CA - Torex Gold: Exceptional Q1 Results But A Softer Q2/Q3 Ahead

2023-06-02 17:00:56 ET

Summary

- Torex Gold reported a 10% increase in revenue for Q1, benefiting from record underground tonnes mined and record mill throughput.

- Its strong performance led to better-than-expected cost performance, with minimal AISC margin compression vs. Q1 2022, an outperformance relative to its peers.

- Despite a solid Q1, Q2/Q3 will be softer due to waste stripping/cessation of mining at the Guajes Pit, making it harder to justify paying up here for the stock.

It was a mixed Q1 Earnings Season for the Gold Miners Index ( GDX ), with several companies reporting flat sales year-over-year and most reporting weaker all-in sustaining cost margins. However, Torex Gold ( TORXF ) was unique with a blowout Q1 operationally, benefiting from record underground tonnes mined and record mill throughput, helping it to report a 10% increase in revenue and minimal margin compression (42% margins vs. 44%). Notably, this was despite inflationary pressures and a persistent strengthening in the Peso relative to the US Dollar ( UUP ), which was unfortunately continued into Q2, with ~50% of Torex's all-in sustaining cost in pesos. That said, we could see unit costs pressured in Q2 and Q3, with tough comps ahead sequentially. Let's take a look at the Q1 results and forward outlook below.

ELG Operations (Company Website)

