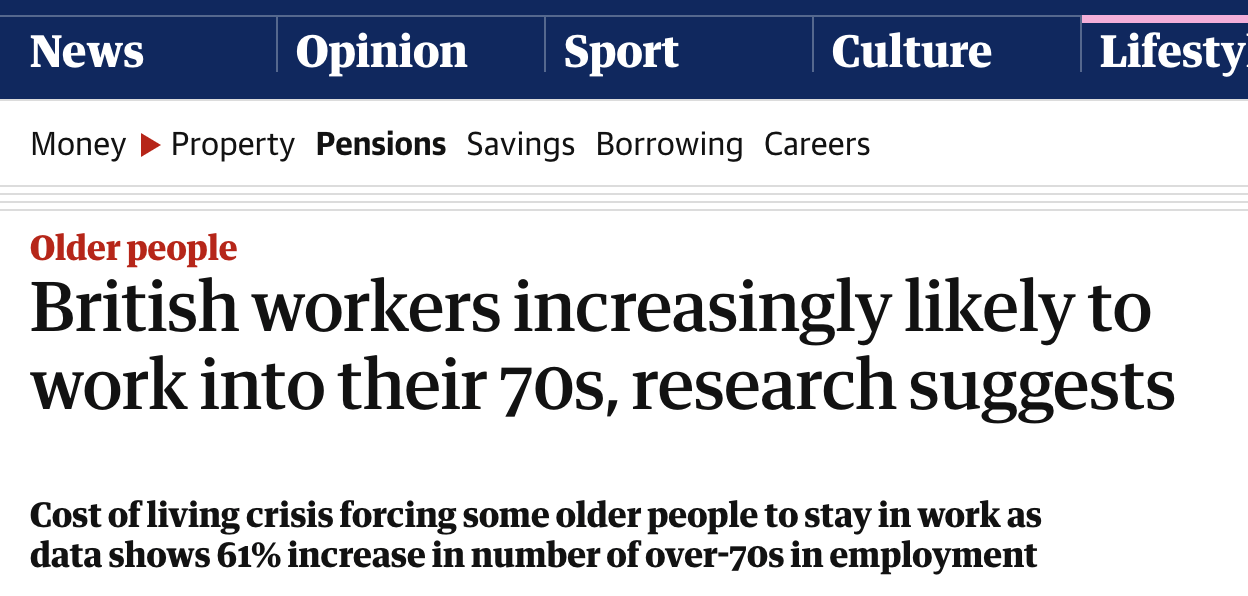

Please note that although the pandemic is over, I still kept in the last part of the quote above, as high inflation is still keeping older people in the workforce.

The screenshot below shows a recent headline from The Guardian , which shows the dire situation among older workers in Great Britain.

{kind=link}

Hence, I incorporated a number of factors in my portfolio (picks):

- Assets with high yields that boost the income component of the portfolio.

- Stocks that combine income and growth, as I wanted to incorporate a growth component. Needless to say, these stocks also come with a high yield to keep the average yield elevated.

- A low-volatility component with a high correlation to the stock market. This is growth-focused without exposing retirees to high volatility that could make it hard to liquidate assets whenever necessary.

- I constructed a portfolio that comes with a terrific risk/reward when dividends are reinvested and a decent return when all dividends are consumed.

- All picks are ETFs, as this takes away the component of stock picking (lower risks). After all, when retired, investors should focus on the things they enjoy instead of tracking their portfolio on a daily basis. That said, I will do a stock-focused article if readers are interested .

Now, let's assess the picks.

The Perfect Portfolio For Retirement?

