CA - TMX Group: A Staple For An All-Weather Portfolio

2023-10-16 13:09:34 ET

Summary

- TMX Group is the owner of the Toronto Stock Exchange and TSX Venture Exchange, with a 66% share of the domestic equities trading market.

- TMX Group has been a dividend grower through thick and thin over the last 20 years.

- Not a lot has to go right to achieve at least high single digit returns.

Introduction

The TMX Group ( X:CA ) is the owner of the Toronto Stock Exchange and the TSX Venture Exchange which are Canada's largest exchanges by far. Other lines of business which Canadian Investors and traders are most likely familiar with that the company owns are TSX Trust Company, AST Canada, TSX Alpha Exchange, Shorcan Brokers Limited, Montréal Exchange ((MX)), Canadian Derivatives Clearing Corporation, BOX Options Market LLC, TMX Datalinx, and Trayport. Many of these business lines will be discussed herein.

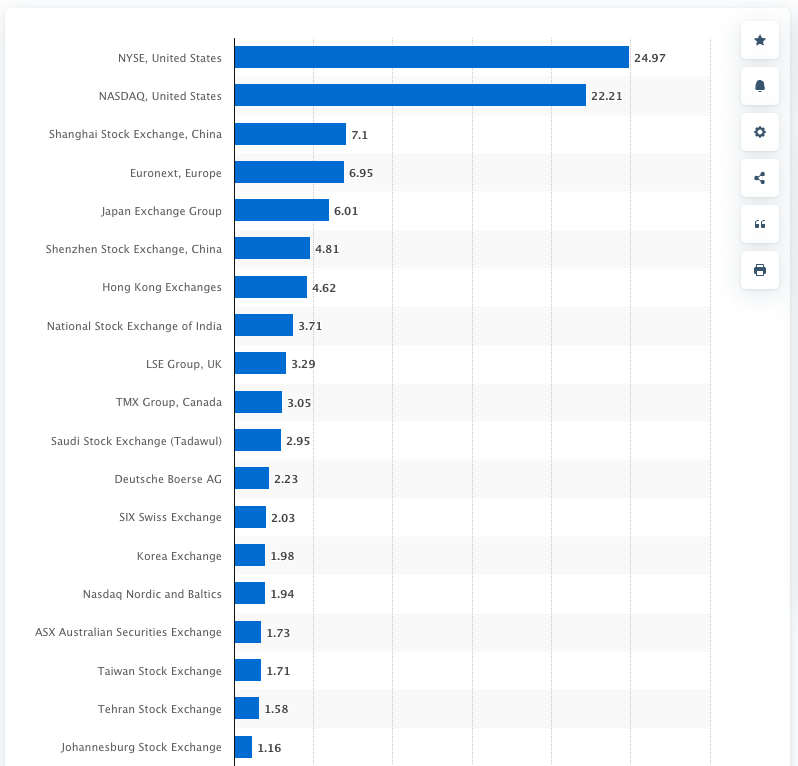

The TMX Group's share of the domestic equities trading market was ~66% as of June 2023 in the Q2 report and is the 10th largest stock exchange operator in the world by market capitalization. Given the Canadian population and listed businesses make up such a small portion of the world's total, this is an impressive feat. The Toronto Stock Exchange is one of the oldest in the world tracing its origins back to 1852. TMX Group essentially has a monopoly over Canadian equity, fixed income, and derivative markets.

Largest stock exchange operators worldwide as of July 2023, by market capitalization of listed companies (Statista)

