CA - TMX Group: A Fantastic Asset With An Upcoming Catalyst

Summary

- TMX Group owns and operates Canada's major stock exchanges.

- It is an excellent business trading at a fair price.

- The company has delivered consistent dividend growth for seven-plus years.

- An upcoming stock split could help shares go higher.

TMX Group (TMXXF)( X:CA ) is a high-quality, toll booth-like business with a massive competitive advantage, good growth potential, and an attractive potential short-term catalyst. Here's why I'm so bullish.

Introduction

(Note: All currency is in CAD unless otherwise noted.)

TMX Group is the owner and operator of the Toronto Stock Exchange (TSX), Canada's largest stock exchange and 10th-largest in the world. It also owns the TSX Venture Exchange (TSXV), which lists smaller capitalization stocks, as well as the Montreal Exchange, Canada's home to derivative trading. The Toronto Stock Exchange has been around since 1861 , with original trading volume consisting of just two or three transactions per day. The cost of membership was just $5.

Things are a little more hectic today. There are a combined 3,500-plus issuers on both the TSX and TSXV exchanges, including 1,155 mining stocks, 942 ETFs, and 249 technology companies. The total market cap for the two exchanges combined to exceed more than $4 trillion as of Jan. 31, 2023.

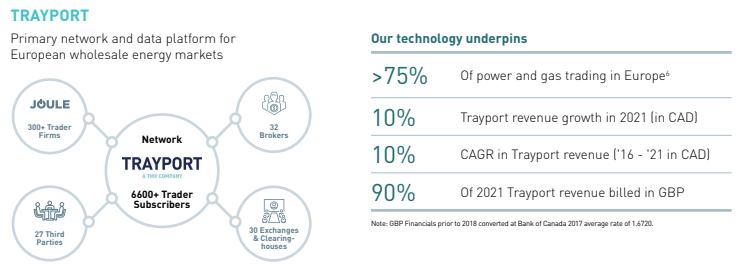

The company has been diversifying away from these main businesses, looking for ways to leverage its informational and technological expertise. This part of TMX Group has been a steady grower over the last decade, buoyed by both organic growth and acquisitions. The biggest acquisition was Trayport, which was purchased by TMX Group in 2017. Trayport's main asset is a platform used by most of Europe's energy traders and is responsible for some 75% of power and gas trading on the continent.

As you can see, Trayport has delivered some pretty solid growth since it was acquired:

{kind=link}

Other recent acquisitions include a 21% stake in VettaFi , which is a U.S.-based data, analytics, indexing, digital distribution, and thought leadership company. TMX Group paid $234M for its stake. It also acquired Wall Street Horizon, a leading provider of global market-moving action and corporate event data. The financials on that deal were not released.

The company is also leveraging its data in a few other ways. It sells real-time data to various sources, including brokerages. It sells feed data, like what you might see scrolling at the bottom of your TV screen. It even sells data to the various companies looking to create indexes and ETFs.

Together, this part of TMX's business is approximately 32% of total revenue. Capital formation - fees paid by companies listing on the various exchanges - is 24% of revenue. Derivatives trading and clearing is 23% of revenue. Equity and fixed income trading is less important than ever, consisting of just 21% of total revenue.

Here's a quick summary of the company's main divisions and their operating margins:

| Division |

| % of total revenue |

| Operating margins |

| Global Solutions & Analytics |

| 32% |

| 64% |

| Capital Formation |

| 24% |

| 42% |

| Derivatives Trading & Clearing |

| 23% |

| 58% |

| Equities & Fixed Income Trading |

| 21% |

| 50% |

It's pretty easy to see why the company is focused on the Global Solutions & Analytics division. It has delivered excellent growth in the past, with a target to increase revenue by high single digits annually going forward. Combine that with high operating margins and you have a winning strategy.

Financial Results

TMX Group has delivered consistently improving top- and bottom-line numbers, especially over the last handful of years. Let's start with the top line. Revenue has increased from $700 million in 2013 to $1.12 billion today. You'll see revenue growth really start to take off starting in 2017, after the company acquired Trayport and really started to focus on that part of its business.

TMX Group revenue 2012-22 (Author using SA data)

Earnings per share have followed a similar path, although various non-cash charges have made earnings much more volatile. The company posts adjusted profit numbers that exclude these non-cash charges, which are a more accurate representation of true profitability.

Adjusted profits per share have grown nicely over the last decade, although that growth has been a little lumpy.

TMX Group adjusted EPS 2012-22 (Author from annual filings)

Consensus analyst projections peg TMX Group's 2023 earnings at $7.27 per share, a 3% increase compared to 2022's numbers. Growth could accelerate in 2024 with earnings expected to hit $7.86 per share.

Giving Back to Shareholders

I'm a 39-year-old early retiree who depends on dividends to support my family. I'm looking for stocks with solid current yields that have potential to increase the payout over time. TMX Group checks off both of those boxes. After a recent dividend raise, the payout is $3.48 per share, which works out to a 2.6% yield. That's an acceptable starting point, at least for me.