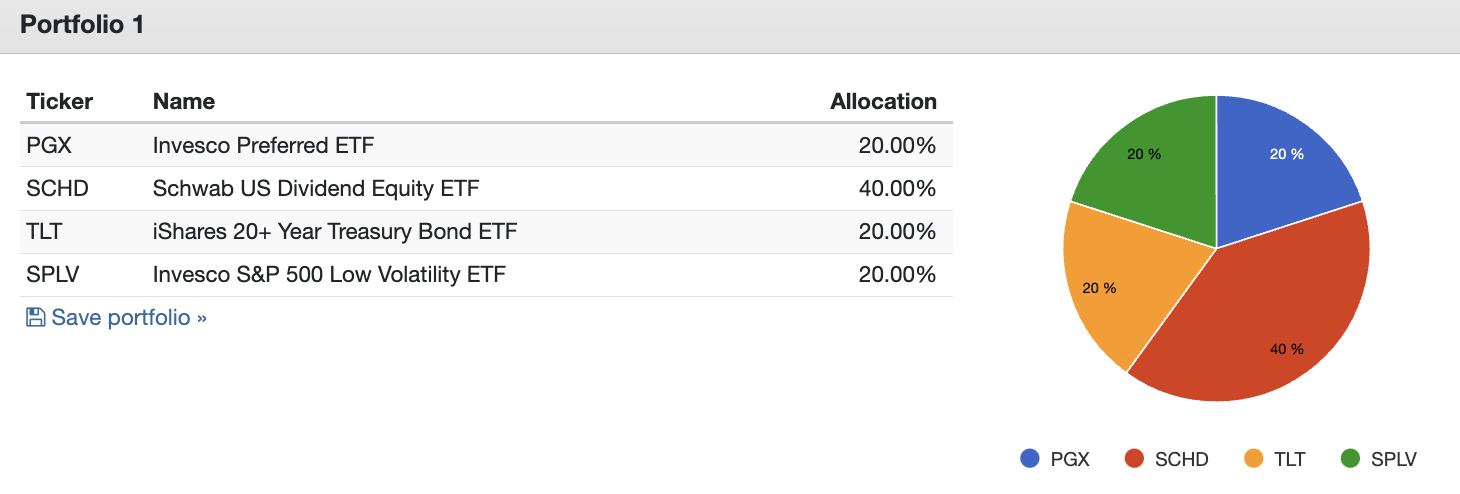

The first portfolio idea I came up with is a mix of four ETFs that each have unique characteristics.

{kind=link}

Please note that I excluded one major income ETF from this ETF, as it hasn't been stock listed very long. It would prevent me from backtesting this idea. However, I am including that ETF later in this article, as I believe it's a cornerstone of a successful retirement (income) portfolio.

Schwab US Dividend Equity ETF ( SCHD )

The core of my portfolio is the Schwab high-yield ETF. If I had picked single stocks for this portfolio, I'm sure most of them would have been a part of this ETF. In March, I wrote an article discussing the details of this ETF and my expectations that it will outperform the market on a prolonged basis.

With an expense ratio of 0.06%, this passive ETF tracks the Dow Jones Dividend 100 Index. It has 104 total holdings with a yield of 3.6% .

On a total return basis, SCHD was able to keep up with the market over the past ten years.

