STLD - TimkenSteel: Why I Am Not A Buyer

2023-10-19 16:41:56 ET

Summary

- TimkenSteel Corporation (TMST) has significantly underperformed its competitors in the steel industry since its spin-off from The Timken Company.

- TMST operates in a highly competitive industry with a thin economic moat and competitive disadvantage relative to peers due to its small size and highly unionized workforce.

- Recent operational improvements by a new management team have resulted in improved financial performance which has sent shares sharply higher over the past three years.

- TMST is currently trading at a premium valuation relative to peers and, in my view, represents an unattractive investment opportunity.

TimkenSteel Corporation ( TMST ) traces its roots back to 1917 as a part of the Timken Roller Bearing Company, which later became known as The Timken Company ( TKR ). In June of 2014, TMST became an independent public company through a spin-off transaction. Since then, TMST has significantly underperformed TKR as well as its self-identified competitor group, which includes Nucor ( NUE ), Gerdau S.A. ( GGB ), and Steel Dynamics ( STLD ).

Company Overview

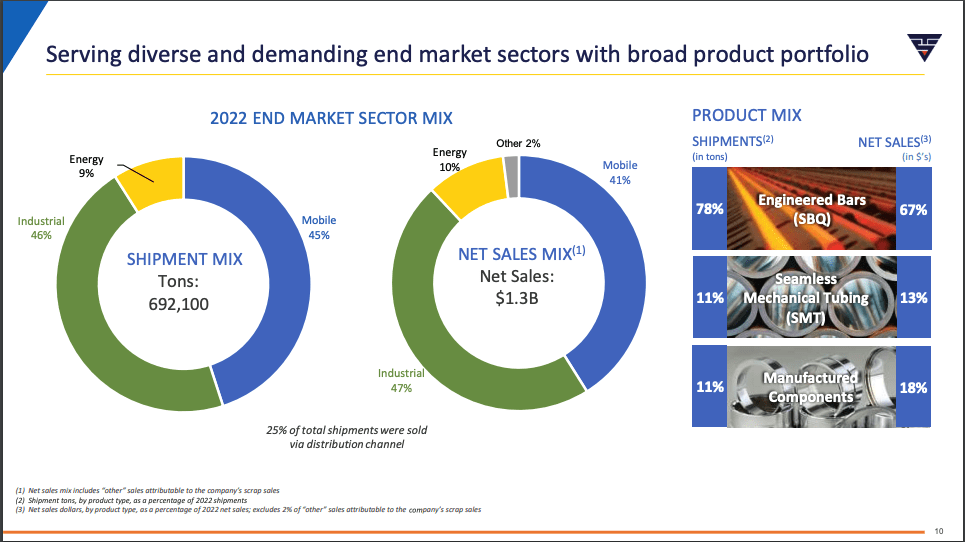

TMST is a steel producer with ~1,750 employees engaged in the production of special bar quality ("SBQ") bars, seamless mechanical tubes, manufactured components such as precision steel components, and billets. The company produces nearly 100% of steel, primarily from recycled scrap metal, using electric arc furnace technology. SBQ bar, mechanical tube, and billet production takes place in the Company's Canton, Ohio manufacturing facility while production of manufactured components takes place at facilities in Columbus, North Carolina and Eaton, Ohio.

Highly Competitive Industry Resulting in a Thin Moat

TMST is a producer of high commoditized products and the level of competition is high. Thus, the economic moat around the business is relatively thin. Moreover, the company's relatively small scale vs other players in the industry makes in difficult for TMST to achieve economies of scale enjoyed by competitors. As shown by the EBITDA margin historical comparison below, TMST has achieved EBITDA margins that have consistently been significantly lower than competitors such as NUE, STLD, and GGB. Furthermore, TMST has generated a much lower ROA and ROE than its peer. The fact that TMST margins and capital efficiency ratios have been significantly worse than its peers in a highly commoditized industry suggests TMST is simply less efficient than its peers. This lack of efficiency may be driven by its smaller size. For FY 2022, NUE generated $41.5 billion in sales, STLD generated $22.2 billion in sales, and GGB generated $16 billion in sales compared to just $1.3 billion in sales generated by TMST.

TimkenSteel Investor Presentation

{kind=link}

{kind=link}

High Stock Price Volatility and Recent Strength

TMST shares have rallied by more than 400% over the past three years, after plunging as low as $2.26 during the COVID-19 market sell-off during 2020. The 2020 experience and rebound are evidence of the fact that TMST operates in a highly economically sensitive business, which has led to high levels of stock volatility. The significant move over the past three years has been driven by an improving economic backdrop as well as significant operational improvements by TMST.