{kind=link}

Q1 Production & Sales

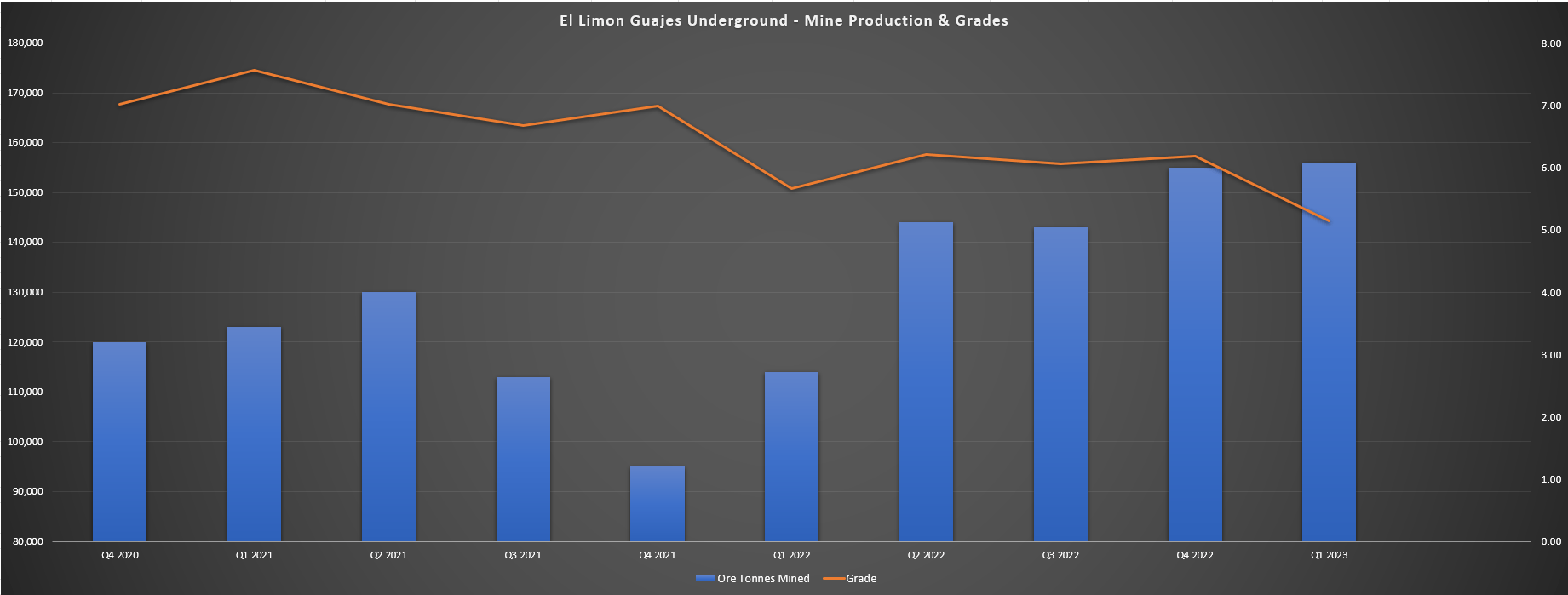

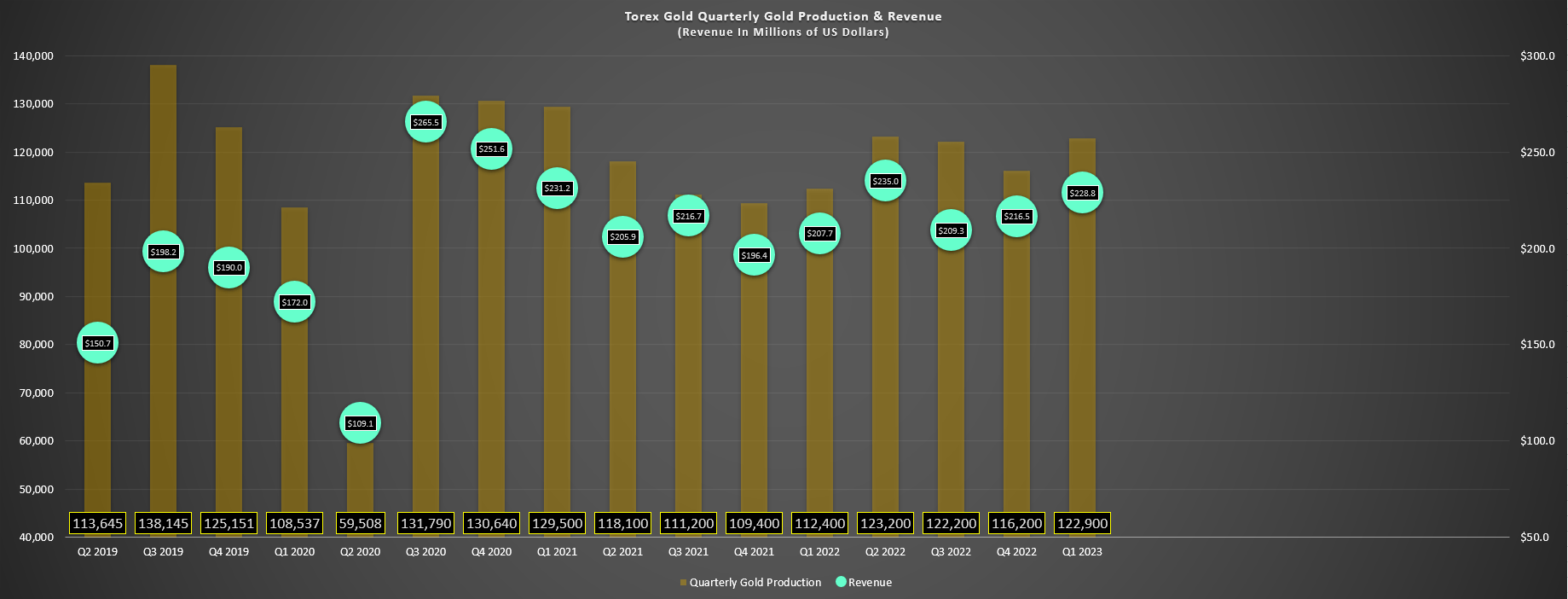

Torex Gold released its Q1 results last month, reporting quarterly production of ~122,900 ounces of gold, a 9% increase from the year-ago period. The exceptional performance was driven by record mill throughput and record underground mine production, with ~156,000 tonnes mined at El Limon Guajes ((ELG)) Underground at an average grade of 5.15 grams per tonne of gold, and just shy of ~13,100 tonnes processed at the ELG Plant. The company noted in its Q1 Conference Call that the record tonnes processed resulted from reduced unplanned downtime, sticking to budgeted times for planned shutdowns, and an increase in tonnes processed per hour, which was credited to good maintenance of the SAG mill and ball mill. So, despite the dip in grades mined underground, the higher open-pit grades, recoveries, and throughput helped to deliver a strong start to the year.

