CA - The Top 5 Dividend Stocks For 2024

2024-01-04 07:00:00 ET

Summary

- The article discusses our top 5 dividend picks for 2024.

- I will go over last year's top picks.

- And provide insights into how I picked the top 5 dividend stocks for 2024.

Written by Sam Kovacs.

Introduction

It's the beginning of the year, which is a great time to make some picks, as I'll invariably look back on them next year to measure how they did, and where we could have done better.

In this article, I'll go over last year's beginning of year picks, give a few insights, then provide you with my absolute favorite top 5 dividend stocks for 2024.

Last Year's Top Picks

I presented a few articles highlighting what I believed were some top picks for dividend investors in 2023.

I took two approaches: the first was to focus on a trend which hadn't been fully capitalized on, which I called the $1 Trillion Opportunity . The second approach was to focus on contrarian picks, highlighting why the market didn't like these stocks, and why this created an opportunity for value.

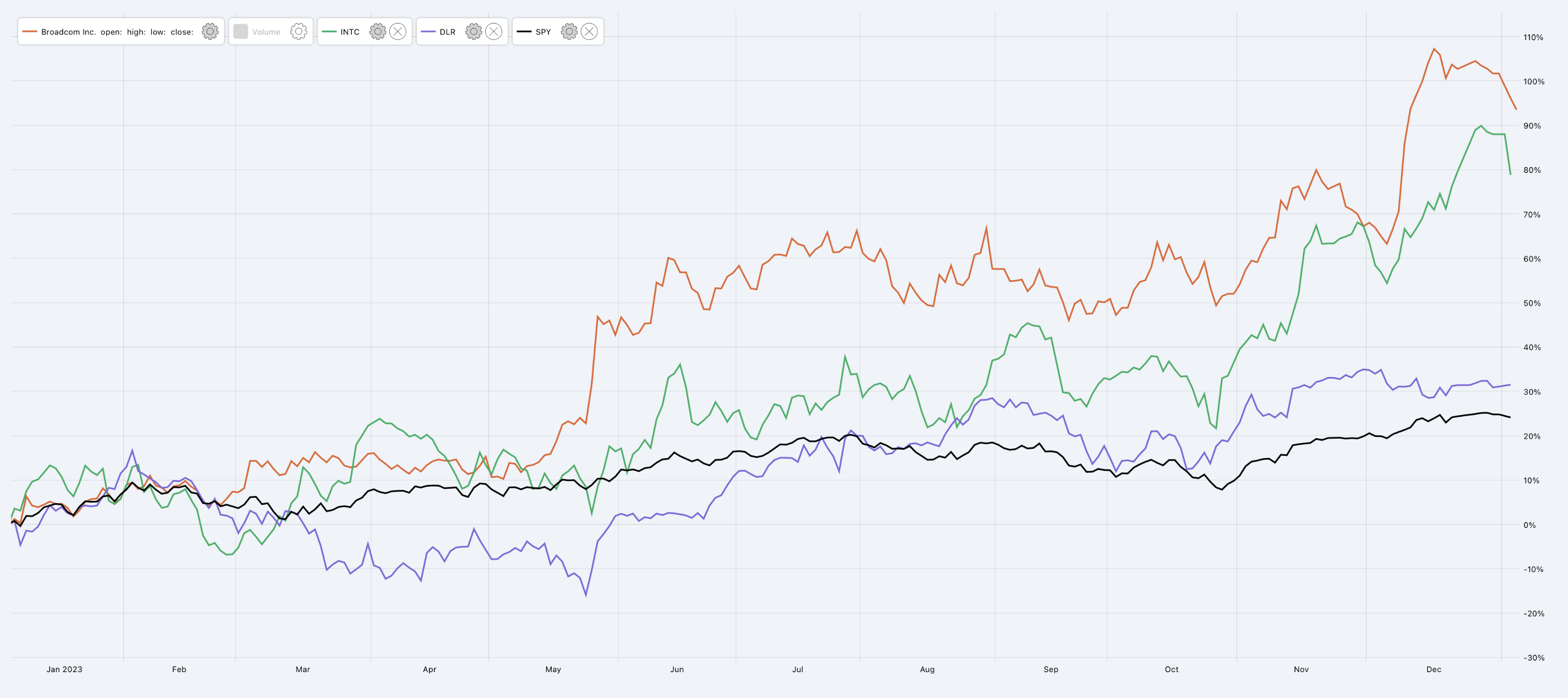

Focusing on the AI/Semiconductor trend paid off.

Our picks at the beginning of the year included Broadcom ( AVGO ), Intel ( INTC ), and Digital Realty ( DLR ).

{kind=link}

All 3 of these picks did better than the S&P 500 (SP500).

Being contrarian involves recognizing value while appreciating that a cyclical trend is going against that security. You're willing to forego short-term performance for long-term gains, knowing that the tide will turn once again at some point.

As I pointed out last year:

If you are investing in dividend stocks to cover your retirement expenses, then your time horizon potentially goes beyond your death. You have no need for performance this quarter or this year, so you can easily give it up for stronger long term performance.

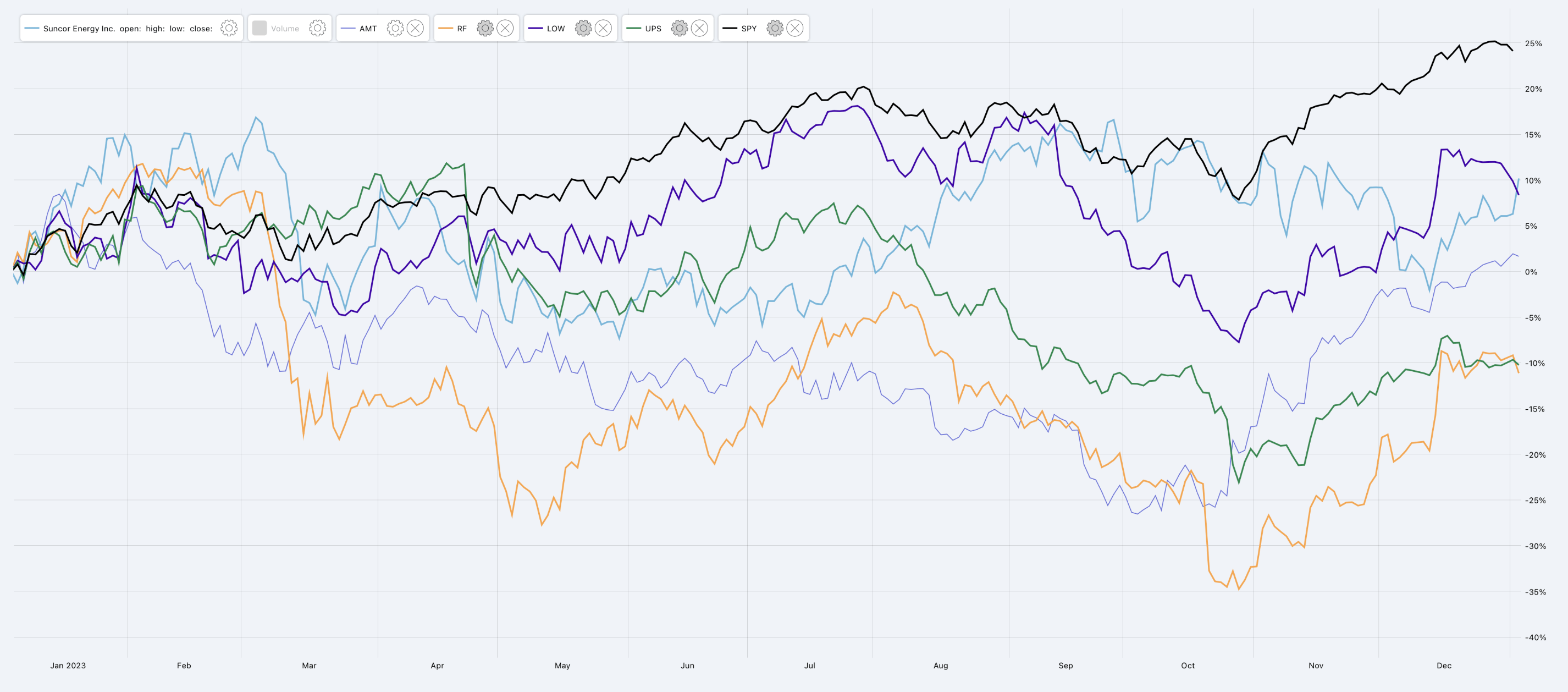

Here's the insights we provided for each of our 5 contrarian picks.

Market participants are projecting that higher rates will hurt real estate companies: this has driven American Tower Corp. ( AMT ) down.

They believe that higher rates will lead to a recession. This recession will hurt discretionary spending such as on home improvement, driving down Lowe's ( LOW ).

It will also make consumers fragile, which is holding back bank stocks such as Regions Financial ( RF ).

They believe that the strength of the dollar will persist forever, keeping Canadian stocks like Suncor ( SU ) down.

Finally, high inflation and weaker consumers will be a burden on transportation stocks such as United Parcel Service ( UPS ).

{kind=link}

All 5 of them underperformed the S&P 500 in 2023, because being "contrarian" often means being wrong until you're right.

Which is a fair and simple approach. Buying quality when it is undervalued is an easy way to do well long term.

Nothing has fundamentally changed in the value proposition of any of these 5 names.

The trends which beat these stocks down in 2022, continued to beat them down in 2023, as going against the trend is a surefire way to cause yourself more trouble.

One classic mistake among investors is to think that information gets efficiently priced in short periods of time. My experience is the opposite.

Bad news or downtrends continue to persist for months or even years, as pessimism turns into throwing in the towel.

The real trick, then, is to find a budding trend, and get in when the stocks are still undervalued so that you can ride for the biggest gains without waiting for too long.

So this year, my 5 picks are based on trends that we've noticed or thought of, which will come to pass in 2024.

2024 Pick Number 5

Business development companies, or BDCs, are not all made equal. This is something I've illustrated time and time again to members of our Investing Group when comparing Blue Owl Capital Corporation ( OBDC ) to Eagle Point Credit ( ECC ).

The former company is splendidly managed and has increased NAV for its investors, all while paying generous dividends.

The latter has destroyed net asset value, and investors will realize that when they add their dividends to the current share price, they'll at best get the price they paid for their shares. ECC has added no value.

On the other hand, OBDC is by far my favorite BDC.

