TOL - Toll Brothers: 5 Reasons To Stay Bullish Into Q2 Earnings

2023-05-02 06:19:52 ET

Summary

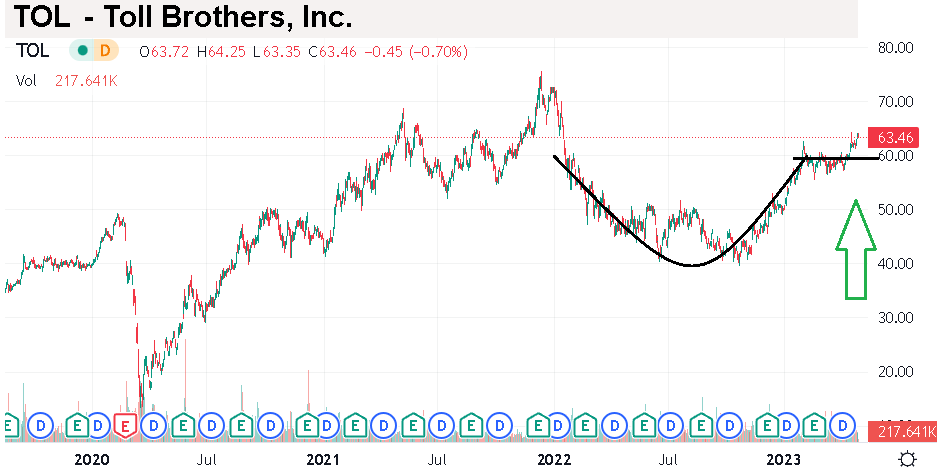

- Shares of Toll Brothers are trading near a 52-week high ahead of its upcoming Q2 earnings report.

- The company's ability to push pricing in the luxury segment of new home construction has helped balance the macro headwinds.

- We see room for shares to keep climbing.

Toll Brothers Inc. ( TOL ) has quietly been a big winner in 2023, with shares up more than 25%. Despite the shifting economic backdrop and ongoing concerns regarding the housing market, Toll Brothers has managed to deliver impressive results. The luxury homebuilder benefits from an extensive backlog and what remains solid demand for new homes.

We like the stock with a sense that TOL is well-positioned to continue generating strong profitability amid resiliency in the broader economy. Stabilizing interest rates and easing inflationary cost pressures are some of the themes that we'll be watching in the company's upcoming Q2 earnings report. Room for the company to exceed what could be a low bar of consensus expectations can work as a catalyst for shares to run higher.

1) Impressive Operating and Financial Trends

Toll Brothers last reported its fiscal Q1 earnings back in February with EPS of $1.70, which beat expectations by $0.31, and up from $1.24 the year prior. The story has been the continued momentum from what was a record 2022 for home sales, fully capturing the exceptional pandemic real estate boom that started in 2020.

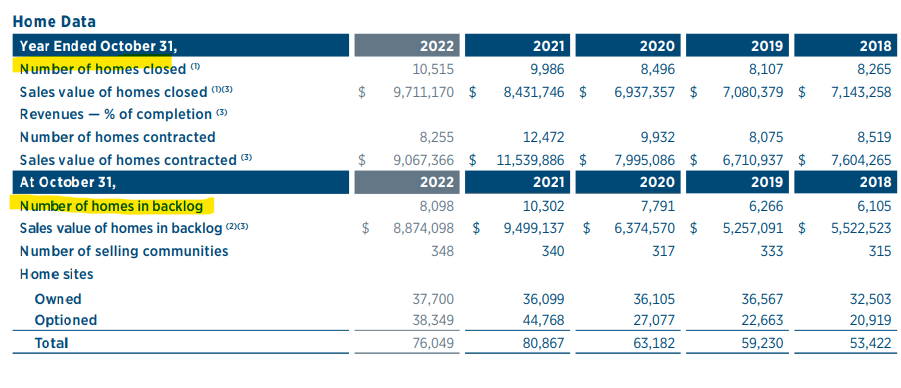

Toll Brothers closed on 10,515 homes , up from 9,986 in 2021, and 8,107 in 2019 as a pre-pandemic benchmark. At the same time, the number of new contracts last year at 8,255 has slowed compared to a high of 12,472 in 2021 and 2020 which reflects the ongoing housing market slowdown amid higher mortgage rates. The uncertainty around these trends has contributed to the volatility in the stock over the period.

