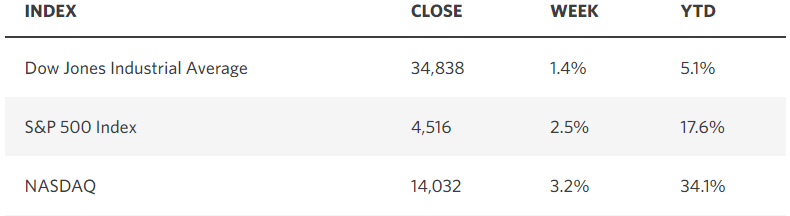

SPY - This Is Why You Should Stay Bullish

2023-09-05 10:25:47 ET

Summary

- The stock market and economy have defied predictions of collapse due to rising interest rates, thanks to post-pandemic stimulus, and unique supply and demand dynamics.

- The recent jobs report showed slower job growth, easing wage inflation, and an increase in labor supply, moving closer to a soft landing for the economy.

- Consumers and businesses are less sensitive to rising borrowing costs, with household debt and debt servicing ratios at historic lows, sustaining consumer spending levels and prolonging the expansion.

One year ago, I advised investors in this report not to be bamboozled by conventional thinking. Most economists and market strategists were convinced that the rapid rise in short-term interest rates from the zero bound to what is now more than 5% would collapse the stock market and send the economy into recession. The consensus was relying on several leading indicators with very reliable track records that were pointing in an ominous direction. Namely, the inverted yield curve.

The fault in this line of thinking was failing to recognize that we are not in a typical business cycle. The combination of the pandemic, unprecedented monetary and fiscal stimulus, and the war in Ukraine over the past three years resulted in extremes in supply and demand that required us to step outside the box of conventional thinking. Regardless, the pessimists have dug their heels so deeply into the bearish narrative that they are about to make the same mistake twice.