The company has increased its dividend each of the last seven years. The dividend growth rate over the last five years is 16.57% and the payout ratio is 46.63% of trailing earnings. The company targets a payout ratio of 40%-50% of adjusted earnings.

One minor concern is the pace of raises. After increasing the payout by 6% in 2020, 10% in 2021, and almost 8% in 2022, 2023's dividend increase was just 4.8%. One likely reason for the disappointing dividend increase was somewhat flat growth in adjusted earnings from 2021 to 2022.

Share buybacks are also an important way to give back to shareholders. While it's clear that TMX Group values acquisitions and dividends ahead of share buybacks, the company has reduced shares outstanding of late. Diluted outstanding shares peaked in December 2020 at 57 million shares. By the end of 2022 the company had repurchased approximately 1.1 million shares. There are currently 55.9 million shares outstanding.

The company's share repurchase authorization expires in March, but it's likely to get renewed for another year. The current authorization gives the company permission to repurchase 1% of total shares outstanding, and I'd strongly suspect 2023's version will look very similar.

Valuation

TMX Group is an excellent business. It has grown the top and bottom lines consistently over the last decade. It boasts 90%-plus gross margins and 50%-plus operating margins. The company has an excellent moat as well. Long-term investors have done very well in this name. Shares are up 285% since 2008, plus dividends.

{kind=link}

I'll be the first to admit this stock isn't truly cheap. It doesn't get to what I'd call value territory very often. But it's still an excellent stock trading at a reasonable price.

The stock trades hands at just a hair over 18x analyst consensus forward earnings , or an earnings yield of 5.56%. This does seem a little expensive in a world where a 10-year U.S. treasury yields almost 4%.

If we look at the stock from a different perspective it seems more reasonable. The current price-to-forward earnings ratio for the S&P 500 is just over 20x, giving the market a forward earnings yield that's a hair under 5%. TMX Group stacks up pretty well when compared to the S&P 500 on that metric.

It's also cheaper compared to its exchange peers. Intercontinental Exchange, Inc. (NYSE: ICE ), the owner of the NYSE and Euronext exchanges, trades at 19x analyst consensus 2023 earnings . Nasdaq, Inc. (NASDAQ: NDAQ ) has an even higher forward P/E ratio, trading at 21.1x analyst consensus 2023 earnings .

Risks

One big risk that could impact TMX Group in the short term is a recession. A prolonged downturn would impact most parts of the company's business. New issues and IPOs slow down during recessions. Trading volumes would most likely fall as well. Many investors choose to ignore their portfolios during turbulent times. Even the Global Insights and data divisions could be impacted by an overall slowdown.

A longer-term risk is alternate trading platforms continuing to gain market share. Technology has made it easier for market participants to make trades among themselves without getting the exchange involved. According to the company's Q3 quarterly report, TMX Group handled approximately 60% of all domestic equity trades in Canada. Even though this is a higher market share than the previous year, there's no guarantee the bulk of Canadian equity trades will remain on the company's platform.

One final long-term risk is private companies choosing to forego the listing process all together and remaining private. Being a publicly traded company opens an organization up to scrutiny, makes the financials public knowledge, and has a certain cost to it. Many companies might choose not to bother, especially if they can access growth capital from other sources.

A Potential Catalyst

Shortly after releasing 2022's full-year earnings in early February, TMX Group proposed a plan to split its stock on a 5-to-1 basis. Instead of owning a single share of a stock currency worth $135.56, investors would own five shares worth approximately $27.11 each. Shareholders must approve this plan at the company's annual meeting in May.

I'll be the first to admit it shouldn't matter if investors own one share or five shares at a lower price. The only thing that should matter is the intrinsic value of each share. The rest is noise.

But there's growing evidence that companies that split their stock actually outperform - over the short term, at least. According to research by Bank of America, the average newly split stock is up 25.4% a year later, compared to 9.1% for the S&P 500. This isn't just some bull market phenomenon, either. The research tracked stock split data since 1980.

It's easy to dismiss these findings and say they don't matter for a stock that trades in Canada, since the data looked at U.S. stocks. But remember, a big portion of TMX Group's revenue is selling data to other market participants. It's extremely unlikely the company proposed the split without looking at what happened to previous splits. If the operator of the stock market thinks a split is prudent, then chances are it will work out.

Final Thoughts

TMX Group is one of the highest quality stocks in Canada. It has a virtual monopoly over public markets in Canada, a similarly strong position in derivatives, and solid growth potential from growth in its Global Solutions & Analytics division. It also boasts a nice dividend with a history of increasing the payout. And it trades at a fair valuation of just over18x forward earnings, slightly cheaper than its peers.

A potential catalyst could send shares higher, too. I recently added this name to my portfolio, and I'd be looking to buy more on any substantial pullbacks.

For further details see:

TMX Group: A Fantastic Asset With An Upcoming Catalyst