WFC - Too Much Leverage Could Bite KKR Stakeholders In 2024 Recession

2024-01-01 08:54:14 ET

Summary

- KKR's share price has experienced a significant upside in late 2023, but an overall economic slowdown suggests taking profits or avoiding the stock during 2024.

- KKR has a history of operating business volatility, while financial leverage is expanding on the balance sheet. Both pose a risk to stakeholders during economic contraction.

- Shares are overvalued and carry significant downside risk, with the potential for a -50% or greater drop given a severe recession shock.

KKR & Co. ( KKR ) has just experienced an amazing stock price move to the upside in late 2023. However, the big picture backdrop of a slowing economy is a warning to take profits, sell shares short, or just plain avoid this name during 2024. Why?

The KKR quote has been roughly cut in half (around a -50% loss) four times over the last 13 years (2011, 2015-16, 2020, 2021-22), making it one of the most volatile financials you can hold in your portfolio since 2010. Plus, with leverage on equity near all-time highs for the stock, excessive debt and business asset leverage means the theoretical "risk" to ownership worth is also sitting in record territory, all other variable remaining the same.

It comes down to past recession performance and its extended leverage today vs. peer asset management, banking, and financial custodian firms. KKR's 14:1 "asset" vs. equity leverage is now one of the highest readings on Wall Street from the major money-changing giants. The underlying problem is asset values do plummet, owned businesses face cash flow issues, and credit/bond rating agencies get nervous during economic contractions in America. If we are soon to face a recession, past performance history says you will want nothing to do with KKR next year.

In my view, existing shareholders have been given a nice financial "gift" this Christmas season with the jump in KKR pricing. My suggestion is don't let this opportunity to lock-in gains pass you by. Hedging your profits through the options market, selling shares, and/or setting tight stop-sell orders might be the correct course of action to start the New Year. Let me explain what I am thinking.

Too Much Leverage

To put it bluntly, KKR now runs one of the riskiest balance sheets of the biggest asset management and banking names on Wall Street (and has since 2021). I have drawn a picture of this idea below vs. peers and competitors JPMorgan Chase ( JPM ), Bank of America ( BAC ), Wells Fargo ( WFC ), Citigroup ( C ), Brookfield ( BN ), BlackRock ( BLK ), Blackstone ( BX ), Morgan Stanley ( MS ), Capital One Financial ( COF ), Bank of New York Mellon ( BK ), and Goldman Sachs ( GS ). While none of them runs a business model exactly like KKR's private equity, LBO, and alternative investment focus, the general concept of leverage is very pertinent to my discussion.

For every dollar in equity, KKR now counts $14 in assets controlled through businesses owned and debt holdings. This leverage can absolutely do wonders during good economic times when interest rates are low. But, the flip side is extended leverage can permanently destroy (impair) shareholder value when a recession appears.

YCharts - KKR vs. Major U.S. Financial Peers, Total Assets to Equity, 5 Years

Some history. The Great Financial Crisis of 2008-09 was centered around the use of too much financial leverage. The Federal Reserve effectively allowed the largest money-changing institutions (especially banks) to extend their leverage ratios from a normalized and safer 10:1 reading over the decades closer to 20:1 in 2007. The root cause of the crisis was souring real estate loans, sure. But the disruptive degree of economic turmoil, requiring Lehman Brothers , Bear Stearns , and others to be forcibly closed or sold to others would not have happened with lower leverage ratios. In essence, real estate related losses would have been more manageable (contained) for the whole U.S. financial system.

However, you can see on my graph, leverage ratios have again been rising since 2019, before the pandemic hit. For me, KKR's 14:1 leverage is getting a little scary, in all honesty. Given a sudden and deep recession, where many of its assets decline in value sharply, it might not have enough equity to backstop forced asset losses on the balance sheet. Just the fear of such a rotten outcome could easily reverse the monster share price increase since October into a serious drawdown for shareholders during 2024.

