CA - Tilray: For Cannabis Stocks Avoid Canada Buy USA

2024-01-09 13:09:48 ET

Summary

- Tilray stock dipped following the release of second-quarter earnings.

- The company's ambitions to enter the United States are hindered by politics, and meanwhile, organic growth and EBITDA margins remain under pressure.

- Tilray's highly leveraged balance sheet adds an additional source of risk.

- I reiterate my strong sell rating and offer investment alternatives.

Tilray (TLRY) saw its stock dip following the release of second-quarter earnings. It has been a while since Wall Street was enamored by the stock, as it has become clear that the company's ambitions to enter the United States are affected by factors out of their control. Meanwhile, it's not clear what progress is being made at the company, as organic growth remains pressured and EBITDA margins remain slim. The company maintains a highly leveraged balance sheet, which does not buy the company much time as it awaits legalization of cannabis in the United States. Outside of meme-stock hype cycles, it's hard to imagine things turning around at this company - I reiterate my strong sell rating.

TLRY Stock Price

TLRY was a global cannabis giant in 2018, back when Wall Street had great ambitions for Canadian operators. Those days are long gone.

I last covered TLRY in September, where I rated the stock a strong sell on account of the low insider ownership and precarious balance sheet position. I continue to see more downside as stockholder dilution and increased leverage look inevitable here.

TLRY Stock Key Metrics

TLRY is a Canadian operator which is best known for its cannabis operations but also has significant alcohol and pharmacy distribution business segments.

{kind=link}

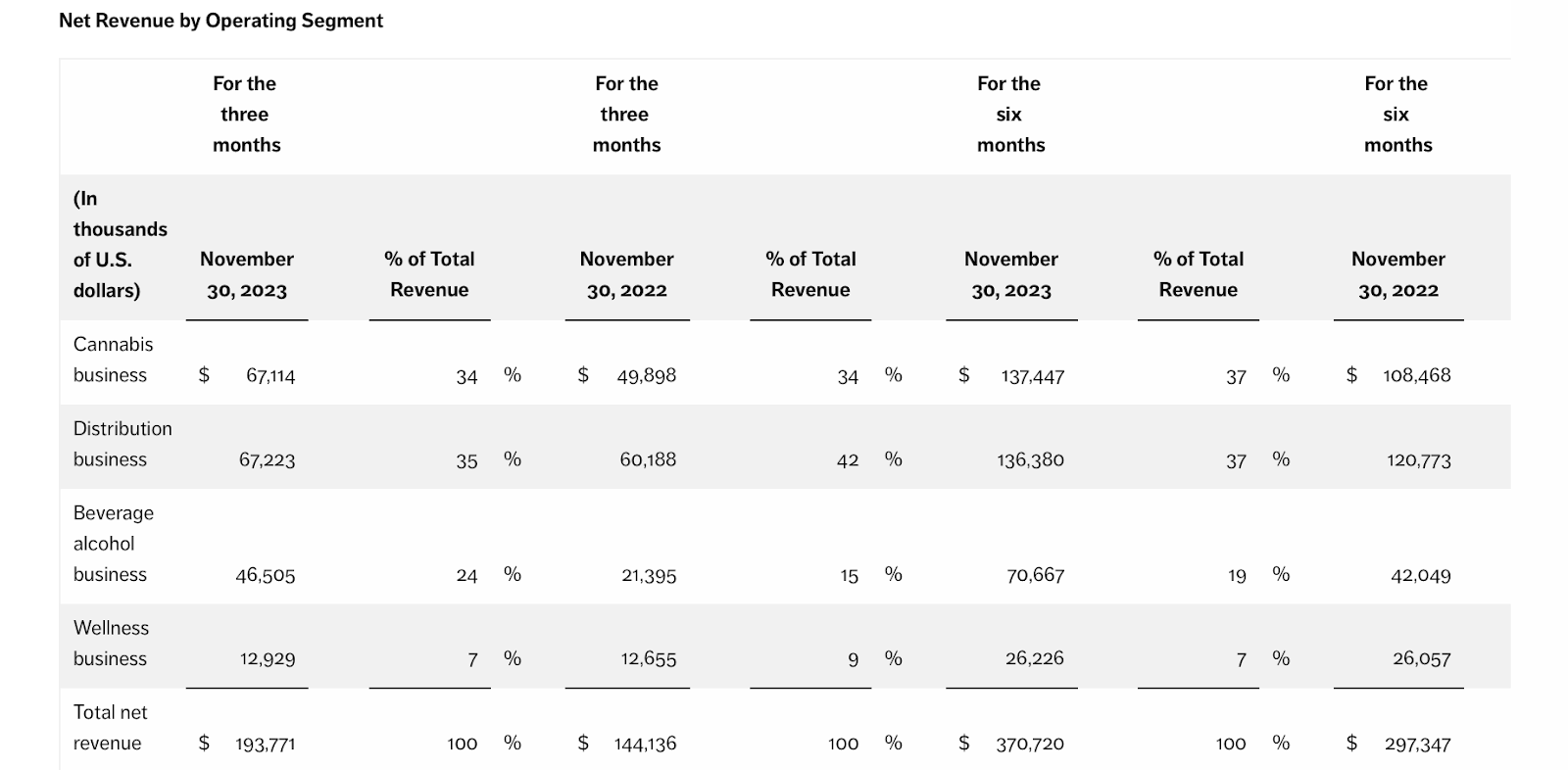

In its latest quarter, revenue grew 34.5% YoY to $193.8 million, the company's highest number ever. I note that shares outstanding grew 20% YoY during the same period - the company has historically driven the bulk of its top-line growth through M&A, with the most recent being the acquisition of cannabis operator HEXO and eight beer brands from Anheuser-Busch. It's notable that while TLRY is mainly known as a cannabis operator, cannabis revenues made up only 34% of overall sales.

