SPY - Too Risky To Buy Now After The Parabolic Rise?

2023-12-30 10:23:23 ET

Summary

- The market efficiently priced the Fed pivot since October, which produced a parabolic rise in S&P 500 in Nov/Dec.

- As long as the fundamentals hold, and the Fed cuts as expected, the S&P 500 is likely to continue to rise in 2024, and any potential dips are buying opportunities.

- The risks are that 1) the disinflationary process stalls prematurely, or 2) the recession still hits, despite the Fed cuts.

The global macro playbook

As a global macro investor/trader, my stock market strategy is fairly simple, I am long stock by default unless:

- The Fed is expected to increase interest rates aggressively.

- There is an imminent recession.

- There is a risk of an imminent systemic credit event.

Accordingly, I was bearish on S&P500 in 2022 when the Fed started one of the most aggressive monetary policy tightening ever, which was a correct view as the S&P500 fall by more than 20%.

During the process of interest rate hikes, the Fed inverted the yield curve in 2023 by a record amount, which was supposed to cause a deep recession sometimes in late 2023 or early 2024. Specifically, the inverted yield curve causes restrictive supply of capital, which eventually causes lower business investment, and ultimately higher unemployment - that's a recession.

Furthermore, the inverted yield curve disproportionally negatively affects overleveraged, less profitable firms, which ultimately produces a credit event, and a deeper stock market selloff.

Thus, I was also bearish on S&P500 in 2023, expecting that recession. Specifically, my view was, what I define as, timidly bearish, since the probability of a recession was high, and yet the economy continued to outperform. My timidly bearish view was executed by selling deep out of money call options on S&P500 futures ( SPX ), with expiration in December 2023. That was essentially the view that the stock market would not go up as much, rather that it would go down. I planned to implement a more aggressive short position once the recession becomes more obvious.

This was a correct view - until the November/December parabolic move higher. Specifically, as of late October the equal weight S&P500 ( RSP ) was down for the year, as well as the economically sensitive small stocks ( IWM ). Unless you were heavily invested in the magnificent 7, your diversified portfolio was down in October for the year - that's because the recession was expected. In fact, I was able to exit the short call positions profitably in October. So, I view this as a correct strategy overall.

Turning bullish

So, what happened in October? The entire bearish case was based on the assumption that the Fed would continue to hold interest rates high and the yield curve inverted until the recession arrived - as this was necessary to bring inflation down to the 2% target. This is the "higher-for-longer" theme.

In November, the Fed Governor Waller, who is known as a hawk, suggested that the Fed could start cutting interest rates because inflation is falling faster than expected, and a recession might not be necessary to restore price stability. This triggered a sharp move higher in the stock market. The Fed Chair Powell confirmed this view at the post-FOMC meeting press conference.

Essentially, the Fed abandoned the "higher-for-longer" policy with a disinflationary normalization policy to bring the interest rates to the neutral level, likely as soon as possible. Thus, the market priced a significant monetary policy easing in 2024.

What does this mean? The Fed is likely to reverse the interest rate hikes and likely to steepen the yield curve, which significantly reduces the probability of a recession and a systematic credit event.

So, 1) the Fed is expected to lower interest rates, 2) the probability of an imminent recession significantly decreased, and 3) the probability of an imminent credit event also significantly decreased. That's not bearish for stocks anymore, thus, it's bullish by default.

The timing risk

The only problem is that I changed my view to bullish after the parabolic rise since October, with S&P500 ( SP500 ) near all-time high. Thus, the risk of a technical correction caused by profit taking is very high. Furthermore, if there is a technical correction, and the fundamentals change subsequently, I could be changing my view again to bearish at a much lower price. This is not a profitable strategy - buy high, sell low. Thus, I am implementing my current bullish view as a covered call on S&P500 futures ( SPX ) and I will actively manage this position on a way down and on a way up by adjusting the long futures/short call option ratio.

Implications - don't look back

The efficient market hypothesis states that the market correctly prices all incoming information, and the future price move is a function of the new information. Thus, to predict the market moves you need to predict the future information. Looking at the charts is looking at history, and that's not very helpful. So, why even look at the chart, and the recent parabolic move, it doesn't matter. As long as the fundamental view of no imminent recession holds, the market is likely to move higher.

