TXMD - TherapeuticsMD: From Fallen And Forgotten To Cash Cow

2023-05-23 09:00:35 ET

Summary

- TXMD is a pharmaceutical company that experienced a tremendous transformation in the last year, fully transforming into a royalty-only company.

- The company sold all its assets and paid down all its debt and is now expecting 8% of royalties plus $30 million in milestone payments from Mayne Pharma.

- The $35 million market cap with $11 million in net cash makes it dirt cheap even assuming flat to no growth in revenues from the licensed drugs.

- Using a DCF model with 3 scenarios for growth/milestone payments I conclude that TXMD's fair value is around $5.6, implying a 30% undervaluation.

The background: from a near-bankruptcy experience to the Mayne deal

The history of TherapeuticsMD (TXMD) is made of many ups and downs. From being loved to the market before and during the FDA approval period - when they traded at an EV above $1.5 billion and analysts were forecasting peak sales in the billions - to today’s $35 million market cap and the drugs doing roughly $80 million in sales a year combined.

The company was able to launch three main products: ANNOVERA, a one-year vaginal ring, BIJUVA, a drug for the treatment of hot flashes, and IMVEXXY, for the treatment of Dyspareunia. The FDA approved these three products between 2018 and 2022 (with the latest sNDA for ANNOVERA approved in mid-2022). However, the market’s expectations for billions of dollars in peak sales and fast growth rapidly faded when it was clear that the commercialization and expansion strategy was not delivering as fast and as profitably as forecasted.

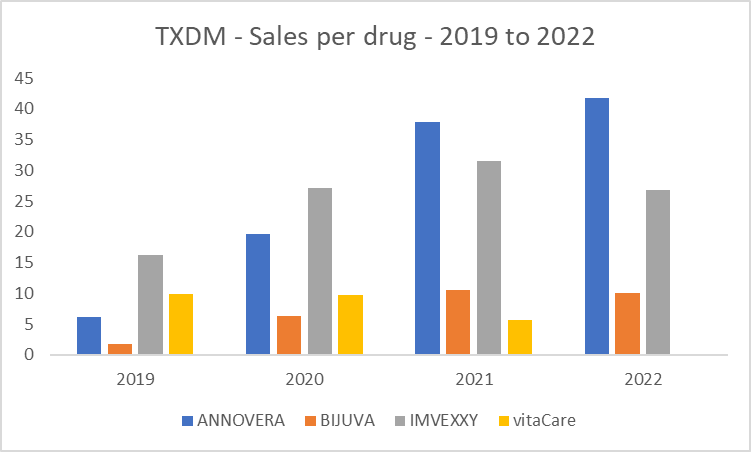

TXMD - Sales per drug (TXMD Filings)

{kind=link}

These are the actual sales per drug, where we can notice ANNOVERA being the leading product, while the sub-tier names like their vitamins (vitaCare) zeroed out during the period. This weighted on the valuation, which rapidly declined and the stock is down 98% in the last 5 years.

So at this point you would ask: what’s the catch with a dead pharma company, with a questionable past and no residual assets? Well, the royalties. TXMD sold down all of its assets for a lump sum AND an 8% royalty on future sales up until the expiration of the patents. This means that you have the opportunity to buy a stub-like company with the chance of plenty of cash coming in the next few years.

In 2022 alone many things happened, but the key events that led to the current opportunity are the following:

-

The company was the object of a takeover offer in August 2022, by a private equity firm called EW Healthcare Partners for a 380% premium at $10 per share, the offer failed as the minimum tender % of capital was not subscribed (only 30%)

-

Close to bankruptcy, the company finalized a $140m deal with Mayne Pharma, where they sold all their products and became a royalty-based company

The opportunity going ahead: Mayne Pharma and ANNOVERA opportunity

The deal was structured as follows:

-

(1) a $140 million lump payment that TXMD used to pay down outstanding debt and liabilities;

-

(2) up to $30 million in milestone payments divided into $5 million for sales above $100 million, $10 million for sales above $200 million, and $15 million for sales above $300 million;

-

(3) an 8% royalty rate to be paid yearly on net sales of the three licensed products.