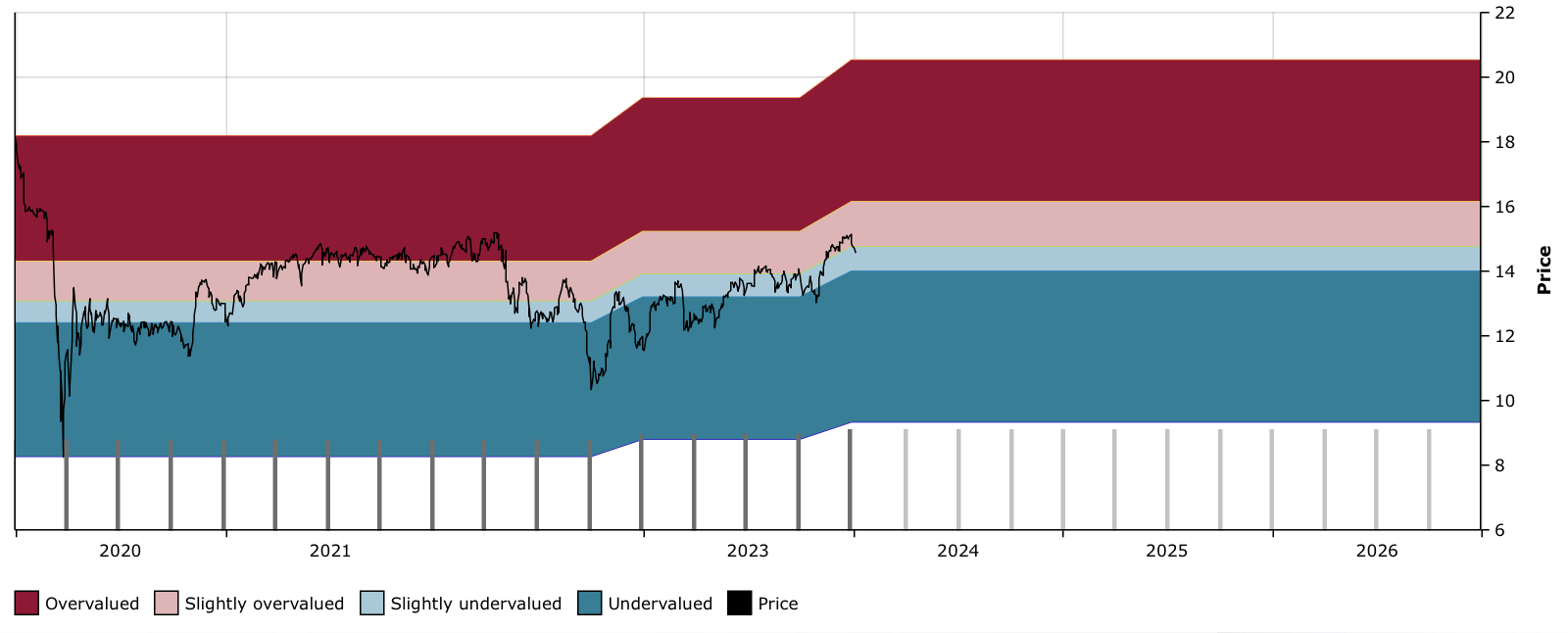

The stock trades at $14.56, backed by a NAV of $15.4, and yields 9.6%, excluding special dividends.

When you add last year's special dividends, that's an extra 1.7% on the current price.

{kind=link}

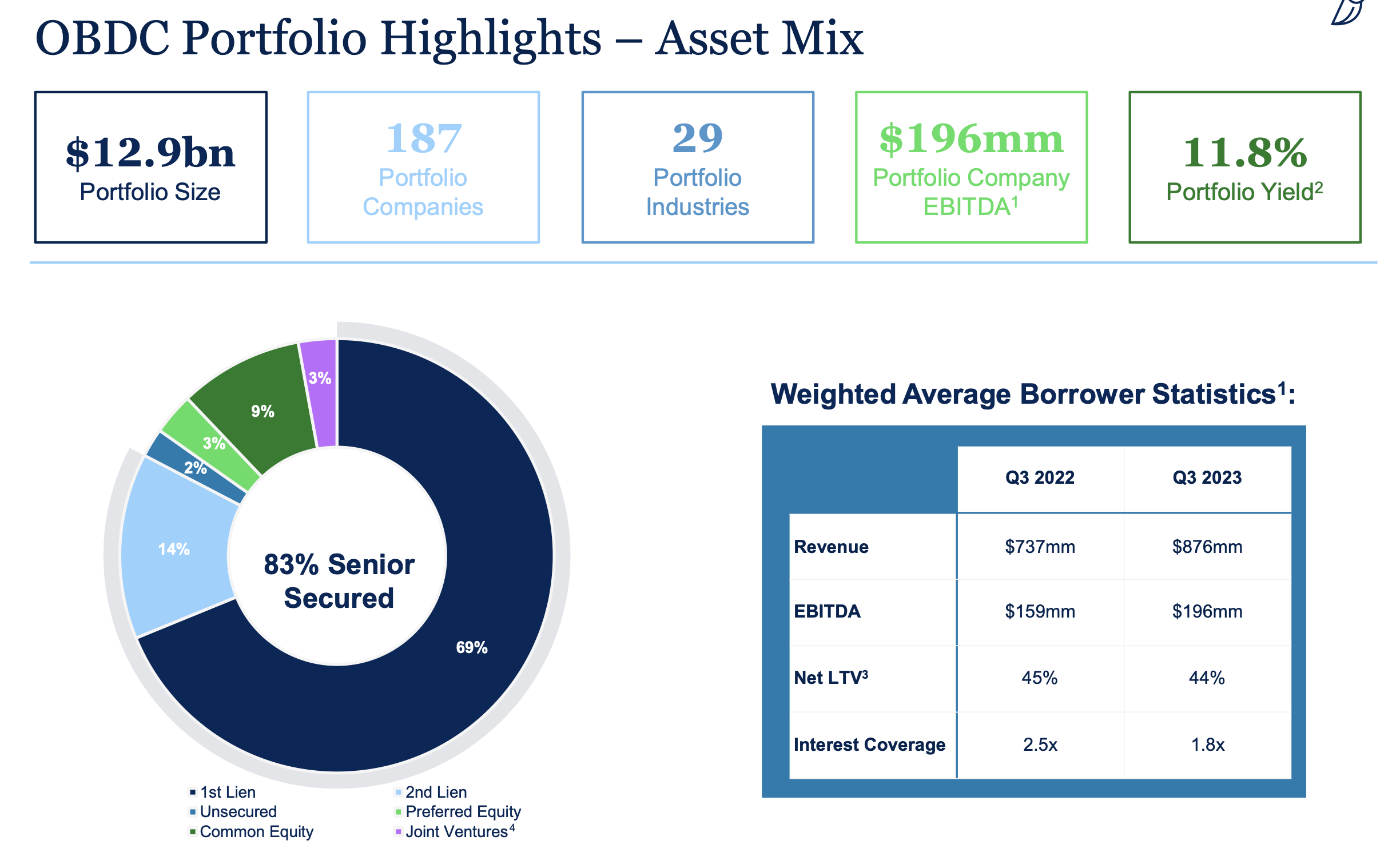

The company has benefitted from higher rates in 2023 to generate high amounts of income off its mostly senior secured loans to middle market companies.

{kind=link}

And while its portfolio companies interest coverage has reduced from 2.5x to 1.8x, OBDC continues to be confident that its borrowers will be able to keep a suitable cushion between earnings and interest payments in 2024, bottoming at 1.5x coverage half way through the year.

Given it will likely take a while for rates to come down, especially if we get our soft landing, OBDC should continue to benefit from the environment for years to come. As Fed Chair Powell noted in his latest conference call:

If the economy evolves as projected, the median participant projects that the appropriate level of the federal funds rate will be 4.6 percent at the end of 2024, 3.6 percent at the end of 2025, and 2.9 percent at the end of 2026, still above the median longer-term rate.

While I don't expect the price to go beyond the NAV, I believe we'll likely see an evolution of the share price between $14 and $17 throughout the year, which still lets us collect a big fat covered dividend, with room for extra special dividends throughout the year.

The stock has traded at a premium to NAV In the past. It now trades at a discount, so there could be some additional gains there.

I like OBDC as a big fat yield to own that has some structural advantages to it in the current rate environment.