{kind=link}

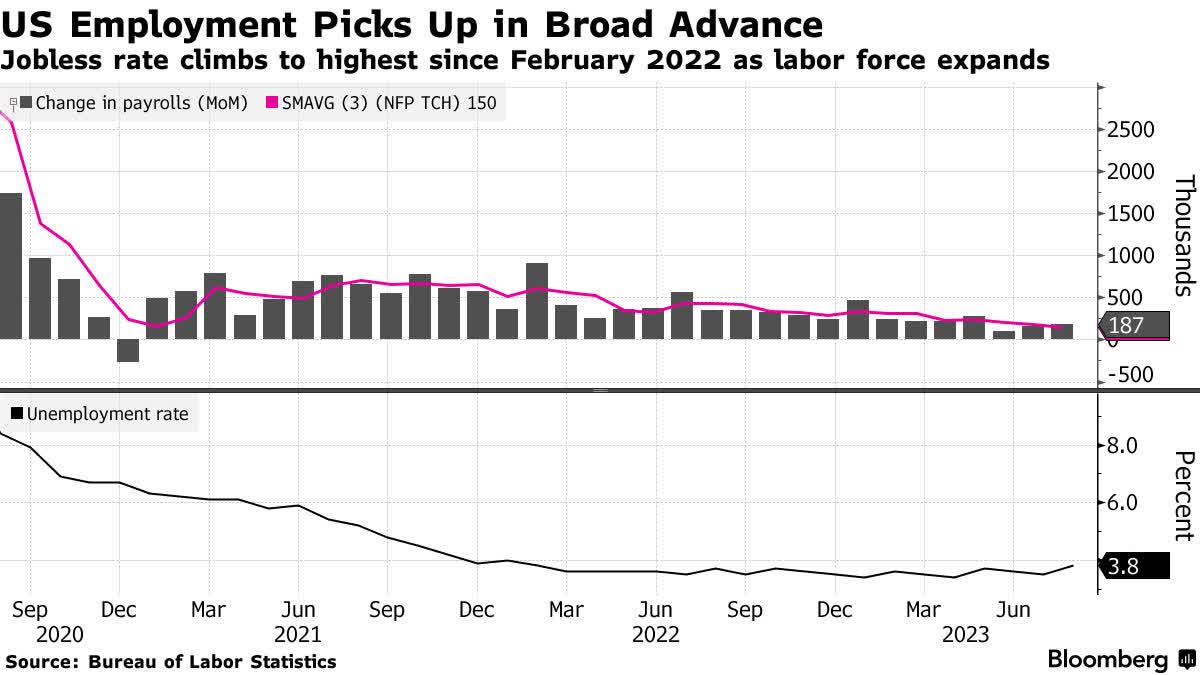

Friday's jobs report for August was another step in the direction of a soft landing. We saw a continuation of slower job growth (187,000), easing wage inflation, and an uptick in the supply of labor, which increased the participation rate. This is music to the Fed's ears in its effort to restore price stability without ending the ongoing expansion in the economy. The increase in the unemployment rate from 3.5% to 3.8% was largely due to new entrants in the workforce.

The pessimists are already pointing to this increase as a warning sign that a significant stock market decline and recession are on the horizon, but they are again failing to recognize the strength of the foundation to this expansion and bull market.

{kind=link}

It makes sense to assume that when interest rates go up rapidly, consumers will spend less on goods and services, businesses will spend less on equipment and expansion, corporate profits will decline sharply, and unemployment will rise meaningfully enough to result in an economic contraction. The anomaly that helped us avoid this fate one year ago when inflation was more than 9% and interest rates were starting to rise was an unprecedented amount of excess savings held on consumer balance sheets. Bearish forecasters failed to appreciate the potency of this phenomena. It was the fuel that kept real (inflation-adjusted) consumer spending growing, which is why we avoided a recession.

Now that excess savings has fallen closer to pre-pandemic levels, those who failed to recognize its significance are asserting that consumer spending will collapse under the weight of the lagged impact of higher interest rates. Again, a logical conclusion, but one that fails to recognize a new development long in the making.

Earlier this year, I forecast that we would see a return to real wage growth just as excess savings no longer became relevant. To that point, last week's jobs report showed average hourly earnings growth of 4.3%, which is in excess of the latest Consumer Price Index figure of 3.2%. That is helping to soften the blow of lower savings levels and softer wage gains, but it does not explain economic resilience in the face of higher interest rates. Today's resilience is due to the fact consumers and businesses are far less sensitive to rising borrowing costs than they have been in the past.

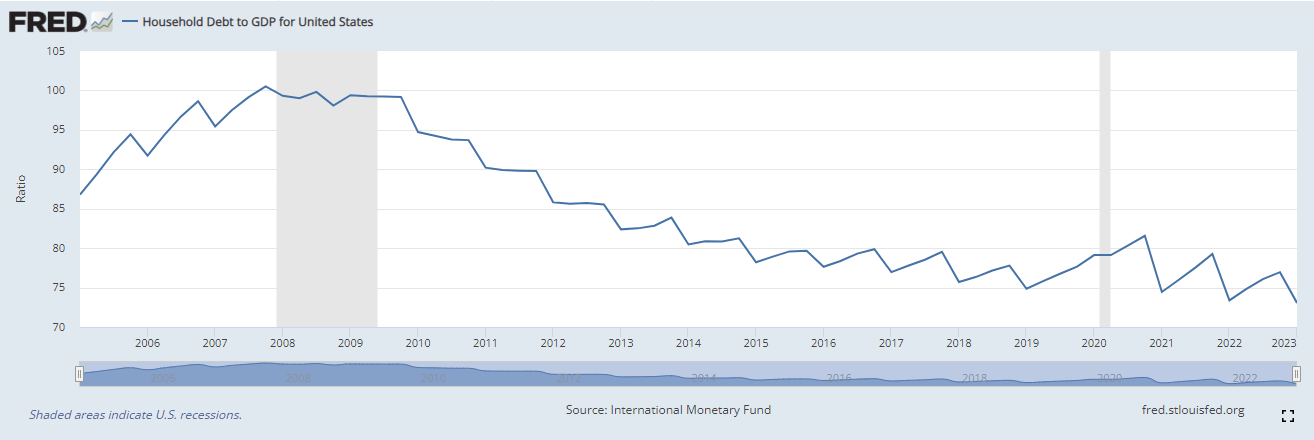

For all the concern about overleveraged consumer balance sheets, household debt as a percentage of U.S. gross domestic product has fallen from more than 100% during the Great Financial Crisis in 2008 to a two-decade low of 77%. This is a result of more responsible lending standards and more reasoned consumers.

