CA - Torex Gold: Mexican Peso Strength Weighs On Margins

2023-08-15 14:00:50 ET

Summary

- Torex Gold's Q2 production declined by 13% due to lower grades and reliance on lower-grade stockpiles.

- Meanwhile, costs soared by over 40% year-over-year, impacted by tough comparisons, a rising Mexican Peso, and increased capitalized stripping.

- In this update, we'll look at how Media Luna is progressing and whether the stock is getting closer to a low-risk buy zone.

Just over three months ago, I wrote on Torex Gold ( TORXF ), noting that while the company put together a solid Q1 report, there was no way to justify chasing the stock and that the sharp rise to US$17.00 was providing an opportunity to book more profits. This is because the stock no longer offered a margin of safety at a market cap of ~$1.50 billion, and it was coming up against a tough quarter from a comparison standpoint in Q2, having to lap ~123,200 ounces at $911/oz all-in sustaining costs from the year-ago period. Worse, it would need to lap these results with elevated sustaining capital due to increased capitalized stripping and a runaway Mexican Peso vs. the US Dollar ( UUP ), suggesting that Torex's headline results would look much softer in the upcoming quarter.

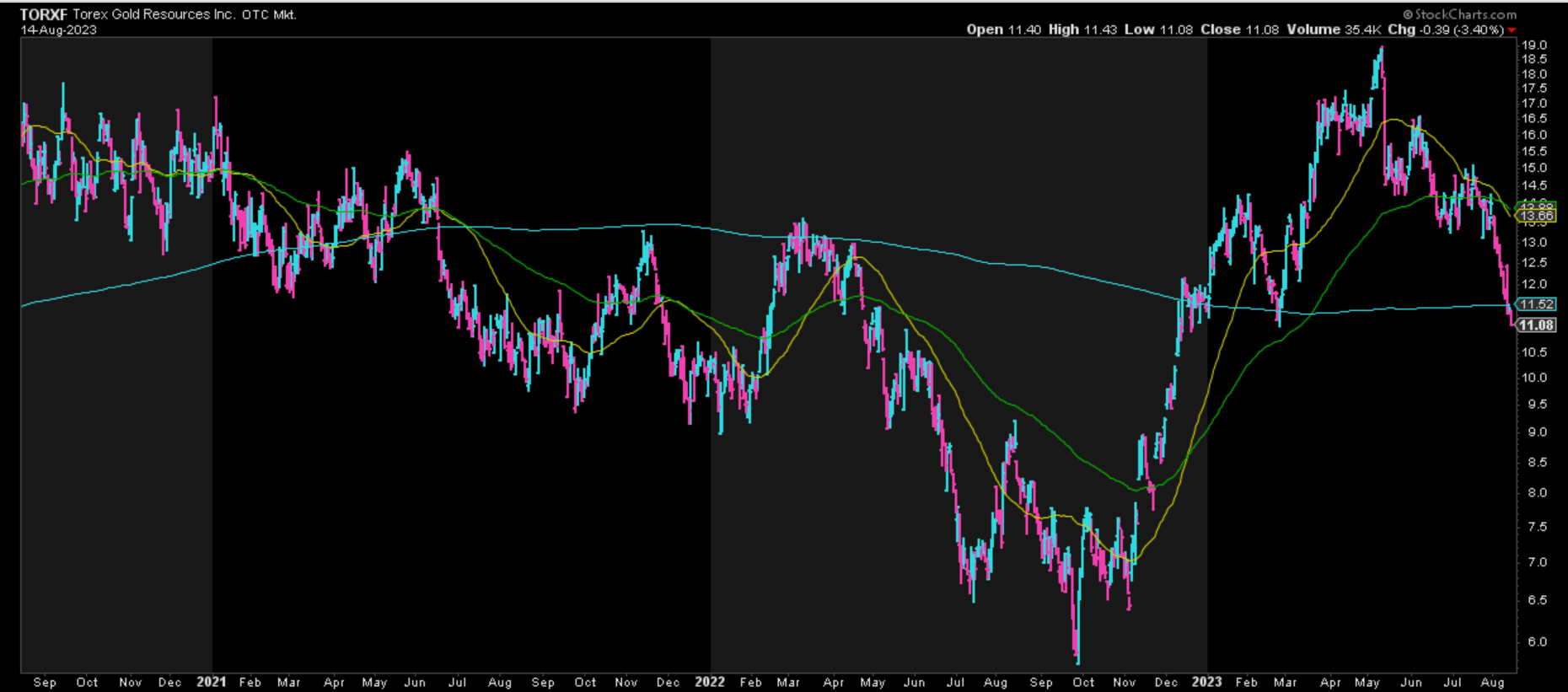

Since then, Torex has been one of the worst-performing miners, down ~36% in just over three months, and massively underperforming the Gold Miners Index ( GDX ). And while this violent sell-off has contributed to the stock trading at a more attractive valuation, there are open gaps in its chart below, and the Q3 results aren't likely to be much better with another quarter of elevated stripping and an even stronger Mexican Peso. Meanwhile, although liquidity is more than sufficient to complete Media Luna construction, significant free cash outflows will persist in the short term, which could make sector peers that are buying back shares and paying dividends more attractive alternatives given that they pay investors to wait for a sector turnaround. Let's look at the Q2 results below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

