UBER - The Next FAANG: The SUV Driving Future Growth

2023-03-07 08:46:37 ET

Summary

- FAANG was coined based on companies who were/are present in everyday life.

- Now that 10 years has passed since FAANG was born, it's time to look at what the next group may look like.

- Spotify, Uber, and Visa may very well be part of this next wave.

Overview

10 years ago, the term "FAANG" was coined to represent the high growth stocks that would drive major gains in the stock market ( SPY ) for the next decade. It is no coincidence that these companies all play a major role in everyday life, not just then but also now. It is my belief that members of the new FAANG will also exhibit the same characteristic of being part of our everyday lives. That is why I break down the possibility of Spotify ( SPOT ), Uber ( UBER ), and Visa ( V ) being major potential players in the next generation of growth, coining the term SUV.

It is hard to argue that Spotify and Uber are not increasingly becoming a component of everyday life. I have written a more detailed description of the disruption that Spotify has caused in a previous article found here . Essentially, SPOT now has the advantage of being played everywhere, anytime, through nearly every audio medium as opposed to the myriad of playing devices and forms in which music was played just 15 years ago. As for Uber, I think you'd be hard pressed to find many cellphones in urban and suburban areas that don't have the app downloaded and frequently used. Lastly, Visa is the number one payment processor and credit card provider in the world that is still sitting in the middle of the cash to cashless global transition.

An important factor that I like to consider for future growth companies is the generational replacement value. For more clarity, I am looking at how a company will benefit from generational changeover. To highlight this, I will use a hypothetical situation with Uber for what could happen in the next 10-20 years as there is a large turnover in the baby boomer generation to Gen Z and beyond. Let's say that there is a population of 50 million baby boomers in North America and that roughly 20% of them have the Uber app and use it on average at least once per month. Now, let's say that the next 50 million in population in North America that grow into adulthood and become consumers will be a part of Gen Z while the next generation is being born that is replacing the boomers and will eventually age towards becoming consumers. Hypothetically, let's say this next 50 million consumer group entering the economy has a 80% rate of Uber downloads and monthly usage.

| Population |

| Usage (%) |

| Total Users |

| Baby Boomers |

| 50 million |

| 20% |

| 10 million |

| New Gen. Z |

| 50 million |

| 80% |

| 40 million |

By doing some quick math we can see that there would be a massive increase in monthly users due purely to generational turnover even if the total North American population stays flat or even decreases.

Spotify

Spotify is the undeniable leader in music streaming and total number of listeners across the globe. To make this even more attractive, it is quickly working to expand its margins. There is still a large opportunity in addressable market expansion and average revenue per user, ARPU, growth. Below I will detail a model that shows how powerful the growth of SPOT could be. Here we will use the most recent annual metrics and input the 2027 targets outline by the company to predict where Spotify might be in 5 years.

- SPOT management is targeting 10% operating margins by the end of 2027

- Spotify has seen 15-20% monthly user growth over the last several years, however I will use a more conservative growth rate forward of closer to 10%

- Assume a reduction of nearly 3 million shares by then end of 2027 as the company continues to buyback shares

- Assume total growth in ARPU of 10.5% by the end of FY2027

| FY2022A |

| FY2027E |

| Monthly Active Users (MAU's) |

| 489 million |

| 800 million |

| ARPU |

| €23.98 |

| €26.50 |

| Revenue |

| €11.727 billion |

| €21.200 billion |

| Operating Profit |

| -€431 million |

| €2.12 billion |

| Shares Outstanding |

| 192.9 million |

| 190 million |

| EPS |

| -€2.23 |

| €11.16 |

There is a large difference in the EPS that Spotify can produce if the company targets and these relatively conservative inputs are met in the next 5 years. If we apply a 25x P/E multiplier that is akin to current major growth stocks to the final EPS estimate, we arrive at a target price of $279. This is a 121% increase from today's price.

Uber

Uber has arguably been the number 1 beneficiary of the "gig economy". But I believe there is a deeper meaning behind the rise in Uber other than people being lazy or increasing their spending habits. I think Uber actually operates as a societal need for three reasons.

- Uber provides an extremely effective solution to drunk driving, a tragedy that takes far too many lives every year.

- It is a more effective use of fossil fuels and energy due to the fact that many riders are in parties of 2 or more and that Uber's navigation is built to optimize drop-off and pick-up routes.

- Rising costs of living versus slower growth of wages creates the need for a large portion of the population to find additional sources of income and become drivers.

I believe the implementation of Uber One is genius, giving it another arm in the gig economy. The addition of food delivery and now other services such as package delivery to the Uber total offering allows Uber to increase the utility of its driver's vehicles exponentially and provides multiple avenues for growth. The monthly subscription model is the icing on the cake as it will lead to greater user retention, greater network effect, and will stabilize revenue.

