PBW - The Portfolio Strategy You Need When The Recession Hits In 2023

2023-03-29 09:56:15 ET

Summary

- I think that the Fed will take a wait-and-see approach after its 25-basis point hike in May 2023. My base case scenario for 2023 is a mild recession.

- There are risks to the real economy if lending standards reduce new loans and deprive smaller businesses of needed capital.

- High quality bonds look more attractive than equities at current valuation levels, while I expect emerging market equities to bring more upside in the near term.

- Pockets of opportunity remain in the healthcare and technology sectors, while consumer staples, industrials and utilities remain attractive.

- The Barbell Portfolio has generated 32.8% returns year-to-date relative to the S&P 500's 3.4% returns year-to-date, an outperformance of 29.4% for 2023 year-to-date.

This article was first posted in Outperforming the Market on March 29, 2023.

Last week, I argued that we could see a Black Swan event happening in the markets in the near to mid-term.

That said, given that a Black Swan is, by definition, is impossibly difficult to predict, I deliberately did not try to identify what this Black Swan could be.

However, I think that a barbell portfolio strategy that is well diversified could outperform the S&P 500 this year, as evident by The Barbell Portfolio, which I will explain in greater detail below.

Side effects of recent banking events

While the recent banking saga brings back memories of 2008, I do not think that what we are seeing today will result in a 2008 like crisis.

This is seconded by many market and industry experts who think likewise. The quality of the banking system is much better.

Even the Fed's Jerome Powell had this to say about the U.S. banking system in the recent March FOMC meeting as mentioned in an earlier article :

The U.S. banking system is sound and resilient. Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain. The Committee remains highly attentive to inflation risks.

That said, banks continue to be an integral part of the economy given the role it plays in the financial system.

With regional banks having a lower risk appetite as they attempt to rebuild liquidity, this inevitably means fewer new loans for the real economy.

The ones that will ultimately hurt are the smaller businesses.

- 50% of the U.S. commercial and industrial lending come from banks with less than $250 billion in assets.

- 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending comes from banks with less than $250 billion in assets.

Ultimately, these banks that survive will have to increase their lending standards, although the extent of the increase should be smaller than that seen in the financial crisis. As a result of this tighter lending standard, what will happen is that small businesses are likely to experience a credit crunch, and the economy will experience lower growth and higher unemployment.

Based on an estimation by Goldman Sachs, if the small banks with low share of FDIC insured deposit reduce new lending by 40% and other small banks reduce new lending by 15%, this will lead to a 2.5% decline in credit growth, which will result in a 0.25 percentage point impact on 2023 GDP growth. If the credit conditions worsen and banks increase lending standards by a larger extend, this will have a greater impact to financial conditions and GDP growth.

Where will the Fed go from here?

There are essentially three options for the Fed. The first is to keep hiking rates to reach its objectives and show the market its commitment to its goal, potentially requiring targeted interventions as a result. The second is to pause the hikes and look at how the economy responds before making any further decisions. The third and final option is to cut rates and this is based on the assumption that the tightened financial conditions as a result of the regional banking saga will correct inflation naturally.

I think the second option is what the Fed will take from here.

With the final 25 basis point hike in May 2023, I think the Fed will take a pause from there.

I do not think that there will be an immediate switch to rate cuts.

Looking historically, the Fed cut rates when inflation was still in the double-digit rank, but the unemployment rate was at 7% then.

Today, with unemployment rates so low at about 3.6% and inflation far above its target, cutting rates would be an unprecedented move and an unlikely one in my view.

Thus, I do think that a pause will be the Fed's move after the May FOMC, and from there, the data-dependent Fed will decide whether or not its policy has made enough of an impact for it to achieve its own targets.