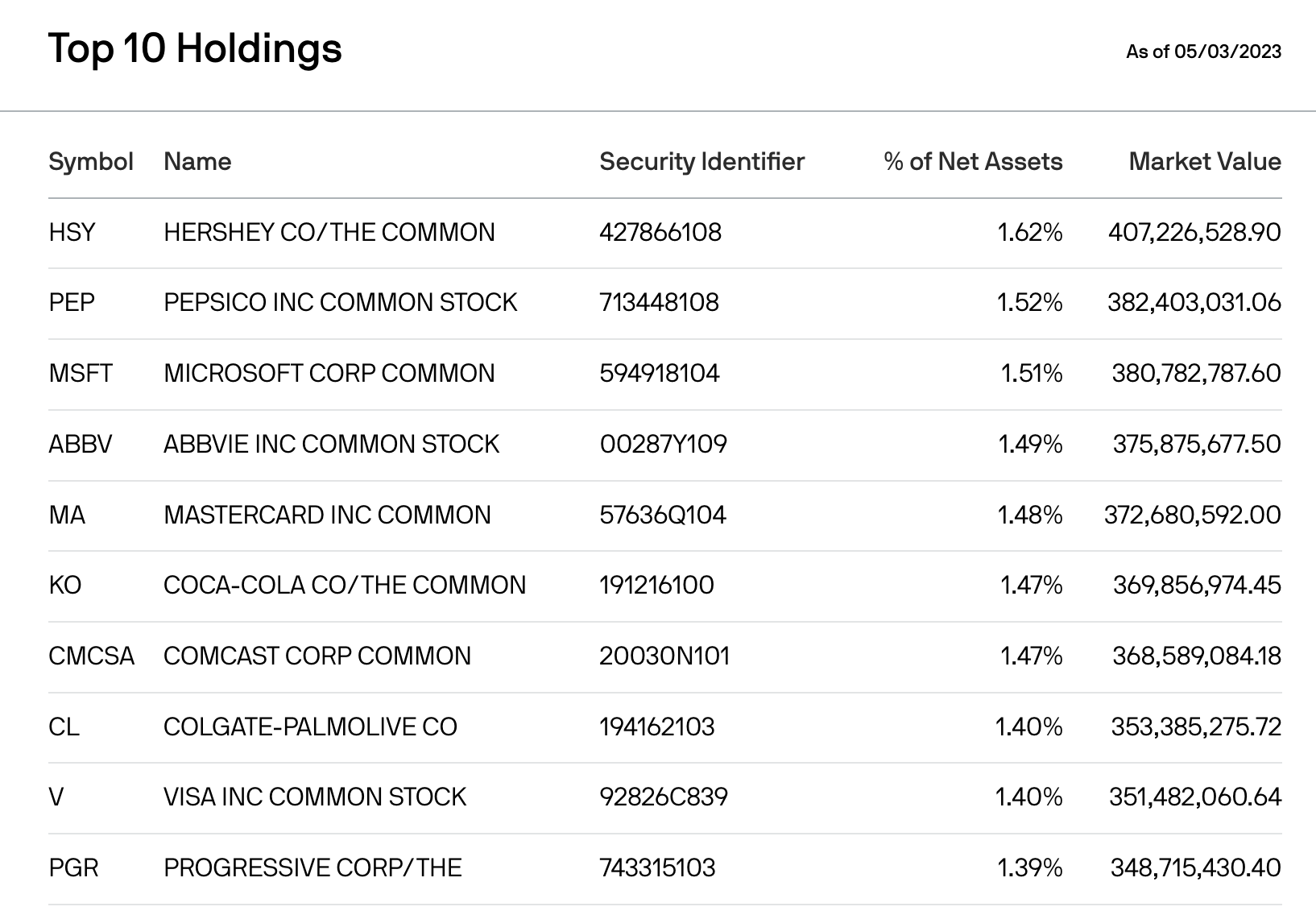

Roughly 70% of its holdings have a market cap of more than $70 billion. Its top 10 holdings consist of some of the most well-known and trusted dividend stocks on the market.

18% of its holdings are industrials, 16% are healthcare companies, 14% are financials, and 13% are consumer staples. In other words, this ETF is underweight growth (like tech) and focused on no-nonsense companies that come with decent yields and consistent dividend growth.

These are its top 10 holdings.

{kind=link}

Furthermore, the average annual dividend growth over the past ten years was 11.7% , which is truly impressive. Over the past three years, that number was 13.3%.

Invesco Preferred ETF ( PGX )

This is the part where I add juice to the portfolio. The Invesco Preferred ETF is a fund that is based on the ICE BofAML Core Plus Fixed Rate Preferred Securities Index. This fund aims to invest at least 80% of its total assets in US dollar-denominated preferred securities that are included in the index. The index tracks the performance of fixed-rate US dollar-denominated preferred securities that are issued in the US domestic market and are rated at least B3 by Moody's, S&P, and Fitch.

These securities must also have an investment-grade country risk profile based on the foreign currency long-term sovereign debt ratings of Moody's, S&P, and Fitch.

This ETF has a yield of 6.4% and a management fee of 0.50%. That may seem like a lot. However, it's decent compared to what other providers are charging, often with lower-quality holdings.