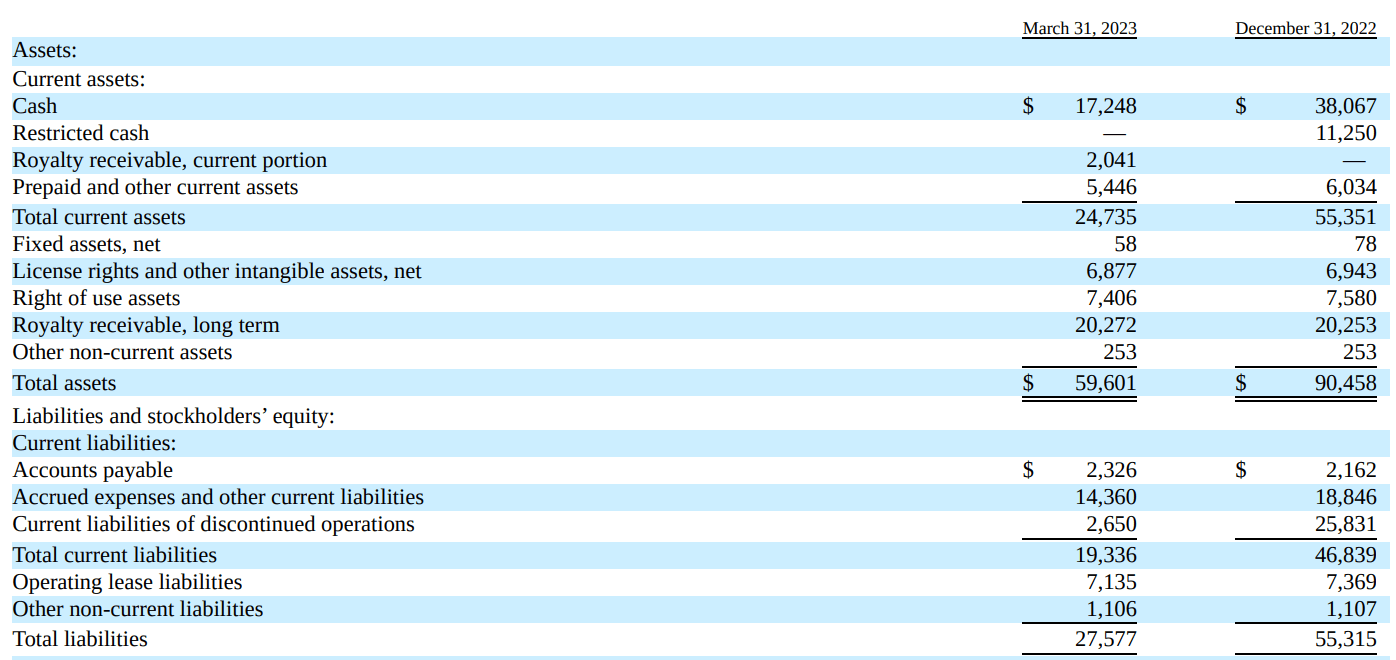

This is what the balance sheet looks like now after the closing of the deal, and the first quarter of Mayne operations:

TXMD Balance sheet (TXMD 10-Q)