2024 Pick Number 4

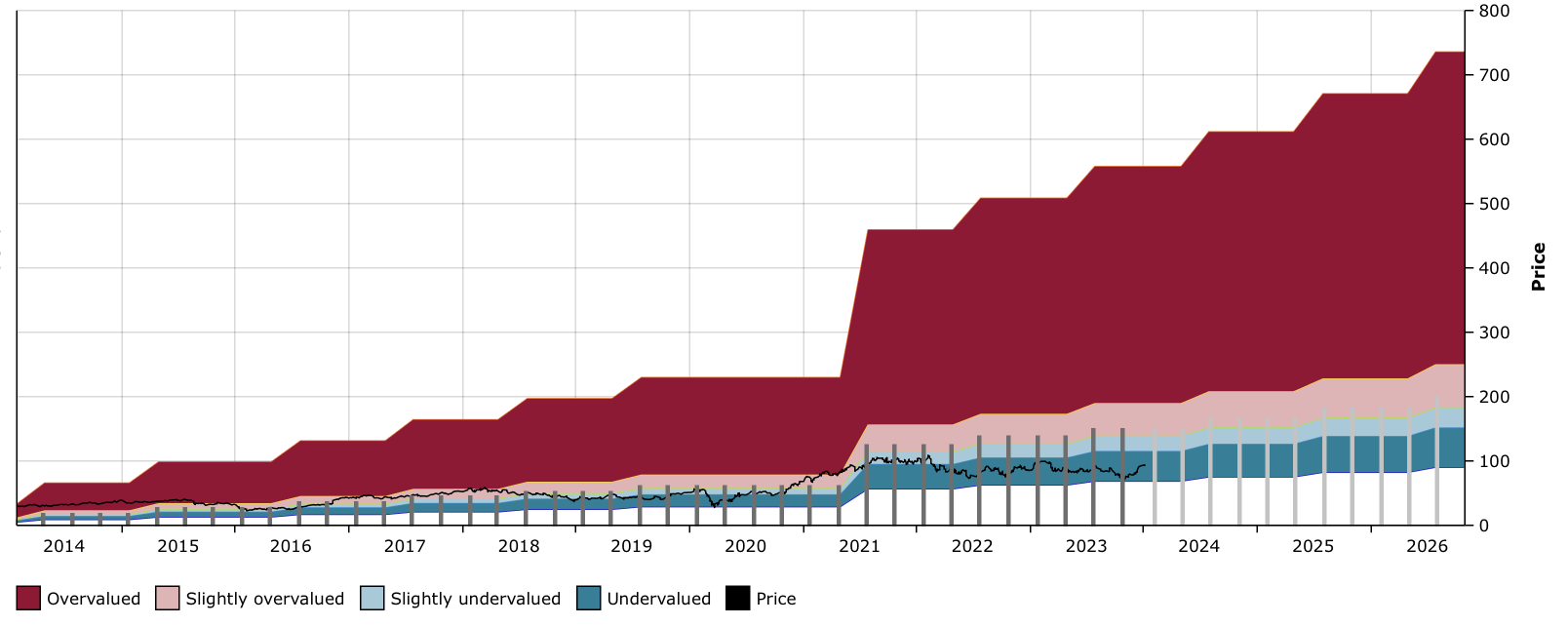

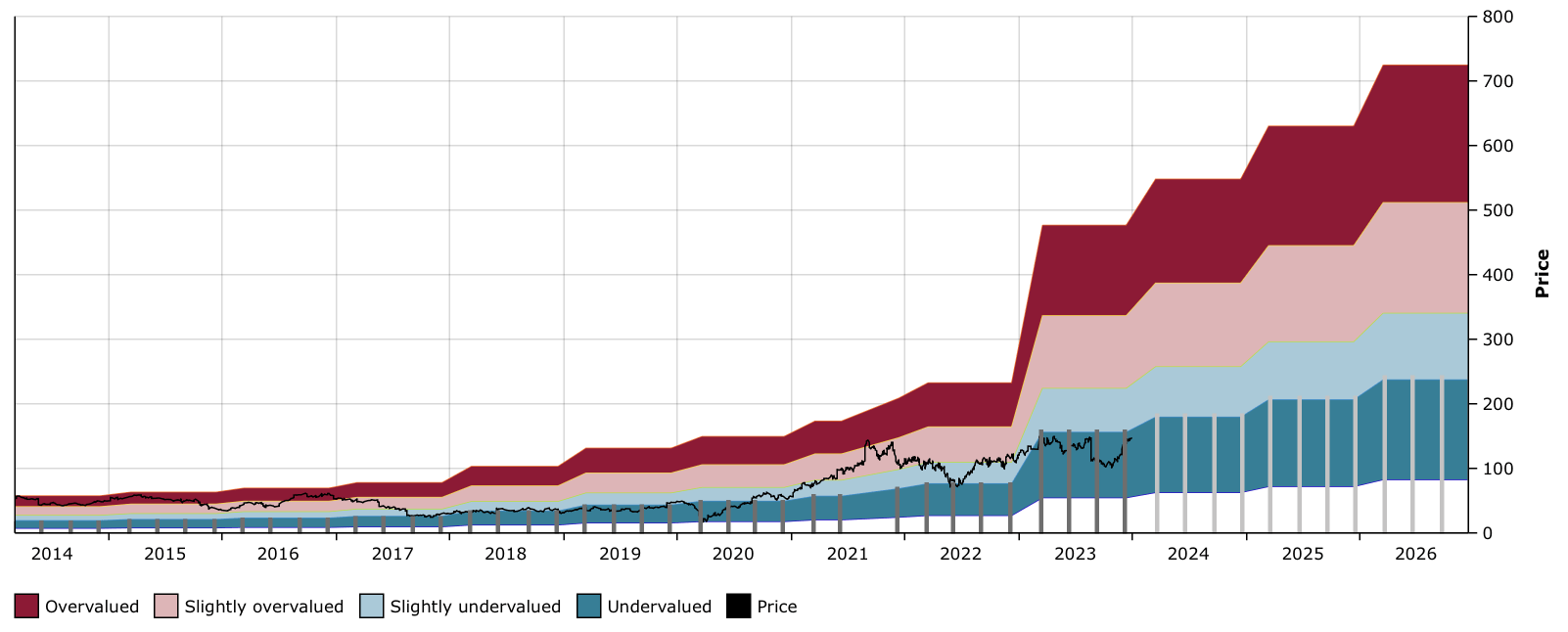

I purchased Morgan Stanley ( MS ) in June 2021, at $92 per share. It had just doubled its dividend, and was all of a sudden looking very undervalued relative to its fundamentals and long-term trend.

Two and a half years later, and the stock is still at $92, although we've enjoyed two 10% dividend hikes since purchasing.

MS currently yields 3.7%, which is still significantly more than its median 2.4% yield during the past decade.

{kind=link}

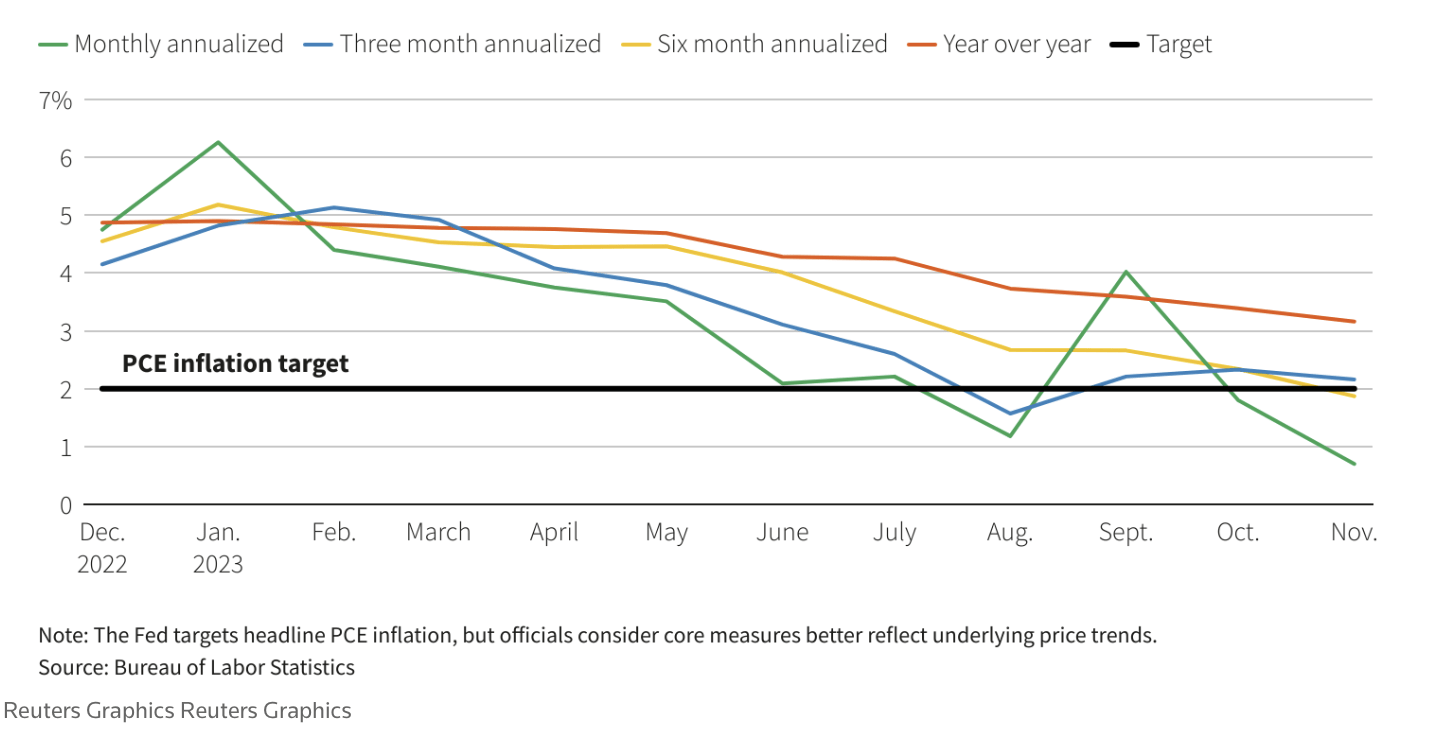

With inflation having hit the Fed's target rates on monthly annualized, three month annualized, and six month annualized periods, we can all agree that it won't take much more confirmation for the Fed to move from where they are to start cutting rates.

If they wait until the yearly inflation rate hits the target, it will be too late.

{kind=link}

Given the current rate of decline in inflation, it can be reasonable to project that the yearly inflation rate will hit the Fed's long-term target by May or June, which means that for the Fed to avoid a hard landing, they would in fact need to start cutting rates by March, at the latest, to avoid a hard landing.

While Powell's Fed's naive decisions during the pandemic caused the massive inflation bout, their rate hike cycle was swift and an adequate response. The risk is now that they are too cautious in cutting rates and do so too late.

I'll be looking eagerly at inflation data next week, and at the minutes from the Fed's meeting on January 30-31st to any hints on their policy.

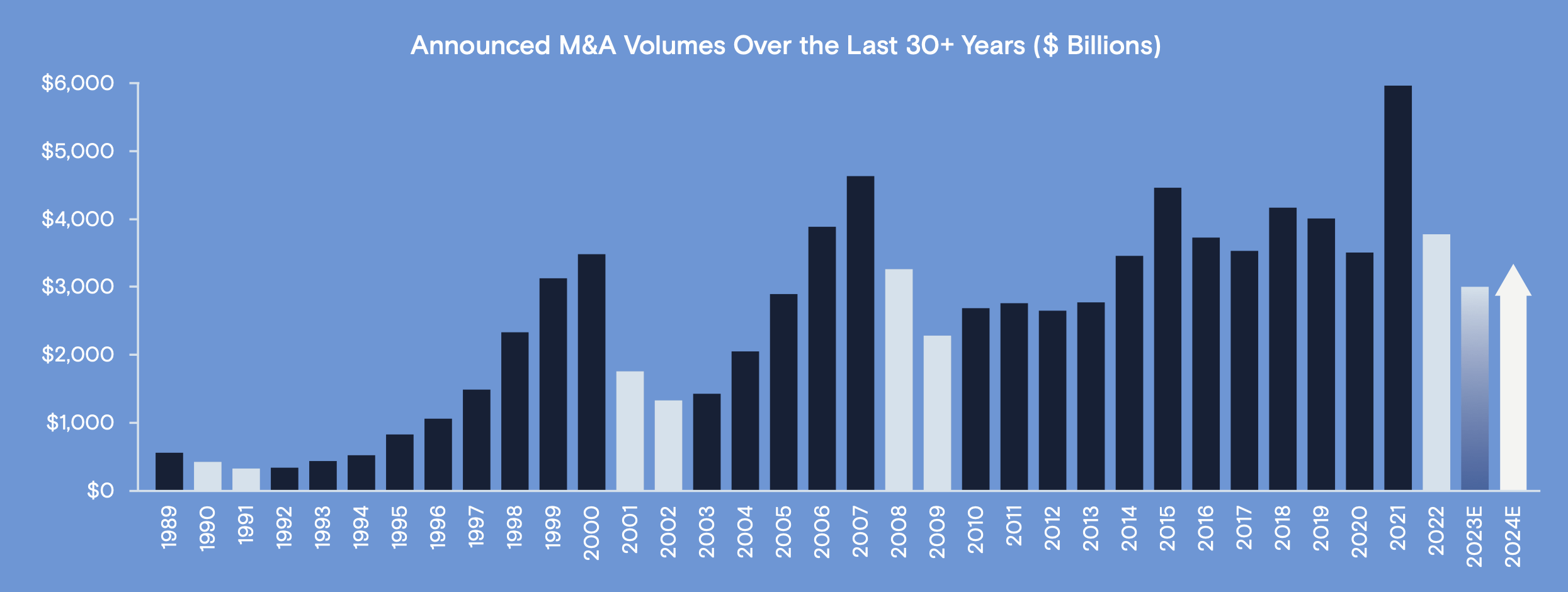

What seems certain in the current environment is that rates will be cut at some point in 2024, which will be great for M&A activity.

Goldman Sachs ( GS ) recently shared their 2024 M&A outlook .

History will show that M&A markets undulate, but pullbacks tend to be reasonably short in duration. Even now, volumes have normalized, and dialogue with corporate clients has been increasing as conditions improve.

Likely M&A will be up in 2024 compared to 2023.

{kind=link}

For the likes of Morgan Stanley and Goldman Sachs (I own both), this is very bullish, and the trend should exacerbate in 2025.

I expect to see MS continue to increase its dividend at 10% per year, and the price to trend up towards $150 between now and 2025. This is 66% above the current share price.

2024 Pick Number 3

Dick's Sporting Goods, Inc. ( DKS ) is the retailer that continues to surprise everyone except those who know where to look.

The stock price increased by 20% in 2023, despite a violent 25% drop in August, which I shrugged off as insignificant and a good buying opportunity for investors.

I said:

What we're really seeing here is a knee jerk reaction to a reduction in inventory, which many retailers have proved time and time again is usually a good decision to keep inventory fresh, and improve performance in upcoming quarters.

While all retail stocks gave back a few percentage points in late December after Nike ( NKE ) reduced its guidance, DKS is still benefitting from an investment cycle in its House of Sports locations and omnichannel experience, which is driving market share gains.

{kind=link}

The stock trades at $141, just off from breaching all time highs of $146, which were reached in 2021.