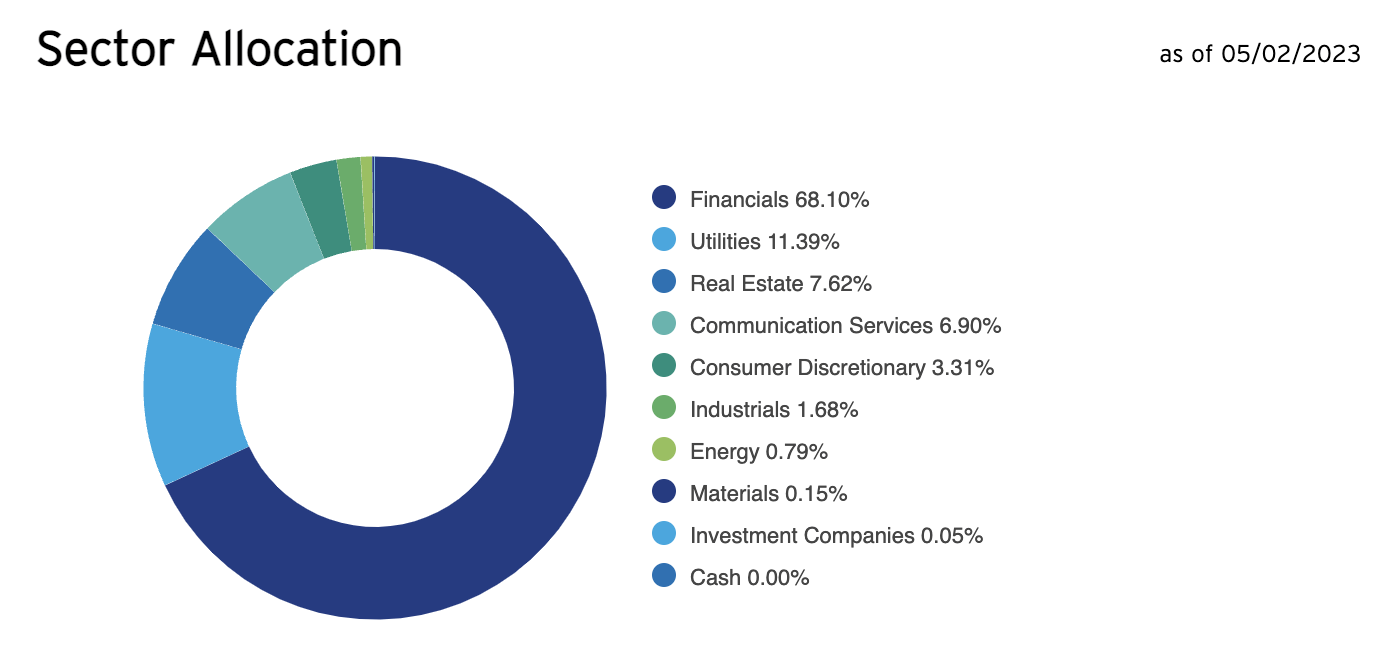

This ETF has 274 holdings. Almost 70% of its holdings are financials, followed by utilities and real estate.

{kind=link}

61% of portfolio holdings have a BBB rating. 1% of holdings have an A rating. 30% of holdings have a BB rating.

