CA - Topicus: Good Organic Growth More Acquisitions Deep Dive Into Q1 Earnings

2023-05-16 10:50:07 ET

Summary

- Topicus.com Inc. reported a solid quarter, with strong revenue growth.

- Organic growth was again a highlight, especially in maintenance and recurring.

- Cash flows were mixed due to a change in receivables and the absence of the preferred dividend. I explain both things.

- Topicus still has substantial dry powder to deploy into acquisitions this year.

Introduction

Topicus.com Inc. ( TOI:CA , TOITF ) reported Q1 earnings last week and they were good, as usual. Last quarter the company had somewhat muted the fears of decelerating organic growth, and this quarter set the continuation of that trend. Organic growth was again the highlight. The lowlight was operating cash flow conversion, driven by increased receivables. Something similar happened to Constellation Software Inc. ( CSU:CA , CNSWF ) a couple of quarters ago. For those who wouldn't know, Topicus was spun out of Constellation.

Without further ado, let's dig right into the numbers.

The numbers

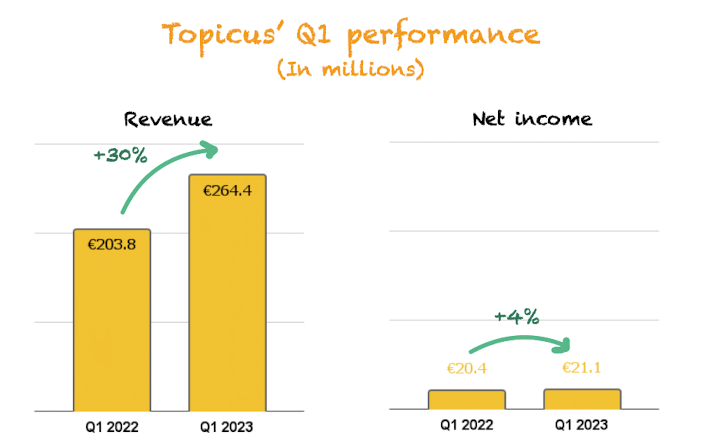

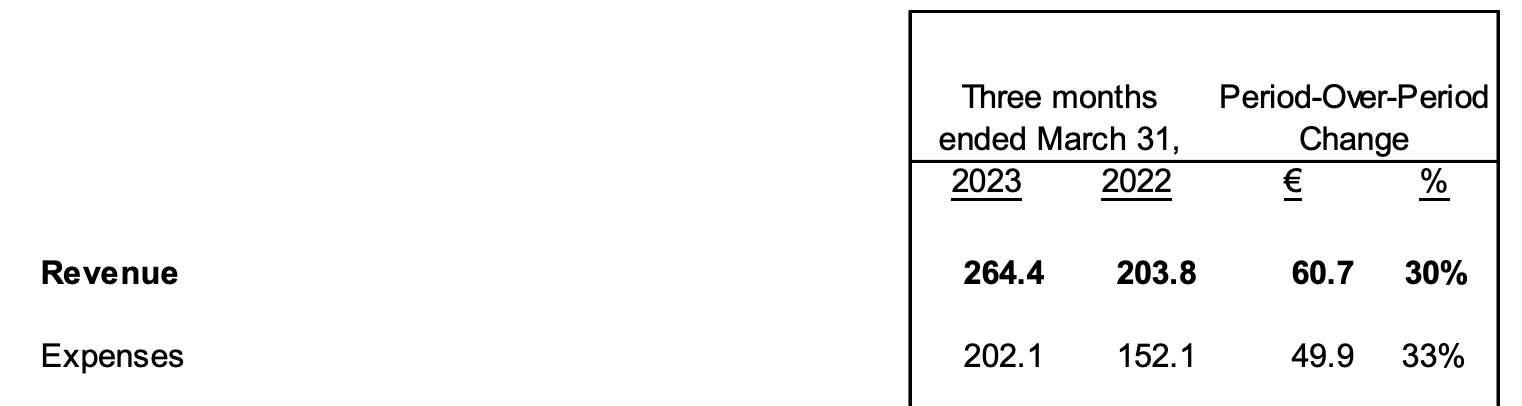

Topicus' top line growth was excellent, accelerating from last quarter. Topicus grew its revenue by 30% year-over-year to €264.4 million. Net income barely grew 4% year-over-year, but net income attributable to the equity holders of Topicus grew 20% year-over-year:

{kind=link}

There was margin contraction for yet another quarter, something we must get used to as the company grows fast by deploying capital into acquisitions.

Digging deeper into the top line

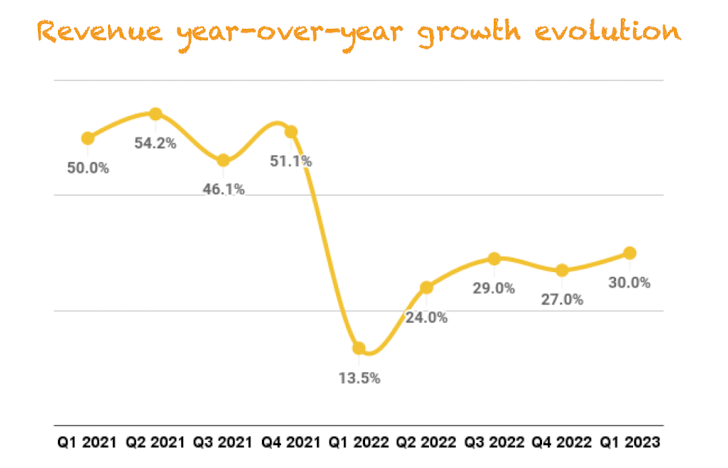

Quarterly revenue growth was great, although it faced easy comps:

{kind=link}

We should expect volatility in the company's numbers. Topicus' growth comes primarily from acquisitions, where the timing causes ups and downs. Acquisitions are difficult to predict, even for management. Investors who want predictable growth will probably be disappointed with Topicus, especially at this small size.