{kind=link}

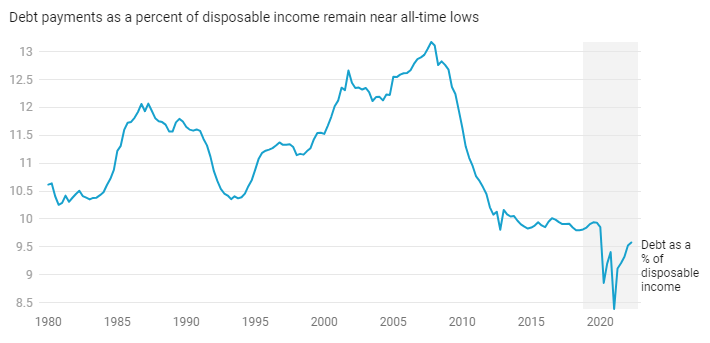

In addition, there has also been a dramatic decline in the amount of after-tax income required to service outstanding debt. The debt servicing ratio fell from a record high 13.2% to an all-time low during the pandemic, and it remains near a multi-decade low of 9.6%.

{kind=link}

The decline in outstanding stock of debt is the reason that the 500 basis points in rate increases by the Fed over the past 18 months only resulted in a 1.5% increase in the percentage of disposable income required to service that debt. This is helping to sustain consumer spending levels, and prolong the expansion, but it isn't just the consumer who is less sensitive to changes in monetary policy.

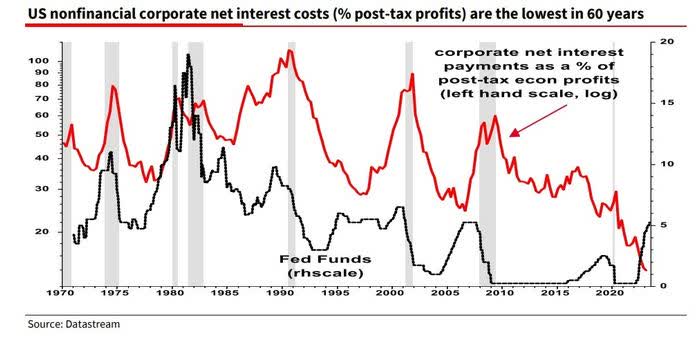

Corporate debt has seen similar changes . The stock of outstanding corporate debt as a share of GDP at 43% is not far from its 2008 peak of 45%, but as a percentage of corporate net worth it is at a 50-year low. Additionally, the debt outstanding is predominately fixed rate and longer term with average maturities ranging from four to 10 years, depending on asset class. The percentage of investment-grade debt maturing after 2028 has risen to 56%, while the percentage of high-yield debt is up to 42%. This means that corporate America is also less sensitive to rising interest rates. In fact, the Fed's rate-hike campaign has been a windfall for most sectors of the S&P 500 (SP500), because net interest costs as a percentage of post-tax profits have collapsed.

During the ultra-low interest rate period from 2020-2022, corporations refinanced outstanding debt at fixed rates for longer terms in the same way that homeowners refinanced mortgages. When the yield curve inverted, due to the surge in short-term rates, corporations started earning huge sums on their cash balances in the same manner that retail investors are profiting from money market funds. This is boosting corporate profits and helping to fuel capital spending, as net interest costs have plunged to a 60-year low.

{kind=link}

Those who remain pessimistic will chant "higher for longer" when it comes to the Fed's monetary policy, which they assert will end the expansion and send the S&P 500 to much lower levels than we see today. I could not disagree more for the reasons I have outlined. Consumers and corporations are far less sensitive to rising interest rates than they have been in the past. With the Fed's rate-hike cycle having likely concluded, and the disinflationary trend intact, a soft landing is looking more probable with each passing month. Estimates for corporate profits in 2024 are inching upward. I expect the S&P 500 will achieve new all-time highs in the coming 6-12 months.

For further details see:

This Is Why You Should Stay Bullish