{kind=link}

Nevertheless, the takeaway here is the company's financials have been transformed at a larger scale. 2022 revenues approaching $9.8 billion are up nearly 40% from the level in 2020. That strength has been further leveraged by higher average pricing, which crossed above $1.1 million per new construction in the last quarter, up from $956k just last year.

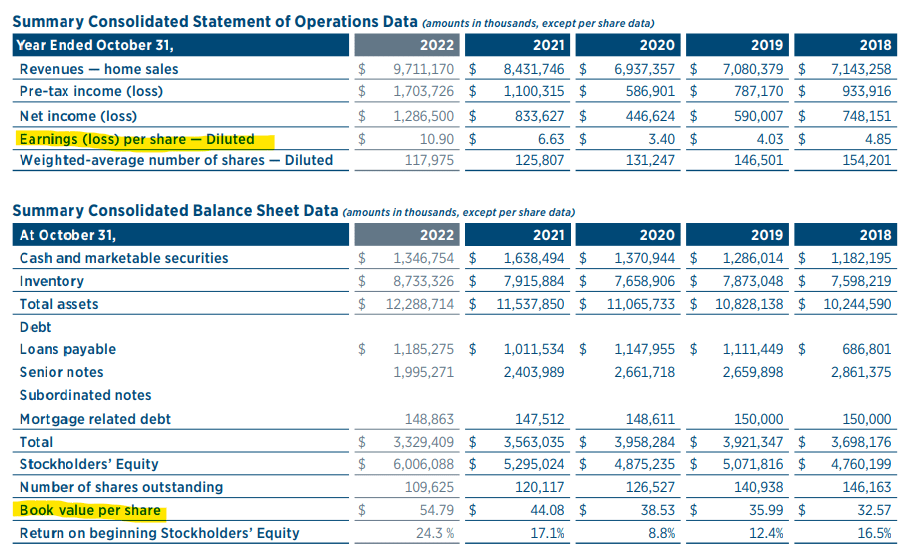

This effort has helped balance inflationary cost pressures on the construction side, as well as the higher cost of capital from higher interest rates. Indeed, net income over the past year has more than doubled in the last 3 years.

The metric that stands out to use is the climbing book value per share which reached $55 in 2022 compared to $36 in 2019. Simply put, Toll Brothers has expanded its profitability with the improved financials even working to reduce the company's debt level. Overall solid fundamentals add a layer of quality to shares of TOL.

{kind=link}

2) TOL is an Earnings Juggernaut

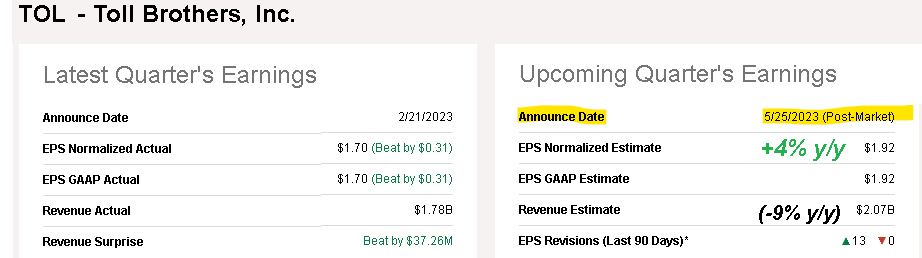

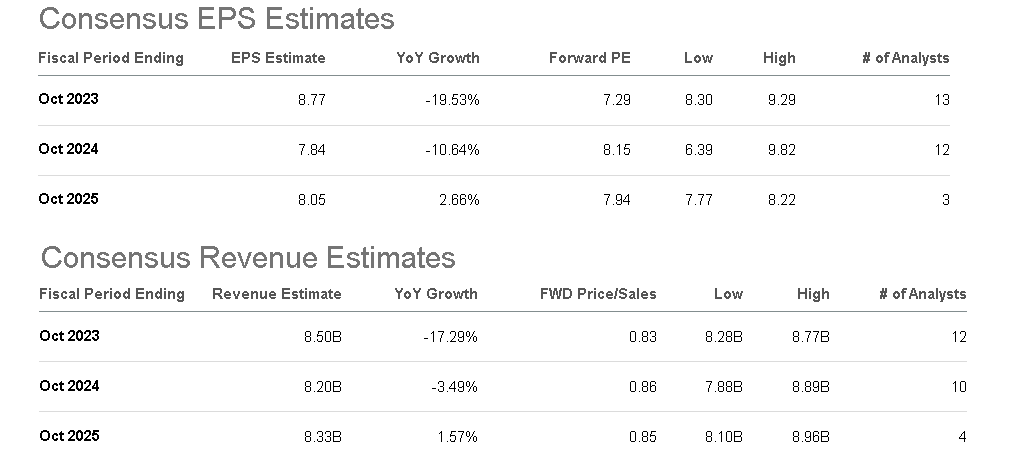

TOLL is set to report its fiscal Q2 earnings on May 25th. The current market consensus is for EPS of $1.92, representing a 4% increase from the period last year. On the other hand, the revenue of $2.1 billion, if confirmed, would be a -9% y/y decline.