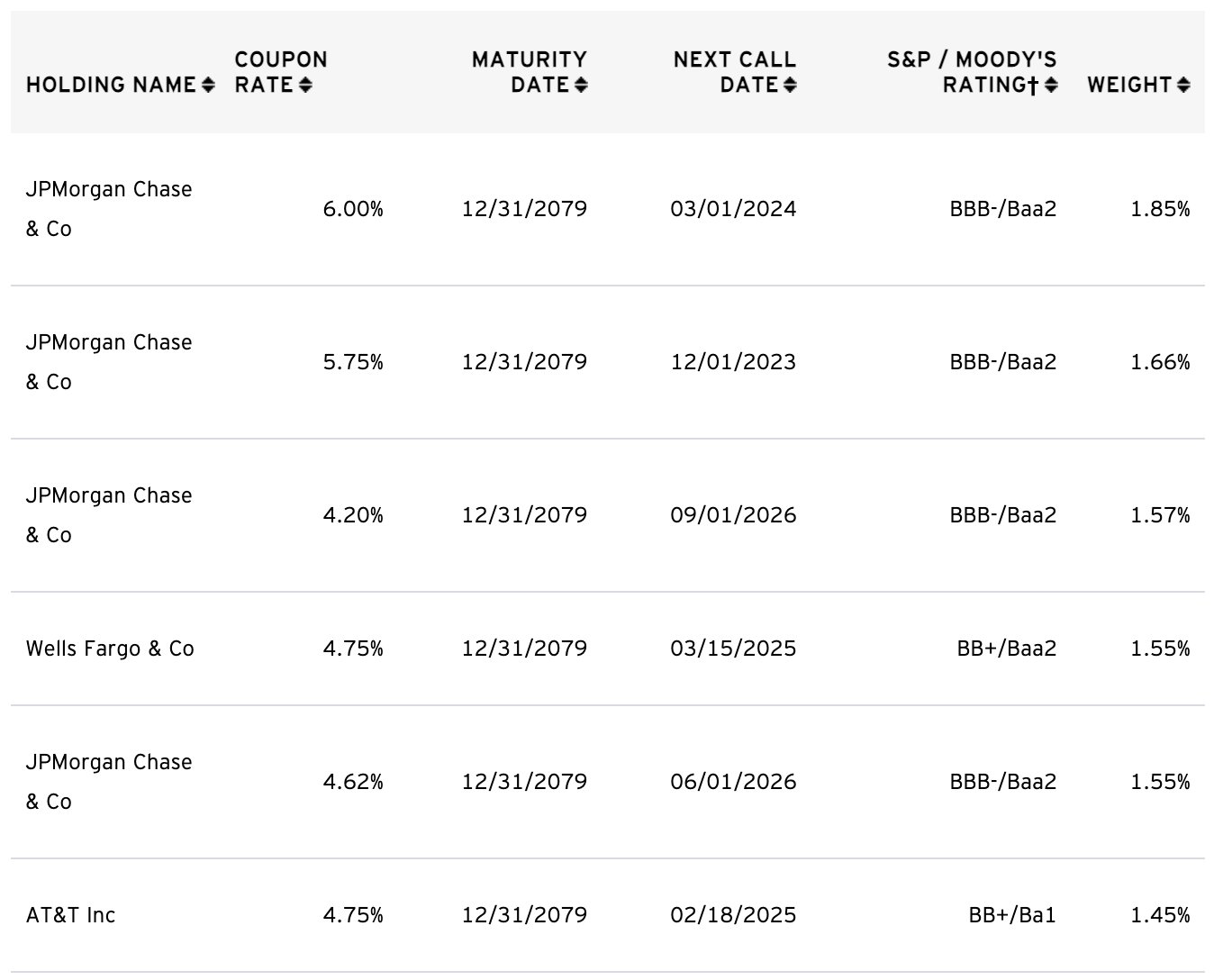

Below is an overview of its top holdings. The weighting is low (due to diversification), but it shows the type of holdings investors are dealing with.

{kind=link}

Over the past ten years, PGX returned 31%, which is down from roughly 60% in early 2022, when higher rates pressured bonds and related fixed-rate investments. What's interesting is that prior to 2022, this ETF held up very well, even on a non-total return basis, meaning if dividends had been consumed.

PGX is a high-yield vehicle, a good one at that. I prefer PGX over most individual stocks and instruments with similar yields. PGX has good diversification and tends to do rather well in normal circumstances. However, investors should not expect strong outperformance. It's an income vehicle, not an investment vehicle with a total return capable of making investors rich.

The other two picks are mainly to provide stability.

Long-Term Government Bonds & Low Volatility Stocks

A large majority of people in my comment sections hold long-term investments that come with growth. While we already incorporated that by adding the SCHD ETF, there are other ways to add value to a long-term retirement portfolio. One way is adding the Invesco S&P 500 Low Volatility ETF ( SPLV ) . This ETF has a yield of 2.2% and tracks the 100 S&P 500 securities with the lowest realized volatility over the past 12 months. Its expense ratio is 0.25%.

Why did I pick this ETF? While this ETF is also prone to corrections and steeper sell-offs, it brings stability to a portfolio. It tracks the S&P 500 with a lower likelihood of steep sell-offs. Especially during retirement, investors might need to sell assets for a variety of reasons. Owning volatile investments might force investors to sell during corrections (at unfavorable valuations). Hence, investments with minimal volatility are key.

On top of that, minimal volatility is a great way to create long-term wealth, something retired investors are still keen on doing. Downside protection is a big part of long-term success. Even if low-volatility stocks don't always outperform during bull markets, they come with a high (expected) total return if the market does well.

Since the Great Financial Crisis, SPLV has returned 240%. This is below the S&P 500 performance. However, it came with much less volatility.

The chart below shows a comparison between the low-volatility S&P 500 and the S&P 500 30-day rolling volatility. Especially during the most recent bear market, low-volatility stocks have fared much better than the market.

The other holding to add stability is the iShares 20+ Year Treasury Bond ETF ( TLT ) , also known as the long bond.

As the name already suggests, this ETF provides exposure to treasuries with long maturities. 98% of fund holdings are invested in 20+ year bonds. The average credit quality is AAA, which is the credit rating of the United States. The expense ratio is 0.15%. The yield is 2.6% .

Unfortunately, just like the PGX ETF, TLT has suffered tremendously due to higher rates and high inflation. The 10-year total return has dropped to 12%.

While this performance has negatively impacted the total return of the portfolio, I'm about to show you why I believe that TLT offers buying opportunities.