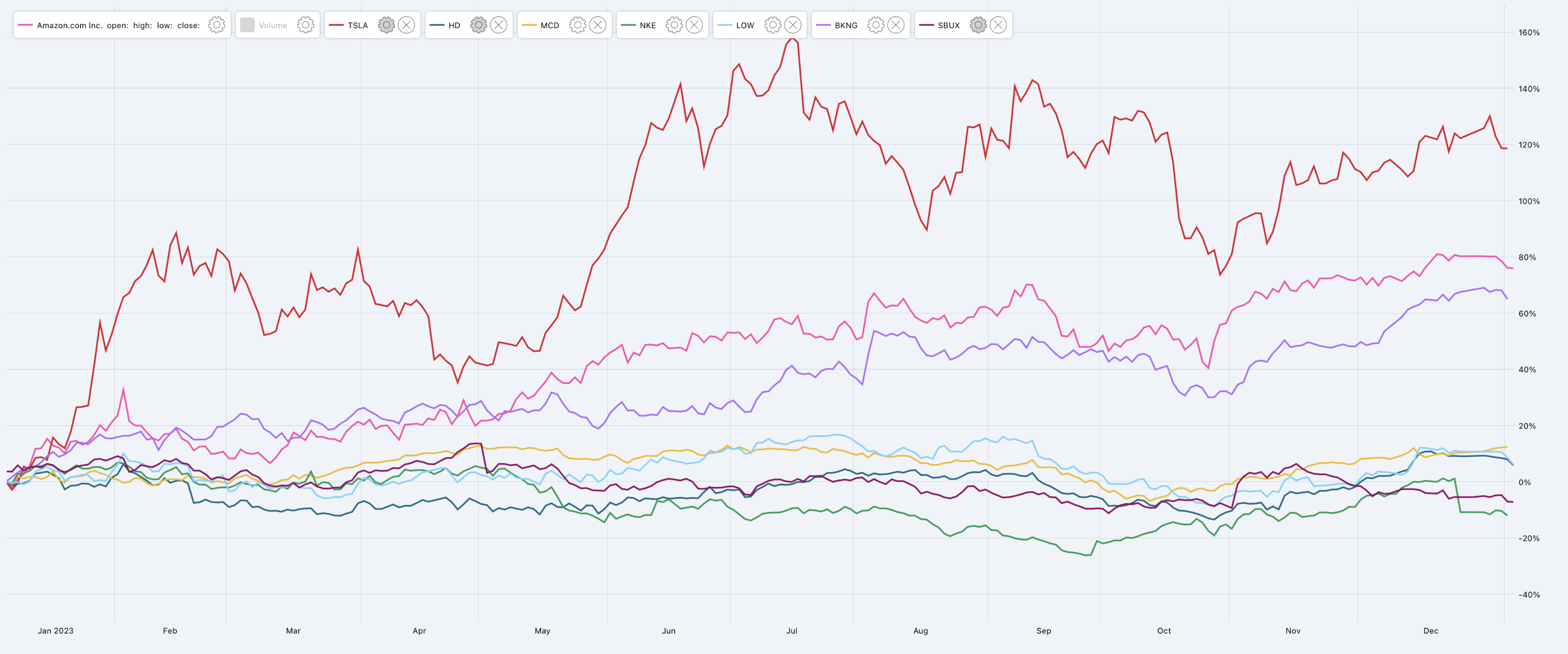

I now expect the stock to break above this level, and trend towards $200 in 2024, as consumer discretionary stocks continue to rise broadly to catch up the sector leaders Amazon ( AMZN ) and Tesla ( TSLA ) which respectively represent 22.9% and 17.8% of the SPDR Consumer Discretionary Index ( XLY ).

For illustration purposes, here are the top 8 constituents of the sector during the past year.

TSLA, AMZN, HD, MCD, LOW, NKE, BKNG, SBUX (Dividend Freedom Tribe)

{kind=link}

What we see is that it is the tech-associated names of AMZN, TSLA, and Booking ( BKNG ) that drove returns for the sector. All of the other names in the top 8 constituents underperformed the S&P 500 in 2023. These include:

I believe that in 2024 we will see a broadening of the performance of the consumer discretionary sector, as I believe that the assumption that a recession will happen is wrong. Everyone was so certain about it in 2023, now they're convinced it's happening in 2024, because "it's got to happen." Why does it? The Fed pulled off a soft landing in the mid '90s, it could do it again.

DKS should benefit as the tide rises for all these names, and remains undervalued with its 2.84% yield. I believe an $18-$200 price would be fair for DKS right now.

2024 Pick Number 2

Verizon Communications Inc. ( VZ ) is a stock that has been awful to own throughout 2022 and 2023.

We came in way too early, but thankfully we have eased into the position slowly.

We purchased some shares in April 2022 at $54, some more in August 2022 at $44, and finally some more in October 2023 at $35.

The consequence is that while the stock is down 28% from our original purchase at $54, the current price of $39 is just 9% below our average cost of $42 on the position.

This is why we buy in increments. In our model High Yield portfolio, for example VZ is still just 2.5% of the portfolio, meaning that we could double the position at the current price.

And that's something we're considering doing.

At the current price, VZ yields 6.75%. This is a whole 2.25% above its 10 year median yield of 4.5%

{kind=link}

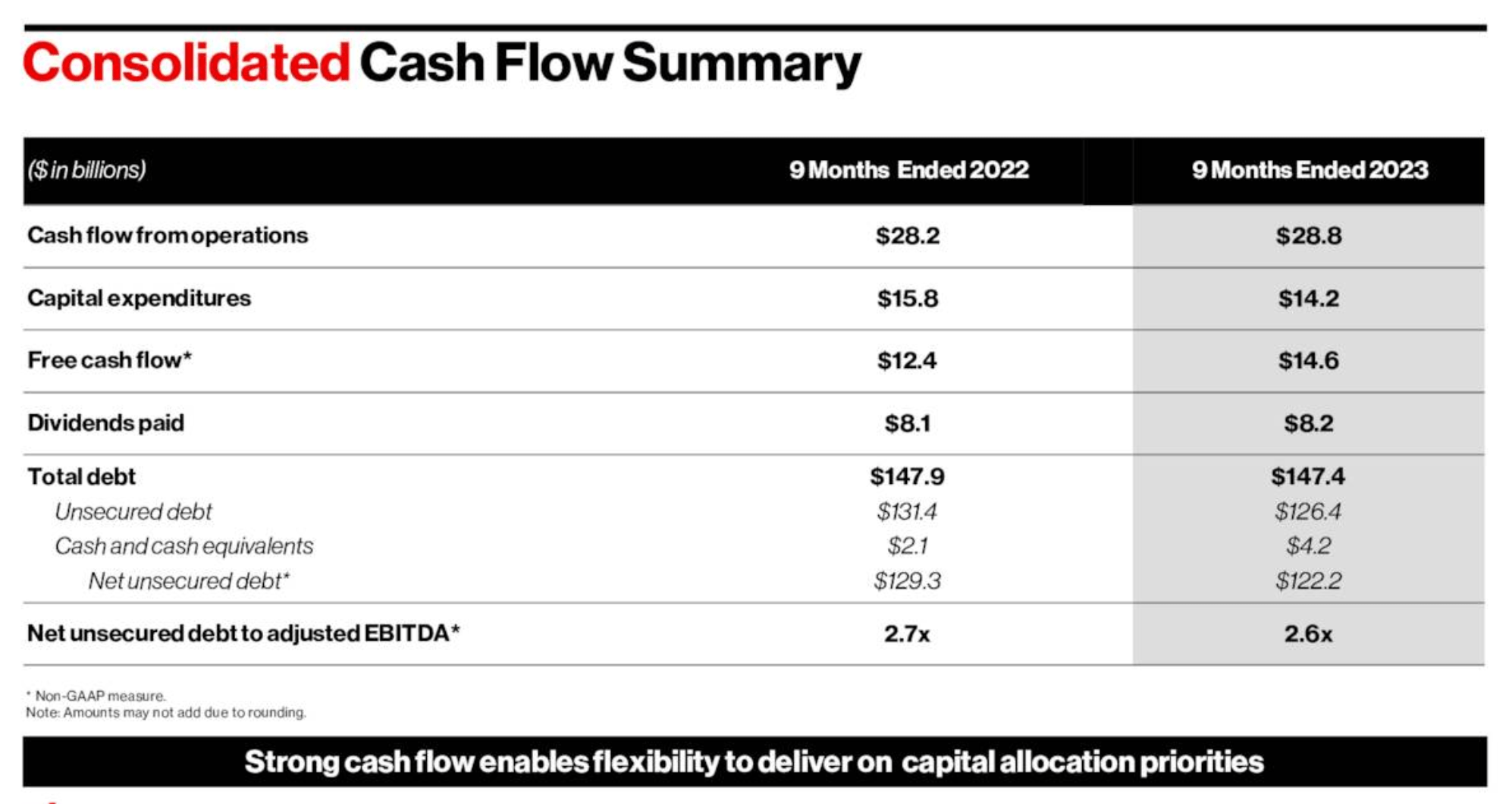

In the first 3 quarters of 2023, the company has already generated more free cash flow ("FCF") than in the entire year of 2022.

It increased its FCF estimate by $1bn, and now expects to generate more than $18bn of free cashflow in 2023.

{kind=link}

Of course, this gives the company the ability to easily maintain its high dividend, and squashes the rumors that the dividend will be cut.

The FCF payout ratio will likely come in at 56%, a reasonable ratio by all accounts.

