SPY - TopBuild: A Good Buy At Current Levels

2024-01-08 00:32:03 ET

Summary

- TopBuild is well-positioned for growth due to the recovery of the residential end-markets, positive supply-demand dynamics, and government stimulus programs helping industrial demand.

- The company's revenue growth has been impacted by a slowdown in the residential end-markets, but the outlook is positive with a recovery expected in the coming years.

- TopBuild Corp. has a strong margin outlook, with potential benefits from sales leverage, labor productivity improvements, and cost synergies from recent acquisitions.

Investment Thesis

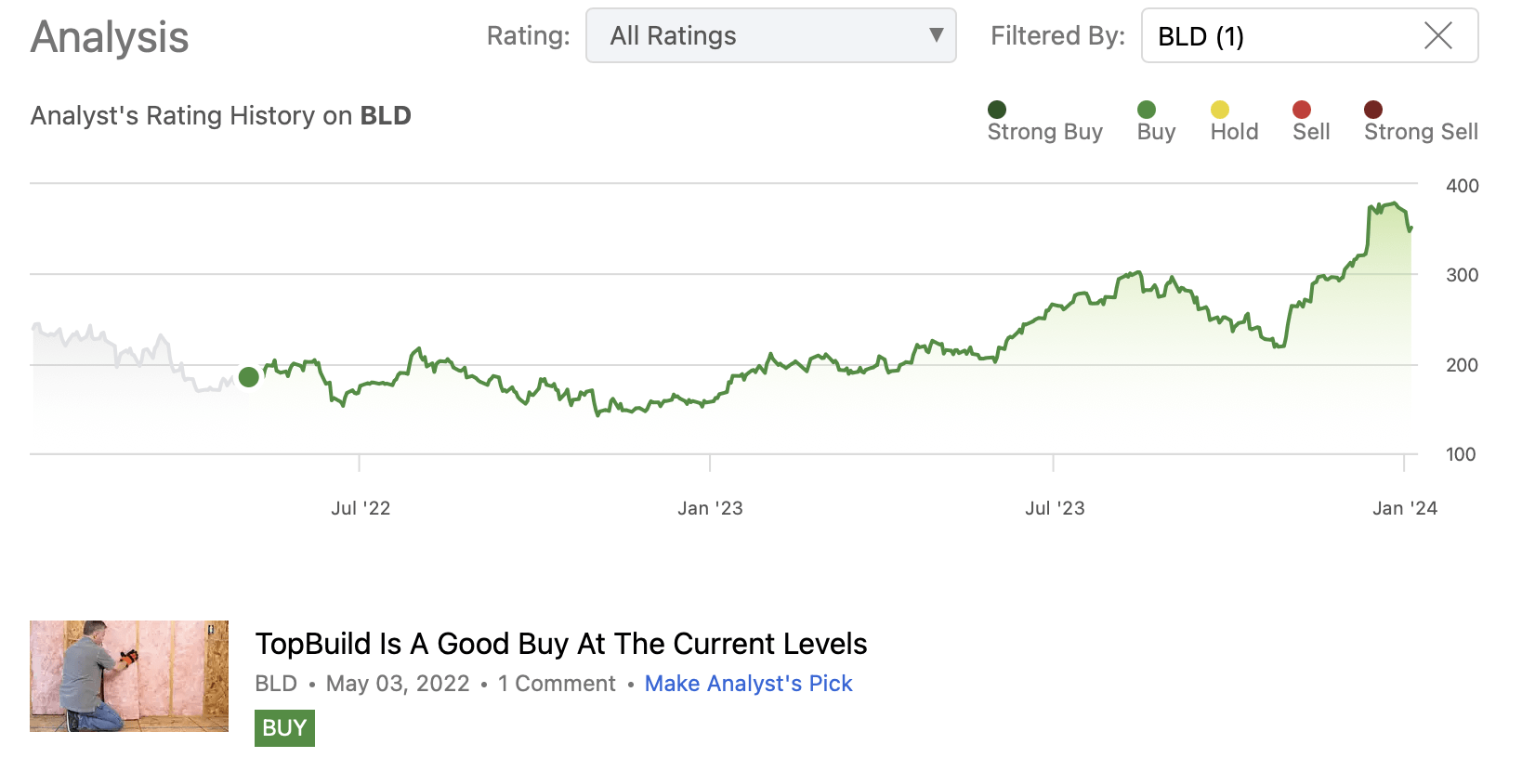

TopBuild Corp. ( BLD ) is up a solid ~90% since I last recommended buying it in May 2022, massively outperforming S&P 500's ( SPY ) ~12.5% gain during the same period. While the broader market was worried about rising interest rates at that time, I expected limited downside due to the tight demand-supply situation in the housing market. Further, the acquisition of Distribution International was expected to help the company post revenue growth even during the downturn.