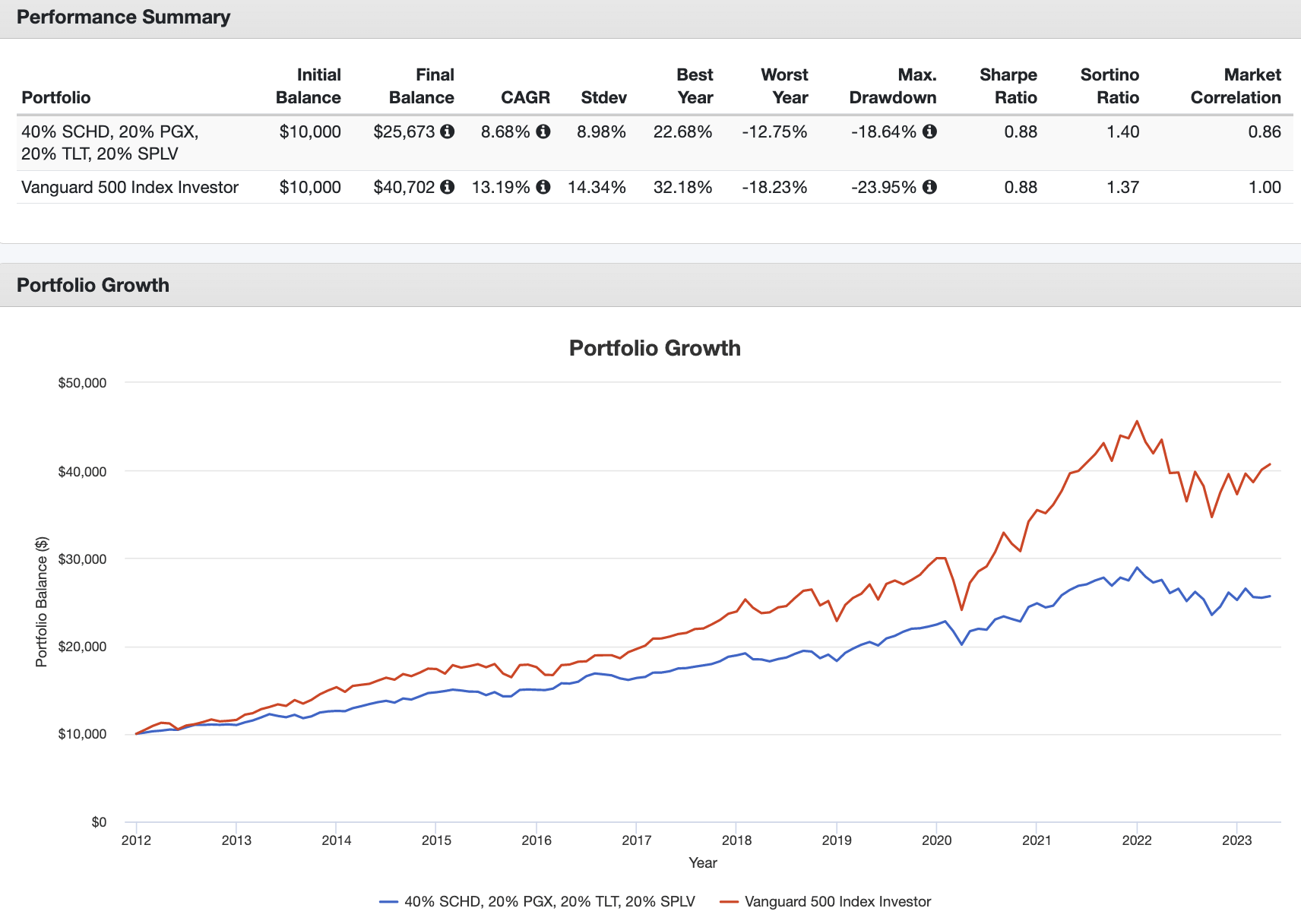

Portfolio Performance

If we assume a portfolio consisting of 40% SCHD, 20% PGX, 20% TLT, and 20% SPLV, we're dealing with...

- An average yield of 3.7% .

- A compounding annual growth rate of 8.7% since 2012.

- A standard deviation of just 9.0% .

- A max drawdown of 19%.

- A Sharpe Ratio of 0.88 indicates a risk/adjusted return in line with the market, despite the lower total return. This is caused by much lower volatility.