{kind=link}

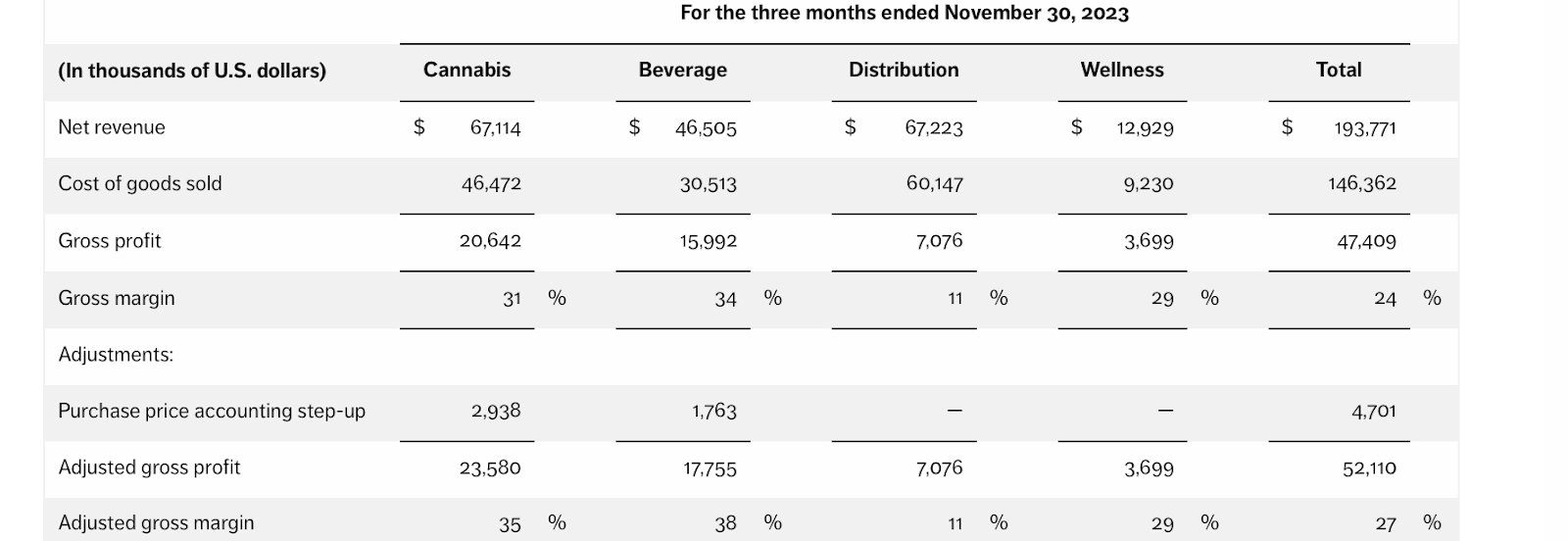

TLRY saw gross margins experience pressure in the quarter, with cannabis margins declining 800 bps YoY, beverage margins declining 1400 bps YoY, and overall margins declining 400 bps.

{kind=link}

TLRY burned through $18.4 million of free cash flow in the quarter, as compared to generating $29.3 million in free cash flow in the prior year. Adjusted EBITDA came in at $10.1 million, down from $11 million in the prior year quarter. These cash flow metrics do not inspire confidence in relation to the balance sheet position, as TLRY ended the quarter with $261 million of cash vs. $454.4 million of debt. Management has reiterated guidance for the full year to see adjusted EBITDA of between $68 million and $78 million, though that guidance implies a steep step-up from the $20.8 million generated through the first six months of the fiscal year. Even if management can hit that target, leverage still stands at around 2.5x debt to EBITDA, a lofty multiple given the low profitability.

Is TLRY Stock A Buy, Sell, or Hold?