{kind=link}

Investment Thesis

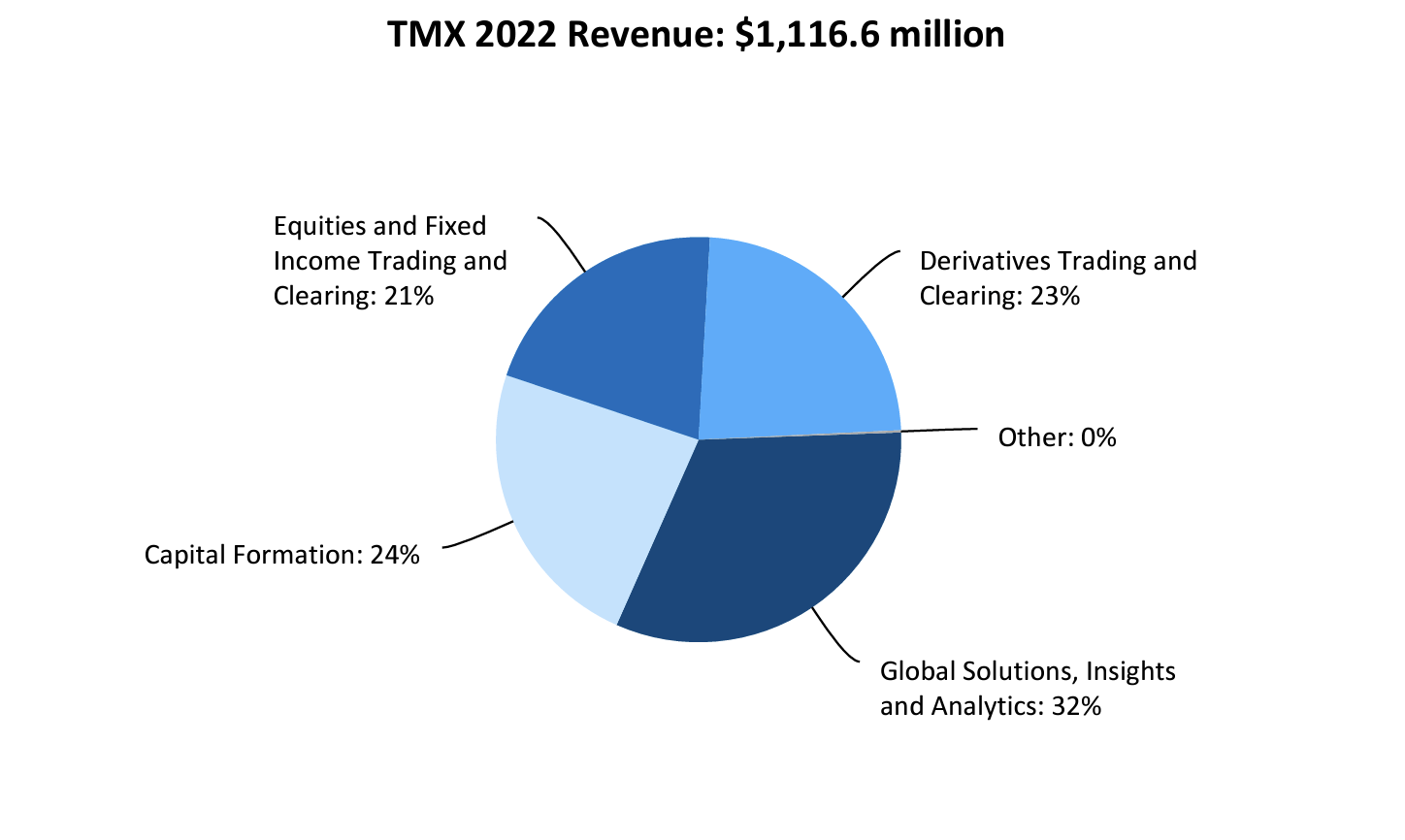

The overview below shows the company's revenue mix. These include the legacy business which includes Capital Formation, Equities and Fixed Income Trading and Clearing, Derivatives Trading and Clearing segment and the non-legacy business of Global Solutions, Insights and Analytics which is becoming an increasingly large share of their revenue.

