CA - Tidewater Midstream: Trading At Just 4x EBITDA On A Deconsolidated Basis

Summary

- Tidewater Midstream owns 69% of Tidewater Renewables, and this hides the undervaluation of the midstream company.

- I can easily see a value north of C$2/share, and that does not even take a re-rating of the Renewables division into account.

- I currently have no position but may initiate a long position over the next few weeks.

- The September 2024 debenture has a 6.8% YTM and could be interesting for income-focused investors.

Introduction

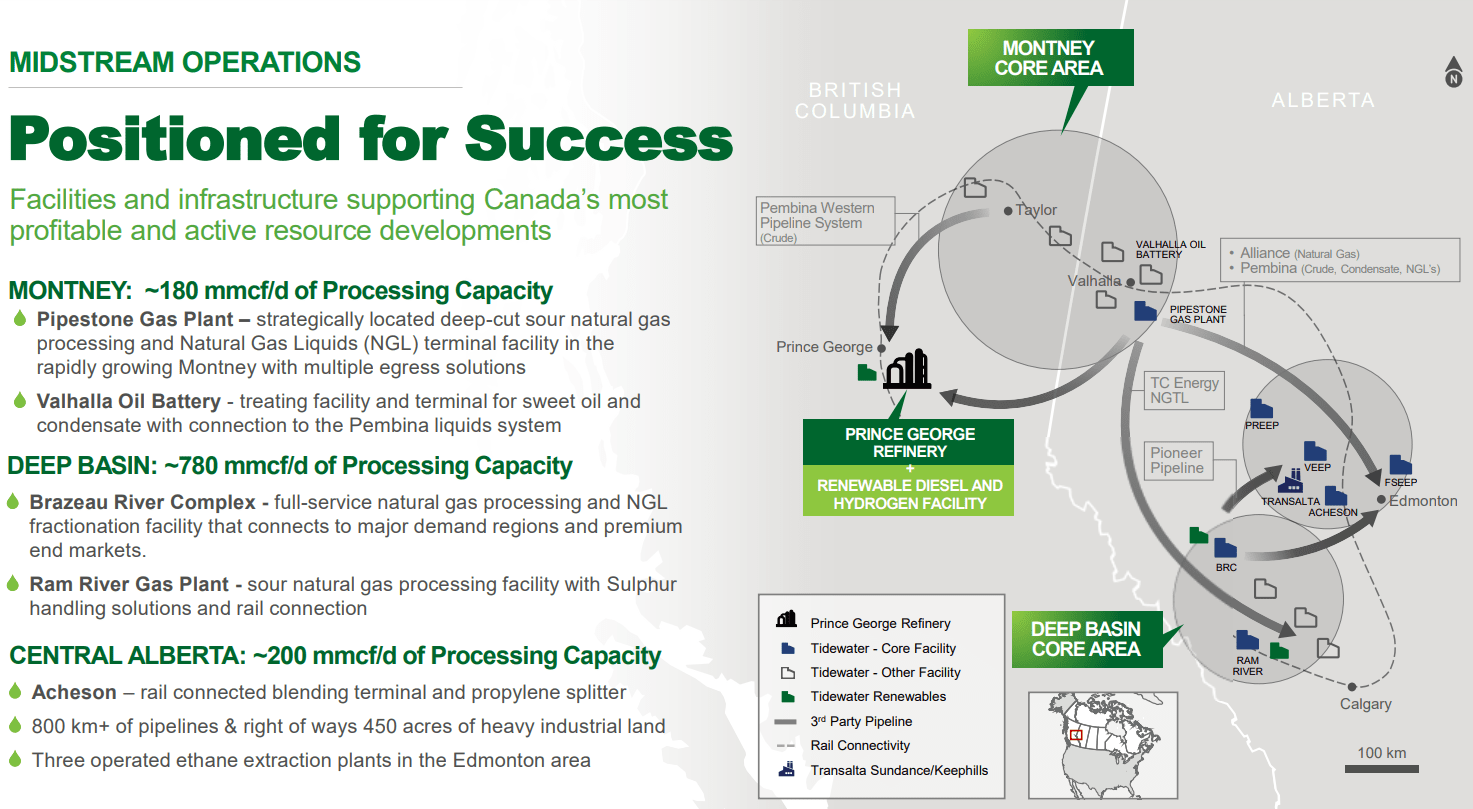

Tidewater Midstream and Infrastructure ( TWM:CA ) ( TWMIF ) is a Canada-based company focusing on its natural gas processing operations (1,200 mmcf/day across three main areas). Another important piece of the company's puzzle is the 12,000 barrel/day Prince George refinery, where Tidewater signed a five-year contract with Husky Energy (now Cenovus Energy) for the output of the refinery (mainly diesel and gasoline).