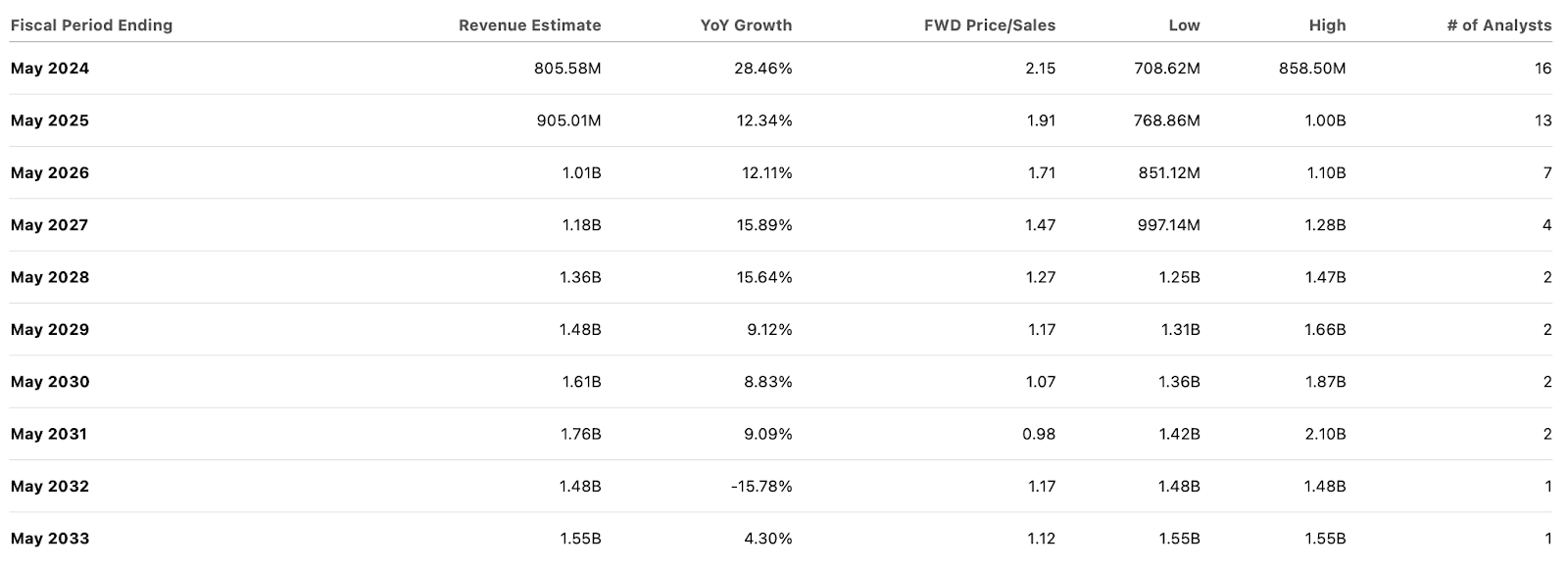

The investment thesis in TLRY has historically been based on the company eventually being able to import low-cost cannabis from its greenhouse facilities into the United States. Over the years, it has become clear that our political system is not quite ready for full legalization, making the timeline for TLRY's entrance quite extended. TLRY is expected to drive double-digit revenue growth over the coming years, but I'm skeptical that the company can achieve that without continued M&A activity.

{kind=link}

Anyone who has seen the Canadian cannabis market can attest to the incredible number of cannabis dispensaries, the prevalence I liken to being more than Starbucks ( SBUX ) or McDonald's ( MCD ). The issue is that Canada has a significantly less dense population base than the United States, making it difficult for the country's cannabis operators to generate high profit margins given the intensely competitive environment. This might help to explain why TLRY has been so aggressive in diversifying outside of cannabis operations, though these efforts do not appear to have helped the bottom line, as the adjusted EBITDA margin remains low at around 5% (compare that with the 35% margin at Anheuser-Busch ).

In my view, the most concerning element remains the potential poor alignment of management with shareholders. As I detailed in my prior report , the bonus pay structure in 2023 was based on an "applicable consolidated net revenue target was $695 million and the Adjusted EBITDA target was $75 million for full bonus payments." The lack of "per share" verbiage may explain why the M&A activity seldom includes discussion about accretion and per-share growth. Management compensation is arguably high, especially when compared to the slim adjusted EBITDA margins.

2023 DEF14A

At the same time, insider ownership is slim, with insiders owning just 0.68% of shares outstanding. TLRY does not appear to have strict equity requirements, as the executive team appears to have low equity ownership in relation to their compensation.

FY24 Q2 Press Release

I view TLRY as being an example in which even the best management can not fix a bad business. The economics of cannabis in Canada appear structurally challenged (high supply vs. limited demand), and diversifying the business has been expensive from a dilution and balance sheet perspective. Many investors may favor TLRY as a way to trade cannabis legalization hype, but it should be noted that a potential rescheduling of cannabis to Schedule III by the DEA will not positively impact TLRY as it still falls short of the legalization needed to allow for international import of cannabis. Instead, I recommend those looking to trade the hype to consider the stocks of the US cannabis operators (MSOs), which tend to have stronger adjusted EBITDA margins and are trading at more reasonable valuations based on adjusted EBITDA.

{kind=link}

The stocks of US cannabis operators stand to benefit from the aforementioned re-scheduling of cannabis due to the removal of 280e taxes, which would lead to a large boost to the bottom line. I would not be surprised if MSOs end up offering greater upside upon any legalization news, and it at least offers more fundamental support. Due to the strained balance sheet and lack of catalysts to improve the financial situation, I reiterate my strong sell rating for TLRY stock.

For further details see:

Tilray: For Cannabis Stocks, Avoid Canada, Buy USA