CA - Torex Gold: Patience Required

2023-03-10 07:59:53 ET

Summary

- Torex Gold had an incredible year in 2022, generating ~$130 million in free cash flow despite elevated spend (Media Luna) and delivering within cost guidance and above output guidance.

- This was helped by solid cost controls, record underground tonnes mined and record mill throughput and despite considerable inflationary pressures that led to misses sector-wide.

- Unfortunately, while 2022 was a record year, 2023 and 2024 will be a little softer from an output/margin standpoint so the company will be lapping near insurmountable comps.

- While this isn't a huge deal if it were priced in, I don't see nearly enough margin of safety here and the stock remains a little extended, so I don't see any way to justify chasing the stock here at US$12.65.

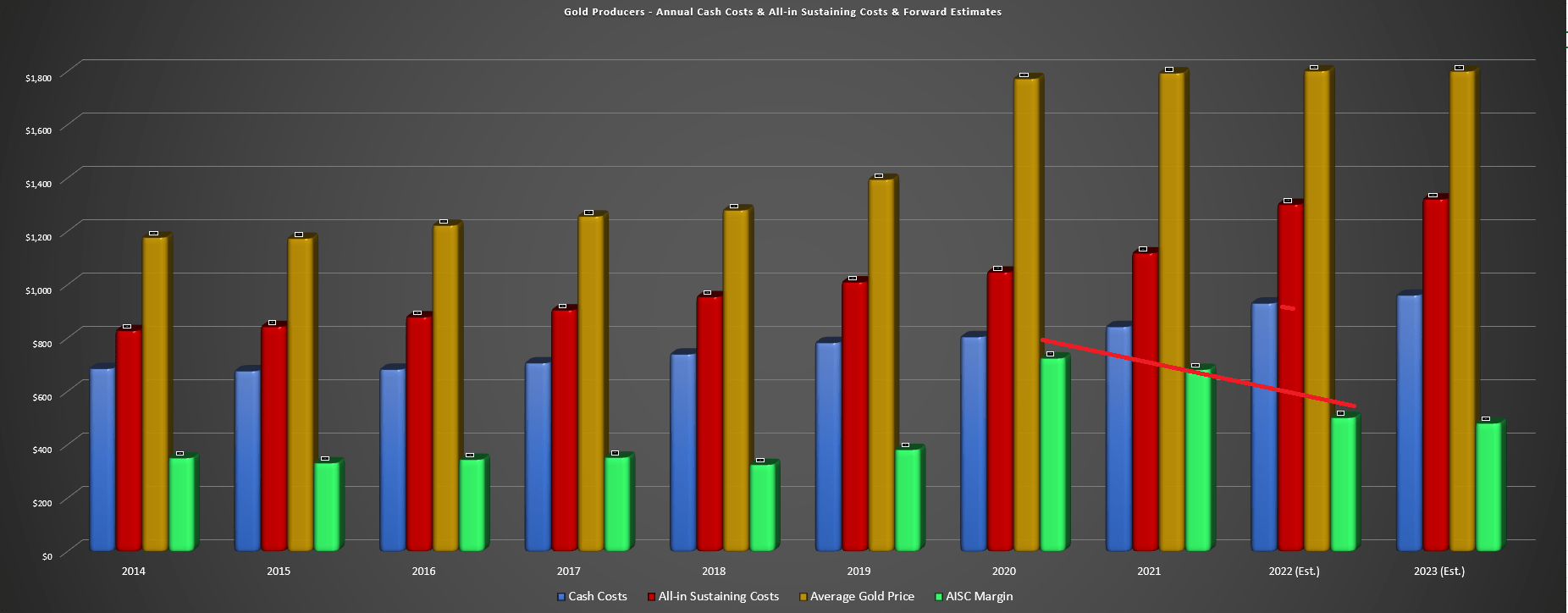

2022 was a tough year for the Gold Miners Index ( GDX ) and although several names rallied to finish the year, we've seen a sharp retracement since the highs at $33.00. The poor performance on a trailing two-year basis for gold producers isn't that surprising, given that most of the margin benefit from a $400/oz increase in the gold price ($1,800/oz vs. $1,400/oz) was eroded by inflationary pressures (fuel, electricity, labor, steel, cyanide, etc.) with minimal margin improvement and higher share counts for many companies because of share-based acquisitions and or large capital raises to fund new mine builds and cost overruns.

