CA - Tin Commandment: Alphamin Still A Strong Buy With A Catalyst

2023-06-29 05:34:42 ET

Summary

- Rising demand for tin in industries like AI, solar, and EVs suggests a potential price upside.

- Alphamin already offers good value, yet is actually set to grow production by ~60% within six months leading to a significant revenue jump.

- I maintain a strong buy rating and share a strategy for a second position and hedge.

Introduction

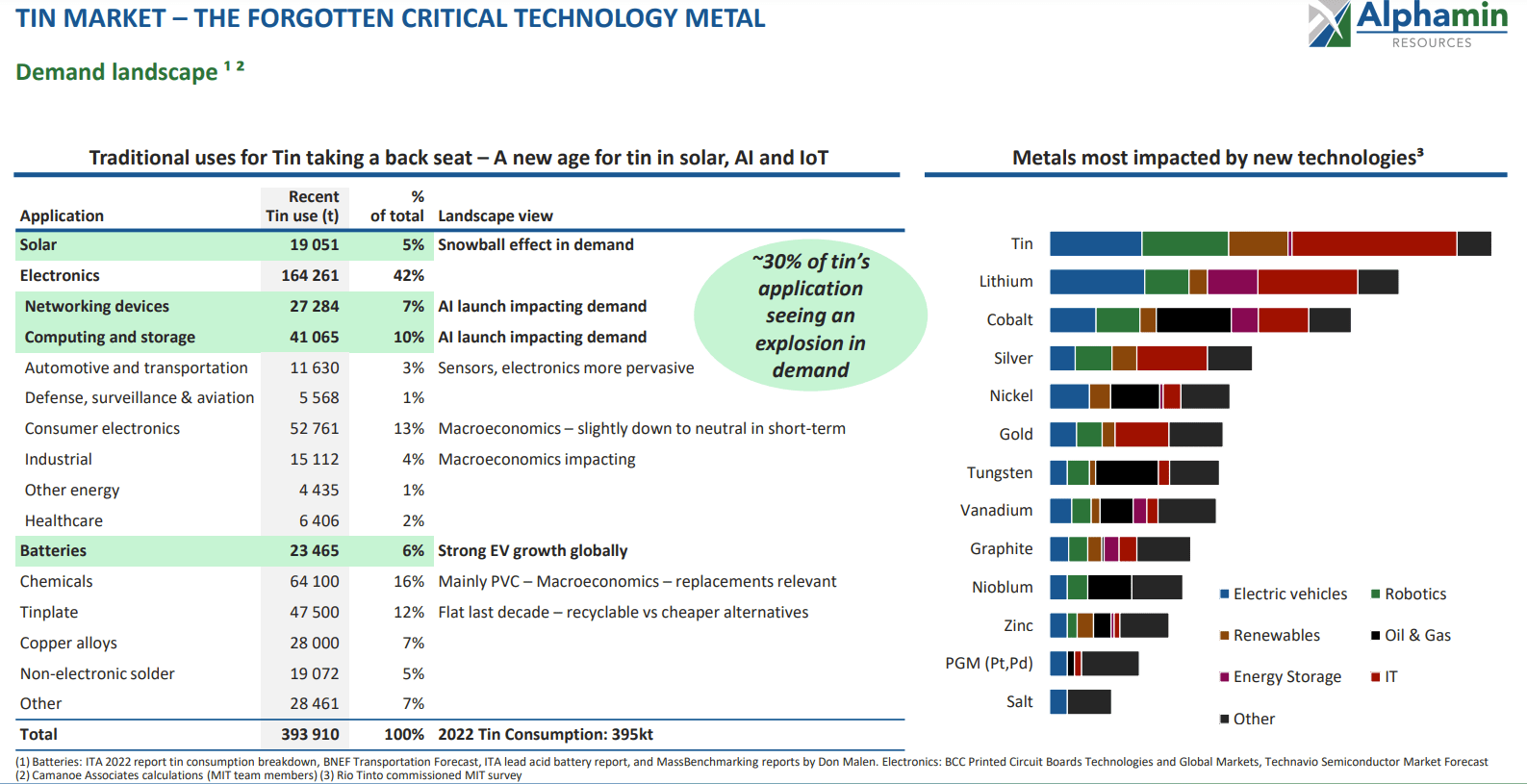

In January, I introduced Alphamin ( AFMJF ) ( AFM:CA ), fondly known as the "Alpha-Mine" of tin (at least to me), emphasizing its significance in semiconductors and sectors such as AI, solar power, batteries, and EVs. I noted that Alphamin was ranked as the third most valuable orebody globally according to mining.com , and that MIT researchers also named tin the "metal most impacted by new technologies" in a study a few years ago.