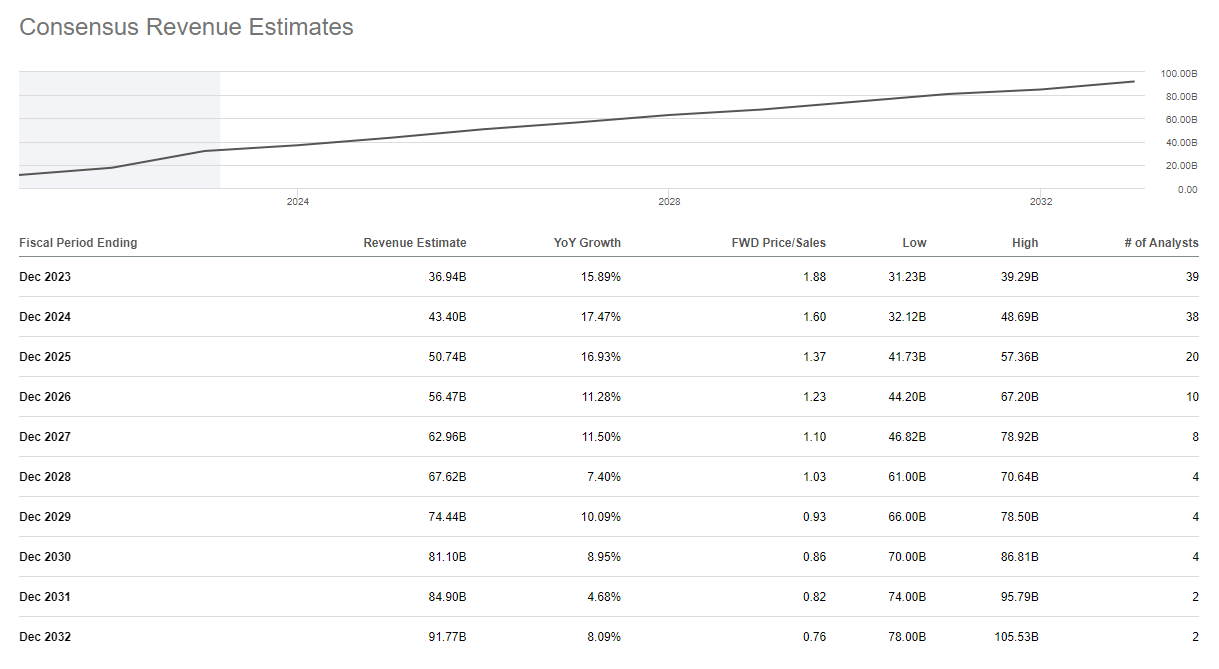

Excitingly, Uber recently posted its first profitable quarter and looks as if there is a runway to accelerate its profitability. The future is bright as well when we take into consideration its forays into the rental car market and the potential for international expansion. Based on current analyst projections, revenue is expected to continue to grow at a blistering pace. If the company is able to continue its improvement of its profit margins, there is tremendous upside for the future.

{kind=link}

Visa

I have previously written my thesis on Visa and why I believe so strongly in its future growth. In this article I will investigate the similarities of Visa with a blue chip growth gem of the past decade, Microsoft ( MSFT ). Let's first look at 2013 Microsoft and see how similar it is to present day Visa.

| 2013 Microsoft |

| Current Visa |

| Net Profit Margins |

| 28.08% |

| 50.28% |

| Rev. Growth (5y Avg.) |

| 10.84% |

| 10.91% |

| Market Cap |

| $310.5 billion |

| $454 billion |

It is interesting to see the similarities in revenue growth and the fact both are in the mega-cap stock category. Visa's visibly greater profit margins are likely the reason for the larger market cap as it commands higher multiples than MSFT did in 2013. If we fast forward to current day Microsoft, we see that net profit margins have expanded to 35.05% (a 25% expansion from 2013), revenue continued to grow at roughly 11% for the past 10 years, and the market cap has increased more than 6x to a whopping $1.87 trillion.

While I would be impressed if Visa could expand its already market leading profit margins by another 25% over the next decade, it isn't out of the question that it will see a meaningful expansion as cashless payments continue to accelerate and the scalability of its business model provide increased effects on margins. Current estimates show a greater than 11% revenue growth for the next several years, in line with what MSFT was able to accomplish over the last decade. If Visa is able to achieve this continued strong growth and an expansion in profit margins, it seems feasible that the stock could see strong returns by 2033.

Risks

Obviously, there are a lot of assumptions built into these projections and future macroeconomic influences are impossible to predict. Additional major risks for Spotify and Uber are competitors that begin to claw away market share or develop technology/services that makes their offerings obsolete. Secondly, both companies have not proven they can achieve and maintain profitability but I believe the size of each of these companies and visible recent improvements in margins show that management knows what they are doing and have a plan for the future. Visa also runs the risk of new technology and competitors such as buy now pay later, new fintechs, and cryptocurrencies. In my opinion however, V has addressed these threats and even began to add these technologies to its business either through acquisition or organic development.

Summary

After looking at each of these companies with a 10 year buy and hold lens, all three look promising. Personally, I think generational replacement value is an underrated source of growth for new companies in new industries and will be an underlying tailwind for both Spotify and Uber. Lastly, these companies exhibit many of the same characteristics as the FAANG stocks in the sense that they are a part of everyday life. A large portion of the world already has the Uber app, the Spotify app, and a Visa card all in their pocket on a daily basis. The question I guess you need to ask is: Do you see yourself using Spotify, Uber, and a Visa credit card 5-10 years from now?

For further details see:

The Next FAANG: The SUV Driving Future Growth