Gold Producer Universe - Cash Costs, AISC, Gold Price & AISC Margins (Company Filings, Author's Chart)

{kind=link}

While Torex Gold (TORXF) has been busy funding its own growth with plans to transition from mining at El-Limon Guajes (current mine) to Media Luna post-2024, it's done a much better job than its peers. This is evidenced by having one of the better balance sheets sector-wide, sitting on more than enough liquidity to fund Media Luna when including future cash flow, and tracking on time and on budget with the project set to be near 20% completion at the end of Q1 2022, and reporting record production at ~44% AISC margins in FY2022. However, after a ~100% rally over the past six months, much of this looks priced into the stock. Let's take a closer look:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q4 Results

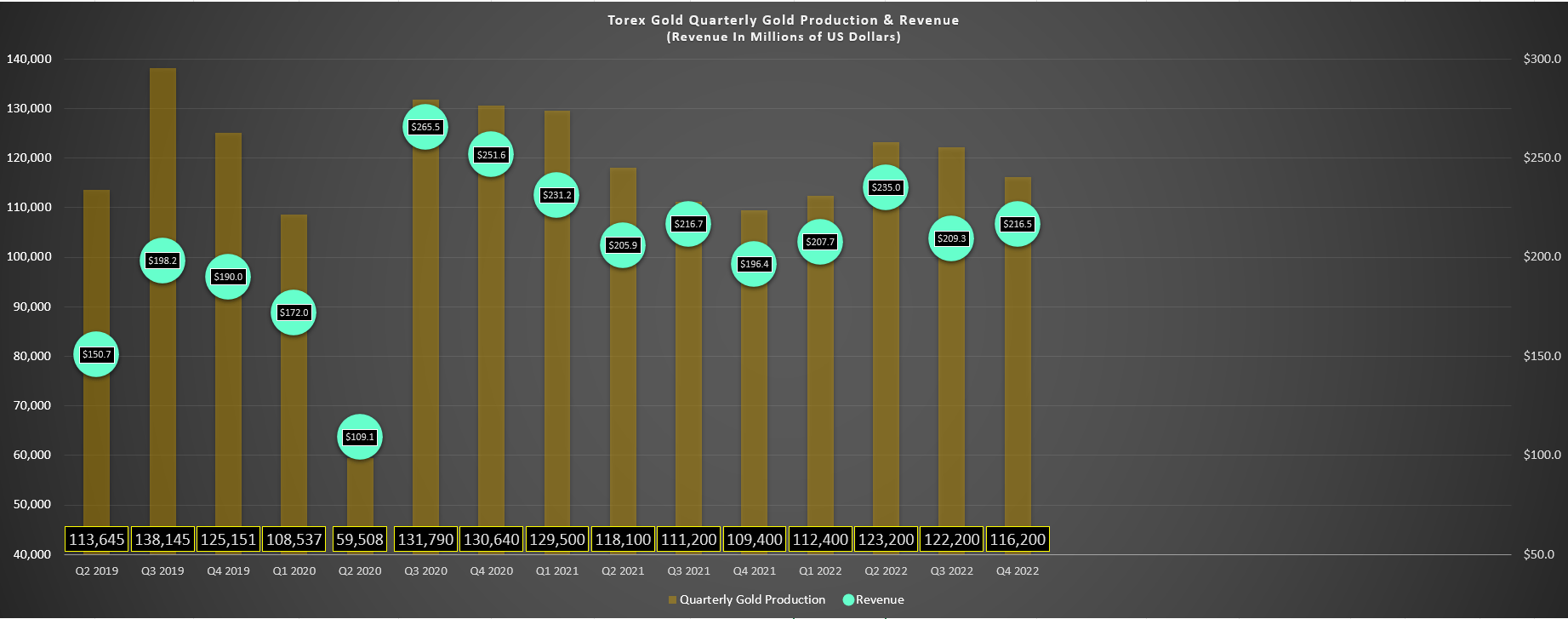