BLD's performance since my previous recommendation (Seeking alpha)

{kind=link}

My thesis played out as expected, and looking forward, the company remains well-positioned to deliver good growth. The company’s revenue growth should benefit from the recovery of the residential end-markets in the coming years, driven by the reversal of the interest rate cycle and positive long-term supply-demand dynamics resulting from a decade of new homes underbuilding, supporting the overall end-market outlook. In addition, good demand in the heavy construction side due to U.S. reshoring trends and various government incentive programs should help the Commercial and Industrial end markets. Further, volume comparisons are also easing in the coming quarters. In the medium to longer term, favorable demand trends from increasing focus on energy efficiency of buildings in the U.S., and accretive M&As should support revenue growth.

On the margin front, the company should benefit from increasing volume leverage with the recovery of end markets, productivity improvement measures, and cost synergies from the integration of the recent SPI acquisition. Moreover, the company is trading at a discount to its historical averages, making the valuation look favorable. Hence, I rate the company a buy.

Revenue Analysis and Outlook

In the years following the pandemic, TopBuild’s revenue growth benefited from pent-up demand in the residential end market and lower mortgage rates. In addition, good contributions from acquisitions also helped the company grow its topline. However, in 2023, the company’s growth rate started to moderate as a result of the slowdown in the residential end-markets especially in single-family households due to increasing mortgage rates in an inflationary environment.

In the third quarter of 2023, the company continued to face headwinds from slower single-family starts earlier last year as there is a lag between housing construction starting and the insulation installation services being used. This led to volume decline in the Installation segment. Moreover, the company’s Specialty Distribution segment largely services the single-family housing market, and as a result of the end market weakness, this segment also faced volume declines. In addition, pricing also moderated as improved availability of raw materials in the Speciality Distribution segment pressured prices. These headwinds were offset by a healthy backlog in multi-family housing, good demand in commercial/industrial end markets, and inorganic growth from acquisitions in the Installation segment.

As a result, total company sales increased by 1.9% YoY to $1.32 billion. Excluding a 2.9 percentage point benefit from acquisitions, same-branch sales (organic sales) declined by 0.9% YoY. This same-branch sales decline reflects a 1.7 percentage point volume decline and a 0.8 percentage point benefit of average selling price increase. On a segment basis, revenue increased by 4.9% YoY in the Installation segment, reflecting 0.1% growth in same-branch sales due to price increases partially offset by volume decline and a 4.8% growth from acquisitions. The Speciality Distribution segment’s sales declined by 2.1% YoY due to lower volumes and pricing.

BLD’s Historical Revenue (Company Data, GS Analytics Research)

BLD Product, End-market Channel and Segment Breakdown (Q3 2023 Earning Call Presentation Slide)

Looking forward, the company’s revenue growth outlook is positive. The residential end market which accounts for ~64% of the company’s revenue is poised for a good recovery in the coming years as the interest rate cycle reverses. The long-term supply-demand dynamic is very favorable in this market thanks to over a decade of underbuilding of new homes post the great housing recession of 2008. This explains the reason behind a relatively shallow housing slowdown in 2023 despite interest rates being at multi-decade highs. Thanks to this relatively tight demand-supply situation, I expect a swift recovery in this market once the interest rate cycle reverses which should help BLD’s sales.

The Commercial and Industrial end market, which accounts for remaining sales, has been seeing fairly robust trends and the bidding activity remains strong, especially on the heavy construction side. This can be attributed to the recent reshoring trend and demand from related mega projects. This demand is further catalyzed by the Federal government’s stimulus programs like the CHIPS and Science Act and the Inflation Reduction Act.

While there are some pockets of weakness on the light commercial construction side like office buildings, I believe the upcoming interest rate cycle reversal should improve the demand there as well, as it increases the return on investment on those projects.

In addition to recovering end markets, the company should also benefit from easing volume comps, especially in the Specialty Distribution segment in the coming quarters.

So, the company’s near to medium-term growth outlook looks positive.

In the long term, the company is well positioned to benefit from the trend towards sustainability as building codes across the U.S. are becoming stricter requiring higher building efficiencies. One good example is California's Title 24 building standards code, which is driving higher insulation demand and the need for better insulation solutions. The Inflation Reduction Act also provides tax credits for the builders of energy-efficient buildings. I expect building code requirements to keep becoming stricter and the government to continue providing incentives for buildings with lower carbon footprints helping the demand for the company’s offerings.