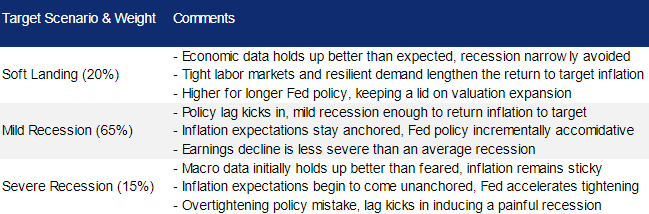

Economic scenario

As a result of the tighter financial conditions, the Fed's restrictive monetary policy and a likely policy lag, I think we will most likely see a mild recession in 2023 and that is likely my base case scenario for 2023. While talks of a soft landing was more frequent in the early months of 2023, I think that given the economic data we are seeing today, along with evidence from the U.S. banking system, I continue to believe that a mild recession will be the base case for 2023.

Economic scenario for 2023 (Citi )

{kind=link}

Bonds are looking attractive relative to equities

With the macro backdrop in mind, let us dive into which asset classes look attractive today.

Equity valuations remain relatively unattractive today despite the selloff we have seen.

The MSCI US index is currently at 17.7x which is still a 10% premium to its 20-year average P/E multiple of 16x, while the MSCI ACWI P/E multiple is currently at 15x, above its long-term average of 14.5x. The valuation of US equities are also trading at a 18% to global equities.

I think that there is scope for further valuation compression within the U.S. equities space if inflation continues to be stronger than expected or if growth disappoints.

On the other hand, I think we are seeing an attractive opportunity to be increasing exposure to high quality bonds instead. I think that investors need to be positioned tactically for a scenario where the Fed may be ending its hiking cycle sooner rather than later.

I elaborated in greater detail about the Fed potentially pausing its rate hike sooner than expected in an earlier article, and this was what I stated in that article:

In the March FOMC statement, it was worth noting that the forward guidance was dropped from "ongoing increases" to "some additional policy firming may be appropriate."

This initially seemed dovish given that Dovish start given the change in the forward guidance. On top of that, Jerome Powell also said that he thought that a pause was considered, which was a result of the recent banking crisis we have seen.

Another point worth noting was that Jerome Powell said in the press conference that the credit tightening we have seen as a result of the banking crisis is acting in the same direction as the rate hikes that the Fed were implementing, which could mean that they may then need to hike less than expected to control inflation and bring it back to their target.

He went on to further emphasize that the new forward guidance includes "some" and "may" which implies that there is a lower probability that more rate hikes were coming.

As a result, I do see a better opportunity for investors to be increasing their bond holdings, with a selective focus on high quality bonds or government bonds opportunities.

Bonds will not only give very attractive yields today, it will also bring capital gains should the economy actually slow down. For investors currently holding excess cash, investing in high-quality bonds today will help you lock in today's decent yields.

In addition, I would highlight an interesting evidence that shows that equities are less attractive than government bonds today.

The current earnings yield gap, which is the difference between the inverted P/E, or the earnings yield, and the 10-year treasury yield is at a 10-year low today and this is below the long-term average.

Bonds are attractive relative to equities (Refinitiv, UBS)

This highlights the attractiveness of high-quality bonds and government bonds over equities at the current levels. 1-year, 3-year, and 10-year US treasury bond yields are trading at 4.4%, 3.6% and 3.4% respectively as a result of the inverted yield curve we see today. For example, the iShares 20+ Year Treasury Bond ETF ( TLT ), which holds US Treasury bonds with remaining maturities of more than twenty years has a yield to maturity of 3.76% today, while the SPDR Bloomberg 1-3 Month T-Bill ETF ( BIL ), which provides exposure to US Treasury Bills with maturities between 1 and 3 months remaining, has a yield to maturity of 4.11% today.