{kind=link}

Tidewater Midstream's main listing is in Canada, where it is trading on the TSX with TWM as its ticker symbol . The average daily volume in Canada exceeds 400,000 shares per day, and I will refer to the Canadian listing and I will use the Canadian Dollar as the base currency throughout this article.

The first nine months of 2022 were fine, and 2023 is also shaping up to be a decent year

Tidewater isn't the easiest company to explain as it still retains a 69% stake in Tidewater Renewables, which it spun off in 2021. This means the asset base and performance of the Renewables company are still consolidated in Tidewater's results. As such, I will be pretty brief on the company's Q3 and 9M 2022 financial performance before isolating the impact of Tidewater Renewables and instead using the share price of the Renewables division as its fair value.

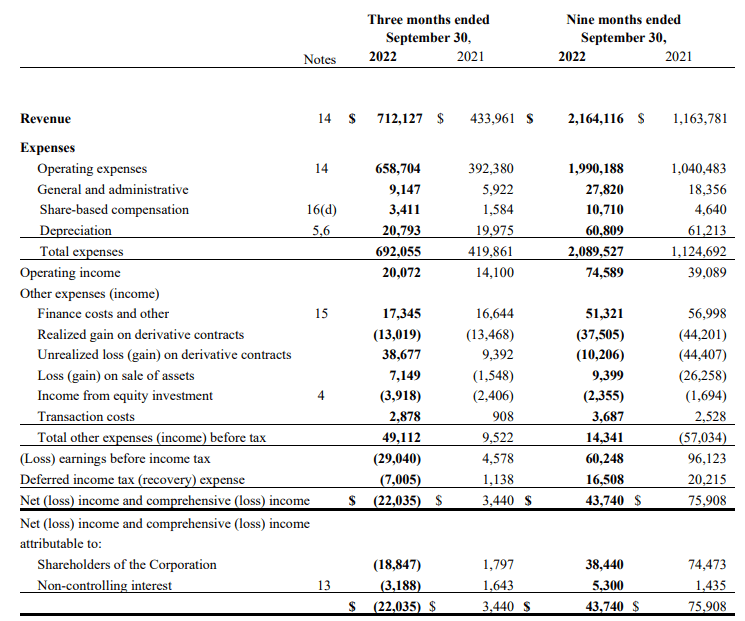

In the first nine months of 2022, Tidewater Midstream reported a total revenue of C$2.16B , resulting in an operating income of C$75M. The company was profitable , mainly thanks to a C$48M realized and unrealized gain on derivatives which resulted in a net income of C$44M of which approximately C$38M was attributable to the common shareholders of Tidewater. This represents an EPS of C$0.11 per share.