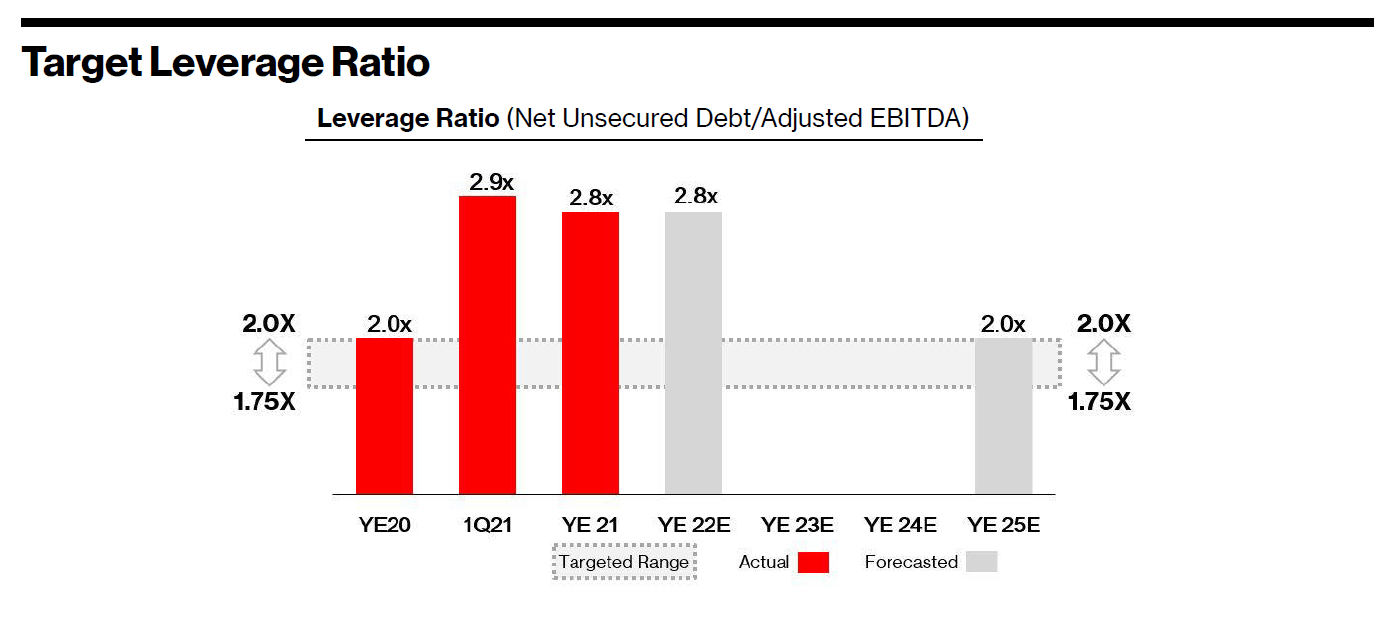

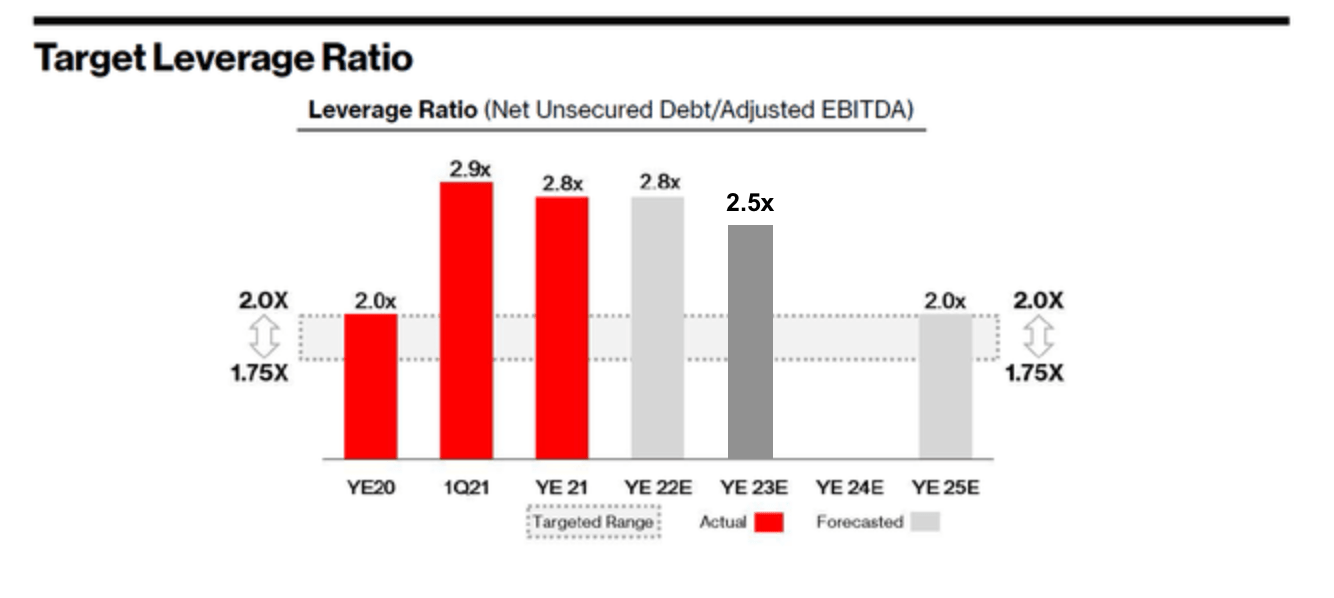

The reduction in debt that was witnessed -- despite CAPEX coming in at the higher end of the range for the quarter -- was encouraging, and it seems very likely that VZ will manage to reach its target leverage ratio in the next two years.

The firm is currently entering an era of lower CapEx after acquiring a lot of spectrum, and this should further enable the firm to lower its debt ratios.

This was the chart they presented at the investor day in 2022.

{kind=link}

And this is what an updated one will likely look like by the end of fiscal 2023.

{kind=link}

This also means that a year or two from now buybacks will be on the table, as management suggested in the Q3 earnings call (emphasis added):

So what we have said before was that we want to come to a ratio of 2.25 over the net debt to EBITDA and we are going to continue to work our way down and that is a primary goal for us. Number one in the capital allocation is to invest in our business. Number two is continue to put our board in a position so they can increase our dividend. We are on 17 years of consecutive increases and thirdly we're paying down our debts. When we come to that ratio, we will start having a conversation about buybacks.

But we want to do buybacks not that one-off or something. It has to be a consecutive program all the time. So, but we're not there yet. But the team is doing great job. Tony talked about the 2.6 billion they we reduced debt this quarter with the tenders were down. So we will continue to do that with the cash flow. That's where we are yielding right now.

At the current rate of reduction of $2.5bn per quarter in net debt (which could accelerate in 2024), we're about 6 quarters away from that 2.25x multiple, which means that by the end of next year, that $2.5bn-$3bn per quarter could theoretically be funneled into buybacks, offering a massive buyback yield.

This would be extremely welcome, as it would pave the way for sustainable dividend increases throughout the next decade.

I believe the worst is over for VZ, and while I'm happy to have bought shares at $35, which was close enough to the $32 bottom, I'm even happier to buy shares now at $39, as the stock is gaining some upwards momentum.

VZ could increase by 50% to $60 over the next two years, and I wouldn't be the least surprised.

2024 Pick Number 1

I believe 2024 will be the year of the real estate investment trusts, or REITs.

Rexford Industrial Realty, Inc. ( REXR ) happens to be one of my absolute favorite REITs, because it is well managed, has high embedded growth, is in a great industry with REITs, and even better geographical concentration within its industry, and has a brilliant niche within its geography.

It is a company which is doing everything right.

REXR currently trades at $55 and yields 2.7%. I believe it could increase to as much as $85 in 2024, which would be 55% higher than the current price.

{kind=link}

Let's run through the scenario for Rexford once again, as I believe it is an absolute bargain at this price.

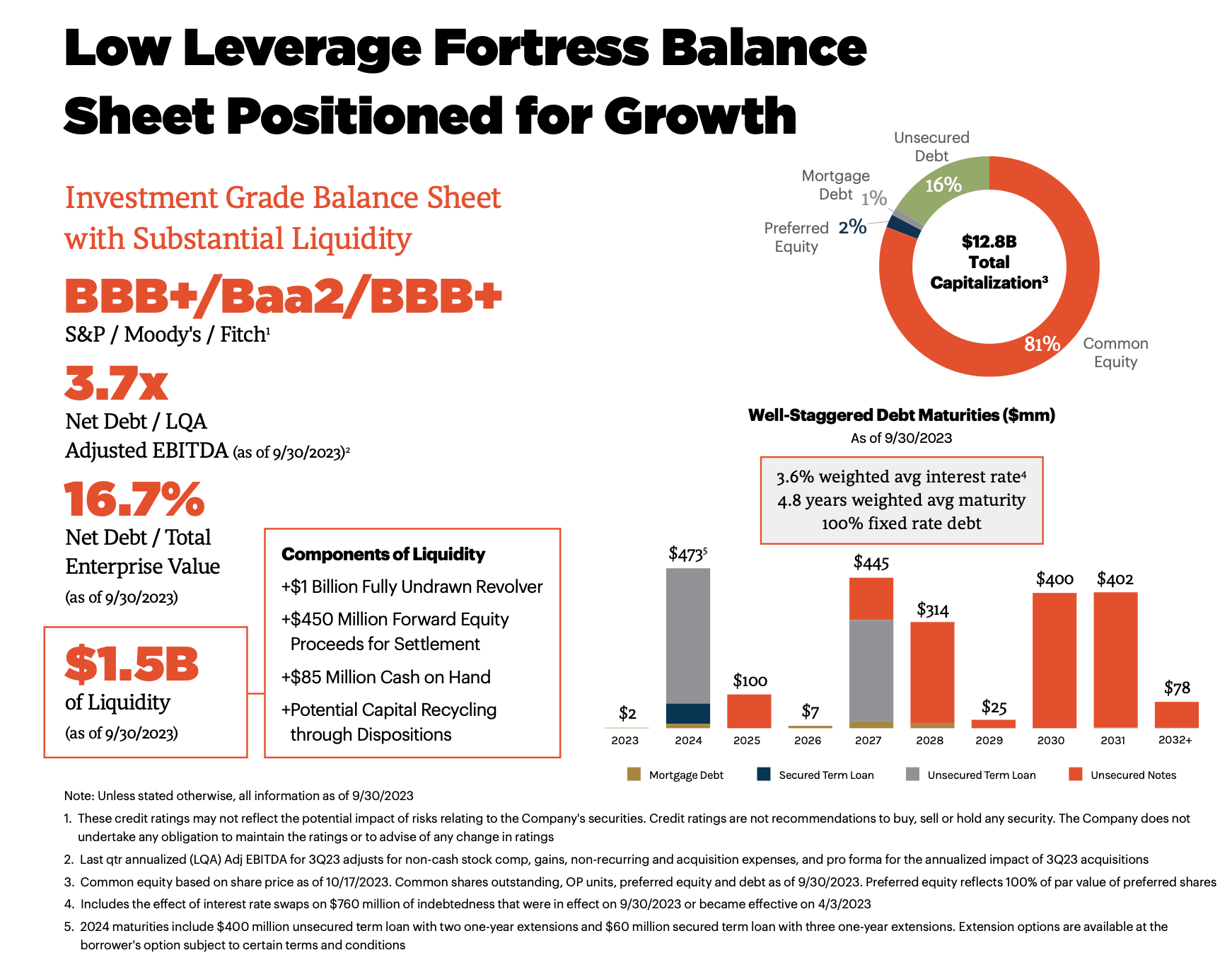

First, let's address the elephant in the room which dropped REITS hard in 2022 and 2023: high interest rates.

REXR was barely concerned, as for one it has a low 17% Net Debt/EV ratio, 100% of its debt is fixed rate, and there are no major maturities before 2027.

This didn't stop it from tanking along with all other REITs.

{kind=link}

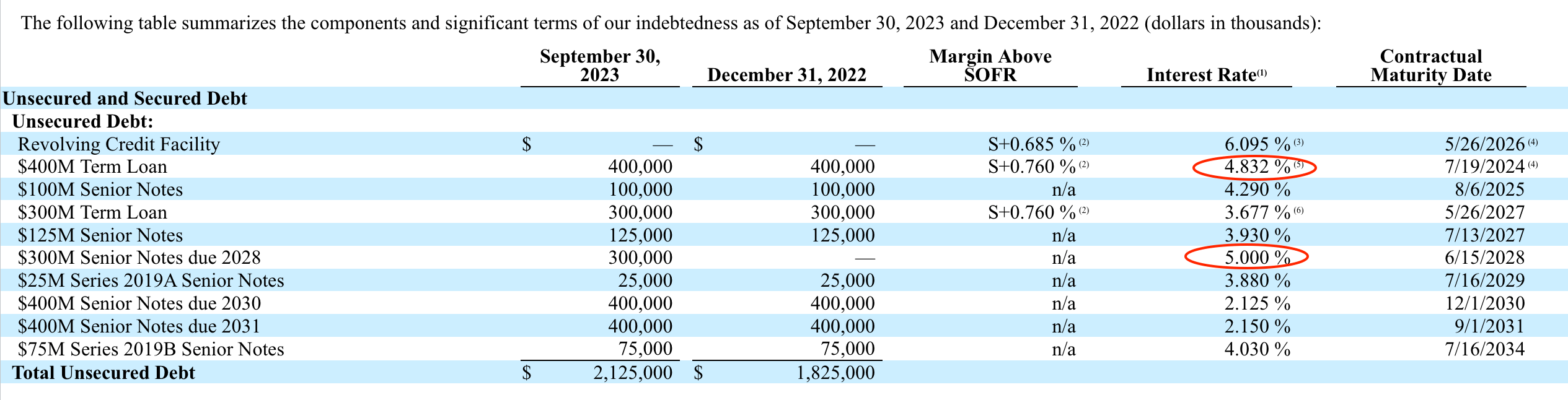

One would note from the slide above that the $400mn unsecured term loan is expiring in July 2024, but this shouldn't really be feared.