But if we zoom out and look at Topicus' Q1 revenue evolution, we can see that the CAGR has been great despite the lumpiness:

Made by Best Anchor Stocks

Topicus managed to grow revenue sequentially as well, albeit at a slower pace than it has been used to.

Growth was primarily inorganic, as you should expect from a serial acquirer, but organic growth was a pleasant surprise for the second quarter in a row. Recall that organic growth is a Key Performance Indicator ("KPI") for Topicus, as a good deal of the Spinout thesis of TSS to acquire Topicus was to acquire organic growth expertise that could later be applied to other operating groups and business units. What was interesting to see was Topicus' CEO discussing during the AGM that he is running an experiment regarding compensation and organic growth (emphasis added):

I'm running an experiment, Howard. So within Topicus, we have three operating groups. TSS Public and TSS Blue, and we have the Topicus Operating Group. Topicus Operating Group was historically very strongly focused on organic growth, and we implemented our Constellation bonus team for this company based on organic growth and not on net revenue growth. It's an experiment.

Source: Robin van Poelje, Topicus' CEO, during the Annual General Meeting.

This change makes plenty of sense, and I can envision a scenario where it jumps to other operating groups if it works well. Only including organic growth in the compensation scheme is dangerous because it can lead to a growth-at-all-costs mentality, but Topicus can control this threat by also including Return On Invested Capital.

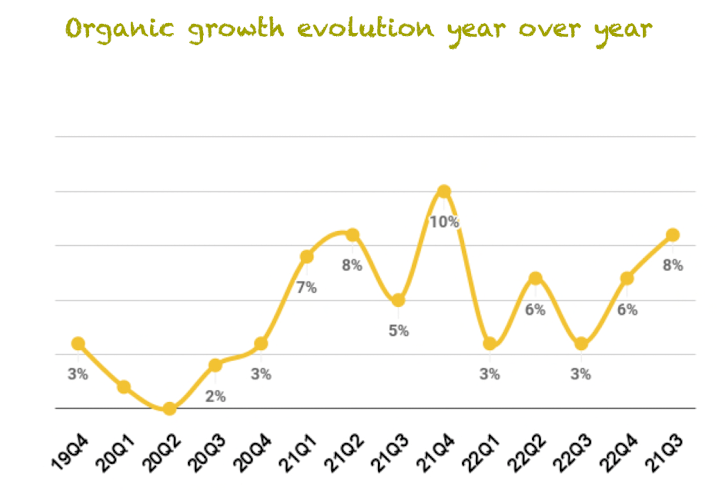

Topicus' organic growth of 6% last quarter was a pleasant surprise after the low organic growth in Q3. This quarter, organic growth accelerated further to 8% year-over-year :

{kind=link}

It's fair to say that the fears of low organic growth and the thesis not playing out are mostly behind us. The low organic growth was just a consequence of growth volatility, which we should be ready for going forward, although to a lesser extent than in inorganic growth.

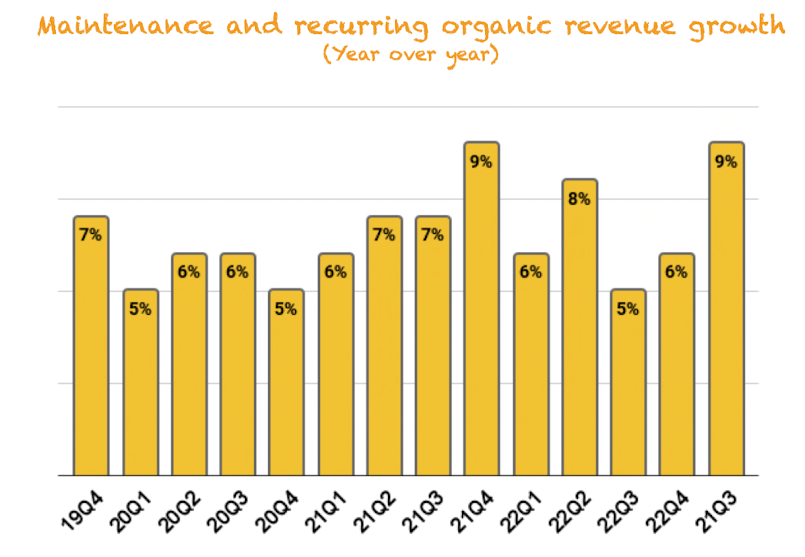

Organic growth volatility is absent in some of the underlying revenue sources of the company. Maintenance and recurring revenue (management's preferred revenue source) grew at one of the highest rates of the last 14 quarters, at 9% year-over-year, and has shown excellent stability through this uncertain economic period:

{kind=link}

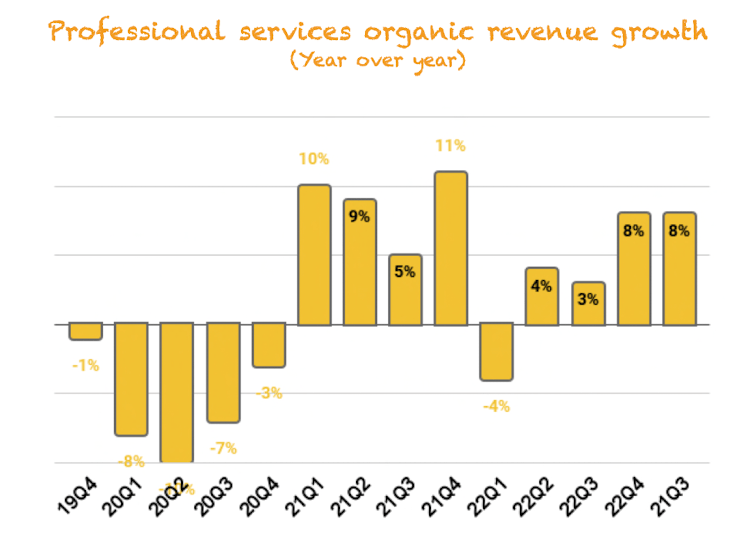

In last quarter's earnings digest for Best Anchor Stock subscribers, we mentioned that the organic growth of most other revenue sources was pretty volatile and that we should focus on maintenance and recurring. We have to take our words back, as professional services revenue seems to be relatively stable, too. This revenue source was heavily impacted during the pandemic because these services are conducted mostly in person:

{kind=link}

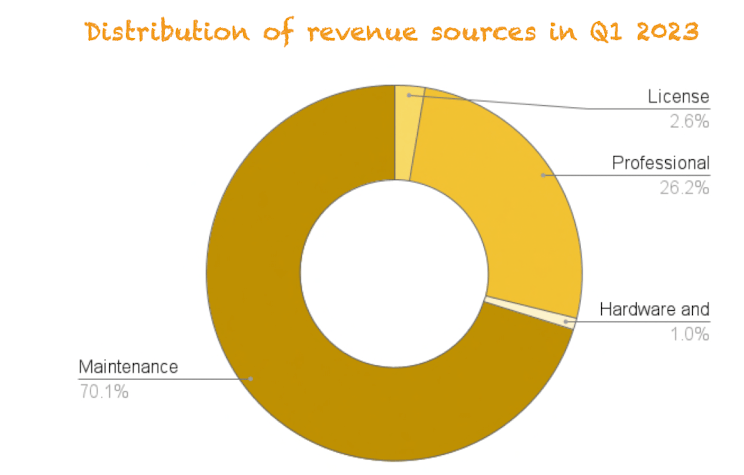

Both maintenance and recurring and professional services make up the majority of the company's revenue (96.3% of Q1 2023 revenue), and their proportion is increasing:

{kind=link}

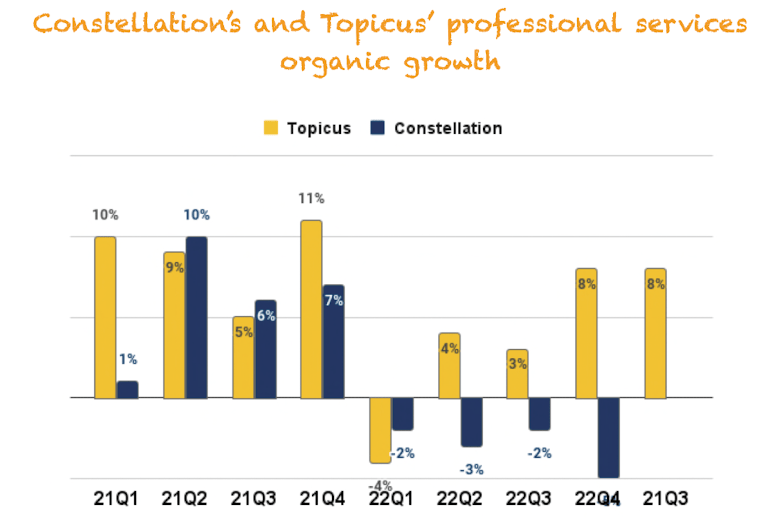

This is great because having most of the revenue tied to more predictable revenue sources will reduce the volatility in overall organic growth, helping the company be more predictable. Constellation Software also generates most of its revenue from these two sources, but in their case, professional services revenue is much more volatile, leading to more volatility in organic growth:

{kind=link}

This said, most of the company's revenue growth will come from acquisitions in the foreseeable future, so we will see significant volatility in top-line growth regardless of organic growth stability. There's little management can do to reduce M&A volatility, as acquisitions do not always present themselves at a steady pace.

Expenses and profitability

For yet another quarter, expenses grew faster than revenue. The differential was not as high as in the last quarter (27% revenue growth vs. 36% expenses growth), but it was still present:

{kind=link}

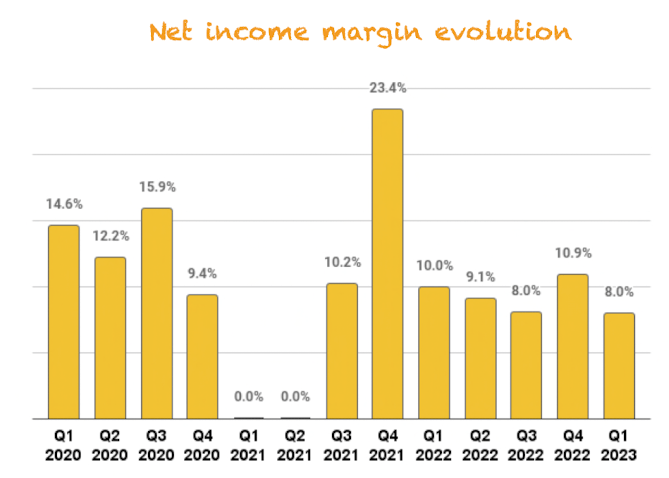

This differential made the net income margin decrease again, now sitting at one of its lowest levels for a long time:

{kind=link}

As evident in the graph above, there's significant margin volatility that also stems from acquisitions. Most of the increased expenses are acquired. As Topicus (like most companies in the Constellation universe) mainly acquires companies in trouble at a low price, it's fair to assume their margins are lower than they should be and lower than the company average. It takes some time until Topicus streamlines the expenses of these companies to match the company average. If more of the growth is organic in the future, we should see significant margin expansion, as this is a more profitable revenue source.