{kind=link}

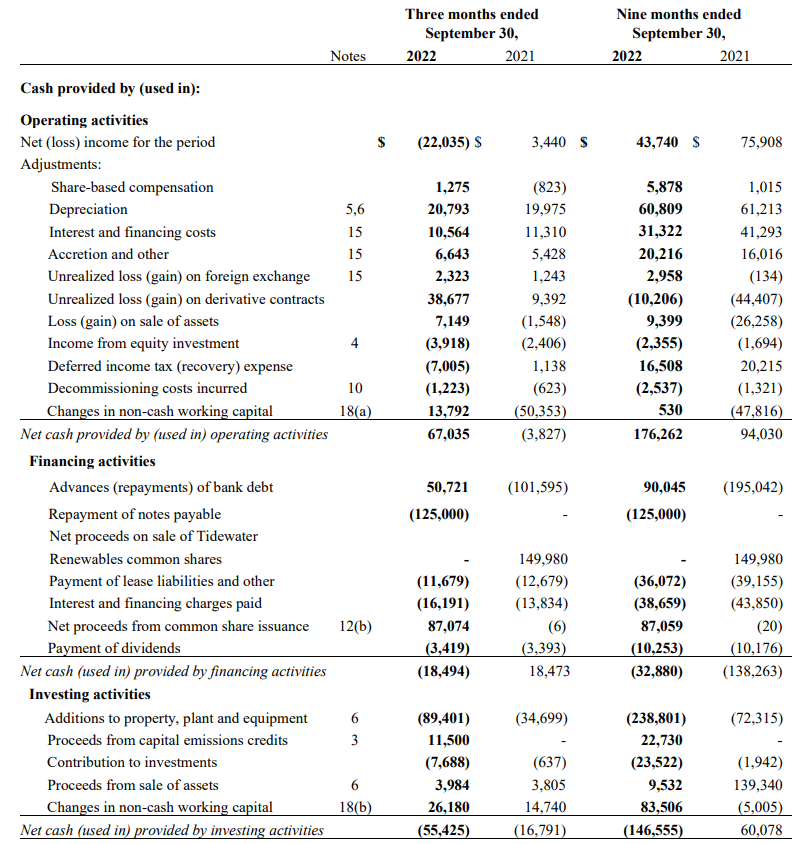

While that is a good result, the sustaining free cash flow result likely is a better metric for an infrastructure-focused company. Fortunately, we can calculate the adjusted operating cash flow from the cash flow statement, while the company's Management Discussion & Analysis document provides a breakdown between total capex and maintenance capex. The image below shows a total operating cash flow of C$176M, but it is worth noting this does not include the C$36M in lease payments and almost C$39M in interest and finance expenses. Additionally, the entire C$16.5M tax bill was deferred and was added back to the operating cash flow.

{kind=link}

On an adjusted basis, the operating cash flow was approximately C$85M in the first nine months of 2022. Keep in mind, this excludes the C$10.2M in unrealized derivative gains but includes about C$37.5M in realized gains.

While the total capex was approximately C$239M in the first nine months of the year, it is worth noting that only a very small portion of the total capex bill was actually related to sustaining capex. As you can see below, only C$42M was classified as sustaining capex . This means that the adjusted sustaining free cash flow result on a consolidated basis in the first nine months of 2022 was approximately C$43M.

{kind=link}

The complicating factor while analyzing Tidewater Midstream is that it owns a majority stake in Tidewater Renewables ( LCFS:CA ), which was spun out from TWM in 2021. Fortunately, the company also provides the deconsolidated EBITDA and sustaining capex, which makes it a little bit easier to calculate a fair value based on the 'sum of the parts'. The image below shows the deconsolidated net debt as of the end of Q3 2022 was approximately C$523M. We also know the deconsolidated EBITDA is expected to come in at C$180-190M which means the net debt ratio (compared to the EBITDA) is less than 3 which is very reasonable. The current enterprise value is approximately C$980M based on the current share price of C$1.08 per share.

Tidewater Investor Relations

We also know Tidewater Midstream expects a full-year EBITDA of C$300M on a consolidated basis in 2023 while Tidewater Renewables anticipates to reach a 'run rate' of C$140-150M in EBITDA this year. As the EBITDA will ramp up throughout the year, we can probably assume the full-year EBITDA on the Renewables-level will be approximately C$100-125M, which means that we should expect a pretty stable EBITDA result on the Tidewater Midstream level. So let's use C$185M as the base case deconsolidated EBITDA going forward.

The interest expenses should be around C$60M per year (on a deconsolidated basis) while the depreciation expenses should be on a similar level. This would result in a C$65M pre-tax income and about C$45M in net income. We also know the deconsolidated sustaining capex is just around C$40-45M per year which means the free cash flow on an annual basis will exceed the normalized net income by C$15-20M, so I don't think it is unfair to assume a C$60M free cash flow yield on the Tidewater Midstream level.

This now allows us to calculate a fair value for the Tidewater Midstream operations. A multiple of 6x EBITDA would result in a fair enterprise value of approximately C$1.15B, or approximately C$650M for the equity. A required free cash flow yield of 8% based on a C$65M sustaining free cash flow would result in a fair equity value of C$800M. The average of both would be C$725M, or C$1.71 per share.

The 23.9M shares in Tidewater Renewables have an additional value of C$260M based on the C$11 share price, and this adds about C$0.61/share to the Tidewater Midstream value, which would then come out at C$2.32.

Investment thesis

In other words, if we would look at Tidewater Midstream from an unconsolidated point of view, the current enterprise value of C$980M would really be just C$720M after isolating the market value of the stake in Tidewater Renewables. Which, at a multiple of just 4 times the deconsolidated EBITDA, appears rather cheap.

As Tidewater Renewables progresses towards realizing its C$150M annualized EBITDA target, the value of the LCFS stake should become even more valuable, and a re-rating of Tidewater Midstream will likely occur over the next 12-18 months.

Income-focused investors who aren't interested in the current sub-4% dividend yield offered by Tidewater Midstream may want to have a look at the 5.5% convertible debenture with a maturity date in September 2024. As that debenture is trading at 98 cents on the dollar, the effective yield to maturity is approximately 6.8%.

For further details see:

Tidewater Midstream: Trading At Just 4x EBITDA On A Deconsolidated Basis