For one, this term loan has 2 one year extensions baked into the contract, to be utilized at the discretion of the borrower, which could push the actual expiration to July 2026 if REXR desired.

Furthermore, the rate paid on this term loan is 4.83%.

{kind=link}

In the first quarter of this year, the company took out a $300mn senior loan at 5% interest rate.

Replacing the loan, therefore, wouldn't likely come at a very expensive cost, and should have a negligible impact on REXR.

Finally, about 40% of its debt is expiring in 2030 at rate of 2.12%, guaranteeing the company a nice cost of debt throughout the rest of the decade.

In other words, REXR is largely untouched by the whole higher rates squeezing REITs rationale, yet the share price still came down with the rest of the sector.

You could argue that it might impact acquisitions to a certain level, as the project-related debt would be impacted, but this is such a marginal impact for REXR that I'm not bothered.

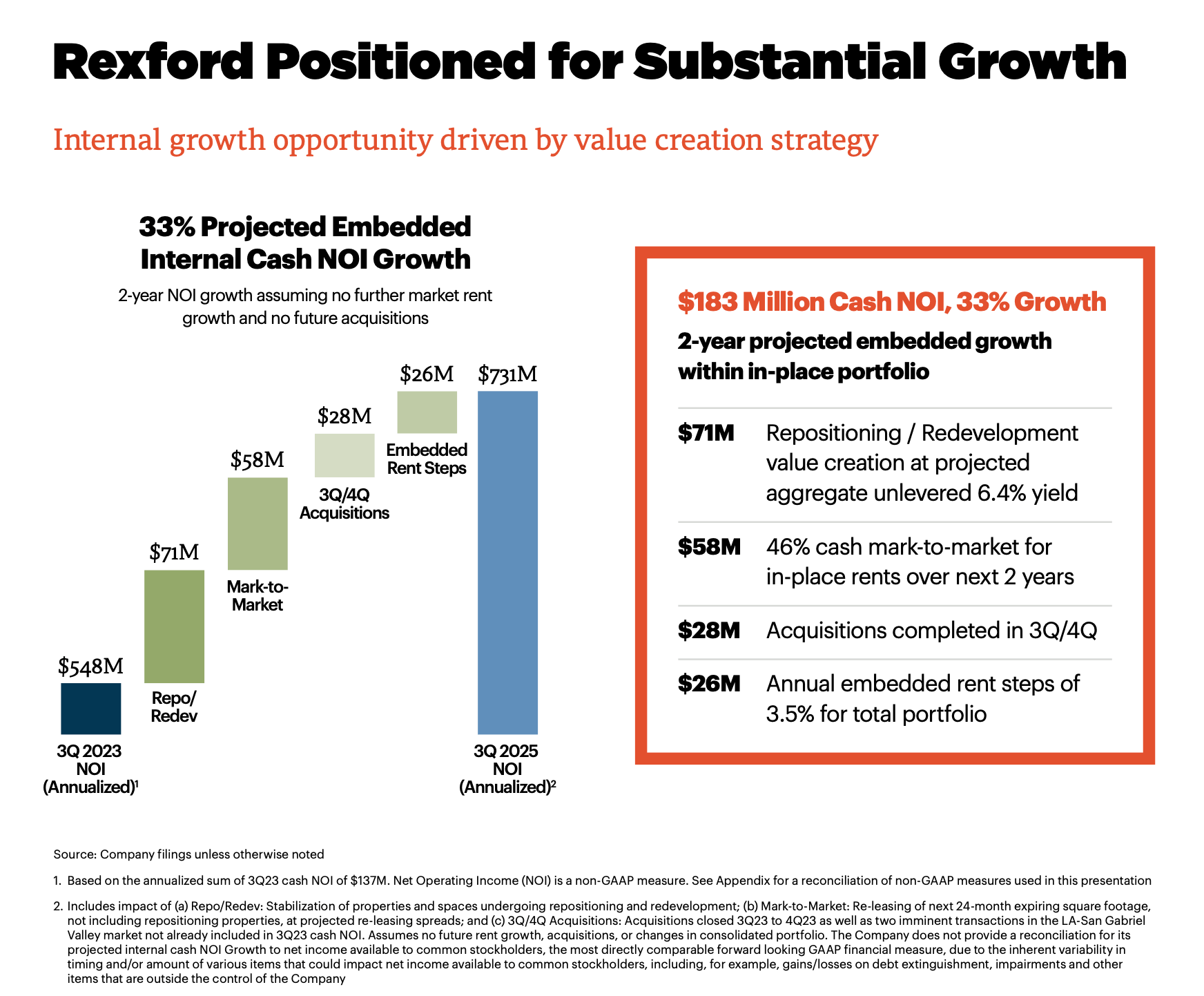

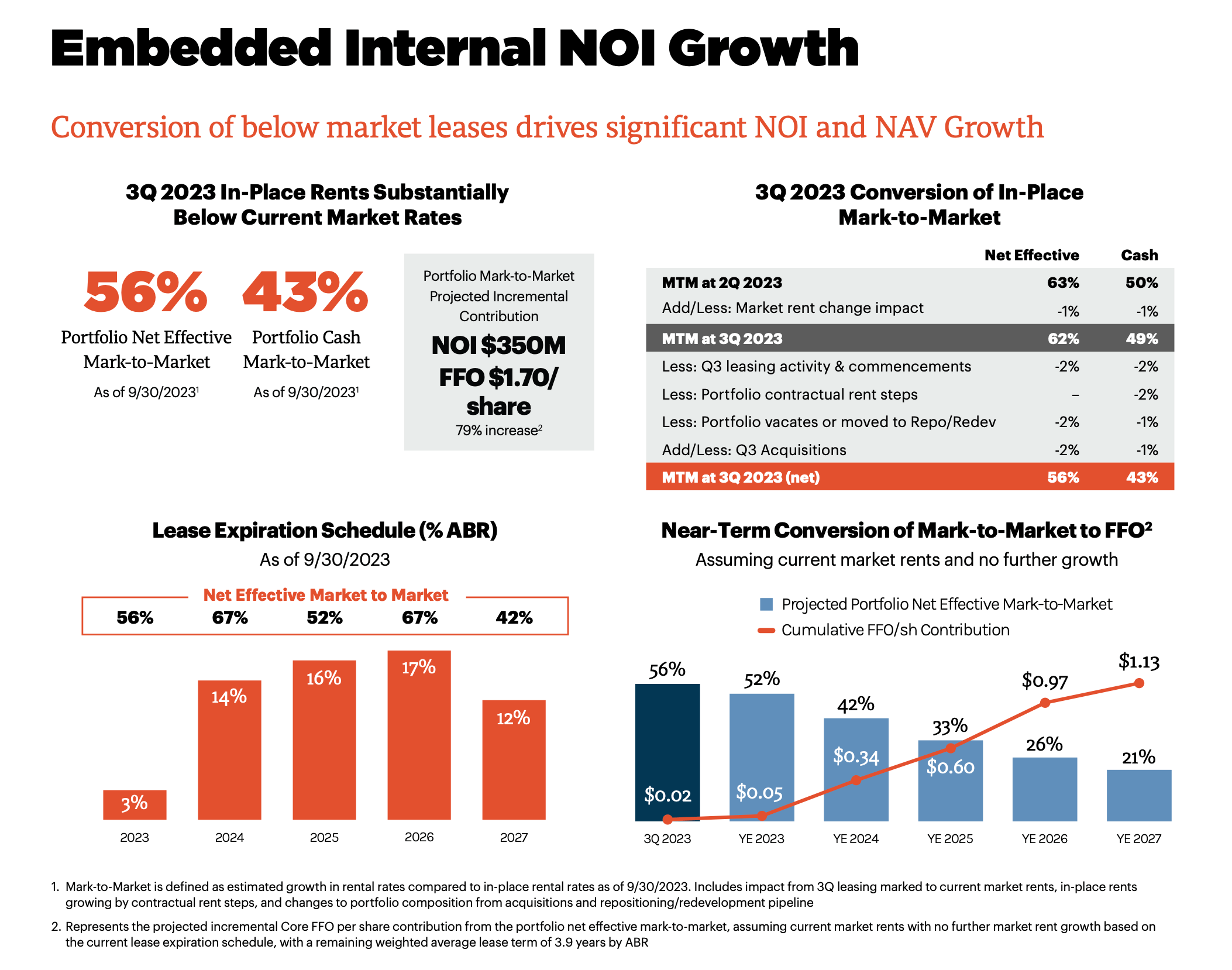

With the existing portfolio alone, REXR is set for substantial growth.

They have become experts at repurposing and redeveloping properties to get maximum yields from them, and expiring leases have massive mark to market rents.

{kind=link}

This is to say that the current in-place rents are substantially below market rents, and as leases expire, these rents are resigned at much higher rates.

Year to date, REXR has had cash mark-to-market yields of 43%.

{kind=link}

Even assuming no further growth in rents, and no other sources of growth, marking the current portfolio to market would result in 10% FFO growth yearly between now and 2027.

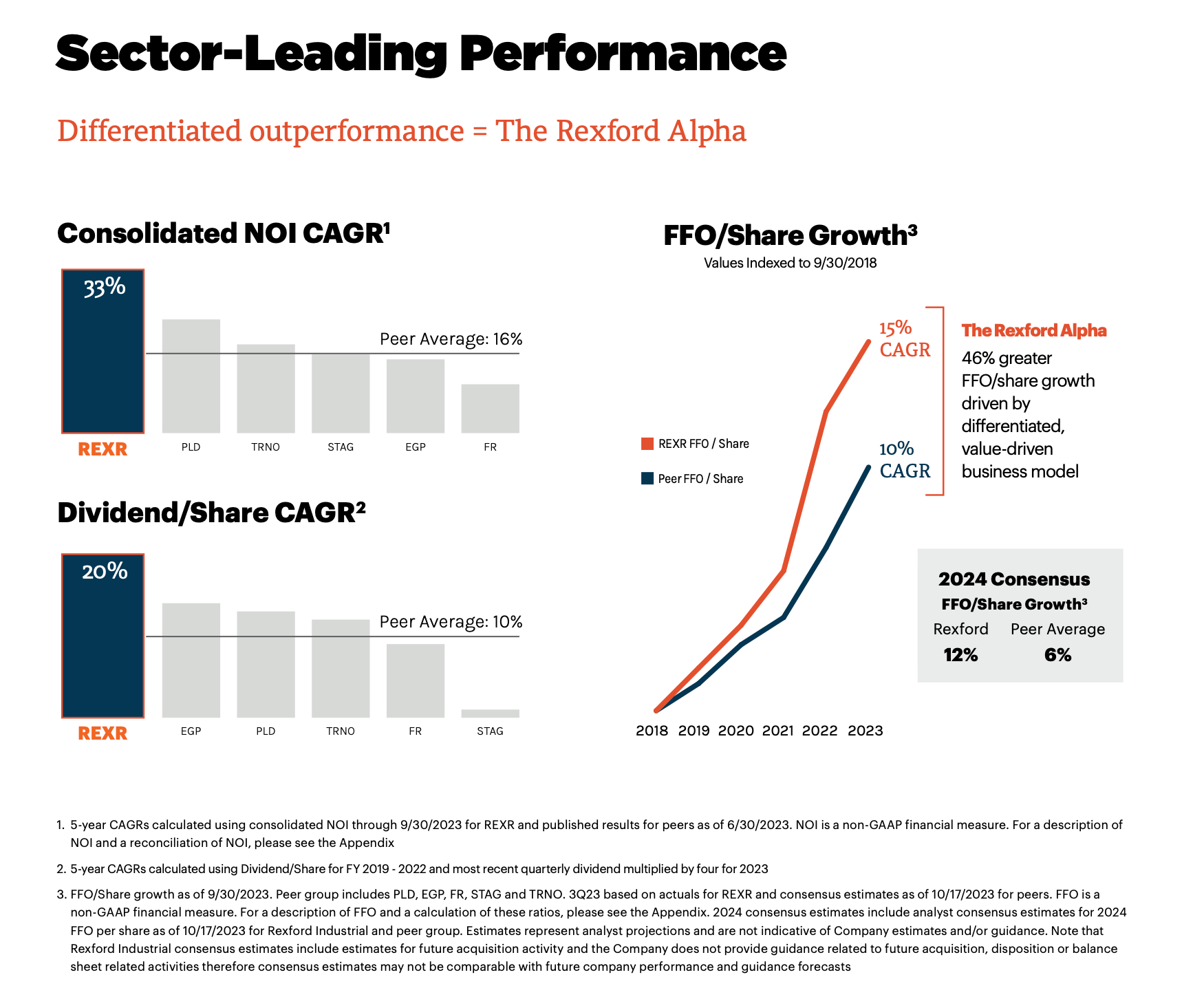

The consequence of these great numbers is that REXR has been growing faster than the competition and paying out that growth as increased dividends.