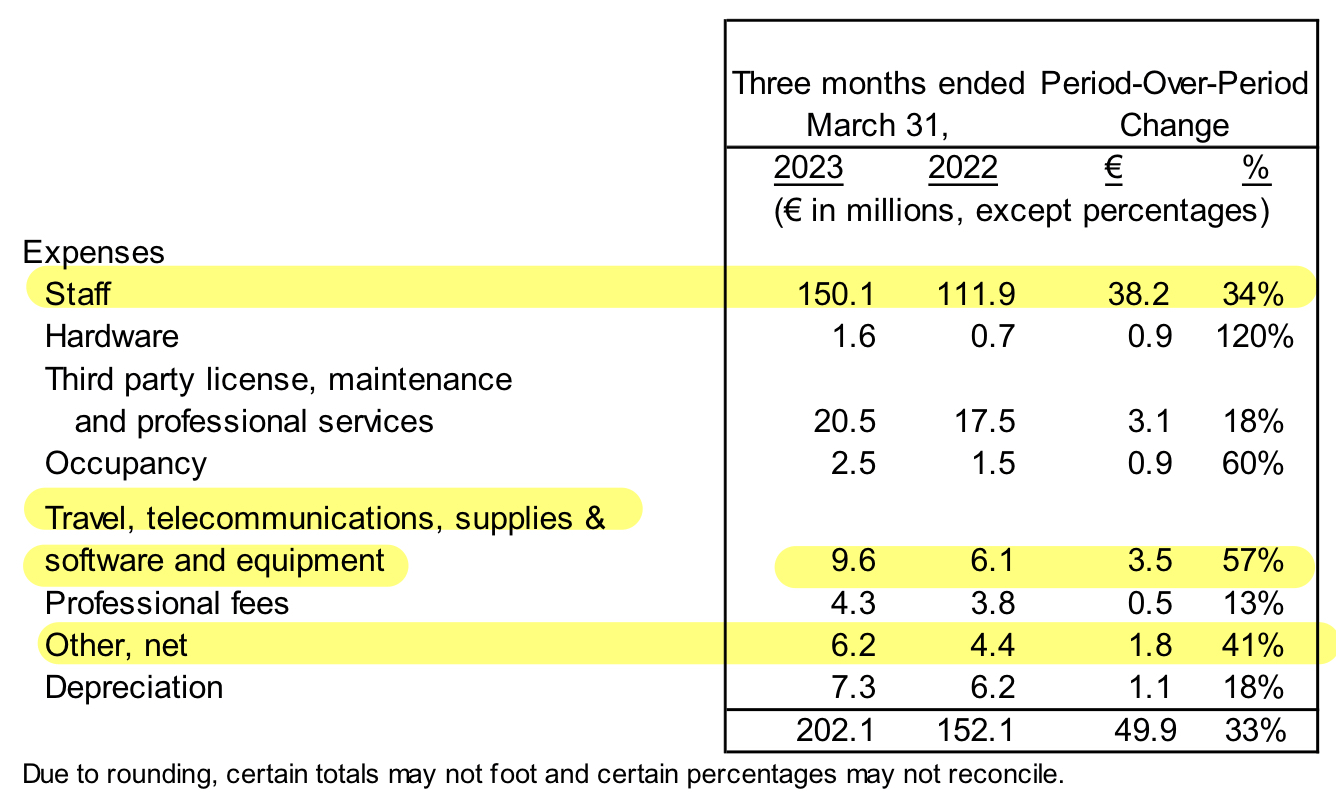

Looking at the expense table, we can see that increased expenses came from the usual suspects (i.e., the same as last quarter): staff, travel, and other, net :

{kind=link}

Both staff and travel expenses increased due to acquired businesses, with the latter probably being impacted by a more normalized travel environment. This is something management discussed during the Annual General Meeting too (emphasis added):

You also see it in travel costs. I think, as we're now sort of moving out of the pandemic and a lot of us are sort of back to much higher levels of travel , you definitely see it in that part of it.

Source: Jeff Bender, Harris CEO, during the Annual General Meeting.