On top of this macro risk to its business model, KKR has a history of lumpy returns from year to year. You can view the wild swings in reported income below as a function of final profit margins, just over the last five years.

YCharts - KKR vs. Major U.S. Financial Peers, Profit Margins, 5 Years

Clear Overvaluation

Too much leverage does not guarantee a bearish outcome for owners. But, the use of too much leverage is usually associated with lower-than-normal share valuations. Not in KKR's case going into 2024. It is actually one of the most overvalued choices today, on top of holding the extra balance sheet risk. It's like a double-whammy of negatives, where owners are really pressing their luck at $83 per share.

The way I look at financials and banks is through two main data points, earnings and book values. On the decade-long graph below, we can see KKR is priced in the top decile (10%) statistically on earnings when they existed (30x), and a record price to book value reading (3.59x) presently.

YCharts - KKR, Price to Earnings & Book Value, 10 Years

Using these two data points in combination, KKR is priced at one of the most elevated positions in the financial peer group today, close to the same expensive position as Blackstone (which operates a less cyclical and very stable business for returns, employing far less leverage, pictured earlier in the article).

YCharts - KKR vs. Major U.S. Financial Peers, Price to Trailing Earnings, 5 Years YCharts - KKR vs. Major U.S. Financial Peers, Price to Book Value, 5 Years