{kind=link}

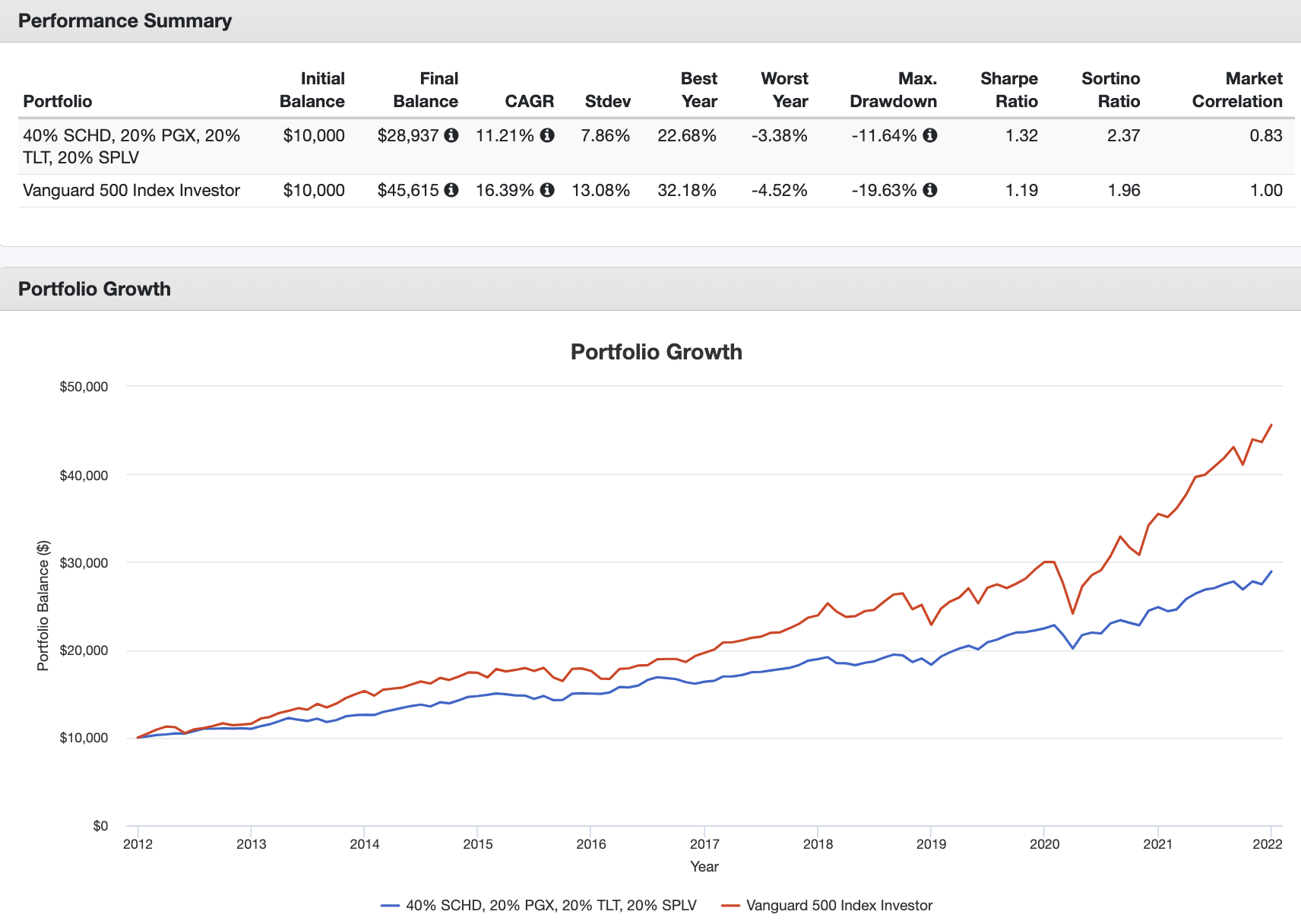

Please note that if we exclude 2022, this model portfolio has returned 11.2% per year since 2012. This came with a standard deviation of just 7.9%.

While excluding bad years is an easy way of hiding a bad performance, it is fair to say that this portfolio holds up very well in years that do not see steep spikes in inflation expectations. And even if it happens again, investors can increase exposure to SCHD and PGX to increase income and inflation protection.

Portfolio Visualizer (2012-2021)

{kind=link}

That said, there are things to keep in mind.

- Backtesting something going back to 2012 doesn't tell us a lot. Most years in this sample had low inflation and subdued interest rates. Sufficient backtesting requires at least a few decades.