{kind=link}

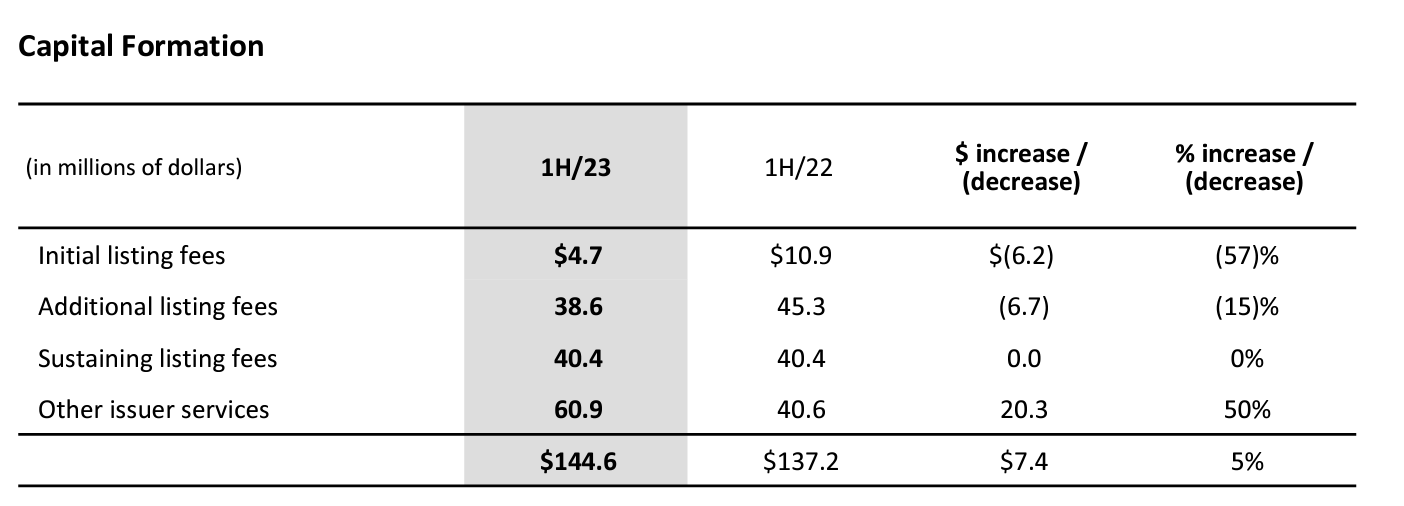

Capital Formation accounts for 24% of revenue as of fiscal 2022. It is comprised of TSX and TSXV, to help companies access the public markets, raise capital and provide liquidity to shareholders. TSX is a leading listings venue for established domestic and international issuers while TSXV is the pre-eminent global platform for facilitating venture stage capital formation. Fees are realized through initial and subsequent listings but primarily from sustaining fees which are fees issuers must pay to remain listed and are based on their market capitalization at the end of the prior year subject to maximums and minimums. This segment can be vulnerable to downturns as companies are less eager to enlist securities in a recession which is what the Canadian economy may or may not be in, but TMX does have the ability to increase fees for those who remain on the exchange to help offset declines in listings. In December 2022 TMX received regulatory approval for price changes for TSX and TSXV listings fees, which increases the TSX maximum sustaining fee to $135,000 and the TSXV maximum new listings fee and TSXV maximum additional listings fees to $70,000.

In addition, TSX Trust has approximately 1,700 transfer agent clients, and revenue is primarily derived from recurring monthly fees, related products, and net interest income on cash balances which is a business segment driven by interest rate levels which has largely offset the declines in initial and additional listing revenue realized YTD.

{kind=link}

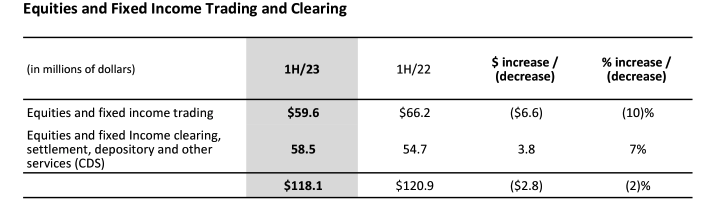

The Equities and Fixed Income Trading and Clearing accounts for 21% of revenue as of fiscal 2022. It consists of TSX, TSXV and Alpha which operate fully electronic exchanges that facilitate secondary trading in TSX and TSXV-listed securities on a continuous auction basis throughout the trading days. Most of the fees on TSX, TSXV and Alpha are volume-based. Shorcan acts as an inter-dealer bond broker that specializes in the Canadian fixed income marketplace, brokering products that include Government of Canada, provincial, corporate, strip, and mortgage bonds, repurchase agreements and swaps. Shorcan charges broker commissions on both sides of the trade upon execution. The division also provides clearing, settlement, and depository services. This division is the most susceptible to a recession as a result of being highly volume-based and we are already seeing this in YTD revenue with trading revenue down 10% from Q2 2022. This decline in revenue has been offset by higher interest income on clearing funds, event management fees, custodial revenues which have increased 7% YoY.