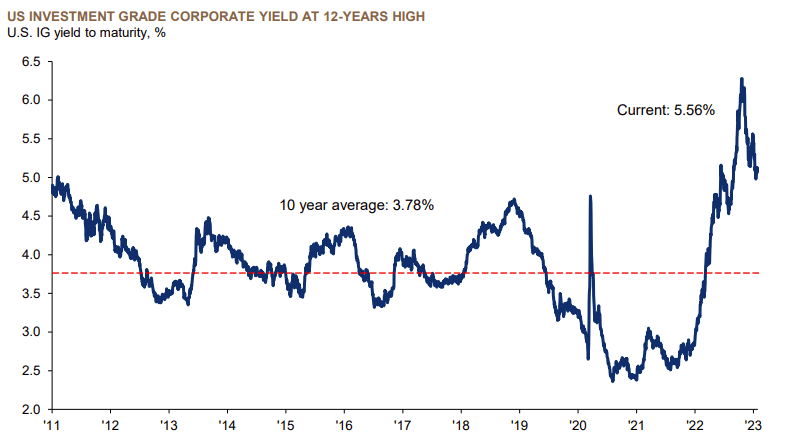

Also, we are seeing the highest yields on U.S. investment grade bonds for more than 12 years as a result of the hawkish Fed and higher inflation. As a result of the higher investment grade yields we are seeing today, I do think that the high-quality investment grade space brings strong fixed income opportunities for locking in of higher yields.

US Investment Grade yield (Bloomberg)

{kind=link}

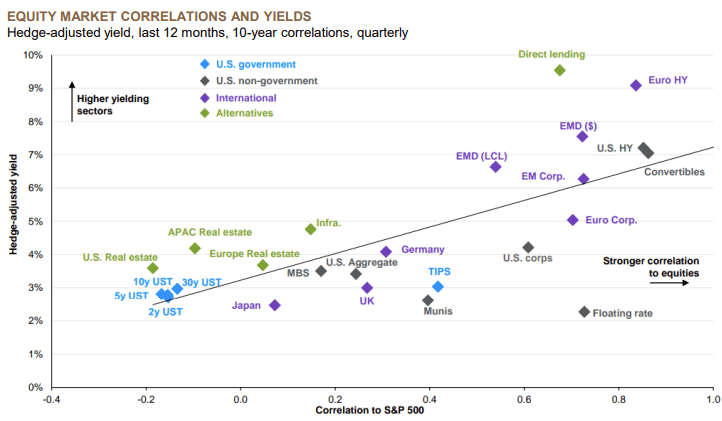

One of the best arguments for high quality investment grade bonds and government bonds is the diversification impact it will bring. Given the current tightening of financial conditions, macroeconomic uncertainty and a potential recession in the United States, the negative correlation that bonds bring to a portfolio is a desirable characteristic for investors today, in my view.

Bonds low correlation to equity markets (Bloomberg)

{kind=link}

Preferring emerging market equities over U.S. equities

In light of the tightening of financial conditions as well as a slowdown expected in the United States, I do think that emerging markets are tactically more attractive in the near term.

As highlighted above, US equities are trading at an 18% premium to global equities and a 10% premium to its own 20-year average P/E. In contrast, global equities are looking more reasonable from a valuation perspective.

Besides that, I continue to like the opportunity that China could bring to an investor's portfolio in the form of diversification and alpha opportunity in 2023.

We have seen that China exited from its zero covid policy very quickly and decisively. As a result of China reopening its economy, this will likely bring positive upside surprise to Chinese equities in the next one year. In addition, China's monetary policy is not currently as restrictive as the U.S. given that we just saw China cut its reserve requirement ratio by 25 basis points to boost its economy.

As a result of pent-up demand, the re-opening of China's economy should lead to a recovery in domestic consumption. In the first half of 2023, we saw the recovery in consumption show a strong rebound as China sees the benefits of its re-opening.

This recovery will not just be domestic, but also benefit other neighbors of China, as well as other consumption and commodity related countries in Europe, Latin America and the Middle East.

In addition, I think that there will be headwinds for the U.S. dollar in the near-term as a result of the end of the Fed's tightening cycle as well as the expected slowdown in the U.S. economy. With a softer dollar outlook, this will benefit emerging markets equities on a relative basis compared to that of the developed markets.

Lastly, emerging market valuations look attractive despite the recent rally. The MSCI emerging market index is trading at a 11.5x 1-year forward P/E multiple. This is a 24% discount to developed markets but roughly in line with its historical average. When looking at a P/B basis, the MSCI emerging market index is trading at a 43% discount to developed markets, which is a level that is historically consistent with a relative positive return over the medium term.

Some of the emerging market ETF ideas include Vanguard FTSE Emerging Markets ETF ( VWO ), iShares MSCI Emerging Markets ETF ( EEM ) and iShares Core MSCI Emerging Markets ETF ( IEMG )

Sector preference

In terms of preferred sectors, there are a few that could outperform in the current environment.