{kind=link}

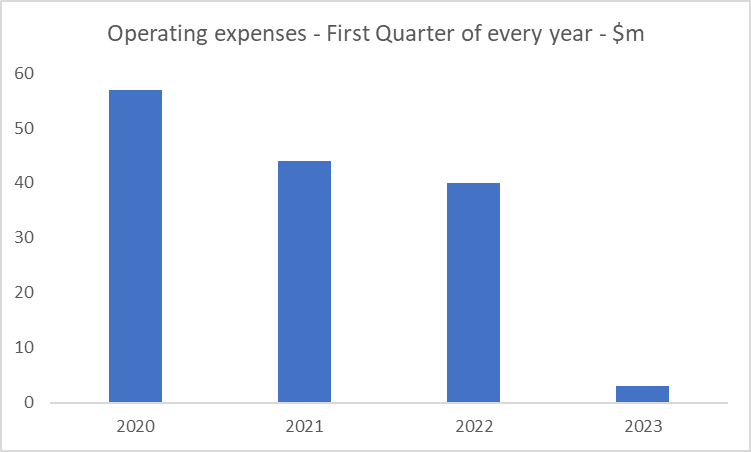

Net cash sits at around $2-3 million, as certain liabilities have been paid down during Q1 2023, and the first royalty receivable has been accounted for ($2 million for the quarter). And if we compare operating costs between Q1 2023 and Q1 2022, we can immediately see the massive slash (that should although continue to reach even better margins): from $40 million in operating costs to $3 million in the last 3 months.

{kind=link}

However, I would expect this figure to drop even more next year as the remaining liabilities (lease and accrued expenses) zero out. Right now TXMD has a $44 million market cap and an EV of around $40 million. Which is clearly not accounting for one big factor: ANNOVERA’s success. In fact, this drug has clearly been underperforming for years, but this was due to two reasons: (1) the inability of TXMD to properly market the product, which was part of many failures by former management; and (2) insurance is not covering the product yet.

For comparison, the most direct competitor, NuvaRing, is making roughly $1 billion in sales per year. The royalty rate on such sales alone would be 2x the current market cap of TXMD. And in my opinion, ANNOVERA is even a better product than NuvaRing (the competitor), given:

-

ANNOVERA can be used for 13 cycles, or basically 1 entire year, compared to NuvaRing’s 1 month of usage

-

ANNOVERA contains lower quantities of hormones, which makes the product more sustainable for more extended periods of usage

If Mayne is able to negotiate with large insurance companies and convince them to cover ANNOVERA it could be a much more successful revenue story. Indeed, I estimate that it could easily capture 15-25% of the market share from NuvaRing, considering (1) higher quality, and (2) higher durability. This move alone would result in hundreds of millions in sales of ANNOVERA and multiples of the current market cap in royalties for TXMD.

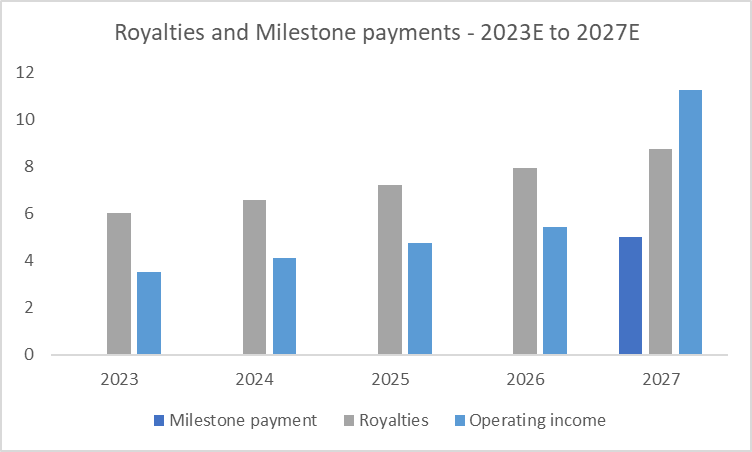

Royalties and Milestones (Author's estimates)

{kind=link}

This is a forecast for sub-optimal growth on ANNOVERA, at around 15% per year for the next 4-5 years, then at 5%. I would expect a more realistic growth rate in the high 20% in the first years as Mayne seems better equipped to properly market the drug. However, those conservative assumptions still yield decent results like the $6-8 million in operating income per year for TXMD (generous considering the $40 million market cap).

What could go wrong: execution and management risks

There are two main risks I can highlight in this opportunity that at first may seem too cheap to be risky: (1) execution risk, as Mayne Pharma needs to be trusted as they deploy and market the drugs; and (2) management risk the current leadership of TXMD has to be 100% concentrated on cutting costs to the bone and on returning all of the capital to shareholders.