{kind=link}

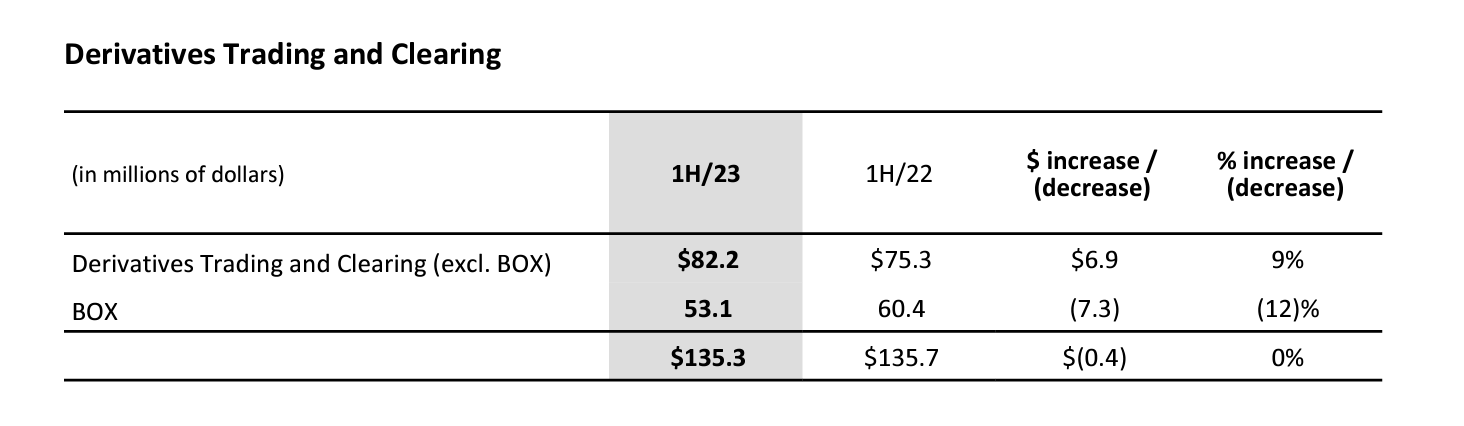

The Derivatives Trading and Clearing segment accounted for 23% of revenue in fiscal 2022. TMX's domestic financial derivatives trading is conducted through MX, which is headquartered in Montréal. MX offers trading in interest rate, index, equity and currency derivatives. BOX is an equity options market located in the U.S. and as at December 31, 2022, MX held approximately 47.9% economic interest in BOX. Those who trade on MX are charged fees for buying and selling derivatives products on a per transaction basis, determined by factors that include contract type and volume of contracts traded. This segment is volume-based but tends to be more stable and can even grow in periods of high volatility as traders tend to be busier with speculating and corporations are keen to hedge risks which increases volumes. YoY this segment experienced flat growth with 85.5 million contracts traded in the first six months of 2023 versus 75.8 million contracts traded in the first six months of 2022 but was offset by lower rates per contract in BOX due to unfavourable product and client mix. There has been virtually no growth in this segment YTD.