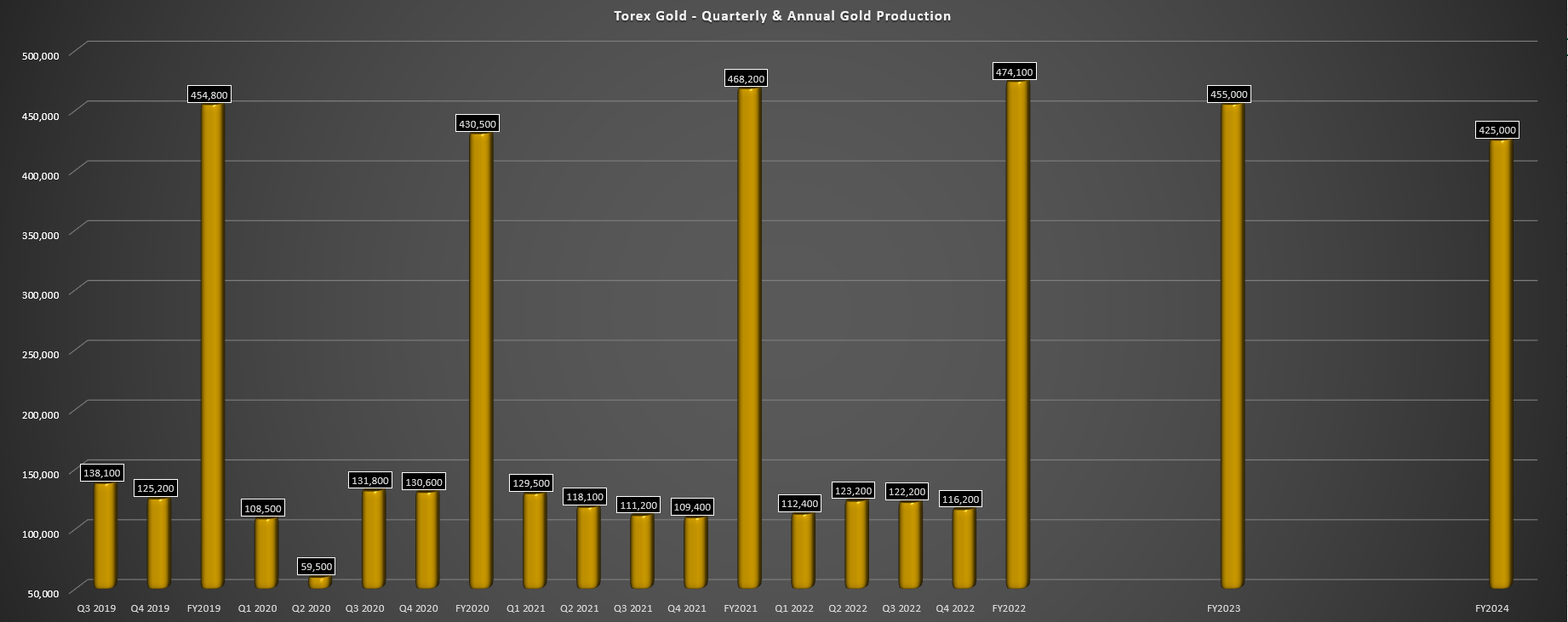

Torex Gold released its Q4 and FY2022 results last month, reporting annual production of ~474,000 ounces, a record for the company and a massive beat vs. its guidance mid-point of 450,000 ounces. The strong performance at El-Limon Guajes was driven by record mill throughput (~12,600 tonnes per day) and record underground mining rates, with mining rates coming in at even better levels in Q4 at (1,685 vs. 1,523 TPD). This was a significant improvement vs. Q4 2021, with underground ore tonnes mined up 20% year-over-year more than offsetting the decline in average grades. Meanwhile, throughput was also higher at ~4.6 million tonnes for the year despite unplanned shutdowns in the SAG and ball mills in Q4 that resulted in slightly lower quarterly throughput on a year-over-year and sequential basis.