Again, the year-over-year weakness on the top line goes back to what was an exceptional start to 2022 leaving a high benchmark of comparables. The expected EPS growth considers some prior guidance by management including the impact of strong home pricing as supportive to the gross margin. Notably, the market theme has been the string of revisions to EPS estimates over the last 90 days, consistent with the recent positive momentum in the stock.

{kind=link}

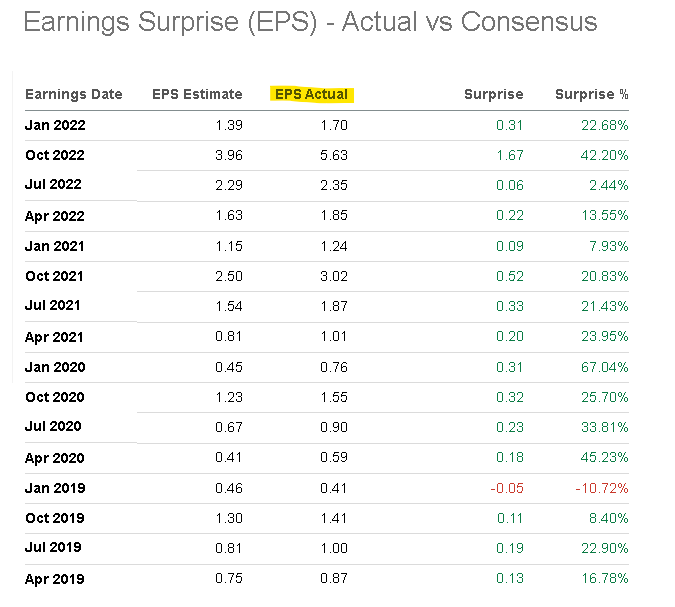

It's worth noting that TOL has a long history of regularly beating EPS estimates. With data for the last 20 quarterly reports, TOL only missed a single while surprising the EPS estimate by an average of 20% since 2019. In our view, there are several reasons to believe this trend can continue.

{kind=link}

3) Easing Inflationary Pressures A Positive For Margins

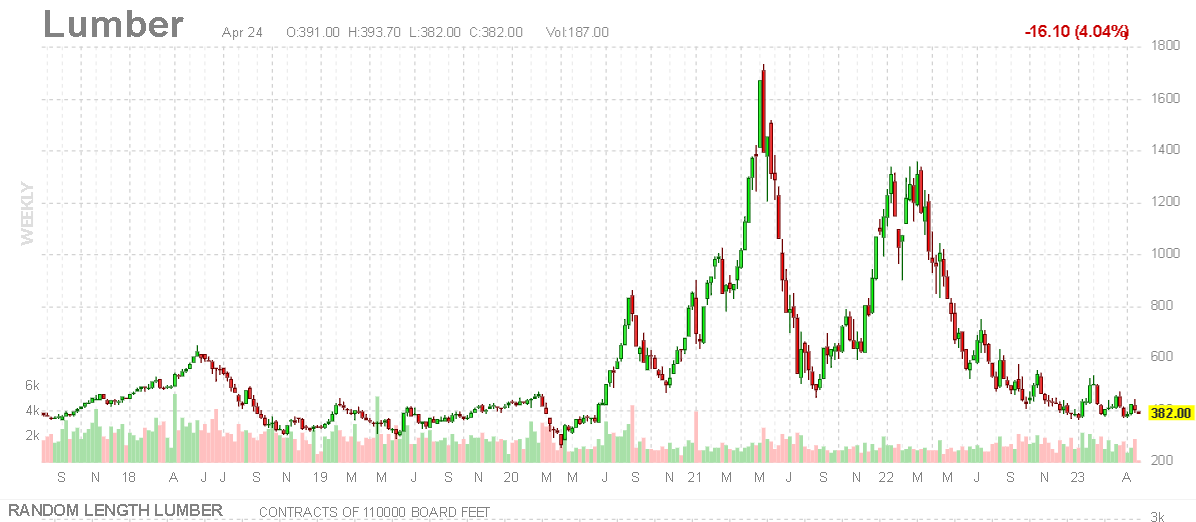

One theme that could be on the table for the Q2 earnings report may be the impact of lower homebuilding costs and construction expenses. Several key commodities including lumber and fuel were previously cited as an industry headwind, while their prices have declined significantly in the past year.