{kind=link}

What is it that makes REXR better than the other industrial plays?

I explained this in July when making the case for certain industrial geographies over others.

Below is the segment of that article which is relevant.

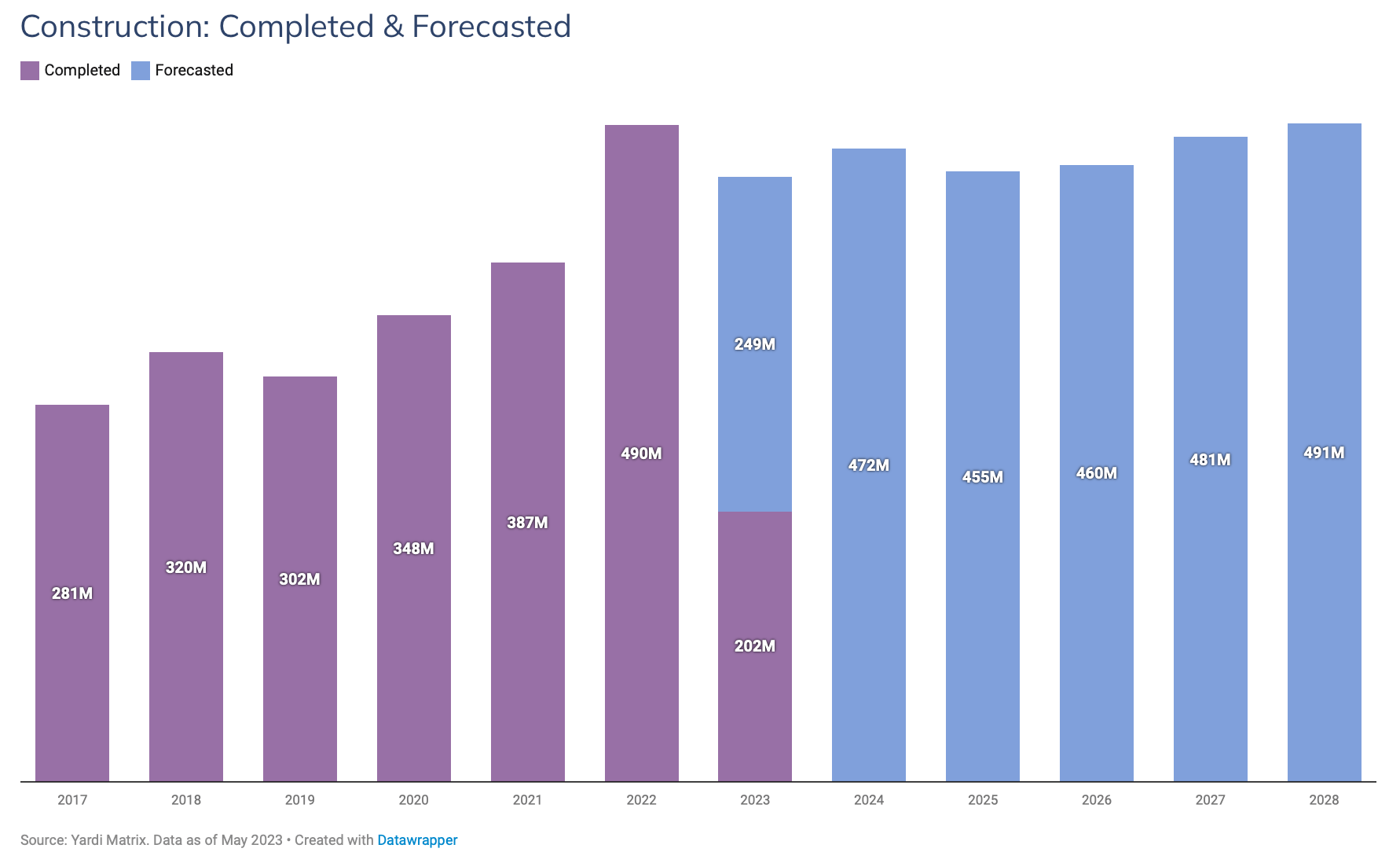

While the rate of construction has slowed down, there is still a lot of square feet which will be coming onto the market in the next 5 years.

This influx of supply will hit different markets in different ways.

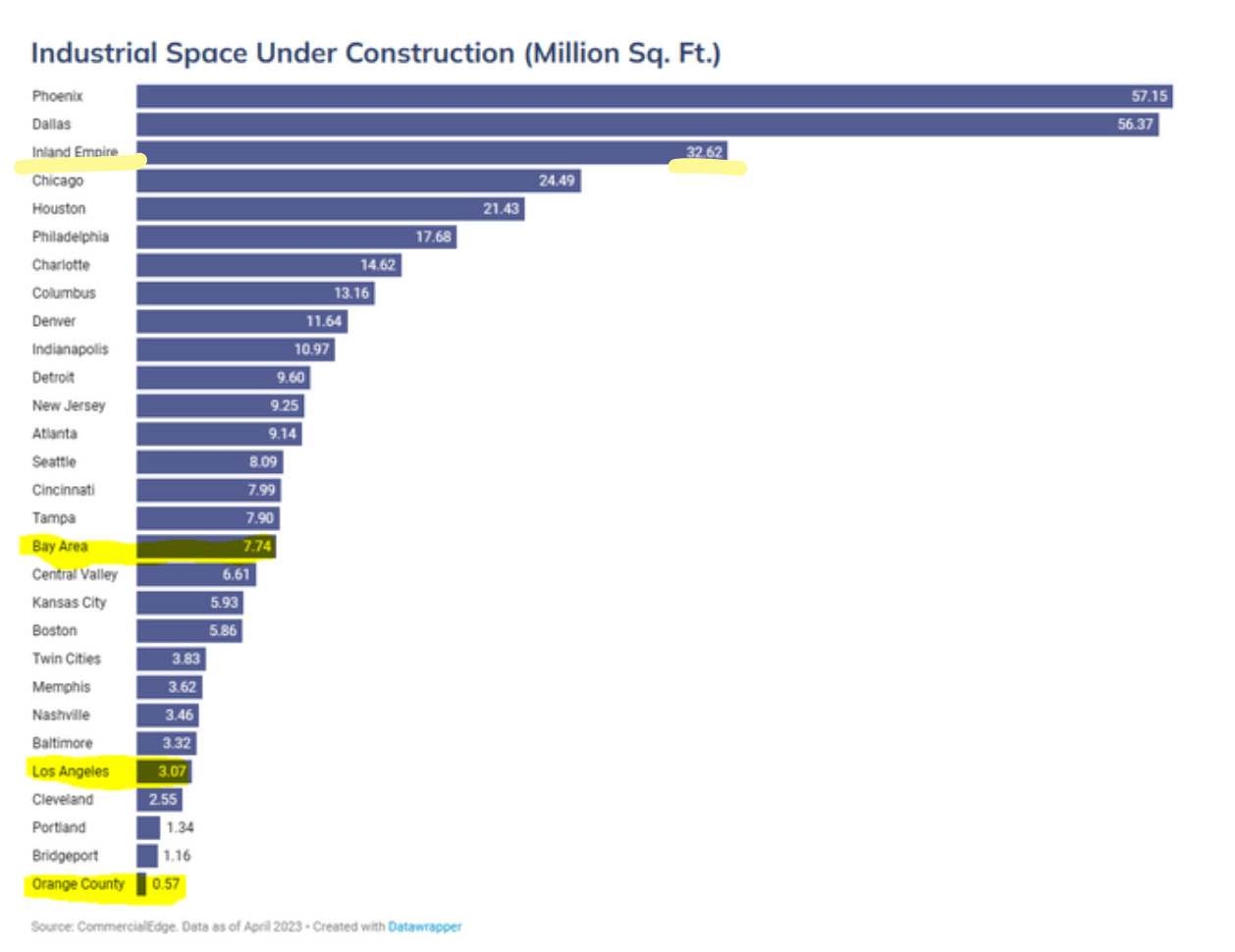

The graph below shows industrial space which is under construction in key cities.

The yellow highlights show the markets to which Rexford is exposed.

As you can see a large amount of the industrial space under construction lies in Phoenix and Dallas.

Except Inland Empire, which is an outlier in the industrial real estate market (and home to Amazon ( AMZN )'s mega fulfilment center), Rexford's key markets are on the lower side of new supply.