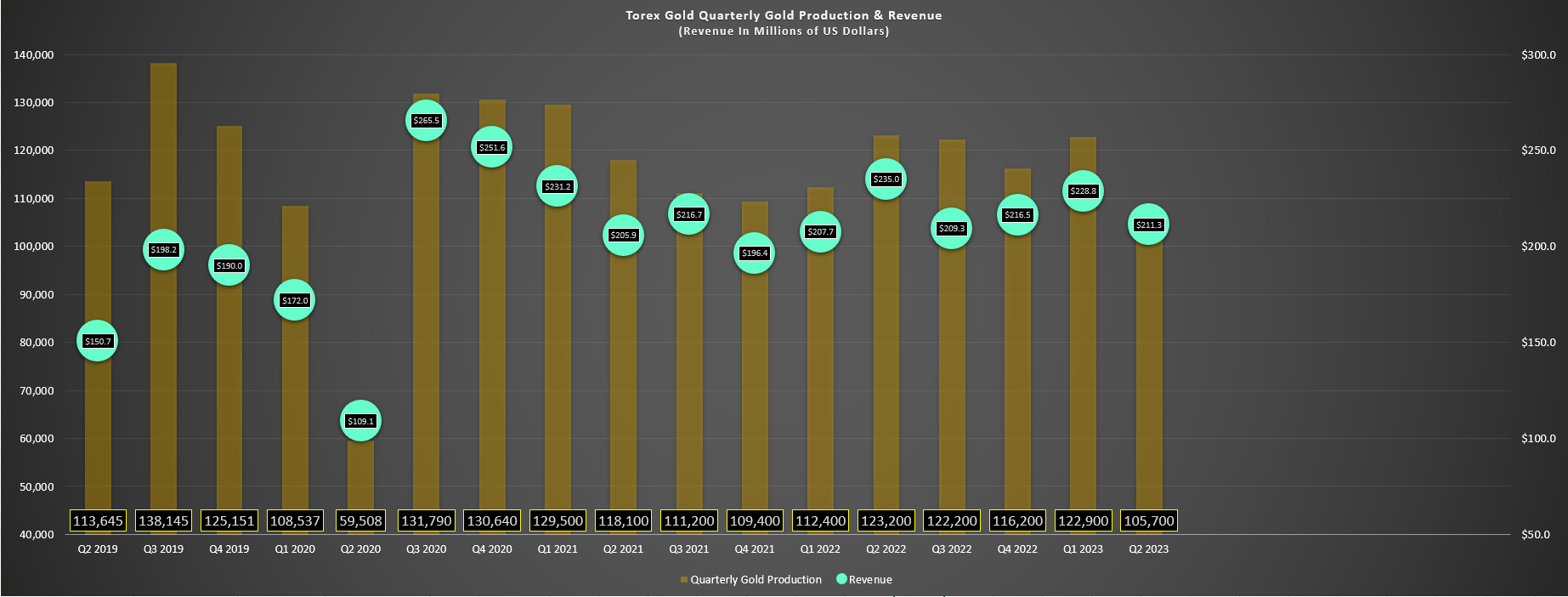

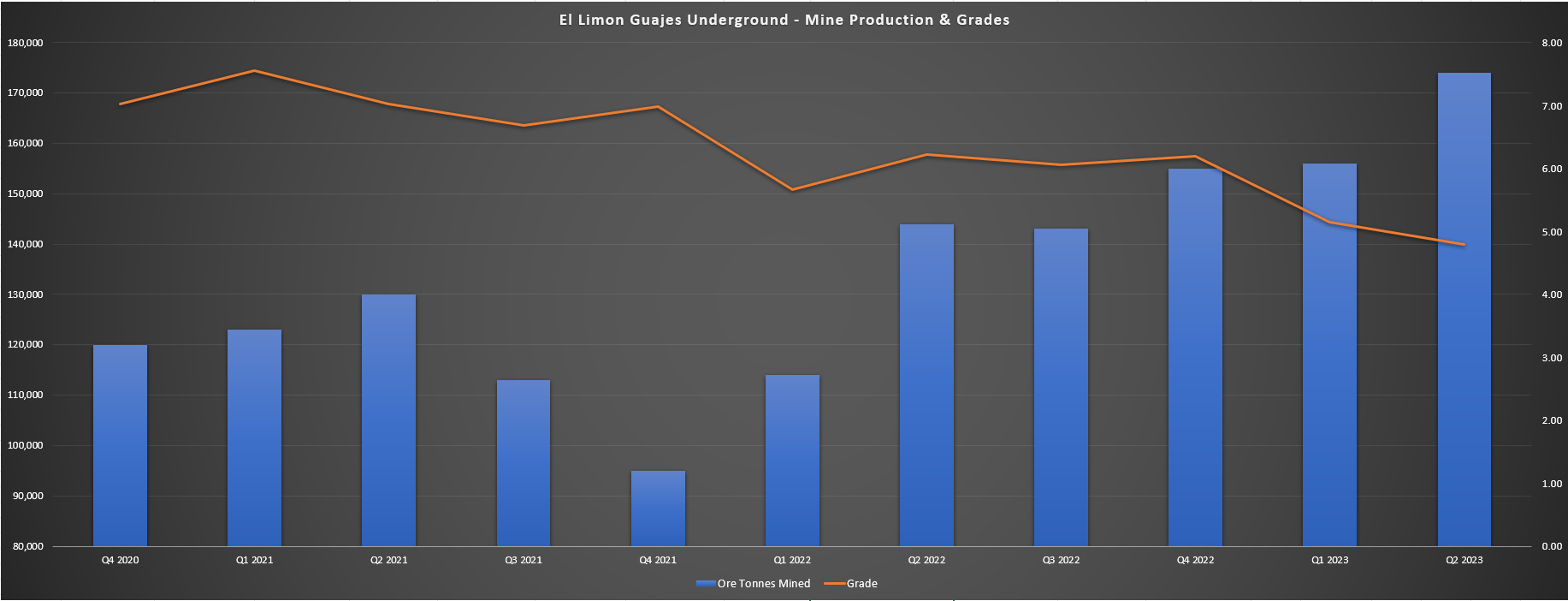

Torex Gold released its Q2 results earlier this month, reporting quarterly production of ~107,500 ounces of gold, a 13% decline from the year-ago period. The lower output at the El Limon Guajes ((ELG)) Mine can be attributed to significantly lower grades in the period with the cessation of mining at the Guajes Pit resulting in a reliance on lower-grade stockpiles to feed the mill. Meanwhile, although underground mining rates came in above my expectations at 1,913 tonnes per day, this was offset by lower grades mined, with the company lapping tough comps from Q2 2022 when it enjoyed grades of 6.22 grams per tonne from ELG UG, above its average reserve grade at the time of 5.74 grams per tonne of gold. The result of the lower production and fewer ounces sold than produced (~105,700 vs. ~107,500) was that revenue fell sharply year-over-year to $211.3 million despite the benefit of a higher average realized gold price.