ELG Underground - Mine Production & Grades (Company Filings, Author's Chart)

{kind=link}

The encouraging news is that despite 38% growth in underground mine production year-over-year, ELG Underground continues to replace its increasing depletion. The evidence was Torex ending the year with ~2.56 million tonnes at 6.17 grams per tonne of gold in reserves at ELG Underground (508,000 ounces), up 2% from ~2.68 million tonnes at 5.81 grams per tonne of gold in the year-ago period (~500,000 ounces) despite a massive year for underground mine contribution. Plus, the growth in underground contribution isn't done here, with Torex confident that it can average mining rates of 2,000 tonnes per day next year, translating to ~120,000 ounces of annual contribution even at a grade slightly below the reserve grade (5.8 grams per tonne of gold). This continues to lift the average feed grade at ELG and will help to pad production in the softer quarter that's on deck (increased waste stripping).

Torex Gold - Quarterly Production & Revenue (Company Filings, Author's Chart)

{kind=link}

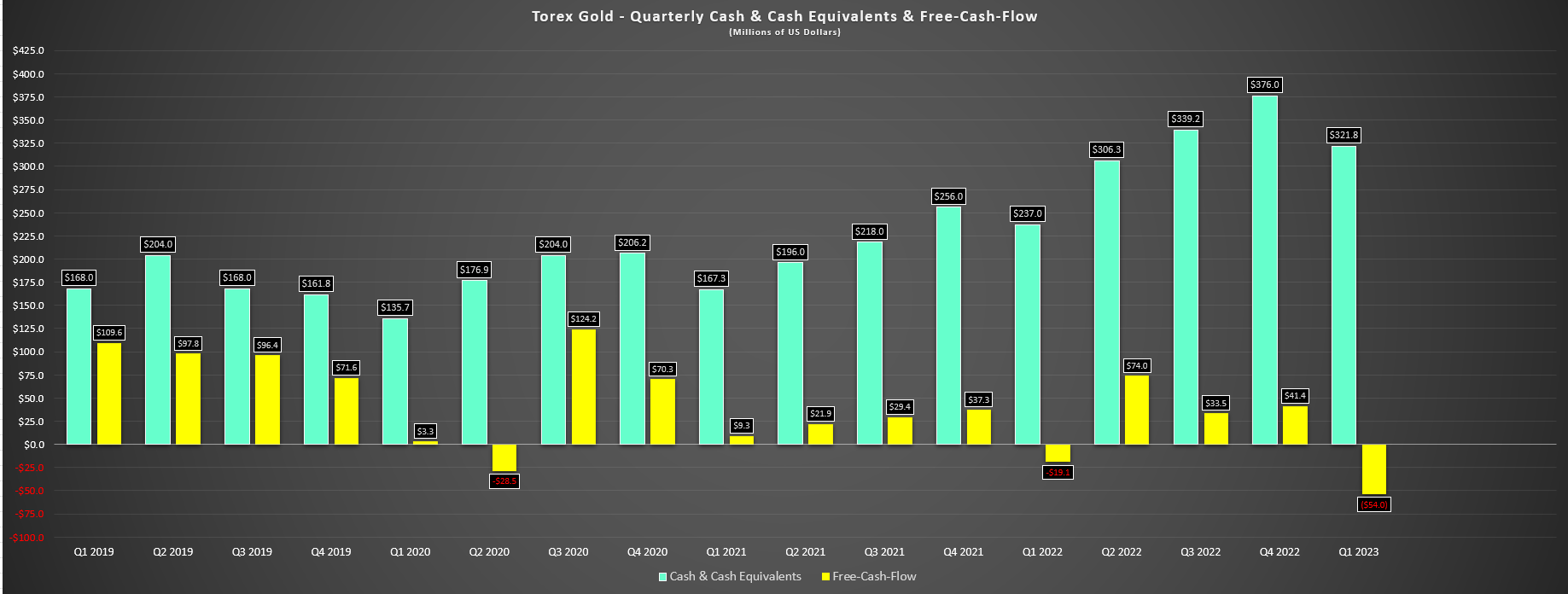

Given the strong production results that translated to higher gold sales in the period (~118,500 ounces sold at $1,899/oz), Torex saw a 10% increase in revenue to $228.8 million, despite minimal help from the gold price which was up just 1% year-over-year. Meanwhile, operating cash flow came in at $47.0 million in the period (Q1 2022: $46.7 million), with Torex being one of only a handful of miners to hold the line on cash flow relative to Q1 2022 even with the impact of higher fuel prices, higher labor costs, and some consumables, such as cyanide. Also encouraging was that Torex has passed the 4.0-kilometer mark on the Guajes Tunnel and reaffirmed breakthrough "in early Q1 2024 or before". In addition, advance rates have improved meaningfully, reaching 7.0 meters a day, up from 6.5 meters per day on trailing-twelve-month cash flow.

Torex - Quarterly Cash Position & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Finally, even with a cash outflow of $54.0 million in the period related to higher capital expenditures at Media Luna in what will be a busy year for construction and development (underground construction/development currently 24% complete as of quarter-end, with surface construction 15% complete), Torex exited Q1 with one of the strongest balance sheets sector-wide, with ~$318 million in net cash and $250 million on its undrawn revolving credit facility. This has placed Torex in a very comfortable position to complete Media Luna construction without the need for an equity raise or selling off assets like we've seen from other producers such as Argonaut ( ARNGF ) and Iamgold ( IAG ), with ~$683 million in spending remaining, and ~$564 million in liquidity, with the gap easily made up by $280+ million in annual operating cash flow even at very conservative gold prices ($1,800/oz).

Torex is further protected during this period against gold price weakness due to forward sales, with ~255,000 ounces sold forward from April 2023 to December 2024 at an average price of $1,952/oz.