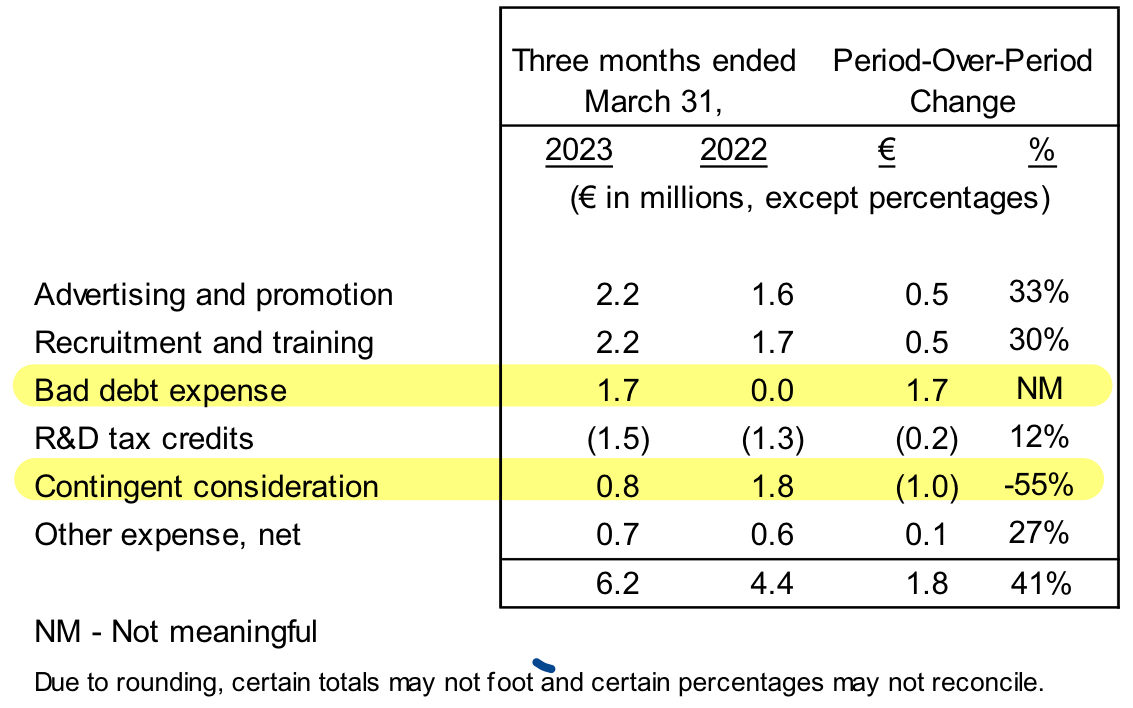

Other, net was not a main driver of the expense increase, but there are several interesting things embedded in it:

{kind=link}

The item that added the most significant increase this quarter in Other, net was Bad debt expense which increased from €0 to €1.7 million, but what is this? When invoices remain outstanding for more than 365 days, the company provisions this amount and allocates it to 'Bad debt expense' to indicate that it might never recover the amount. However, management said that the customer plans to pay the bill:

The customer has indicated that they plan to pay the outstanding amount.

When the customer pays the bill, we should see the company write down the provision and reduce other, net expenses in the quarter this happens.

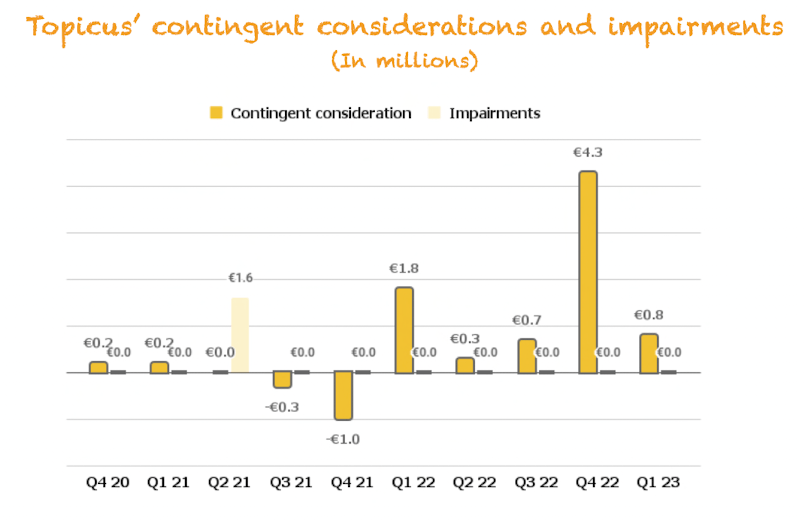

The other expense we always discuss is contingent consideration . This expense measures the payments the company has to make if acquisitions are producing better results than previously expected. A rise in this expense is bad for margins, but it's good at the same time because it shows us that Topicus is conservative in making its acquisitions. Contingent consideration decreased year-over-year but remained positive for yet another quarter.

The flipside of contingent considerations is impairments, which the company incurs if an acquired company fails to deliver on the targets assumed in the investment thesis. This quarter marked the 8th consecutive quarter of no impairment charges. The graph below may indicate that Topicus is, on average, making good acquisitions:

{kind=link}

When we discuss both metrics, we always write a disclaimer, so we'll leave it here:

Note that this conclusion is not entirely accurate as impairments apply to every acquisition, but we don't know how many acquisitions are made with contingent considerations.