One of which is good old consumer staples and utilities, both of which has been traditionally well positioned in an economic slowdown and outperforms the general market when the economic indicators are weak.

I think we could see some bright spots within industrials. This is particularly so for green industrials given the huge investment being put into green investments as a result of the US Inflation Reduction Act and other positive regulations globally. As a result, this will help green tech companies and green industrial companies set to benefit from the sustainability theme.

There are some pockets of opportunity within healthcare and technology, although the current MSCI AC World Healthcare trades at 17.2x forward earnings, a 15% premium to the market, which is above its historical premium and the MSCI ACWI IT subindex is trading at 23x forward multiple and dislocated with its relationship with real rates. Based on the relationship between inverted real rates and the forward P/E for technology companies, the P/E multiple should be trading at a multiple of between 16xand 18x. That said, I think there remains to be pockets of opportunity within both healthcare and technology where valuations appear compelling while the business models and fundamentals remain solid.

MSCI AC World IT P/E vs US real rates (inverted) (Refinitiv datastream, UBS)

I am neutral on the energy sector today. As a result of a strong macro backdrop, 2022 was an extraordinary year for energy as there was a supply shock to the energy markets as a result of the Russia Ukraine war, while there has been an under investment in oil. At the same time, the world began to re-open and relax covid restrictions, increasing the demand for oil.

Whether there is a structural case for higher oil prices remain to be a debate, but as energy prices have come down from its peak, there is bound to be some near-term correction for the energy sector in the meantime. That said, I do think that the sector remains cheap at 7.8x forward P/E and has an attractive 4.4% dividend yield. Even if the earnings growth may disappoint in 2023 as a result of a stellar run in 2022, I think those that have a strong conviction in the structural story in the under-investment in oil and gas could find some opportunities here.

Brent price vs MSCI AC World Energy (Refinitiv datastream, UBS)

Some of the green tech and industrials ETF include Invesco Solar ETF ( TAN ), iShares Global Clean Energy ETF ( ICLN ) and Invesco WilderHill Clean Energy ETF ( PBW ), amongst others. In addition, consumer staples exposure can be obtained through ETFs like Consumer Staples Select Sector SPDR Fund ( XLP ), Vanguard Consumer Staples ETF ( VDC ) while utilities ETFs possible include Utilities Select Sector SPDR Fund ( XLU ) and Vanguard Utilities ETF ( VPU ), amongst others.

Portfolio strategy

It is important to remain nimble in volatile times like this. What works for 2022 may not work so well for 2023. For long-term investors, it is important to remain invested in high conviction stocks while getting rid of those companies with lower quality or conviction.

The Barbell Portfolio has generated 31.4% returns year-to-date relative to the S&P 500's ( SPY ) 3.7% returns year-to-date. This is an outperformance of 27.7% for 2023 YTD generated by The Barbell Portfolio.

The Barbell Portfolio outperformance (Author generated)

The outperformance in The Barbell Portfolio came from stock selection in green tech, emerging markets and even semiconductor and technology stocks. Moving forward, I continue to be told members to remain selective in the stocks, and most importantly, being aware of the valuation of the company.

I continue to like the alpha opportunities in the portfolio coming from the green tech and green industrials companies we hold, and at the same time from the diversification opportunities that comes from the exposure to emerging markets.

In the longer-term, due to the mix of value, contrarian and growth stocks in the portfolio, I continue to see the barbell strategy outperform the market across different markets.

The fact that the portfolio has generated such outperformance in a difficult year like 2023 is a strong evidence that the barbell strategy is working as intended.

All in all, I continue to advocate for a well-diversified, barbell approach to the portfolio strategy. In the near-term, high-quality bonds and government bonds, along with emerging market equities, look attractive at current levels. In terms of the sector exposure, there is a preference towards more secular trends and defensive sectors like consumer staples, green tech, utilities, and careful selection within technology and healthcare.

For further details see:

The Portfolio Strategy You Need When The Recession Hits In 2023