{kind=link}

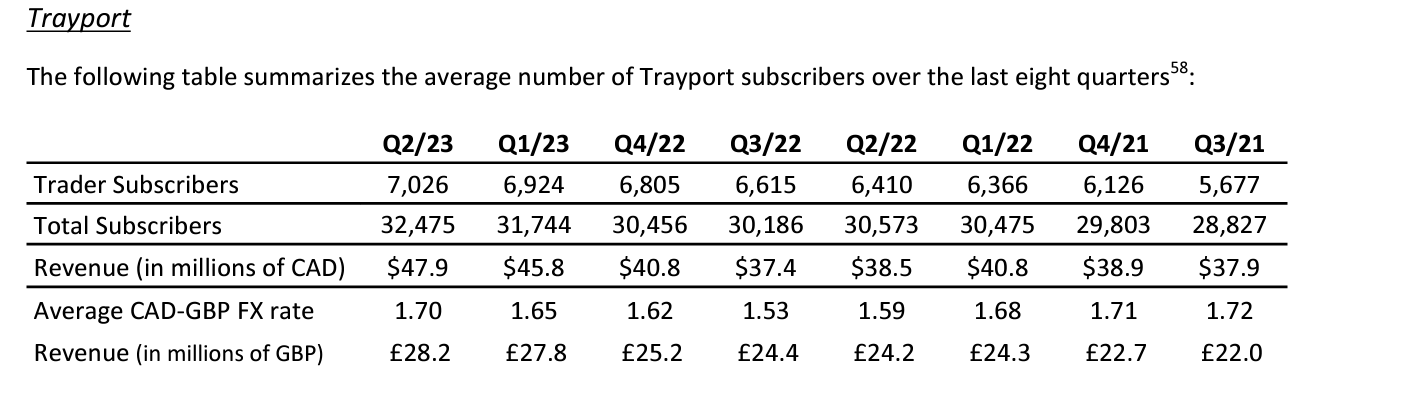

Finally the segment which has experienced by far the most growth over the past two fiscal years, the Global Solutions, Insights and Analytics segment which accounted for 32% of revenue in fiscal 2022 and 34% YTD. This segment delivers data to improve high-value proprietary and third-party analytics to assist clients make better trading and investment decisions, as well as provide solutions to European wholesale energy markets for price discovery and trade execution. With TMX Datalinx, subscribers generally pay fixed monthly rates for access to real-time streaming data, but may also get charged on a per quote basis. Trayport was acquired in 2017 to serve European energy traders. Trayport subscribers pay a monthly rate for access to the platform.

The Global Solutions, Insights and Analytics division has grown 16% YoY due to increases in subscriptions but the growth has been pretty prominent since 2021 with Trayport's trader-subscribers growing 2% quarterly since 2021. Trader subscribers are a subset of Total Subscribers but account for over 50% of total Trayport revenue. Revenue in the segment has increased 4% quarterly since 2021 although it has been assisted by the strengthening GBP the last three quarters. TMX Datalinx subscribers have been flat the last few quarters, but have seen growth through increases in data feeds, co-location, benchmark and indices, and enterprise agreement renewals.

2022 MD&A (TMX GROUP LIMITED) 2022 MD&A (TMX GROUP LIMITED)

{kind=link}

{kind=link}

I see this business segment being resilient to economic shocks as institutional investors and traders if anything tend to have greater demands for data and analytics with increased pressures from clients.