Torex Gold - Quarterly Production & Sales (Company Filings, Author's Chart)

{kind=link}

While the headline production numbers may appear disappointing, it's important to note that Torex is tracking well in line with its FY2023 production goal of 440,000 to 470,000 ounces (~230,400 ounces produced year-to-date), and the progress on underground mining rates is commendable, with the company well on track to beat its 1,800 tonne per day goal for its 2023 exit rate. This is very positive news given that the Technical Report assumed mining rates of ~1,400 tonnes per day with the rest of the feed coming from Media Luna ore and stockpiles. However, if the company could displace 500+ tonnes per day of ore and extend the mine life at ELG UG, this would certainly have a positive impact on economics and its NAV at its Morelos Complex. And just as importantly, the bonanza grade hits and likely resource growth discussed in my last update could extend ELG UG's mine life past 2030 vs. an envisioned cessation of mining here in late 2027.

ELG UG - Mine Production & Grades (Company Filings, Author's Chart)

{kind=link}

Meanwhile, at the mill, Torex continues to fire on all cylinders here as well. And while this may not have shown up in the headline results, Torex reported a record mill throughput of ~13,300 tonnes per day, above the design of 13,000 tonnes per day based on 92% mill availability. So, Torex enjoyed bonus production in this period where it relied more on stockpiles as it works to transition to Media Luna (commercial production expected in 2025), and it's certainly encouraging to see the plant and underground beating design levels. That said, even with the higher underground mining rates and outperformance at the mill, I would not expect to see much of a step-up in production in H2, with higher waste stripping and a continued reliance on stockpiles.