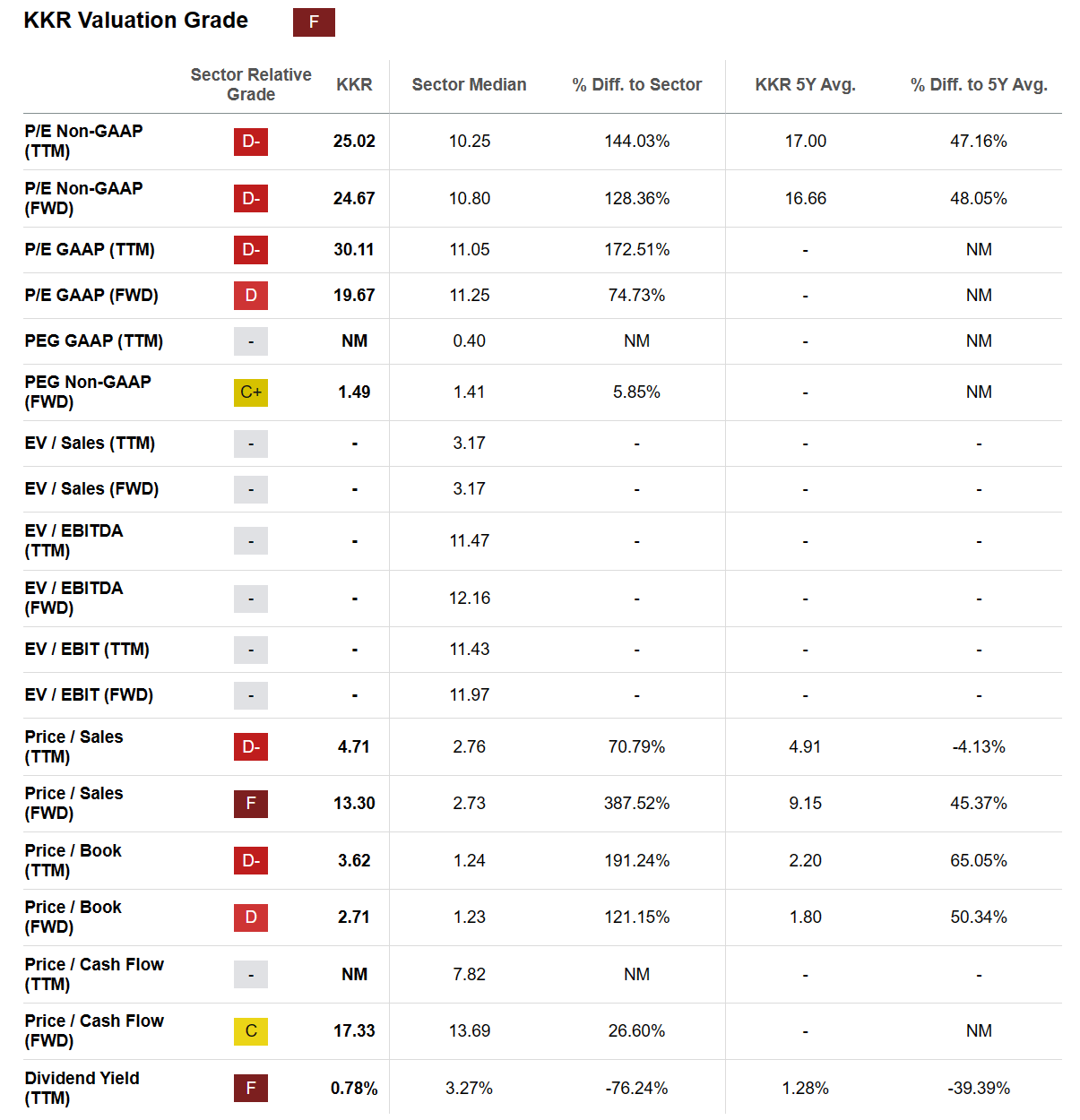

Seeking Alpha's computer sorting system, Quant, gives KKR an "F" Valuation Grade . Compared to peer valuations today and the company's own 5-year history, there isn't much to like about what's backing up each share. And, I will remind you, this horrible rating assumes a decent economy next year. Given a recession, you will not be happy holding this stock, as the failing valuation catches up to the stock quote.

Seeking Alpha Table - KKR, Valuation Grade, December 29th, 2023

{kind=link}

Final Thoughts

Over the past 10 weeks, KKR's almost +60% share price jump ranks as one of the greatest increases ever over a short period of time, and the most bullish since the 2020 pandemic bottom. Optimists are hoping this is the "beginning" of a long-term trend higher, the action usually witnessed after a recession has just ended. Nevertheless, our recession has not even begun yet. (I am still assuming we have one.)

This potential disconnect in investor sentiment vs. reality is truly worrisome. All told, it's like Wall Street and investors in general are thinking the proverbial glass of water is nearly full, when it may be almost empty.

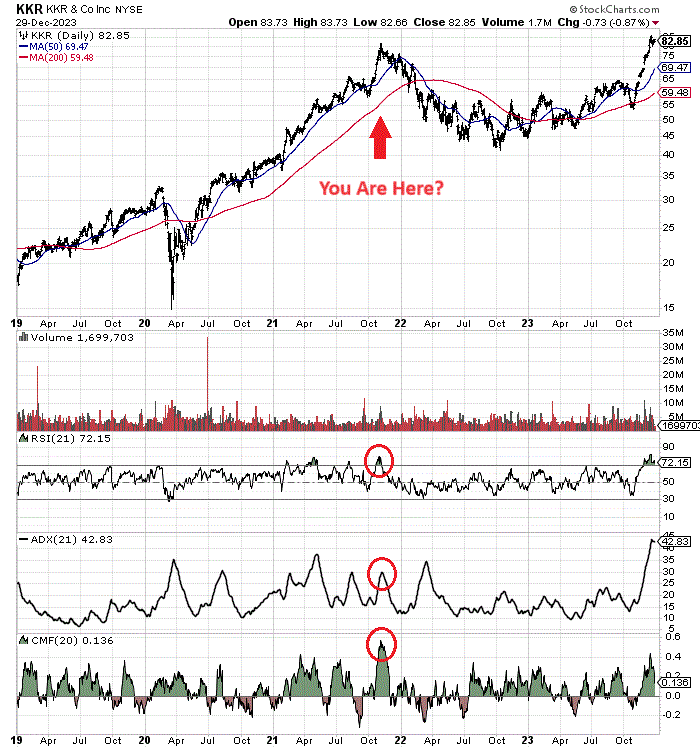

The closest parallel in trading may be the overly optimistic KKR top of November 2021. On the 5-year chart of daily trading below, I have drawn a red arrow pointing at that situation, where a sharp gain was quickly reversed into a near -50% price decline by late 2022.