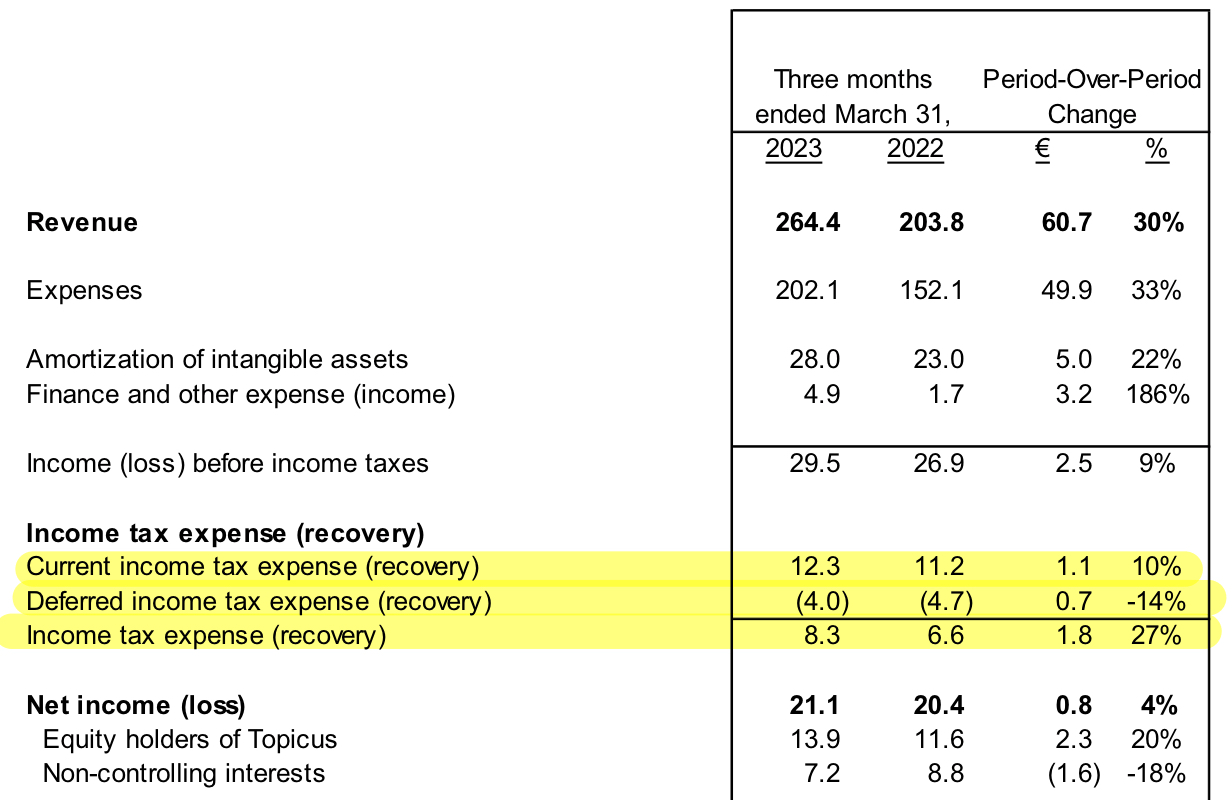

Taxes were also a headwind to net income, as they increased considerably more than operating income. The current income tax expense did increase in line with operating income, but the company has less recovery of taxes this quarter:

Topicus' Q1 Management's discussion and analysis

{kind=link}

To be honest, we wouldn't focus too much on quarterly taxes, as they will be quite volatile and don't tell us much about the company's operations.

The divergence between net income for equity holders and non-controlling interests was interesting. Consolidated net income grew slightly, but most of this growth accrued to equity holders of Topicus and not to the non-controlling interests, which saw their profits decrease 18% year-over-year:

{kind=link}

We have looked into this topic, and even though we don't have an exact answer, we think the differential might come from one of two sources or both:

-

Companies where there's a non-controlling interest (Geosoftware, Sygnity, and Subsurface) performed worse than the average company owned by Topicus during the quarter

-

Currency exchange rates weigh negatively on the profits of these companies as most of them have their operations in non-euro-denominated currencies

Note, too, that it might result from quarterly discrepancies in profits for companies included in NCI and not mean much. This said, we wanted to share how we think about this. Unfortunately, management gives us little detail on this topic, so we can only speculate with some possible explanations.

Looking at cash flows, the key metric

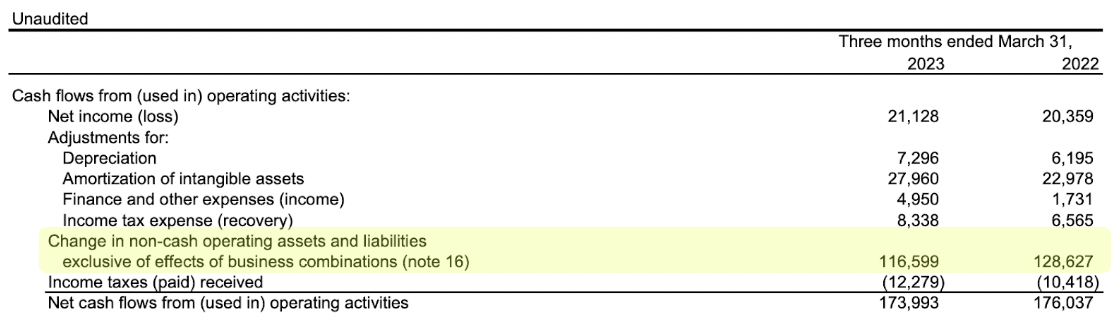

Operating cash flow growth was weak this quarter, decreasing 1% year over year. Low net income growth didn't help, but neither did some specific elements of operating cash flow:

Topicus Q1 Management's discussion and analysis

{kind=link}

Weakness was primarily created by an unfavorable change in non-cash operating assets and liabilities:

Topicus' Q1 financial statements

{kind=link}

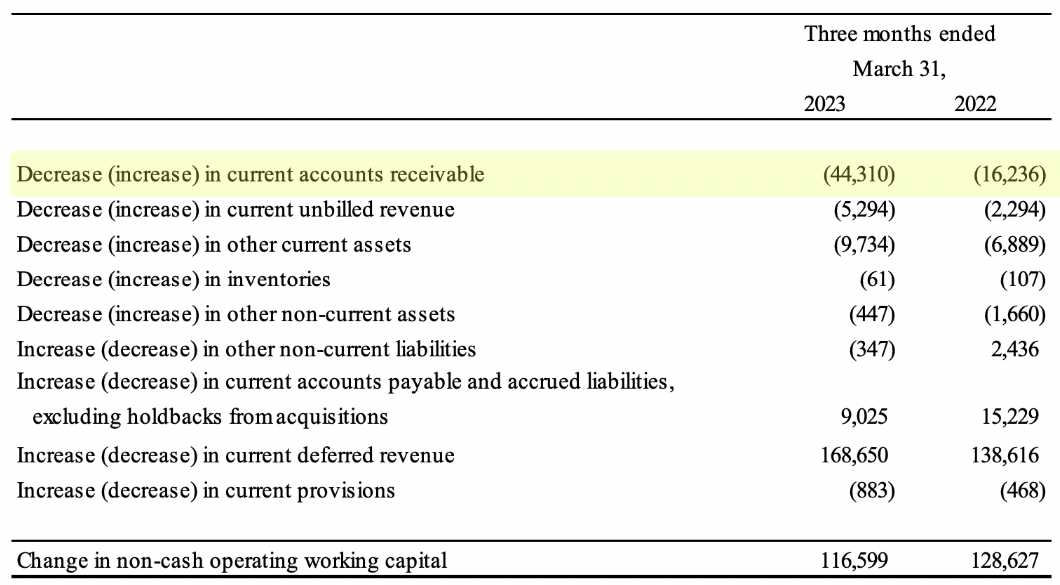

If we double-click here, we get to the following table, which shows that most of the weakness came from an increase in accounts receivables :