In their recent presentation on June 19, 2023, Alphamin highlighted the "exploding" demand for tin in various industries.

{kind=link}

However, despite the flourishing trends in AI, EV, and IoT securities, both tin and Alphamin seem to be overlooked. In this article, I will provide an update on recent developments, discuss charts and technical analysis, and present a hedged investment strategy for AFM shares. I believe they offer compelling value and maintain a strong buy rating.

Tin Prices Stabilizing, Showing Potential for Upside

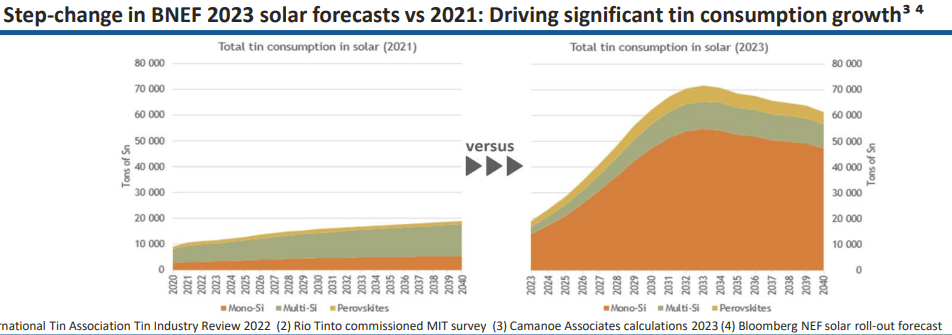

In my previous article, I delved into the global supply and demand dynamics for tin. Notably, global reserves have steadily declined over the years, while demand projections have experienced meaningful upward revisions. For example, the solar industry's estimated tin requirements have surged by over 150% just in the last two years:

{kind=link}

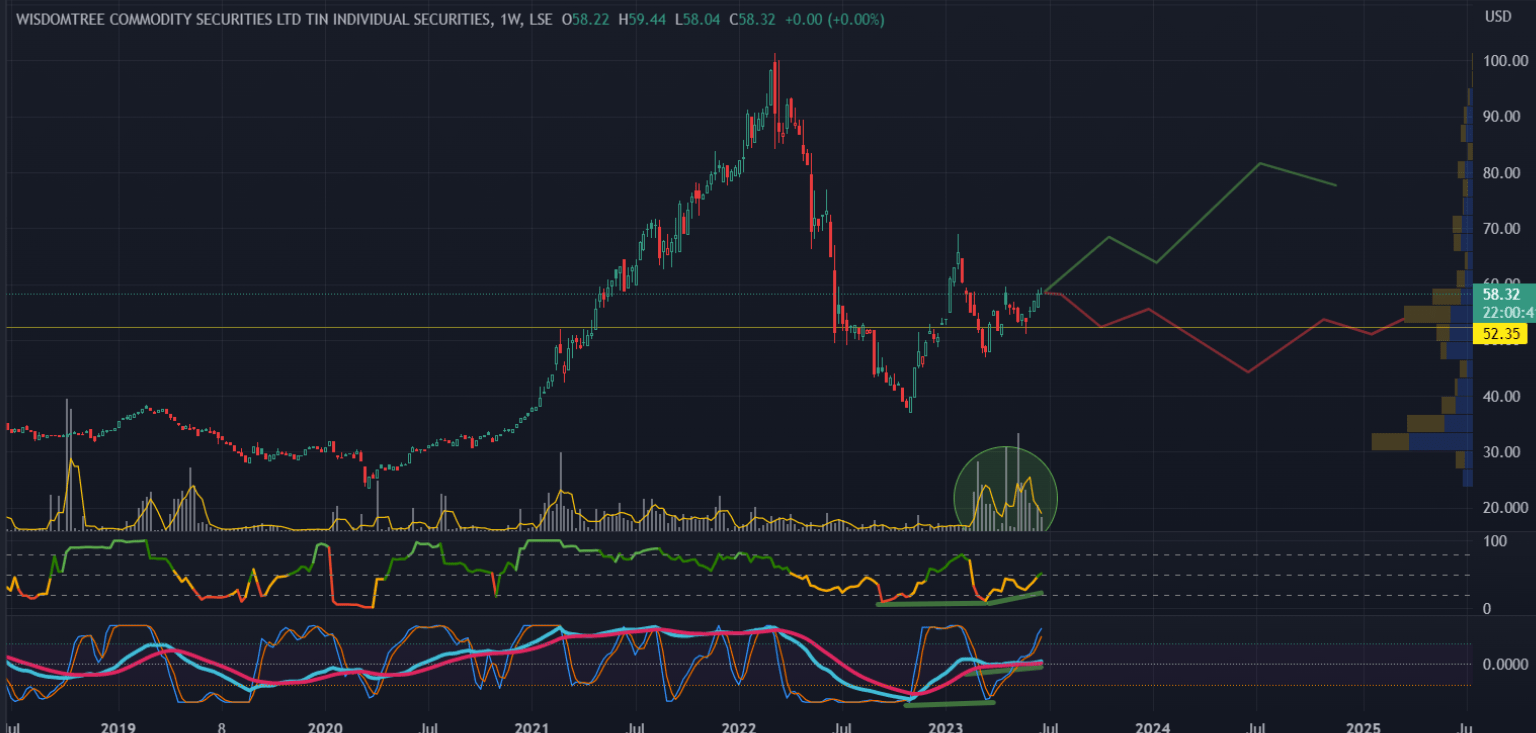

As also mentioned previously, the required incentive price for new tin projects is estimated to be $25k+. Recently prices have stabilized above $25k (yellow line on this tin ETF around $52.35), and volumes have picked up, lending credence to this theory. Additionally using some technical analysis, both the money flow (indicator panel 1) and momentum indicators (panel 2) show positive divergences on the weekly timeframe.

Author's historical analysis and projected scenarios

{kind=link}

Using the green and red potential paths outlined above, I've illustrated what I think are two potential scenarios for the tin price over the coming months. Even in a bearish scenario, I don't see prices dropping too much further toward their pre-COVID levels.

Fundamentally, supply tightness may even worsen in the coming months and into next year due to 1) Myanmar (10% of global production) planning a production stoppage in August and 2) Indonesia (20%) reducing production and threatening to ban exports in favor of domestic development. To understand the significance of these outages/deficits, I turn to the "tin king" Mark Thompson, whom I also referenced in my first article.

Twitter

Thus, Myanmar or Indonesia reducing exports could easily mean significant upside for tin - and Alphamin.

AFM: Unique and Underpriced, Especially With Revenue Growth Catalyst

Alphamin's appeal extends beyond the potential surge in tin prices. As I have previously highlighted, Alphamin boasts the world's highest-grade tin mine, positioning it to accrue value even in low price scenarios. It trades at approximately 4.5-5x EV/EBITDA for 2023.