Today's massively overbought condition is highlighted by the 21-day Relative Strength Index , 21-day Average Directional Index , and 20-day Chaikin Money Flow . I have circled in red the spike highs in each during November 2021. If you knew nothing about KKR's extremely leveraged balance sheet, a purely technical trader would be tempted to sell the current overbought setup, all by itself.

StockCharts.com - KKR, 5 Years of Daily Price & Volume Changes, Author Reference Points

{kind=link}

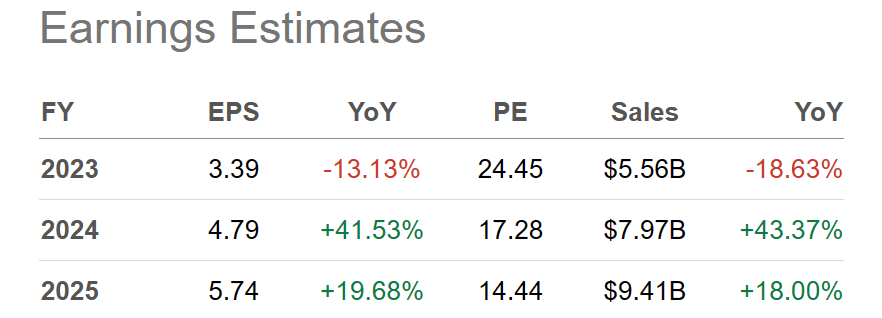

The excuse for the latest rush to buy KKR centers around the belief interest rates are headed lower next year and a soft-landing scenario without recession will be our future. Analyst estimates for 2024-25 earnings growth are quite rosy today, again assuming no recession is in sight.

Seeking Alpha Table - KKR, Analyst Estimates for 2023-25, Made December 29th, 2023

{kind=link}

My view is $83 for price fully values the business in a growing economic environment with declining interest rates, the current conventional wisdom sentiment expectation for 2024. If everything works out in a bullish manner, owning KKR at 15x forward EPS (18 to 24 months down the road) is close to its 10-year valuation average.

There might even be another +10% to +20% of upside, if stock market bubble-logic is approaching during early 2024. However, the downside risk if these assumptions prove wrong is enormous. For starters, the 0.8% dividend yield annually is not much of consolation prize to support the quote.

YCharts - KKR vs. Major U.S. Financial Peers, Dividend Yield, 12 Months

Given a severe recession shock in 2024, another -50% drop in KKR's price would be my initial downside target. And, if we experience a prolonged and deep recession over a period of several years, projecting a KKR quote closer to ZERO is not that difficult. In the end, share ownership investment risk holding KKR's massive leverage may be closer to -100%. Don't laugh, cry maybe.

Remember, a -50% price drop would get the valuation on book value back to 10-year averages (median and mean), not below them! If a recession decimates book value, and investors discount all the leverage with a sub-average price to book value multiple, KKR may fall in price to a number well under $40.

YCharts - KKR, Price to Book Value, Decade Averages, 10 Years

For me, the risk/reward equation makes absolutely no sense to own KKR. Do you really want to hold a KKR stake in your portfolio, if my math arguments are accurate? Balancing +20% in best-case upside gains, against -100% in worst-case scenario downside losses, with equal odds for either outcome over the next 12 to 18 months, is a tough ask to buy.

I rate KKR a Sell and Avoid. I have no interest in owning it until we experience another -50% share price drawdown. If you continue to own KKR from $83, you have to pray nightly a recession is avoided in 2024.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Too Much Leverage Could Bite KKR Stakeholders In 2024 Recession