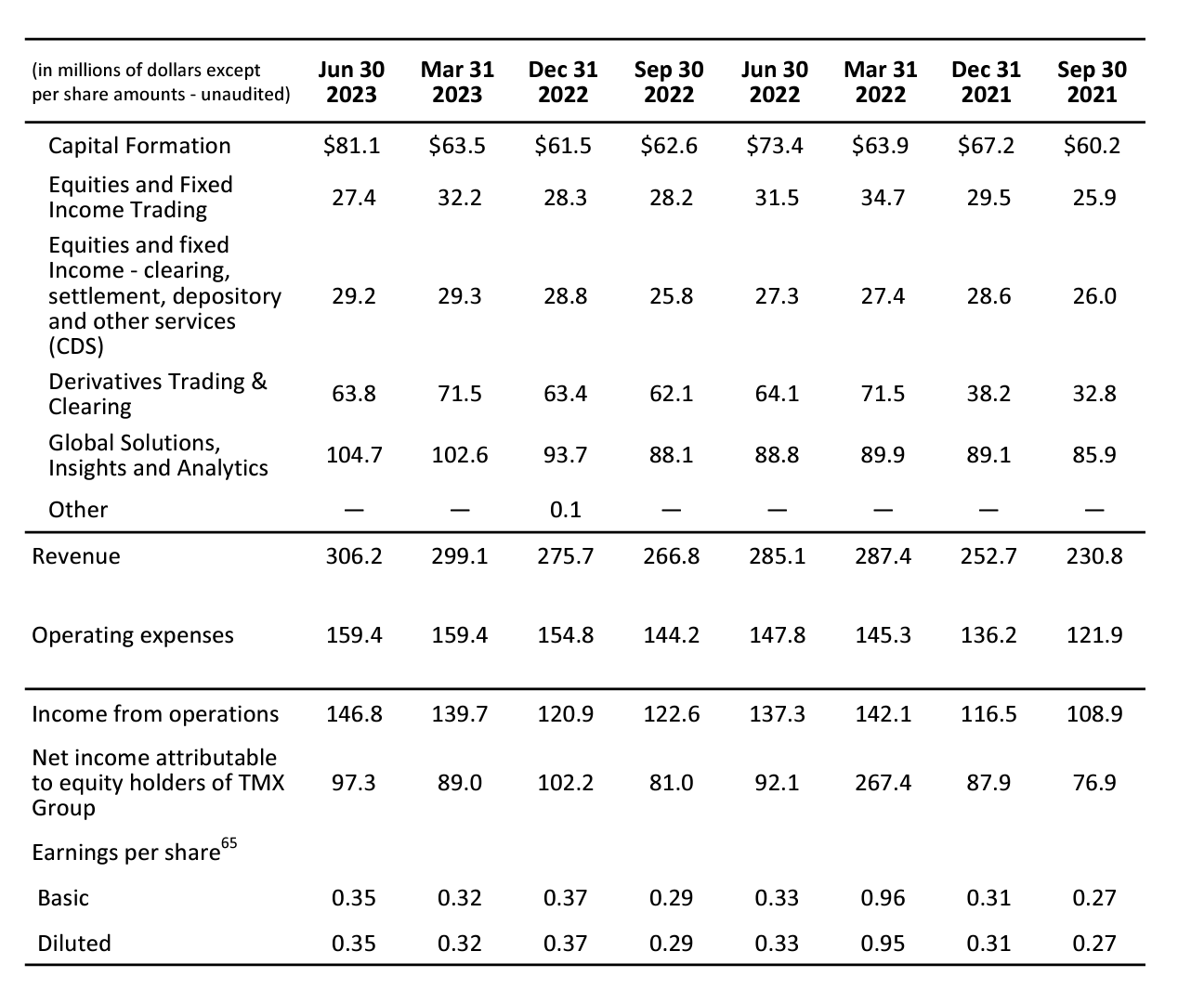

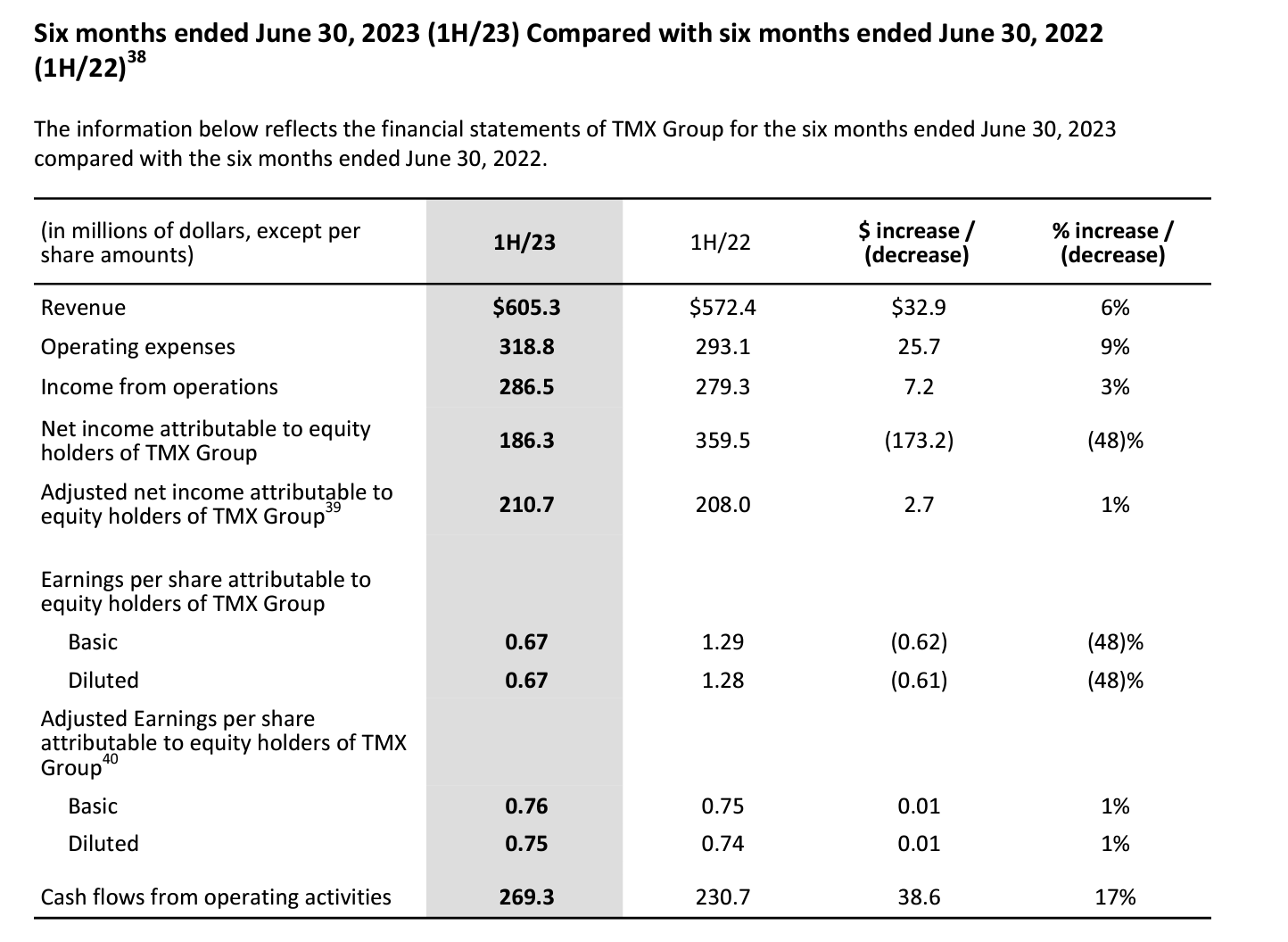

On the whole revenue has increased 6% through the first six months of 2023 from Q2 2022. Unfortunately, this has been offset by a 9% increase in operating expenses which has only increased adjusted EPS by 1%. The increase in operating expenses was attributable to a 14% increase in compensation and benefits which were in large part due to $4.9 Million in one-time integration costs related to AST Canada which otherwise would have increased operating costs 10%.