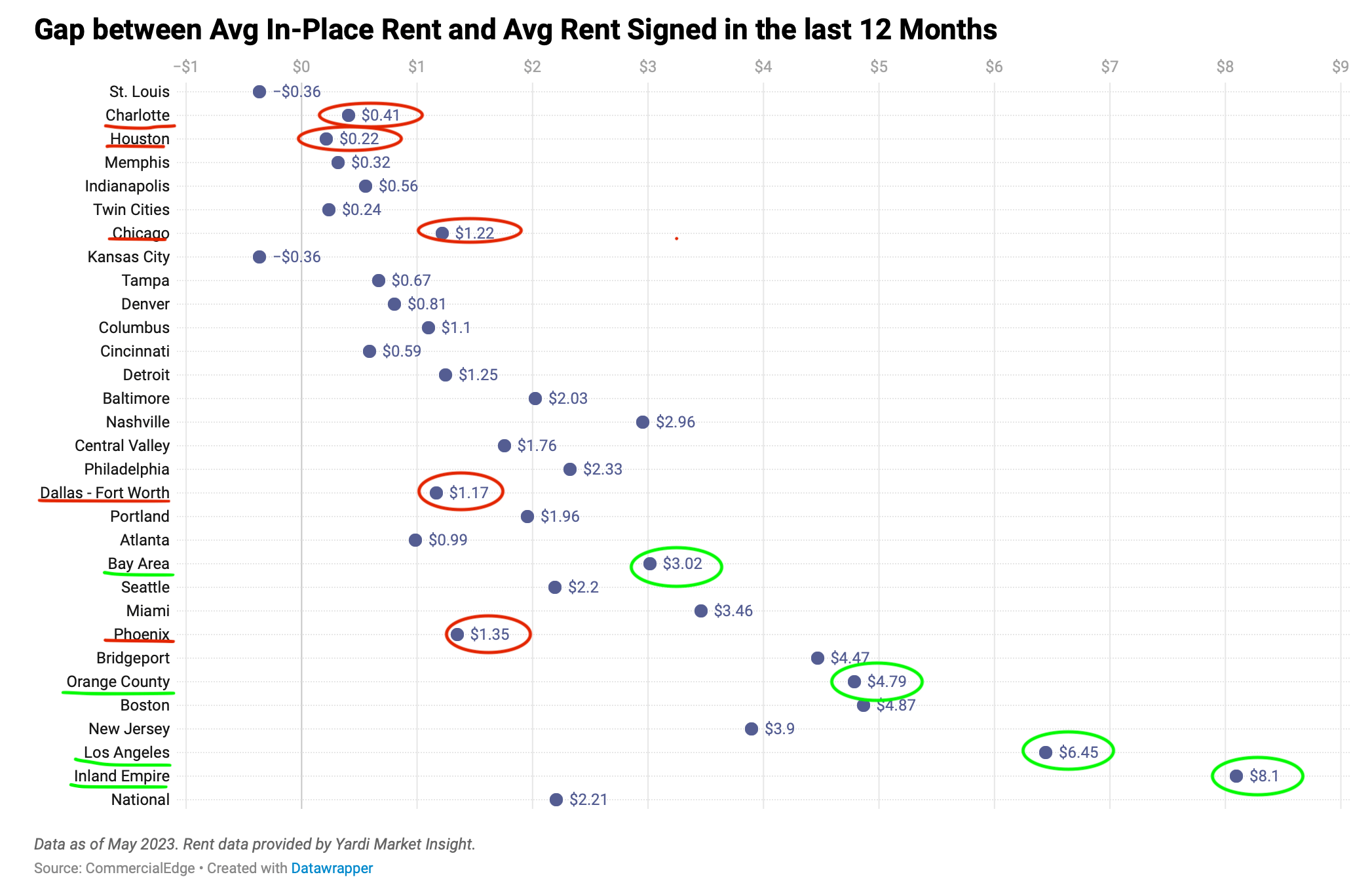

This is by design and as you can see, the leasing spreads have been particularly attractive for Rexford's markets, whereas they've been below the national average for markets with high construction.

Once again, Inland Empire is an exception.

This is by design. By focusing on Southern California, and in particular LA, which represents 54% of their square footage, have virtually no new construction permits, no available land, and remain in strong demand because of their proximity to ports, and the demand derived from LA being a huge entertainment hub in the US.

{kind=link}

{kind=link}

{kind=link}

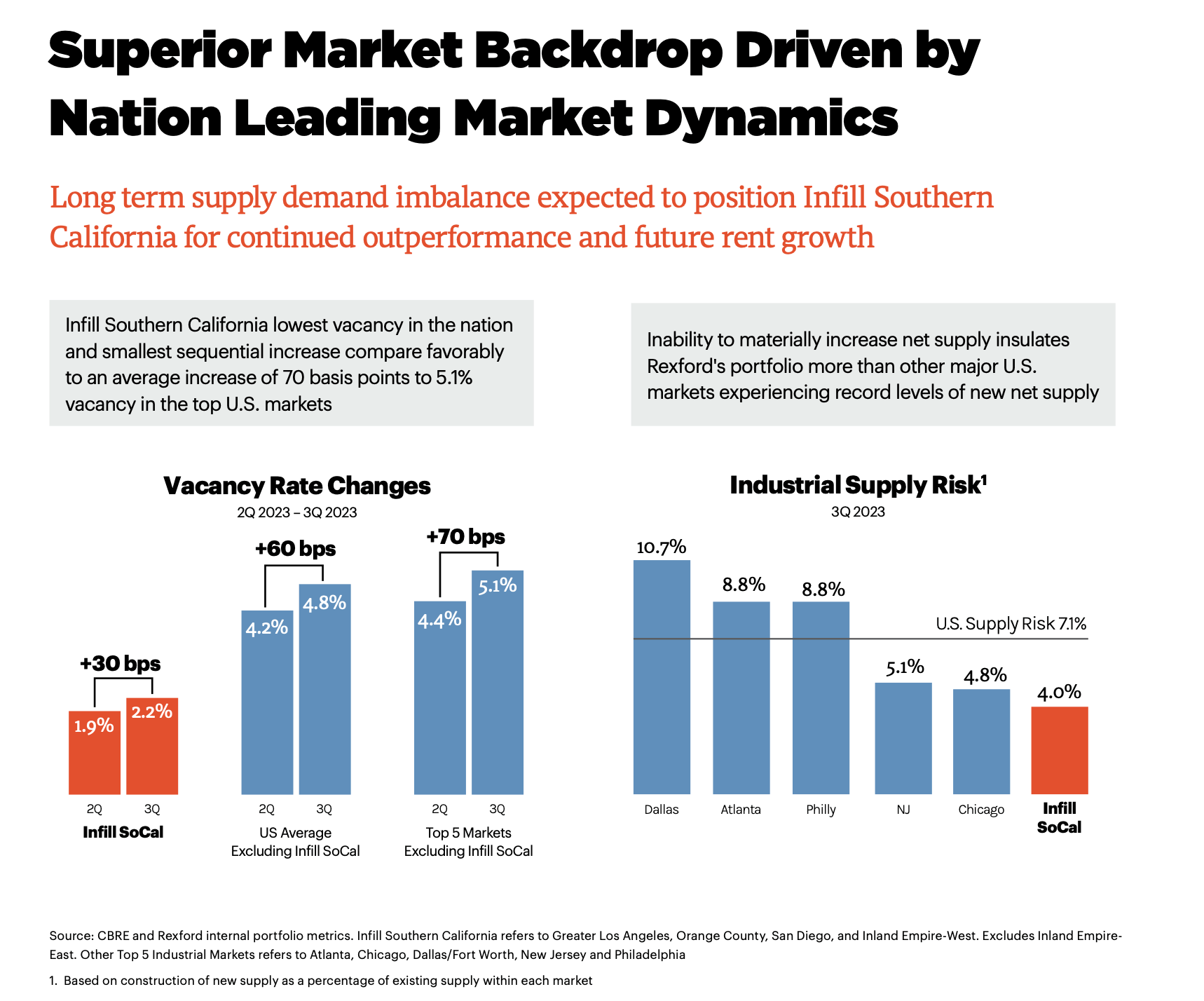

This has clearly continued to play out in between Q2 and Q3, where vacancies have increased to 5% on average nationwide, and only 2.2% in Infill SoCal market.

{kind=link}

In Dallas, which I highlighted as particularly prone to oversupply, they have reached 8% vacancies.

Which market do you think will have a better time at increasing rents? The one where there is 2% vacancies, or the one where there is 8% vacancies?

Yes that was rhetorical.

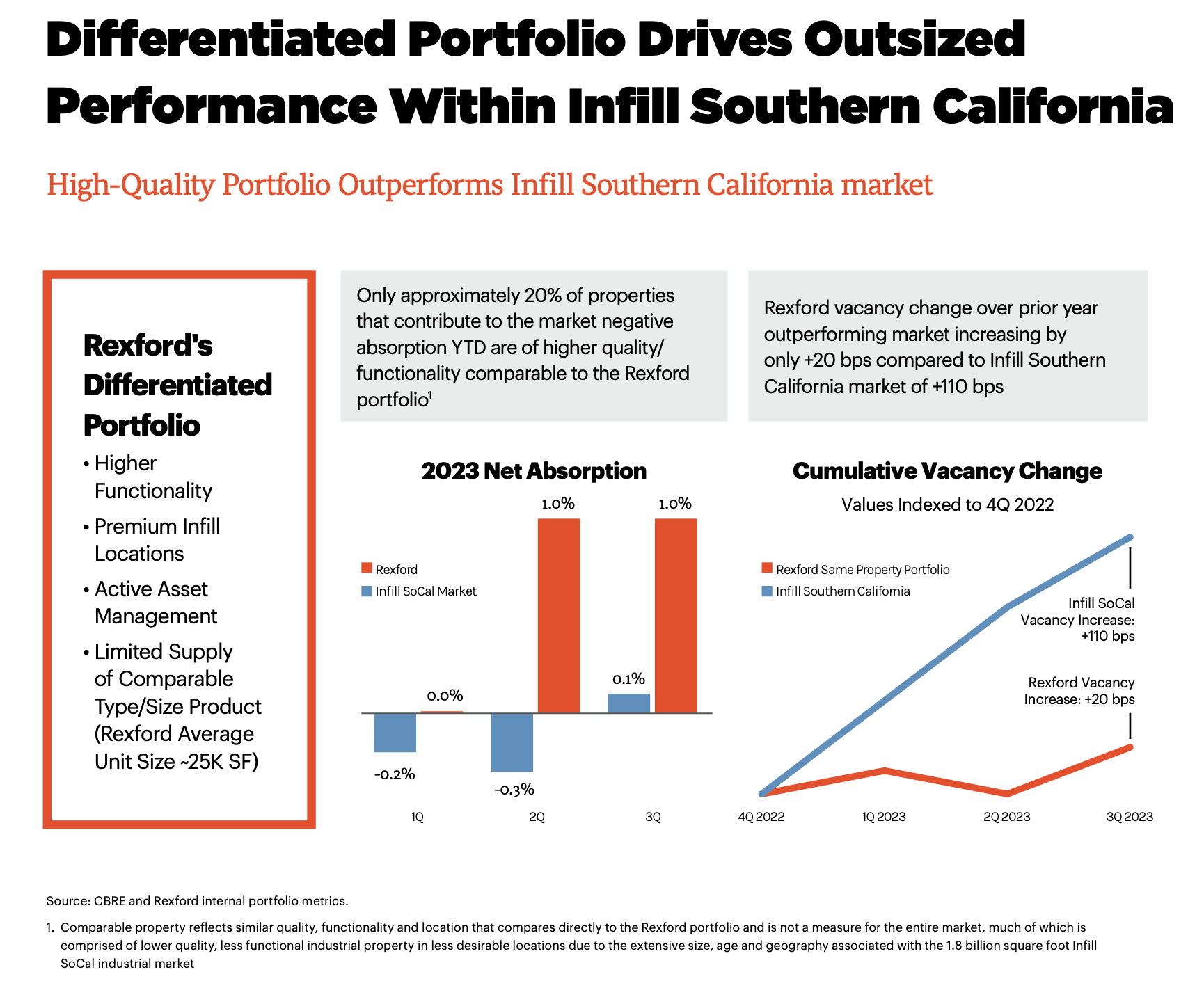

Furthermore, Rexford stands out even within the Infill SoCal market.

By focusing on smaller units, with high functionality and premium locations, REXR has had positive net absorption of 1% in both of the last quarters, meaning it has rented out more space than has been vacated. Occupancy remains at 97.75%, suggesting occupancy in line with the industry. It should be noted though that throughout the past 3 quarters, REXR vacancies increased just 20bps vs. the market's 110bp increase.

{kind=link}

Rexford industrial is continuing to show their expertise in their geographic market, and their business savviness in selecting this particular port market as their focus.

It is a bargain today, and should be added to investor's portfolios.

Conclusion

This was once again a much bigger article than I had planned to write, as I really wanted to highlight the case for all 5 of the stocks that we were presenting.

They are all running on certain trends which are still early. Maybe a few won't quite play out as I imagined or not on the timeline I wished, but all provide value and great income in the form of yield and dividend growth.

I have included low yield picks with high growth, and high yield picks with lower growth, which should create a well-balanced addition to anyone's dividend portfolio in 2024.

For further details see:

The Top 5 Dividend Stocks For 2024