In addition to good organic growth prospects, the company should also benefit from its bolt-on M&A strategy which should help it gain market share. While the company has a relatively solid market share of ~40% on the residential side, its market share in commercial and Industrial insulation is low double digits. The company recently announced the acquisition of Specialty Product and Insulation, or SPI, a North American Specialty distributor with a strong presence in the Commercial/Industrial end market (~80% of its $700 mn annual sales) to improve its position in this market. The company’s good track record of M&As coupled with the fragmented nature of the markets makes me positive about the company’s inorganic growth outlook.

Overall, I am optimistic about the company’s near-term as well as long-term growth prospects.

Margin Analysis and Outlook

Over the last year, the company was able to more than offset headwinds from inflationary materials and labor costs, and volume deleverage due to a slowdown in single-family housing end markets through price increases, productivity improvements, and cost synergies from acquisitions.

In the third quarter as well, the company was able to deliver margin expansion despite the negative impacts of lower organic volumes. High margins in multi-family and commercial projects due to a better mix, operational efficiencies due to labor productivity improvements, and continued benefits from acquisition cost synergies helped the company offset headwinds from organic volume deleverage. This resulted in a 130 bps YoY increase in adjusted gross margin to 31.7% and a 150 bps YoY increase in adjusted EBITDA margin to 21.4%.

BLD’s Historical Adjusted Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, the recovery in end markets should also help the company’s margin which should see benefits from sales leverage. The company has guided for incremental EBITDA margin (organic) in the 22% to 27% range. In addition, insulation installation is a labor-intensive process and the company is working on improving labor productivity through better use of technology which should help margin in the medium to long term.

BLD's Strategic Focus on Technology (Investor Day May 2022 Presentation Slide)

The company’s margin should also benefit from cost synergies from the integration of the recent SPI acquisition. Management has given a target of $35 million to $40 million in run-rate cost synergies by year 2, with half of it coming from improved material sourcing and leveraging TopBuild’s scale and best practices, while the other half coming from operational improvement like leveraging IT spending across the two companies, back office synergies and achieving enhanced asset utilization.

So, I am optimistic about the company’s margin expansion prospects.

Valuation and Conclusion

TopBuild Corp is currently trading at a 16.9x FY24 consensus EPS estimate of $20.81, which is below its historical 5-year average forward P/E of 17.62. On a TTM basis, if we look at the FY23 consensus EPS estimate of $20.81, the company is trading at a 17.87x P/E which is also a discount to its 5-year average P/E ((TTM)) of 19.11.

In the initial periods of interest rate cuts, the stock typically trades at higher-than-average multiples as its growth prospects are augmented by end-market recovery catalyzed by these rate cuts. For example, just before the pandemic, when the Federal Reserve started lowering interest rates in 2019, the stock's P/E multiple jumped to the low 20s. After the pandemic-induced rate cuts catalyzed end-market demand, the multiple was even higher (mid to high 20s.) While I am not expecting the P/E multiple in the mid to high 20s range that we saw in the years immediately following the pandemic, I believe a P/E multiple can reach ~20x given we are in the early phases of recovery in the end market which should be catalyzed by interest rate cuts. So, the stock looks undervalued. Further, the sell-side estimates also look conservative as they are still not building in the benefits of SPI acquisition (which is not closed yet) in their estimates and the sell-side consensus is likely to get revised upward making the valuation cheaper than what it looks based on consensus estimates.

{kind=link}

I believe the company has good growth prospects ahead as it should benefit from the recovery of the residential end-market with interest rate cycle reversal in coming years, secular demand trends in the Commercial and Industrial end-markets, easing volume comparisons, increasing demand for higher building efficiency products amid stricter building codes across the U.S., and inorganic growth. Margins should also increase with volume leverage, productivity improvements, and cost synergies. Hence, lower than historical valuation and good near and long-term growth prospects make the company a buy.

Risks

- Inorganic growth is relatively riskier compared to organic growth as there are risks associated with post-acquisition integration and the company overpaying for an acquisition. While the company has a good track record of disciplined inorganic growth, if it overpays for an acquisition or fails to realize intended synergies there may be a downside.

- Investors are expecting multiple rate cuts this year and I concur. However, if there is any delay in rate cuts or the pace is slower than expected, it may negatively impact investor sentiments.

For further details see:

TopBuild: A Good Buy At Current Levels