{kind=link}

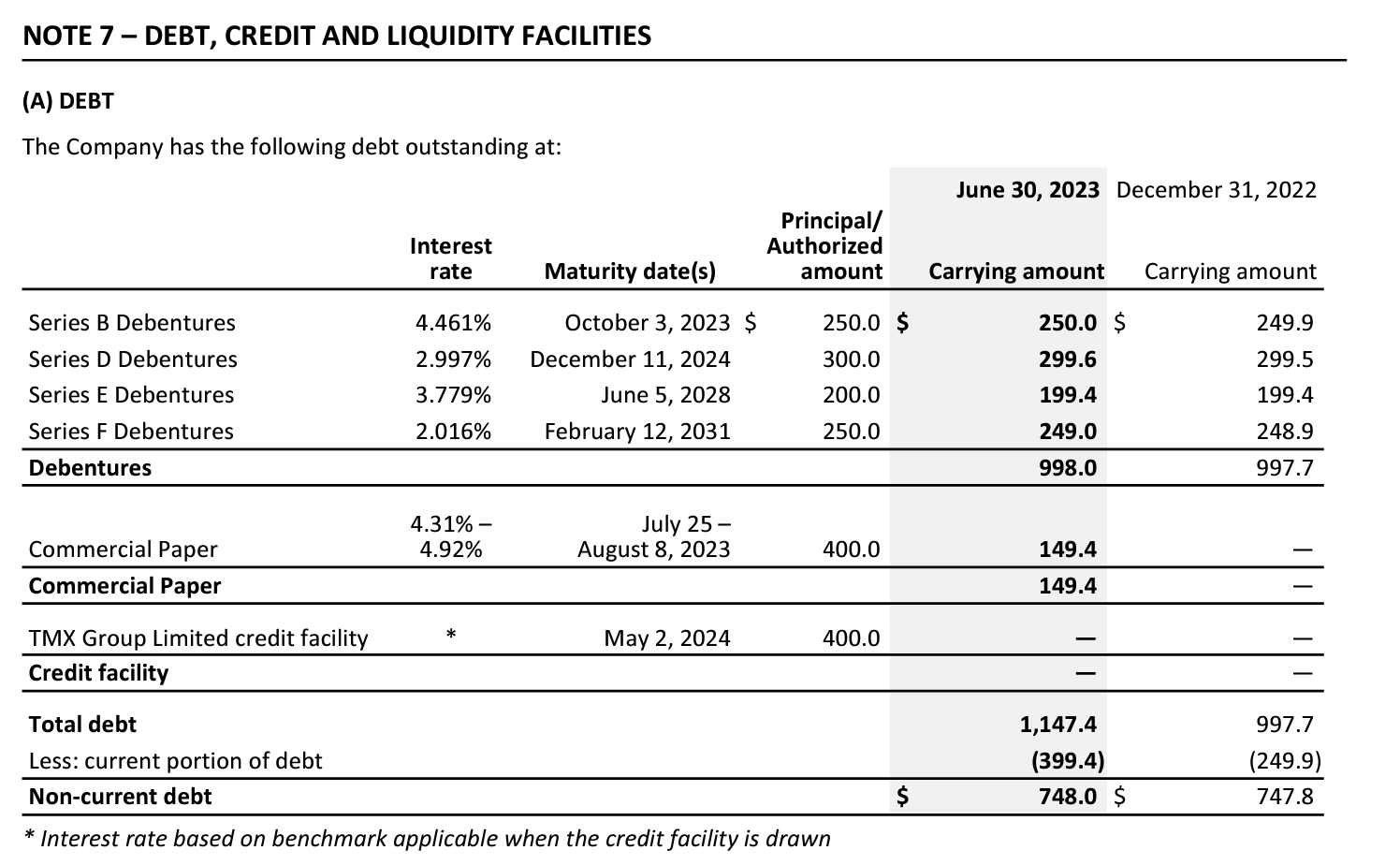

Fortunately, this is an asset-light business with minimal capital requirements. The debt to equity is very low at 14% so I do not expect rising interest rates to affect earnings significantly in the near term. The Series B Debentures and commercial paper will be up for renewal before Q3 2023. TMX is already paying 4.3-5.0% on this debt so refinancing at ~6% on this $400 Million would not impact their interest expense heavily. Moreover, there is ~$690 Million in cash and equivalents so I would expect most of this debt to be retired. The remainder of the $1,150 Million is due between 2024 and 2028.

{kind=link}

Analyst growth expectations for earnings are about 5% annually for the next couple years which is well below the 11% annualized rate of the Global Solutions, Insights and Analytics Business since 2021. The legacy businesses may have seen some decline during the Great Recession, but so far they have held up. If these businesses can at least hold up it would not be unreasonable to expect at least 5% growth in earnings over the next 3-5 years where the Global Solutions, Insights and Analytics Business is responsible for most of the growth. Maybe even 10% if the recession turns out to be fairly mild.

TMX has been one the highest quality Canadian stocks growing revenues, earnings, and returns to shareholders in almost every year since 2005 other than 2009-2010 but even still did not cut the dividend. It maintains strong controls as well as the payout ratio hasn't exceeded 56% in the last five years and operating margin has averaged 48% over the last five years.

Valuation/Verdict

The stock isn't exactly cheap with a forward P/E of 20X but not particularly expensive as it has often traded above 25X. This still equates to an earnings yield of only ~5% which doesn't look like a screaming deal when the Five-Year Canada Bond yield is ~4.20% but the earnings yield is about the same as the S&P TSX Composite Index. The TMX Group's earnings have been far more stable than most companies in the S&P TSX composite index which if anything should demand a premium to the S&P TSX Composite Index.

It also stacks up well against the CME Group Inc. ( CME ). CME owns CBOT, NYMEX, the Kansas City Board of Trade, the NEX Group, and COMEX. TMX is less than a tenth the size of CME by market cap and trading volume but as of Q2 2023 still derives 89% of its business from clearing and transactions rather than market data and information services which in the current climate appears to be a faster growing and more resilient segment which makes the premium less justified.

Therefore if 5% earnings growth is to be expected for the next 3-5 fiscal years, that would still generate 6-8% annual returns at a 21-22X multiple. This doesn't even consider dividend growth and share buybacks which would add 2-3% in shareholder returns. Therefore, not a lot has to go right to achieve at least high single-digit returns which is conservative as I think the legacy businesses are more resilient than have been given credit and could see double-digit earnings growth over the next 3-5 years.

Should the stock fall below 20X earnings I would substantially increase my position.

For further details see:

TMX Group: A Staple For An All-Weather Portfolio