Costs & Margins

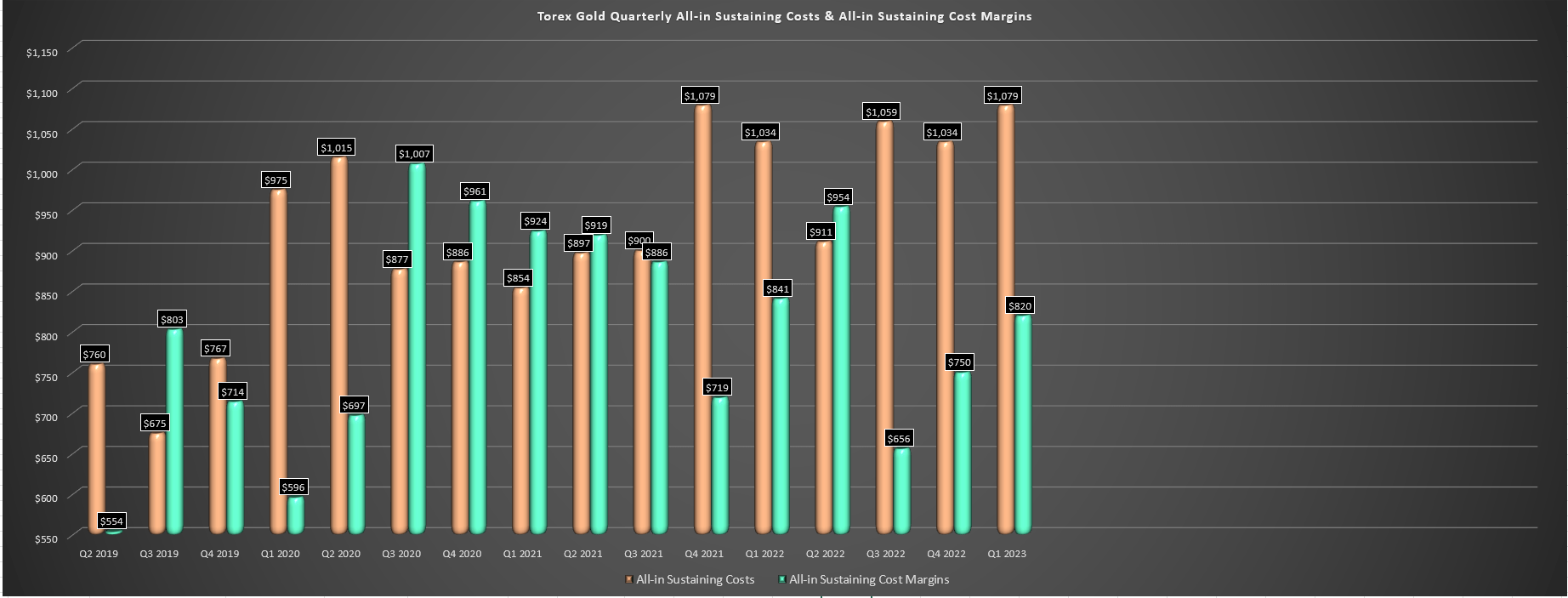

Moving over to costs and margins, Torex reported all-in sustaining costs ((AISC)) of $1,079/oz in Q1, coming in just below its FY2023 guidance range of $1,080/oz to $1,130/oz. This represented a 4% increase from the year-ago period, but AISC margins barely budged, coming in at $820/oz vs. $841/oz. Plus, AISC margins remained well above the FY2022 industry average of ~$510/oz, and the increase in costs was not company-specific given the inflationary pressures felt sector-wide and was despite a significant increase in sustaining capital (+65% year-over-year), and the strengthening in the Mexican Peso which affected unit costs. So, given these unusual headwinds relative to most other producers, the company's cost controls were impressive, with per tonne underground mining costs actually down ($80.42/tonne vs. $86.14/tonne), benefiting from economies of scale.

Torex - AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

However, while the Q1 results were solid and Torex outperformed its peers from a margin standpoint, we will see some mean reversion in Q2 and Q3 with a focus on waste stripping and continued strength in the MXN/USD exchange rate. This could lead to two consecutive quarters with costs closer to $1,200/oz, and the company will see less of a benefit from the higher gold price than most peers because of being partially hedged during Media Luna construction. So, while several producers should see meaningful margin expansion from Q1 to Q2, Torex could see margin compression, making it harder to justify paying up for the name as we head into a softer Q2 report in late July/early August. Let's dig into the valuation and see whether the tough comparisons on a sequential basis are priced into the stock already.