However, AFM is not only well-positioned defensively, it is also growing. In under six months, Alphamin plans to open its second mine, Mpama South, located just a few hundred meters away from the North Mine. This expansion will boost the company's tin production by 60%, and will also solidify its position as a premier, long-term, low-cost producer. While AFM is a price-taker so must accept tin market prices, I believe the demand growth and bearish supply fundamentals I've outlined above mean AFM's revenue should jump 50%+.

After production increases, and using current tin prices of $25k, Alphamin will trade at an attractive ~3.5x consensus EV/EBITDA for 2024. This assumes 20ktpa and an EBITDA margin of 45%, which sounds high but is in line with the company's Q1'23 print and its last 2 years of prints. MacroTips Trading just wrote a good article on AFM here with detailed historical and projected financials if you want to do more calculations or check math.

The market is still seemingly sleeping on this production upgrade! While Alphamin carries risks (which I cover more later), I believe this valuation is too low for a Tier 1 mine in a critical metal with potential for significant growth.

Technical Analysis

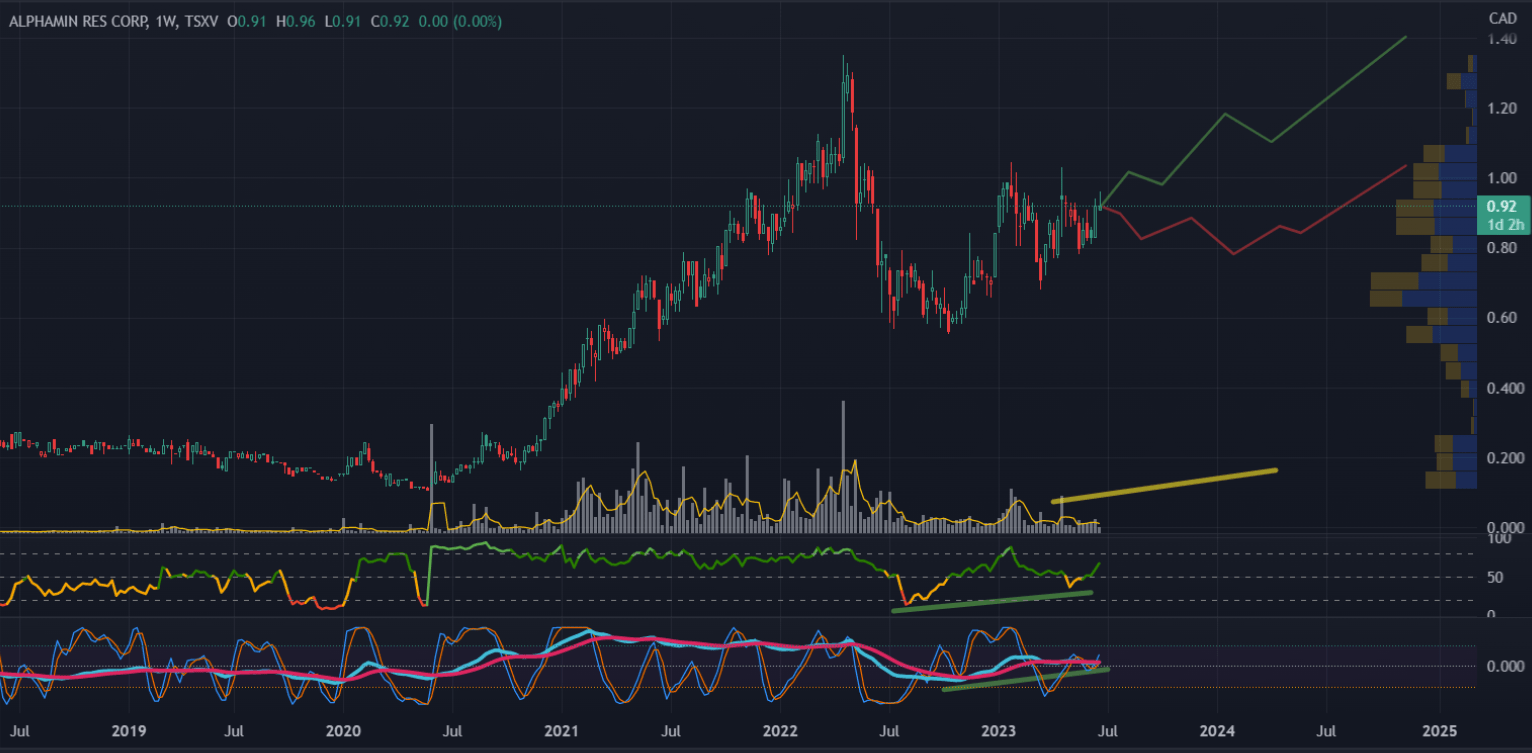

Considering all of the aforementioned fundamentals, in tandem with clues from the technical chart, I have estimated two possible scenarios for AFM's stock. These scenarios serve as insights rather than predictions, but can help anticipate the stock's potential trajectory. Take a look:

Author's historical technical analysis and projected scenarios

{kind=link}

TA Notes:

- The chart looks similar to the tin chart, but you'll notice that Alphamin held up well and did not reach a significant low in late 2022 compared to the tin price.

- I expect volume to increase over the second half of 2023 and into 2024 (yellow trend line).

- There are positive divergences on both the money flow (indicator panel 1) and the momentum indicators (panel 2).

In a bullish scenario, I think AFM could reach new highs by mid-late 2024, coinciding with Mpama South's impact on the financials and its full reflection in AFM's valuation.

In a bearish scenario, AFM could continue to struggle around these levels (while still paying a 6.4% dividend), likely due to downside economic risks and/or reduced supply threats.

Risks and Hedging Strategy