Topicus' Q1 Financial Statements

{kind=link}

This is somewhat coherent with the bad debt expense we discussed earlier. The company's receivables are aging, and we see this both in the P&L (through provisions) and cash flows (through worse cash conversion). We don't have much visibility on this topic, and management simply disclosed the following (emphasis added):

Contributing to the decrease in CFO was an increase in aged accounts receivable at March 31, 2023 compared to the same period in 2022.

Seeing receivables climb faster than revenue is never a great sign, although it might be a consequence of customers being more diligent with their cash flows during this period of economic uncertainty.

This is a topic we should monitor closely, both for Topicus and Constellation. Constellation suffered a similar impact some quarters ago for similar reasons, with management writing the following (emphasis added):

The primary reason for the decline in CFO for the three and six months ended June 30, 2022 is that CFO includes the impact of changes in non-cash operating assets and liabilities exclusive of effects of business combinations or "changes in non-cash operating working capital.

There are many reasons contributing to the non-cash operating working capital variance none of which are indicative of an underlying concern with the Company's overall non-cash operating working capital balance. Specifically, no concerns with accounts receivable or unbilled revenue aging.

Something similar might have happened in Topicus' case. As we are mainly going "blind" here, we must trust the company's managers, who have given little reason through the years to distrust them.

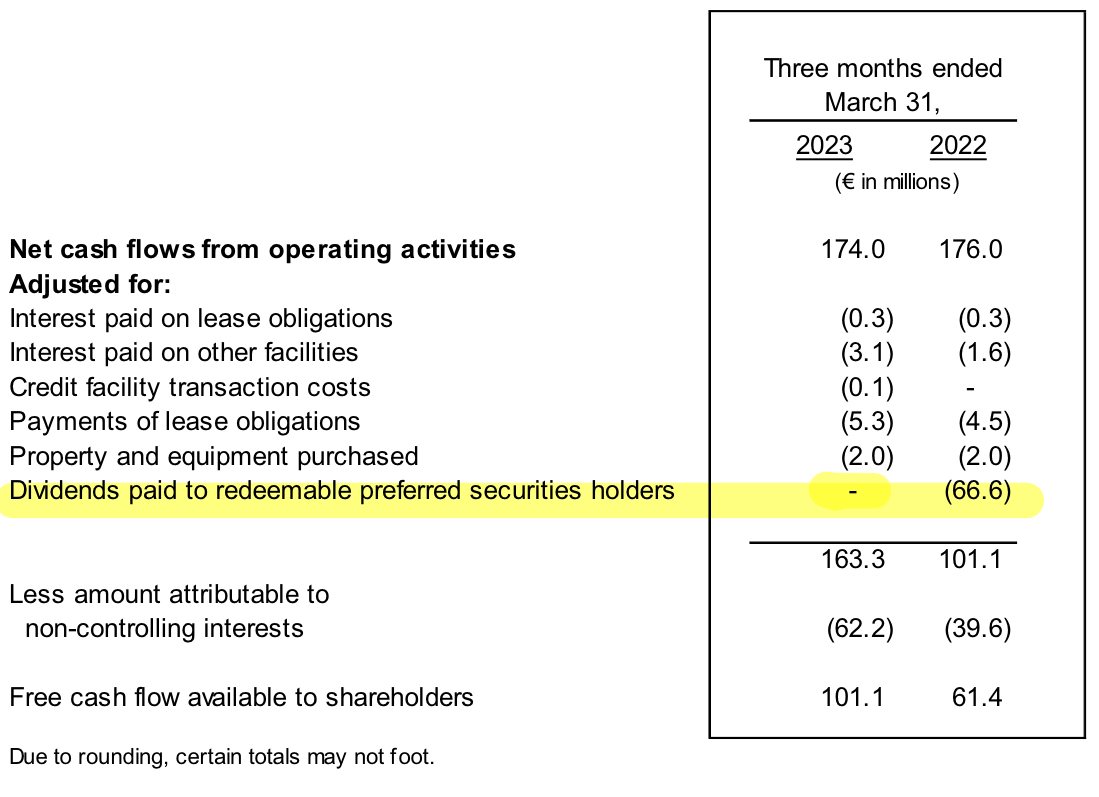

The picture in FCFA2S ("Free Cash Flow Available to Shareholders") was the complete opposite. Despite the weakness in Operating Cash Flow, FCFA2S grew 65% year-over-year , aided by the absence of the preferred dividend:

Topicus' Q1 Management's discussion and analysis

{kind=link}

The last dividend payment was made in Q1 last year, so this is where the surge comes from. It shouldn't impact the numbers in subsequent quarters.