Valuation & Technical Picture

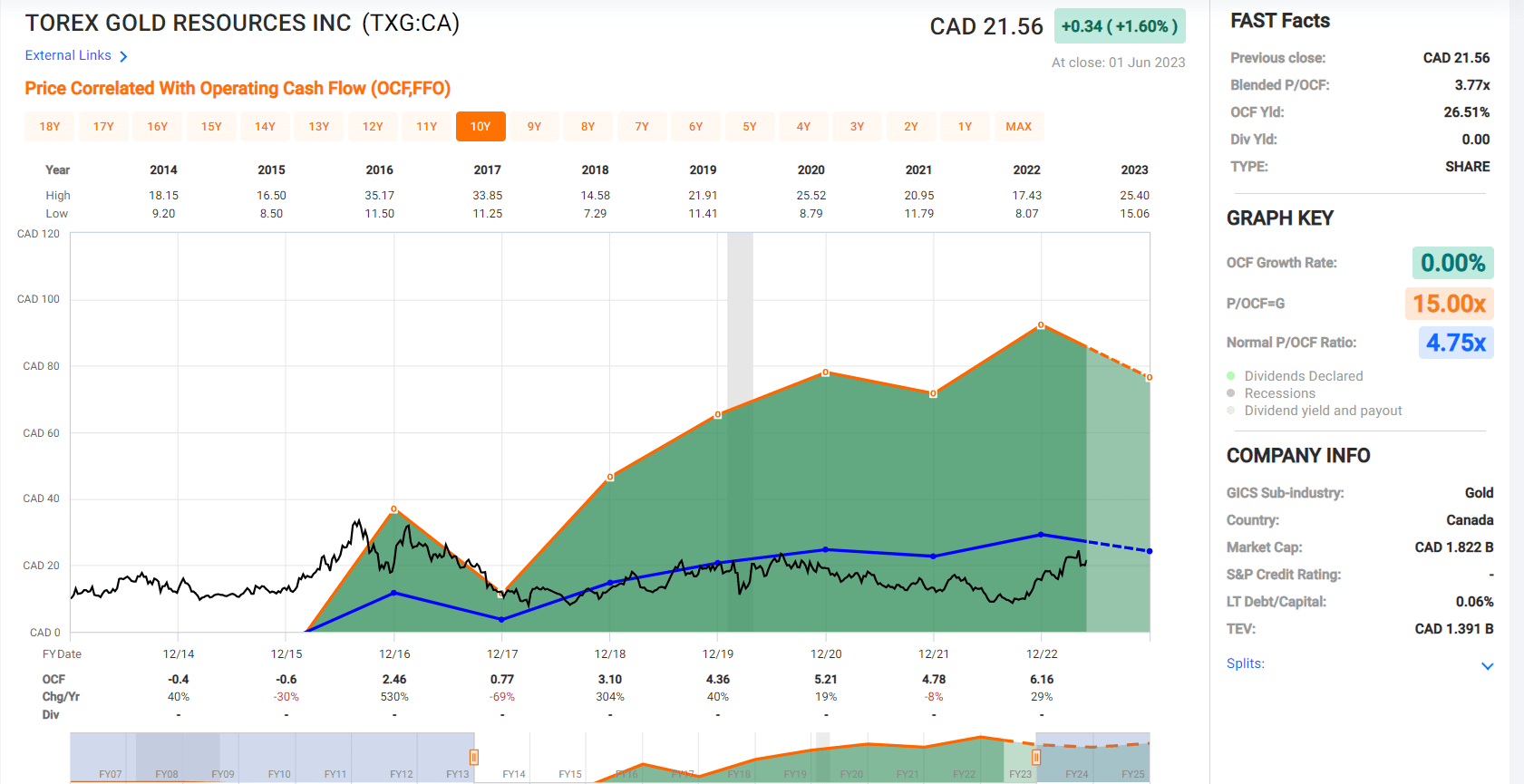

Based on ~87 million fully diluted shares and a share price of US$16.20, Torex trades at a market cap of $1.41 billion, a more reasonable valuation relative to its recent peak market cap of ~$1.65 billion reached earlier this year. However, from a P/NAV standpoint and using a more conservative multiple of 0.90x P/NAV given its position as a single-asset miner in a less favorable jurisdiction (Guerrero State, Mexico), I continue to see the stock as nearly fully valued with an estimated fair value of ~$1.45 billion (US$16.65). And even if we use a 70%/30% weighting to derive fair value using P/NAV and cash flow per share using a multiple of 5.0x cash flow, this translates to a fair value of US$17.90, pointing to just a 10% upside from current levels.