Costs & Margins

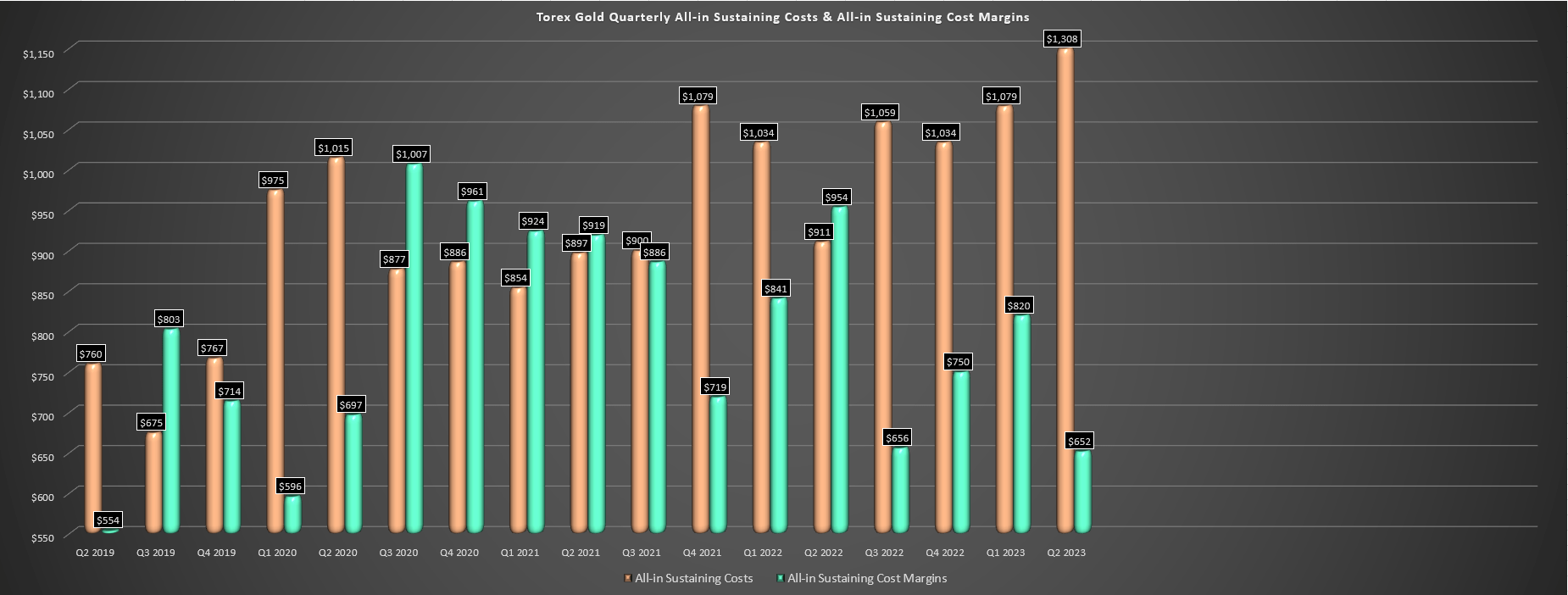

Moving over to costs and margins, Torex reported cash costs of $848/oz in Q2 2023 and all-in sustaining costs of $1,308/oz, a massive increase from $703/oz and $911/oz in the year-ago period. This sharp increase in costs in Q2 2023 was attributed to several items, one of which was the ~$45/oz impact year-to-date from the stronger Mexican Peso, which made a new multi-year high vs. the US Dollar. Second, sustaining capital increased materially in the period to $41.4 million (Q2 2022: $19.5 million) because of increased capitalized stripping. Finally, Torex sold ~2% fewer ounces than it produced in the period, putting a further dent in all-in sustaining costs. These items had a very negative effect on Torex's AISC margins, which plunged from $954/oz in Q2 2022 to $652/oz in the most recent quarter. And with the Mexican Peso strength, it's hard to rule out some minor cost creep vs. the Media Luna estimated build costs.

Torex Gold - AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Given that the strength in the Mexican Peso has not subsided as of Q3, and we will see elevated waste stripping in the current quarter, Torex likely has another high-cost quarter on deck, and this time it may not get as much help as it did during Q2 from the gold price unless it cooperates soon. Unfortunately, this prompted Torex to state that it is tracking to the higher end of its cost guidance for FY2023 of $1,080/oz to $1,130/oz, and it looks like Torex may miss the range slightly on costs if the Mexican Peso can't cool off soon and return above the 18.0 to 1.0 level (USD/MXN). That said, these costs are not reflective of the sub $900/oz costs expected (even adjusting for inflationary pressures) over the life of mine at Media Luna, and while compressed short-term, Torex's margins remain solid and slightly above the industry average even in a high-cost quarter.