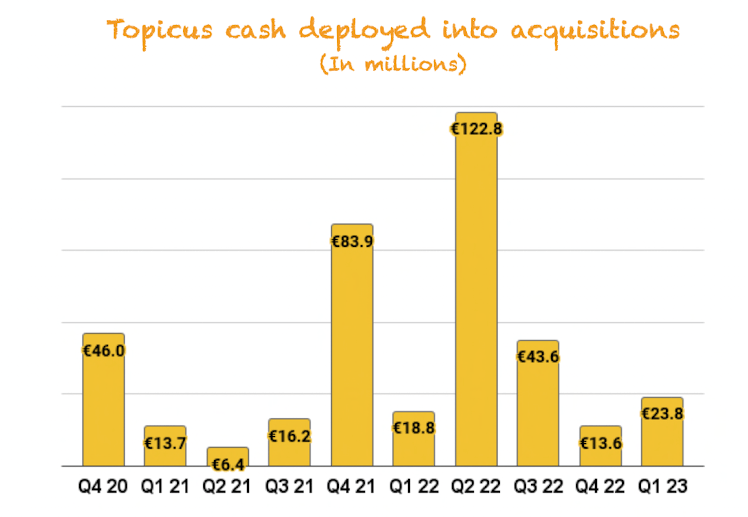

Acquisitions - An improvement from last quarter

Topicus deployed €23.8 million into acquisitions this quarter, a slight improvement when compared to last quarter:

Made by Best Anchor Stocks (I took out from Q1 2021 the purchase of Topicus from Ijsell)

{kind=link}

The timing of acquisitions is not predictable, and there's quite a bit of volatility here, so we shouldn't really read much into quarterly numbers. What matters is the long-term trend, and there are ample opportunities for the company to deploy capital.

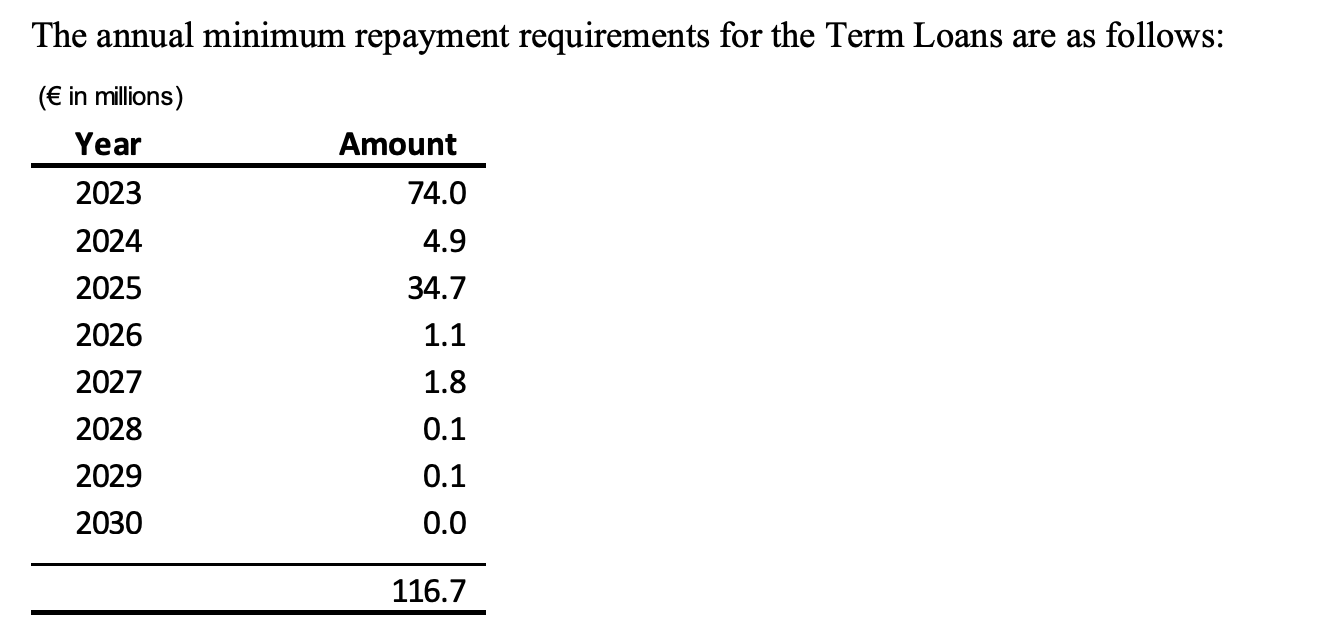

Topicus still has substantial dry powder to conduct more acquisitions this year. Cash increased to almost €200 million. The company faced significant debt repayments in 2023:

Topicus' Q4 Management discussion and analysis

{kind=link}

Topicus has repaid most of its 2023 debt, and the debt burden has gone down considerably:

Topicus Q1 MD&A

So, how can the company improve its cash position while repaying debt simultaneously? The answer lies in the seasonality of cash flows. Most of the company's cash comes in in Q1, so its figures should moderate as the year goes by.

Considering the company still has the Constellation loan of €30 million to repay this year, we could argue that there's around €200 million in dry powder to conduct acquisitions . This results from €197 million in cash, subtracting the debt payment to Constellation, and adding around €30 million of cash flows for the remaining quarters, consistent with last year. Of course, this is only a guess, as the reality might be very different, but it's consistent with what we expected last quarter.

Conclusion

All in all, it was a good quarter for Topicus.com Inc. Top-line growth was a highlight, especially organic growth, which continued last quarter's positive trend. The only lowlight was Operating Cash Flow conversion, which was impacted by increased receivables. Receivables are aging, which was also recorded through an increase of debt bad expense, so we should monitor this closely going forward. But for the rest, this was a great quarter for Topicus.com Inc.

In the meantime, keep growing!

For further details see:

Topicus: Good Organic Growth, More Acquisitions, Deep Dive Into Q1 Earnings