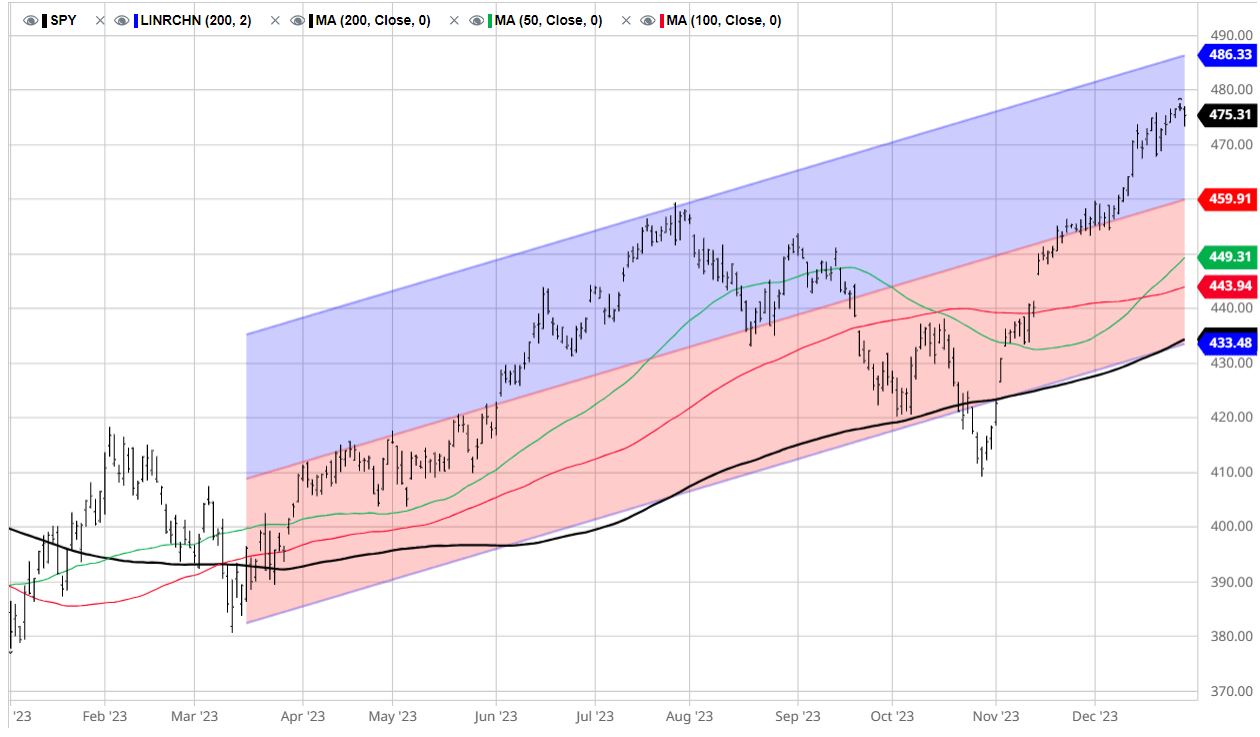

So, here is the chart for S&P500 ( SPY ), it's up by nearly 16% since October 27th. Note that, the equal weight S&P500 ( RSP ) is by 18% since October 27th, and it was down for the year in October. So that's the recent parabolic move.

{kind=link}

As previously explained, the recent parabolic move in S&P500 was due to the efficient pricing of the new information - the Fed abandoned the "higher-for-longer "policy and now it plans to cut interest rates aggressively before the recession arrives, which cancels the recession.

So, what are the risks of buying now? The risks are:

- The Fed walks back and delays the cuts. In this case the market overpriced the expected cuts, and also the recession probability increases. Thus, let's follow closely all Fed communication for the clues. In my view, this is unlikely, as this Fed does not want to disappoint the market.

- Unexpected increase in inflation. The Fed could be forced to delay the cuts if the disinflationary process stalls. However, due to the base effects and the predictable decrease in rents, the disinflationary process is likely to stay on track at least until June.

- The recession hits despite the Fed cuts, or the Fed cuts are due to a recession. In other words, the inverted yield curve possibly did the damage already. In addition, the excess savings are gone, the student loan repayments resumed, the debt levels are high, delinquencies rise, housing crashes...This scenario is unlikely until the labor market weakens; thus, it is important to monitor the labor data, especially the weekly claims data.

So, yes, there are risks of buying now, but not due to the parabolic rise. The risk is that the fundamentals could change - as always is.

Tactically bullish for now.

Wish You a Happy and Prosperous New Year!

For further details see:

Too Risky To Buy Now After The Parabolic Rise?