Torex - Quarterly Output & Revenue (Company Filings, Author's Chart)

{kind=link}

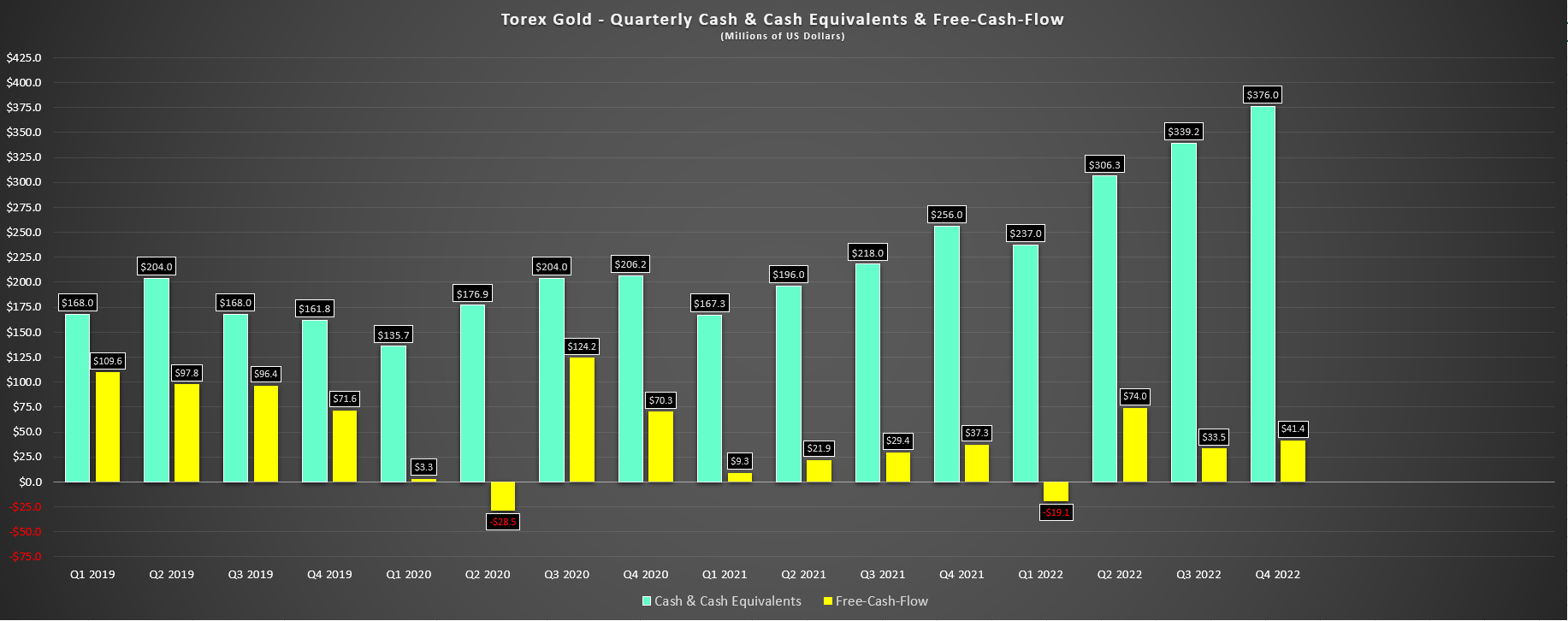

Fortunately, the lower throughput in Q4 was more than offset by grades, with a much higher contribution from underground (~155,000 tonnes vs. ~95,000 tonnes) lifting overall head grades to 3.78 grams per tonne of gold (Q4 2021: 3.35 grams per tonne of gold). The result was a 7% increase in revenue due to higher sales volumes in the period and despite a 1% lower average realized gold price year-over-year which was a minor headwind ($1,784/oz vs. $1,798/oz). On a full-year basis, revenue came in at ~$870 million and Torex Gold generated ~$130 million in free cash flow, an incredible performance for a one-mine company and especially one in a relatively high capex period as it funded the start of construction and early works at Media Luna.

Torex Gold - Quarterly Cash & Cash Equivalents & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Given the record production and despite a relatively flat average realized gold price with a volatile year for the precious metal, Torex ended the year with ~$377 million in cash, an undrawn $250 million credit facility, translating to total liquidity of ~$620 million. This liquidity position covers more than 80% of remaining Media Luna Capex (~$750 million) even before operating cash flow that the company will generate this year. Just as importantly, Torex was proactive and hedged ~25% of gold production over the rest of the Media Luna build, a move that I think was very smart and par for the course from a team that continues to execute near flawlessly.

With ~27,000 ounces hedges per quarter at $1,924/oz, some miners might have a tough Q2 and rest of the year if the gold price can't hold $1,800/oz, but Torex is in great shape.