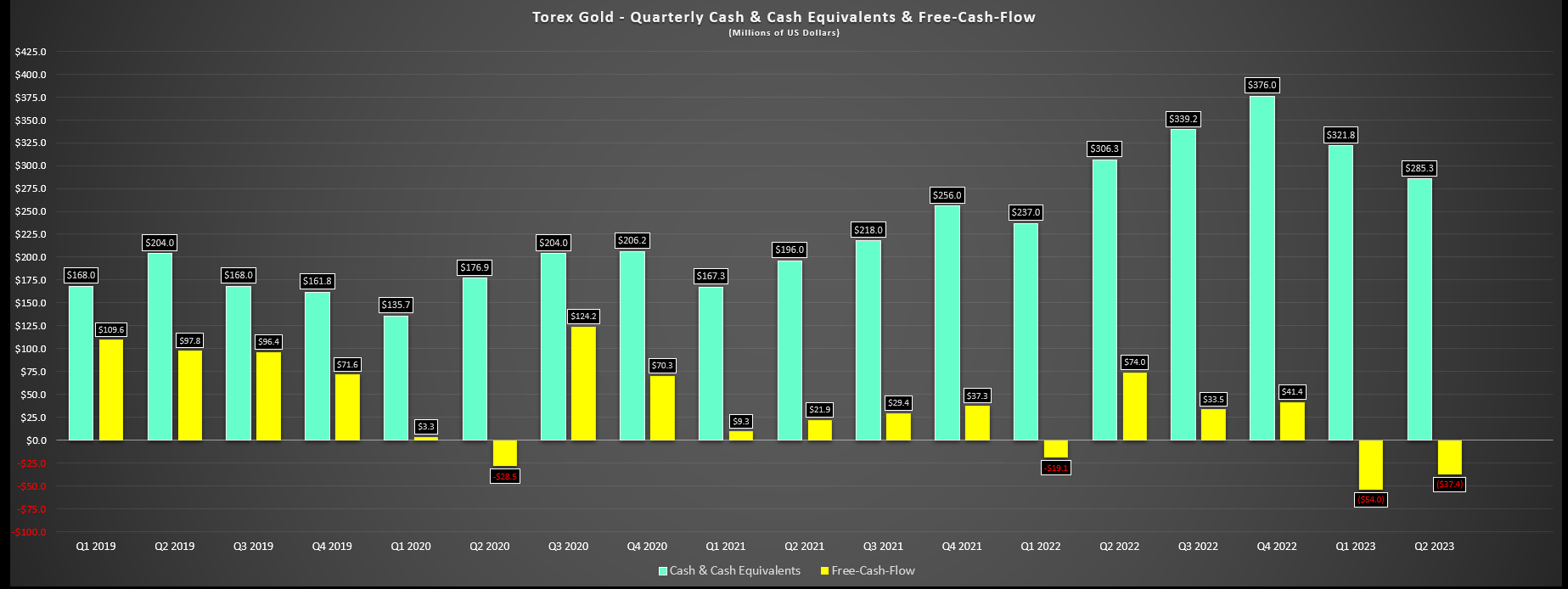

Torex - Cash & Cash Equivalents & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Given the high-cost quarter, operating cash flow sunk to $92.8 million (Q2 2022: $120.8 million), and we saw a free cash outflow of $37.4 million, with higher lease payments and interest combined with elevated capital expenditures related to its growth project and capitalized stripping ($124.5 million in Q2 2023 vs. $52.5 million in Q2 2022). However, despite the cash outflow, Torex ended the quarter with ~$275 million in net cash and over $520 million in total liquidity, giving it ample flexibility to fund the remaining ~$600 million left to completion when combined with operating cash flow from its operations over the next 18 months. Plus, the company noted that it is looking to increase its RCF from $250 million to $300 million, providing further liquidity if needed.

So, Was There Any Good News?