- Moreover, backtesting something for ten years does not incorporate the changing needs of retirees. For example, going from age 70 to 80 requires bigger financial adjustments than going from 30 to 40. The older people get, the more they tend to require income - or safety if they opt to go for the 4% rule that is based on selling their investments in parts each year.

Needless to say, if investors have accumulated $1 million to invest, they can get $37K in pre-tax dividends from this portfolio. In addition to social security, which is currently a maximum of $3,627 in the United States, investors have a decent income that likely allows them to do the things they have planned for retirement.

Furthermore, it is easy to make adjustments. Investors can reduce investments in bonds or low-volatility stocks and boost their investments in higher-income investments.

One of them was excluded from the portfolio due to backtesting issues.

However, it deserves to be included in this article.

Why JEPI Makes Sense

The JPMorgan Equity Premium Income ETF ( JEPI ) - 9.6% Yield

I wanted to include this ETF in the portfolio. However, I didn't do that because this ETF was established in 2020, which would have given me less than three years to backtest.

However, I would include it in the model portfolio above. Giving JEPI a 20% weighting by lowering the exposure to TLT and SPLV from 20% to 10% (each) would improve the portfolio yield to 5.1% .

So, what's JEPI?

JEPI is a fascinating mix of top-quality dividend stocks and a method to enhance income.

As explained by Brad Thomas in a recent article , JEPI uses covered calls to improve its yield (emphasis added).

One of the main strategies behind JEPI is the use of Equity Linked Notes ("ELNs") as well as covered calls . For those of you unfamiliar with covered calls, let's take a few minutes to explain.

A covered call is an option contract where the option seller owns the underlying stock or ETF that you're going to sell. Selling a covered call to a third party gives the buyer the right to purchase the underlying security at an agreed upon price (strike price) by an agreed upon date (expiration date) . Every option contract has a buyer side and a seller side.

1 option contract = 100 shares of the underlying security, which is often a stock or ETF.

When selling an option, you earn a premium. Selling a covered call means that if the underlying security's price goes above the strike price by expiration, you would be required to sell 100 shares per contract you sold at the strike price. So, in order for this option contract to be considered "covered," you need to own at least 100 shares of the underlying position.

In other words, the ETF makes money by selling covered calls. By doing so, it collects a premium. If its holdings suddenly rise, it may be forced to sell. However, because the ETF holds the equities (covered), risks are low. While the ETF somewhat limits upside potential, it does boost the dividend yield a lot.

Technically, investors who own individual stocks can follow this strategy by selling their own covered calls. However, this comes with risks, and it takes time. JEPI does this for its investors.

Since its inception, JEPI has returned 43%, which is in line with the total return of the S&P 500. Excluding dividends, the performance is below 10%, which is caused by limited upside related to the dividend-enhancing option strategy.

Furthermore, this 9.6%-yielding ETF has an expense ratio of 0.35%.

In its portfolio, it holds 132 holdings, with a turnover ratio of 195%. A turnover ratio of 100% means that an ETF or mutual fund has bought and sold all its positions within the last year, which indicates that this is an active ETF. That makes sense, given its options strategy.

Looking at its top 10 holdings, we also see that no holding has more than 1.7% exposure. Also, most of its major holdings are well-known dividend (growth) stocks. In other words, JEPI is a bit similar to SCHD, except that JEPI has a dividend-enhancing options strategy.

{kind=link}

So, with all of that said, here's the bottom line.

Takeaway

In this article, we discussed the complications that come with picking the right assets for a retirement portfolio. I presented a number of picks that could help retirees enjoy a mix of low-volatility income and decent capital gains on a long-term basis.

The suggested investment mix includes preferred shares, the JPMorgan premium equity income ETF, and the Schwab High-Yield ETF - all of which offer high yields and consistent dividend growth. In addition, the article proposes alternatives such as a low-volatility S&P 500 ETF and long-term government bonds to add stability and growth potential to a retirement portfolio.

Depending on individual income requirements, investors can construct a low-risk portfolio with a yield of 5.1%, which can be raised to 6% without adding significant risks.

Needless to say, multiple roads lead to Rome, which means I will discuss other alternatives in the weeks and months ahead - especially as there are more suitable ETFs and strategies. Also, we'll cover single-stock portfolios that come with high yields and subdued risks.

So, please don't hold back in the comment section. Let me know what you think of these picks and what you would like to see going forward.

For further details see:

The Near Perfect High-Yield Retirement Portfolio