Turnaround and Operational Improvements

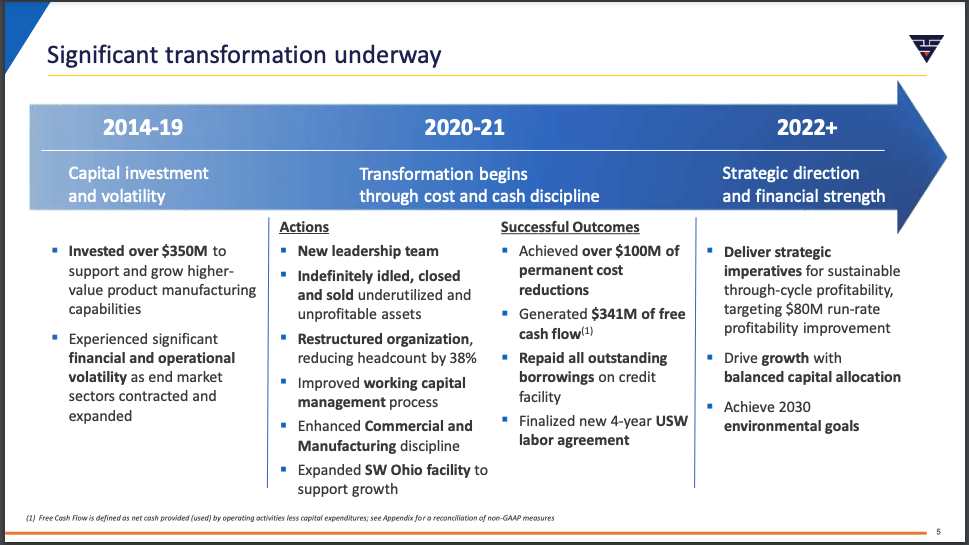

In October 2019, Tim Timken Jr., a fifth generation member of the Timken family, stepped down as CEO, paving the way for new management. Ultimately, Michael Williams was appointed CEO in 2020 and has implemented significant changes. TMST closed and sold unprofitable assets, reduced headcount by 38%, repaid all outstanding debt, finalized a new USW labor agreement and improved the working capital management process. These changes helped the company improve its financial performance, resulting in record EBITDA and free cash flow generation in Q2 2022.

TimkenSteel Investor Presentation TimkenSteel Investor Presentation

{kind=link}

{kind=link}

Pension Liabilities Restructuring

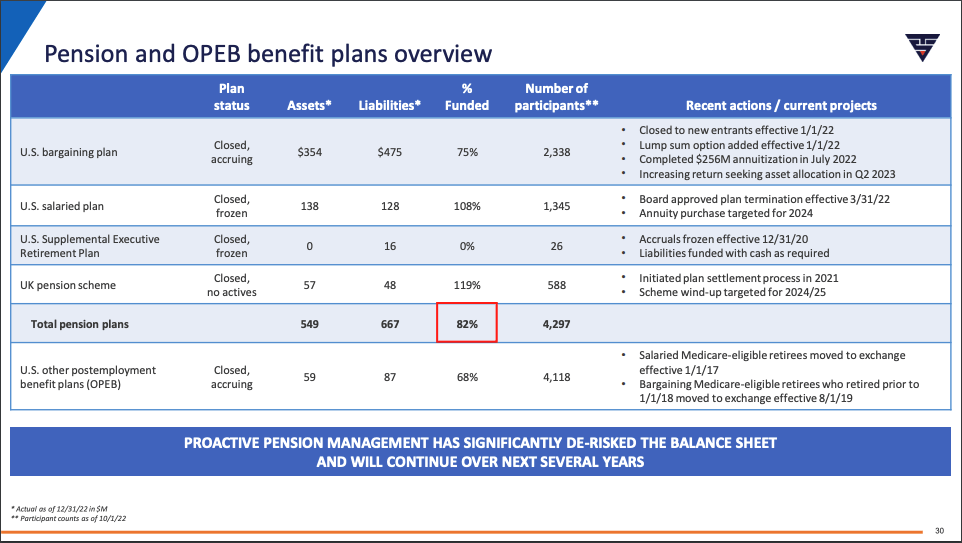

In July 2022, TMST announced a deal to purchase an annuity contract from Prudential to settle ~$250mm of the then outstanding $800mm in U.S. pension obligations. This move was a significant step in terms of fixing TMST's pension liability problems. However, TMST continues to have total unfunded liabilities of $146mm. While this is manageable in context of current profitability, it is a negative in that it is something that the company will need to address in the coming years and thus may limit the company's ability to return excess cash flow to shareholders.