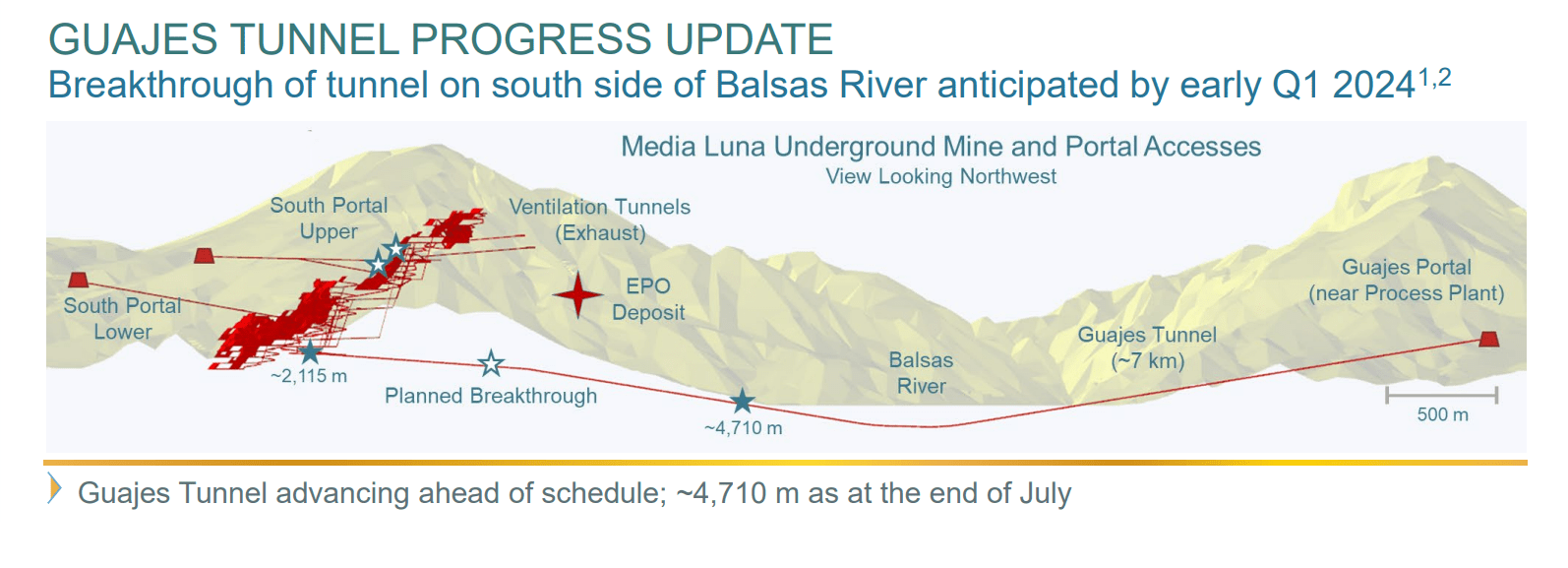

Aside from the impressive progress on improving underground mining rates, the Guajes Tunnel continues to move ahead in line with schedule, with the company on track for the breakthrough of the Guajes Tunnel in Q1 2024. This is because as of quarter-end, it had advanced over 4,700 meters of ~7.0 kilometers total, and Torex is enjoying improved advance rates of 6.9 meters year-to-date. Meanwhile, the South Portal Lower has advanced over 2.1 kilometers, and it completed the main spiral ramp following quarter-end. Finally, physical progress for Media Luna is 35% complete and remains on track for commercial production in H1 2025. So, with this being the key item for investors to ensure a smooth transition and to maintain the company's 400,000 ounce production profile, it's positive to see that the project remains on schedule and nearing 40% completion with just over 18 months to go to its planned commercial production.

{kind=link}

Summary

Torex's headline Q2 numbers certainly weren't pleasing with lower production at much higher costs, but this shouldn't have been surprising given the sharp rise in the Mexican Peso, the elevated waste stripping, and the tough comps that the company was lapping from Q2 2022. That said, the company continues to make solid progress behind the numbers, with Media Luna on schedule for commercial production in H1 2025, continued exploration success across its large land package, and impressive underground mining rates that are tracking ahead of the 1,800 tonne per day goal (exit rate for 2023). Meanwhile, from a valuation standpoint, the stock is quickly becoming one of the more attractively valued names sector-wide, trading at just ~0.65x P/NAV and less than 5x FY2025 free cash flow estimates, a dirt-cheap valuation for a mid-tier producer, even if operates out of a less favorable jurisdiction.

{kind=link}

That said, and as highlighted in my previous update, the stock has multiple open gaps in its chart, which makes it hard to rule out a lower low below the current price of US$11.10. So, while Torex could bounce short term after a violent 5-week sell-off, it would not surprise me to see the stock touch the US$10.20 area before year-end, pointing to further downside from current levels. Given that Torex is already one of the more undervalued producers sector-wide, I would expect further weakness to provide a buying opportunity, but the updated low-risk buy zone for the stock has shifted to US$9.70 after its recent support break. So, while I see the stock as becoming more attractive, I remain on the sidelines for now and focused on better reward/risk setups elsewhere.

For further details see:

Torex Gold: Mexican Peso Strength Weighs On Margins