Apart from the usual considerations, It is important to evaluate Alphamin's risks, primarily its location in the Democratic Republic of Congo, which has a history of armed conflict. The potential for regional conflict and production interference contribute to the undervaluation of Alphamin's stock. However, I have previously noted a few mitigating factors: the Congolese government owns 5% of AFM, a South African parastatal owns another 10%, and the Bisie complex is relatively remote and not near much infrastructure.

Additionally, I think investors can adopt two investing strategies to lower underwriting risk. First, maintaining a slightly reduced AFM position size to provide some protection and peace of mind. Second, holding another tin security, such as Metals X Limited ( MLXEF ) to serve as a hedge while also adding to your tin allocation.

Although Metals X has lower grades, and correspondingly, higher costs compared to AFM (presentation here with key elements on Slide 11), it offers exposure to the attractive tin market in a safer jurisdiction (Australia) and will benefit significantly from any disruptions to Alphamin's mine. If Alphamin were to go offline, tin prices would likely shoot to $60-$100k in a short period. With current MLX prices ($0.28 AUD), the security would be trading around or under 1x EV/EBITDA and due for a sharp re-rating.

Personally, I am currently implementing this strategy, although my tin allocation is slightly higher. I hold nearly a full position of Alphamin and roughly around a 2/3 position of MLX.

Closing Thoughts

In conclusion, I believe Alphamin offers a very good investment opportunity, providing exposure to an uncorrelated and attractive resource market, the AI and technology sectors, and the energy industry simultaneously. The company's undervaluation, coupled with its expected 60% production jump and its current 6.4% dividend, make it an enticing value in the near and mid-term. I consider a 3.4x EV/EBITDA base case for 2024 too low and maintain a strong buy on the shares.

There is never time to put everything relevant in one article, but as always, thank you for reading. Please consider your risk tolerance, time horizon, and overall portfolio before making any financial decisions. Avoid making decisions based on any one viewpoint, including mine. I often like to be active in the comments so feel free to share your thoughts or ask questions below.

For further details see:

Tin Commandment: Alphamin Still A Strong Buy With A Catalyst