TimkenSteel Investor Presentation

{kind=link}

High Union Labor Percentage

Roughly 62% of the TMST employees are covered under a collective bargaining agreement which was ratified by USW Local 1123 on October 29, 2021. The contract is in effect until September 27, 2025. While TMST has some time before the next contract negotiation, recent union strikes by the UAW and WGA suggest that the negotiation may be a challenging one. Comparably, competitor NUE does not have a highly unionized workforce and just 5% of the STLD workforce is represented by collective bargaining agreements. Thus, I believe TMST will remain at a long-term competitive disadvantage relative to peers which operate with much lower levels of unionized labor.

Short-Term Risks to Automotive End Market Due to UAW Strike

The ongoing UAW strike against GM ( GM ), Ford ( F ), and Stellantis ( STLA ) has led to a significant drop in automotive production. The drop in automobile production is starting to impact the steel market as well. U.S. Steel has already announced that it is idling some production due to reduced demand due to the UAW strike. TMST is highly exposed given that 41% of its sales are part of its mobile business, which sells to automobile companies. While I believe the

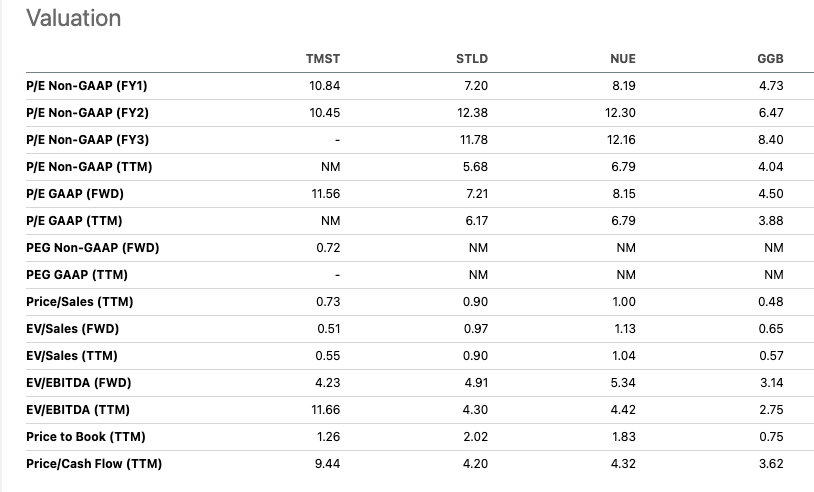

Valuation Relative to Peers

While TMST trades at a relatively low forward PE ratio of just 10.8 compared to 18x for the S&P 500, the valuation is much less attractive than TMST's peers based on traditional key metrics such as PE ratio and EV to EBITDA. The premium valuation relative to STLD, NUE, and GGB is not warranted given TMST's history of significant operational underperformance in terms of margins. Moreover, in my view, the high levels of union labor at TMST compared to STLD and NUE argue for a valuation discount as opposed to the currently observed premium.

{kind=link}

Alternative Valuation Methods

Given that TMST generated highly volatile cash flows, I do not view a traditional DCF as an appropriate valuation method. Moreover, given the competitive nature of the industry I have a low degree of confidence that TMST will continue generating free cash flows in the further out years which often serve as the basis for a large part of any DCF valuation. Additionally, given TMST lack of profitability over the course of its history, it is difficult to look to historical average PE ratio analysis. Thus, in order to get a sense of what might be a reasonable valuation for TMST, I have decided to look to EV to Revenue, Price to Tangible Book Value, and EV to Forward EBITDA.

On an EV to Revenue basis, TMST is trading fairly close to its historical average since becoming a public company. However, I think it is important to note that TMST has generally not been a good investment since coming public, and thus I would not want to own TMST at its average historical valuation but rather a significant discount. In terms of price to tangible book value, TMST is currently trading at 1.22 compared to a historic average of 1.07. Similarly, on a EV to Forward EBITDA basis, TMST is also trading well above its historical average (though the period of available data is shorter here.) Based on these metrics, I believe TMST is overvalued.

Conclusion

Generally speaking, in my view, the steel industry tends to be a challenging one for long-term investing due to high levels of competition and high asset intensity. TMST is not positioned for success relative to peers, given the company's relative small scale and high percentage of union labor. That being said, recent actions taken by the new management team have resulted in some level of operational improvement, leading to better financial results. The improvement in financial performance as well as a stronger macroeconomic forces have led to a significant rally in TMST shares over the past few years. TMST is now trading at a premium valuation relative to its peers based on many metrics. Thus, I believe TMST represents a below average investment opportunity at these levels and investors should look to other opportunities to invest in higher quality businesses with wider moats.

For further details see:

TimkenSteel: Why I Am Not A Buyer