Torex - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

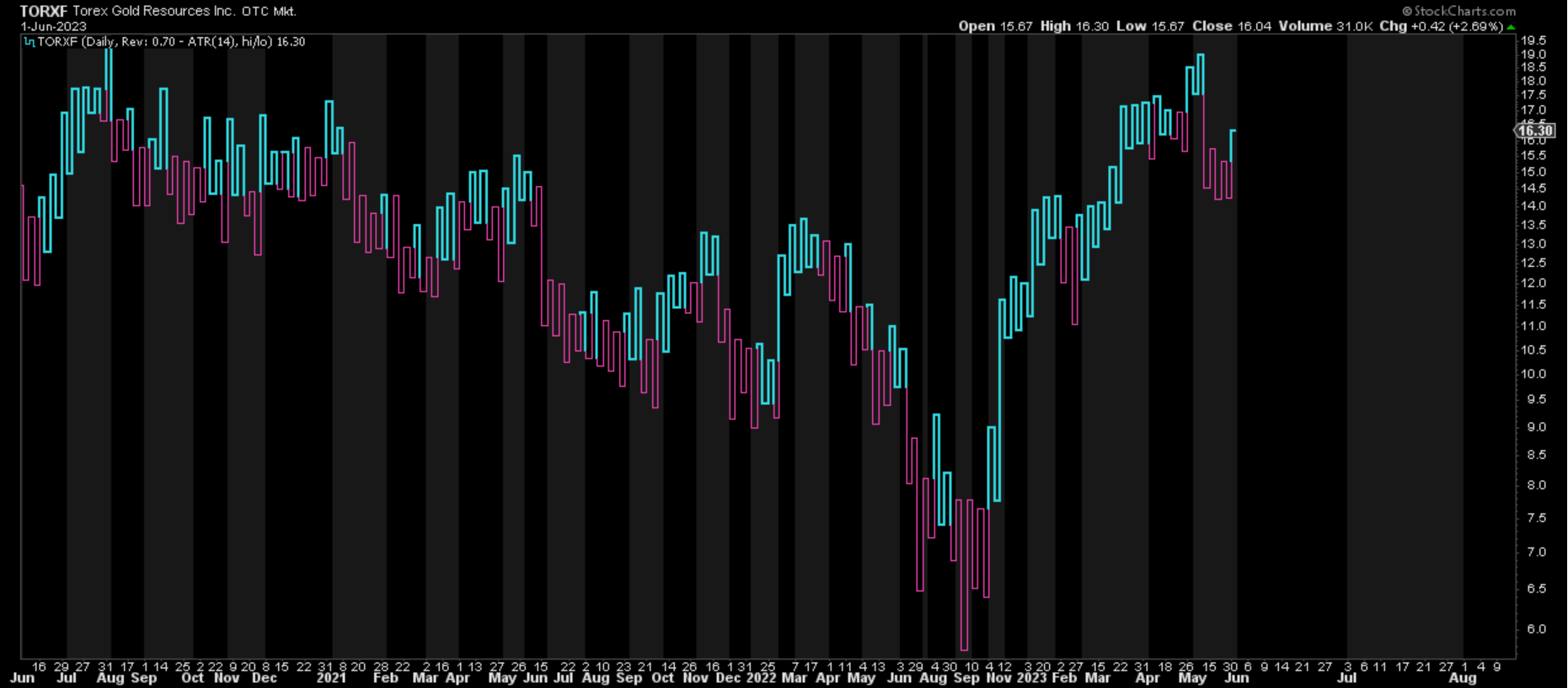

While some investors might be comfortable with a 10% upside to fair value, I prefer to wait for a significant discount to fair value to justify entering new positions, and especially for single-asset producers in less attractive jurisdictions. And based on a minimum 40% discount to fair value from an estimated fair value of US$17.80 (70%/30% P/NAV and cash flow per share weighting), the ideal buy zone for Torex would come in at US$10.70 or lower to bake in an adequate margin of safety. Obviously, there's no guarantee that the stock drops to this level, but I prefer to buy at the right price or pass entirely. Hence, I don't see any way to justify paying up for the stock here, and I would view any rallies above US$17.75 before August as an opportunity to book more profits, with the potential for the stock to register a double top if it makes a second run at its May highs.

TORXF 3-Year Chart (StockCharts.com)

{kind=link}

Summary

Torex Gold put together a solid Q1 report and is tracking slightly ahead of its guidance mid-point, which should help it deliver into cost guidance despite the strength in the Mexican Peso and sticky inflationary pressures. However, Q2 and Q3 are likely to be softer with a focus on waste stripping and the cessation of mining at the Guajes Pit, setting up two quarters of ~$1,200/oz plus AISC if we don't see some mean reversion in the MXN/USD exchange rate. So, with tougher comps sequentially and Torex massively outperforming its peer group, I think there are far better ways to allocate one's capital in the sector currently, with a few names offering larger discounts to fair value. To summarize, I would need lower prices to get interested in Torex, and I would view any rallies above US$17.75 before August as an opportunity to book more profits.

For further details see:

Torex Gold: Exceptional Q1 Results, But A Softer Q2/Q3 Ahead