Costs & Margins

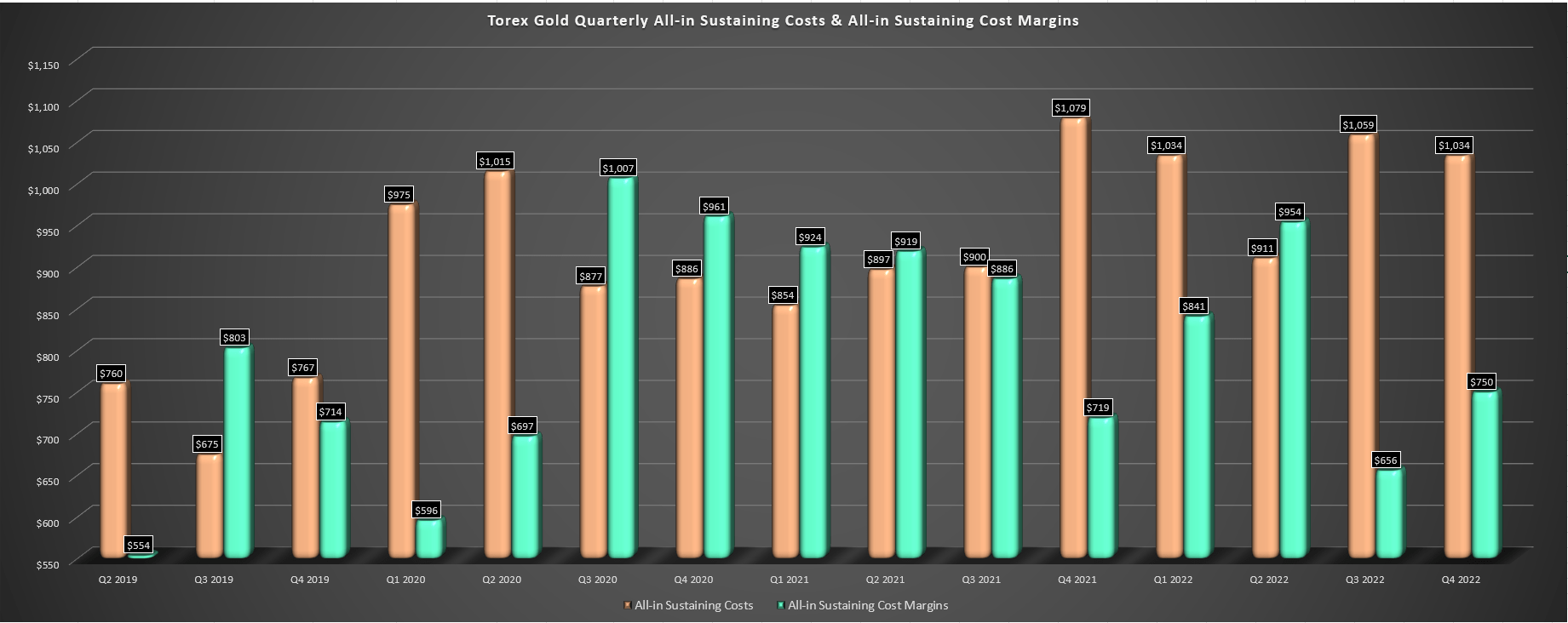

Moving over to costs and margins, Torex put up glowing results here as well, reporting Q4 all-in-sustaining costs [AISC] of $1,034/oz and AISC margins of $750/oz. These AISC margins were actually up year-over-year and dwarfed sector average AISC margins in Q4 of ~$450/oz despite inflationary pressures with items called out by Torex including steel, labor, diesel, explosives, and cyanide. Fortunately, Torex did see some offset due to reduced cyanide consumption related to blending, and benefited from higher sales volumes given the impressive Q4 performance with record underground mining rates that helped to increase output in the period.

Torex - Quarterly AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Looking at the annual results, Torex delivered into its cost guidance of $980/oz to $1,030/oz, an impressive feat given that several other mid-tier, intermediate, and even major producers saw misses of 5% to 20% relative to guidance, with Equinox ( EQX ) being one of the worst performers. This is a testament to the company's ability to deliver on its promises and its conservatism, with the impressive margin performance (44% AISC margin or $801/oz) being achieved despite having no help from the gold price during the year. That said, while 2022 was an incredible year for the company and its share price outperformance vs. several peers that struggled is absolutely justified, 2023 will be a much different year.