Execution risk is quite real considering that Mayne is itself in a complex operational restructuring process, during which they sold down their manufacturing facilities in the US and some of their assets. My opinion is that they cut a deal with TXMD because they saw the massive undervaluation of their drugs, so we should expect them to focus a lot on ANNOVERA and the other products. But the risk of not properly marketing the products, or that NuvaRing has acquired an insurmountable MOAT during these years is real.

Management risk is also a thing as the sitting leadership may continue to spend too much, compared to both incoming royalties and the market cap. This will erode shareholders' value, which given the small size is sensitive even to “small” spending items in the $100-500k range. And that range is very small for a company that was spending hundreds of millions 2 years ago.

What’s the proper fair value for TherapeuticsMD? Let’s model it out

I already gave a mild scenario where Mayne was able to get a sub-optimal growth rate, and royalties came in in decent amounts yearly for TXMD. But what if we consider other (not-so-improbable) scenarios where the drugs become a success?

Let’s understand the opportunity by running three different scenarios:

-

Worst case: Mayne actually fails to complete the turnaround, starts to struggle financially, and declares bankruptcy. The worst case in this specific case can’t rule out the out-of-business situation (we are not buying Apple after all). I assign a probability of 15% to this scenario and an associated fair price of $0.

-

Medium case: Mayne is able to properly market the drugs in the short-medium run, and gains some market share from 2025 and beyond, as insurance companies start the coverage. I assign a probability of 60% to this scenario and an associated fair price of $5.1.

-

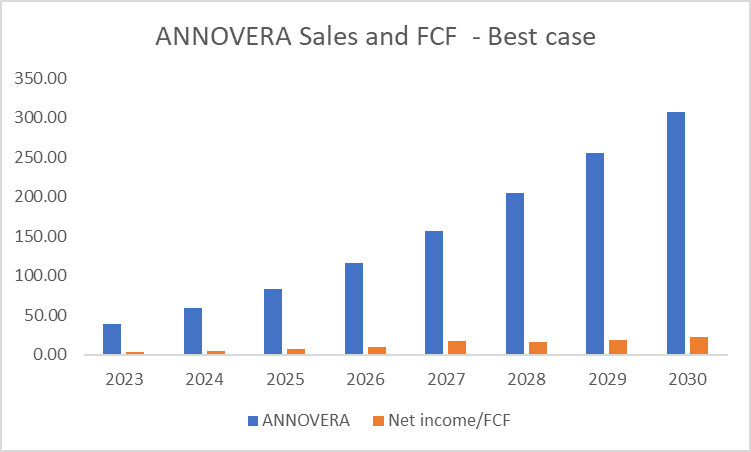

Best case: The insurance companies immediately start to cover ANNOVERA, which also starts to be recognized and widely used instead of NuvaRing. The growth rate is above 40% a year for the next 4 years. And the drug will capture 30% of the TAM (around $1 billion) by 2030. I assign a probability of 25% to this scenario and an associated fair price of $10.2.

ANNOVERA sales and FCF (Author's estimates)

{kind=link}

Other assumptions that are common to every scenario are the following: (1) discount rate of 10%; (2) the bulk of gains in revenue growth is coming from ANNOVERA, leaving little expected improvement on the other 2 treatments; (3) fixed Opex between $2.5 and $3.5 million per year; (4) tax rate between 5% and 15% given the large NOLs accumulated by TXMD in the past.

This yields a probability-weighted fair price of around $5.6, which implies an undervaluation of 30% from the current prices.

Conclusion

TherapeuticsMD offers the opportunity to buy an “empty box” that however is expected to be filled with cash in the coming years, coming from royalties. While some risks still exist, the current price along with an overall promising turnaround plan by Mayne Pharmaceuticals suggest that the 30% undervaluation is real and maybe even conservative.

For further details see:

TherapeuticsMD: From Fallen And Forgotten To Cash Cow