This could play out in a higher gross margin for Toll Brothers, which is a metric that had already been improving in recent quarters but likely has further room to expand. Similarly, management has done a good job of limiting SG&A expenses which have declined as a percentage of revenue.

What makes TOL unique for us is its special focus on high-end of residential construction. The ability of the company to push the pricing for its units based on name and brand recognition supports a positive outlook.

{kind=link}

4) Signs The Housing Market Is Bottoming

The question that remains is how the housing market will evolve through the rest of the year. The good news is that data suggests new construction has been stronger compared to existing home sales, and the slowdown could moderate going forward.

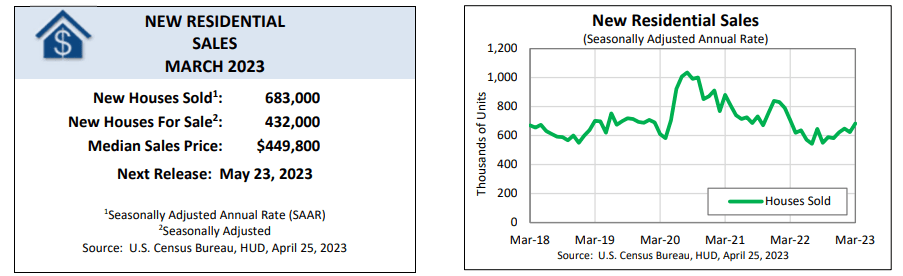

For March, U.S. Census Bureau reported total new residential sales of 683k were up 10% over February, and even 25% higher from the cycle low of 542k last July. While this indicator is still down more than -30% from the pandemic-era high back in 2020, the bigger point is that this current range of around 650k is simply back to averages between 2019 and 2018.

{kind=link}

The apparent resiliency of new residential sales in this cycle corresponds to the trend in interest rates that have stabilized in recent months. This follows some more favorable inflation data and messaging from the Fed that the group may be near the end of its rate hiking cycle.

The 30-year Mortgage Rate is currently at 6.4%, which is elevated compared to trends near 3% back in 2021, but the sense is that the upside is limited from here has helped give homebuyers some confidence.

As it relates to Toll Brothers, the company is proving it can outperform the broader housing construction industry in terms of units sold and pricing. Here is where we see an opportunity to look at the current consensus EPS and revenue estimates for the next couple of years. Even with the market forecasting a -20% earnings decline compared to 2022, the EPS estimate for 2023 at $8.77 and revenue of $8.5 billion are still tracking above the results in 2021.

The potential that the company emerges stronger than expected while macro conditions improve would likely lead to a string of revisions higher for these estimates as a catalyst for the stock.

{kind=link}

5) Value Next To Homebuilding Peers

In terms of valuation, we can point out that TOL trades at a discount to a group of residential construction peers. It's a price-to-book value multiple at 1.1x and even the forward P/E of 7.2x are well below the average from names like D.R. Horton Inc. ( DHI ) or Lennar Corp. ( LEN ). Recognizing Toll Brothers' premium and luxury focus, we make the argument its valuation deserves a higher premium.

That perception of value with TOL also extends to its dividend yield of 1.3%. While a relatively modest amount, TOL has been hiking the rate over the past 2-years and currently offers a higher yield compared to PulteGroup Inc. ( PHM ) at 0.9% of KB Home (KBH) at 1.0%. Shares of TOL would need to climb higher for its dividend yield to converge lower.

Final Thoughts

We rate TOL as a buy with a price target for the year ahead at $80.00, sending shares to a new all-time high by 2024, representing an 11x multiple on year-ahead consensus EPS.

The attraction here is a high-quality builder that is consolidating its lead in its luxury segment of residential real estate. Optimism towards economic conditions with room for interest rates to stabilize should add to the company's long-term earnings potential.

For the upcoming quarterly report, the gross margin and the evolution of the housing backlog will be key monitoring points. The main risk to watch for the stock on the downside would be a deeper deterioration of the housing market that adds further pressure to pricing on the luxury side. Significantly higher interest rates would also force a reset of our bullish view.

{kind=link}

For further details see:

Toll Brothers: 5 Reasons To Stay Bullish Into Q2 Earnings