CA - Tidewater Midstream: Focus On Maximizing Shareholder Value

2023-03-20 06:31:52 ET

Summary

- Tidewater Midstream's Q4-2022 results were solid, but the management now sees a $50 million funding gap at Tidewater Renewable, and the FY2024 EBITDA guidance is walked back slightly.

- The stock is still grossly undervalued even adjusting for the funding gap.

- The discount won't close itself and the new management team is looking for solutions.

Situation Overview

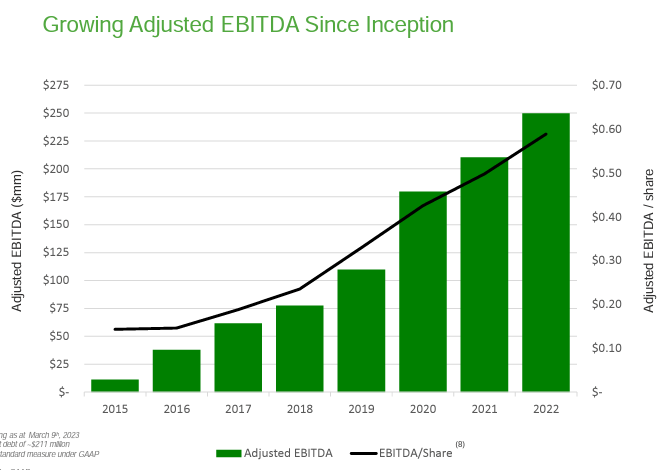

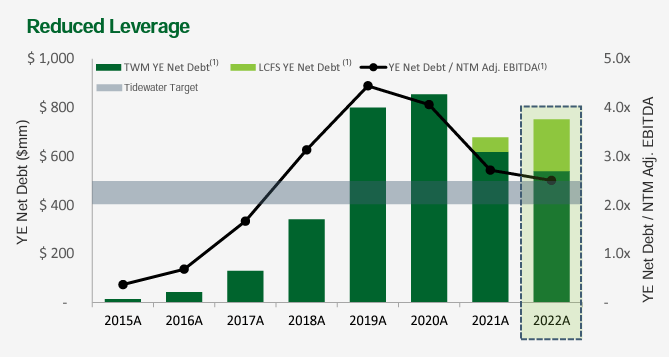

Tidewater Midstream ( TWM:CA ) reported solid Q4 and year-end 2022 numbers. The consolidated Adjusted EBITDA reached a record high of $250 million, driven by strong performance at the Prince George Refinery and increased volume across its gas processing facilities. Furthermore, TWM achieved its long-term target by reducing year-end net leverage to 2.9x (deconsolidated). However, the company's common equity experienced a significant decline following a negative surprise: the renewable diesel plant faces a $50 million funding gap due to rising inflationary pressures in labor and materials costs.

As a reminder, the original gross project cost was estimated at $260 million. However, the management has recently revised it to $342 million. Although there will be an inflow of $53 million from the sale of BC LCFS credits, the net amount still leaves a funding gap of $50 million that the management needs to address.

There are two potential solutions to address the funding gap. The first option is to request an additional $50 million from AIMCo , the provider of the existing $150 million five-year senior secured second lien credit facility. However, due to recent market fluctuations, the coupon on the additional capital may not be favorable, and it may also result in further dilution through warrants.

The second option available to TWM is to provide an inter-company loan to Tidewater Renewable. After the year-end, TWM extended its $550 million credit facility (with approximately $470 million drawn), and more significantly, the $50 million minimum availability requirement was waived for one year. It is likely that TWM will utilize its own revolver to cover the $50 million funding gap. However, this may result in a tight liquidity situation for TWM. Additionally, the scheduled turnaround at the Prince George Refinery in Q2-2023 and the need to focus on the $75 million convertible due in September 2024 may add further pressure to TWM's finances.

Fortunately, despite the higher capital cost, the project's economics are still very appealing. Even with the revised net capex of $180 million and the re-iterated EBITDA of $80-90 million, the 3,000 bbl/d Hydrogen Derived Renewable Diesel project is still being constructed at approximately 2.0x multiple. Furthermore, TWM's core business operations are still performing strongly. The Prince George's crack spread is forecasted to remain within the range of $80 to $90 for 2023, and although natural gas prices have been depressed, the outlook is optimistic with several North America LNGs expected to come online in 2024.

Closing The Discount

During the earnings conference call, the interim CEO's prepared remarks contained an encouraging statement: "We believe that our company is undervalued relative to the sum of our assets, particularly when compared to our Midstream peers. We do not expect this discount to resolve itself. While we have implemented disciplined capital allocation, we have also initiated a review of our asset portfolio and will explore potential alternatives to unlock the value we see." When an analyst inquired about which asset may be on the block, the interim CEO responded that he did not want to speculate about the outcome of the review, as it is still ongoing. The company is assessing all of its assets and examining how they are valued in both the internal and external markets. Although all assets are being considered, it is too soon to predict where this review may lead.

As a shareholder of TWM for a considerable time, I am encouraged to hear that the new management recognizes the significant undervaluation issue, which has been apparent for some time. It is reassuring that the management acknowledges the need to take action to address this matter. Despite TWM's substantial growth in EBITDA since its IPO, achieved through astute acquisitions and effective project implementation, the share price has persistently underperformed not only the broader equity market but also its midstream peers. Except for those who acquired shares near the COVID-19 lows, it is safe to say that no one has made a profit on TWM, as the stock is currently trading below its IPO price of $1 and the subsequent follow-on offerings at higher prices.

From my perspective, the counterintuitive underperformance of TWM's strong track record of EBITDA growth can be attributed to the previous CEO's emphasis on growth. Although the underlying businesses continue to generate healthy EBITDA, the EBITDA-to-FCF conversion rate is low due to ongoing capital projects that absorb cash flow. Additionally, TWM relied heavily on debt to finance these projects, which avoids immediate equity dilution but leaves little room for error. As a result, TWM is reliant on the capital markets' willingness to provide funding and/or refinancing when necessary, without much financial cushion. The failed refinancing of the $125 million senior bond is a prime example - given TWM's business quality and leverage, the refinancing should have been straightforward, but since the market was closed, TWM had to redeem the bond using its market cap.

As a long-term board member, the interim CEO has identified two key strategic priorities. The first is to ensure the successful completion of the renewable diesel project, while the second, more crucial, priority is to transition to a more rigorous approach to capital allocation and proactively address the undervaluation issue through a corporate event. In my opinion, this shift towards more disciplined capital allocation and proactive measures to address the valuation discount is the correct corrective course of action.

Company Presentation Company Presentation

{kind=link}

{kind=link}

Valuation

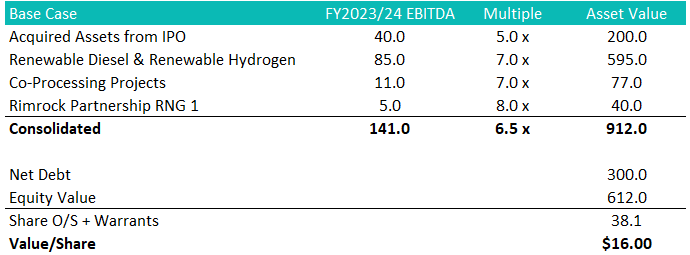

I have previously presented my valuation for LCFS. Taking into account the additional $50 million funding gap, which is included in net debt, I estimate the fair value of Tidewater Renewable (LCFS) to be $612 million or $16 per share.

{kind=link}

Valuing the midstream and downstream business at 5.0x and factoring in 69% of my fair value for LCFS, and subtracting $545.2 million of net debt, I value TWM at $1.83 per share. It is important to note that if we exclude the $422.3 million LCFS value, the fair value of standalone TWM is $0.83 per share, which is approximately 5% lower than its current trading price of $0.88 per share.

Author

Conclusion

Although the funding gap is disappointing and has resulted in near-term uncertainty, I view this selloff as a buying opportunity. The renewable diesel project is nearing commissioning, and only a small amount of capital is required to complete it. Furthermore, the new management team acknowledges the undervaluation issue and has demonstrated a desire to take action to address it. The interim CEO has initiated an internal review aimed at maximizing shareholder value. In my opinion, the commissioning of the renewable diesel project will serve as a positive catalyst in the near term, and TWM has substantial upside if an asset or corporate sale takes place.

For further details see:

Tidewater Midstream: Focus On Maximizing Shareholder Value