Torex Gold - Quarterly & Annual Gold Production (Company Filings, Author's Chart & Company Guidance Midpoint)

{kind=link}

As noted by the company, FY2023 is expected to be a slightly softer year operationally with production of ~455,000 ounces at the mid-point and AISC of $1,105/oz. This would translate to a 10% increase in costs year-over-year based on the guidance mid-point and even Torex enjoys an average realized gold price of $1,850/oz, we will see a significant decline in margins ($745/oz vs. $801/oz). Meanwhile, capital expenditures will increase to ~$540 million, resulting in a significant cash outflow of up to $270 million vs. $~130 million in free cash flow last year.

It's important to note that this is still a very impressive production profile at industry-leading margins and the cash outflow is temporary with peak spending at Media Luna. Still, it will be a much weaker year when lapping record results in 2022. Meanwhile, FY2024 is expected to be a softer year as well, with production expected to come in closer to 430,000 and AISC likely to remain elevated near $1,100/oz when incorporating what have been sticky inflationary pressures and slightly lower sales volumes. Let's look at how Media Luna is progressing:

Recent Developments

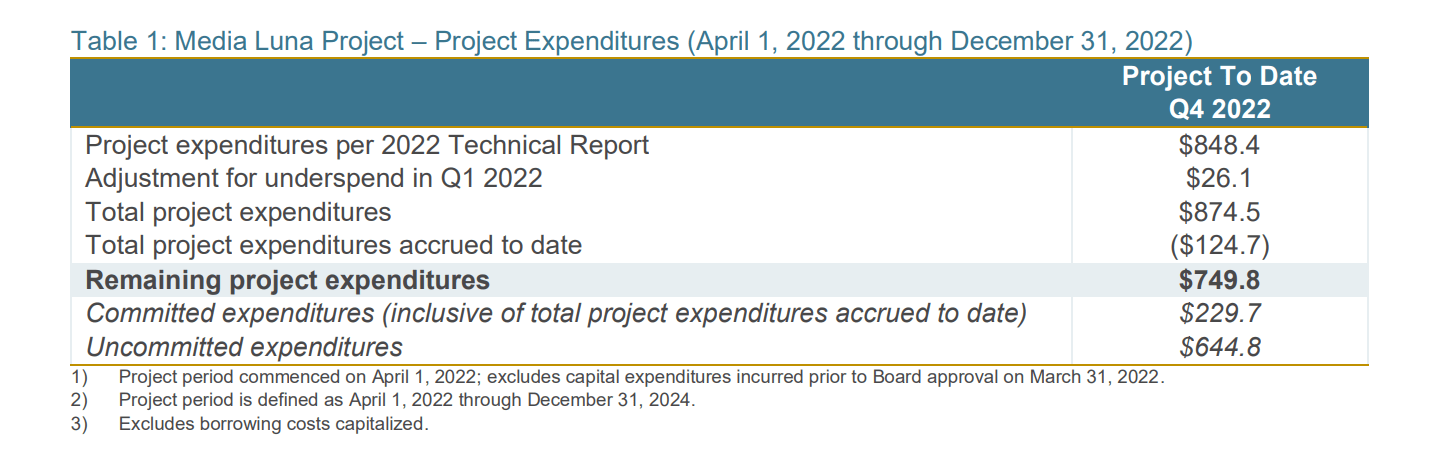

Moving over to Media Luna, Torex noted that the project is on schedule and budget as of early February (15% at year-end), with the first production from the mine expected in late 2024. As of the most recent update, 26% of upfront costs were committed and letters of intent were in place for the mobile underground fleet. Finally, the company expects the breakthrough for the Guajes Tunnel to be completed in Q1 2024, in line with its previous disclosure, and it has received approval to increase the power draw to its Morelos Property to 65 megawatts (45 megawatts currently).

Based on current liquidity of ~$620 million and upwards of $400 million in operating cash flow over the next 18 months, Torex is in great shape to fund Media Luna with no share dilution even if we see minor cost creep vs. the current capital estimate (~$870 million). This is very positive news since this is not the case for many other producers sector-wide that have had to make tough decisions to fund major growth projects or have suffered meaningful share dilution. Some examples include IAMGOLD ( IAG ) which sold Rosebel and Boto and gave up some ownership of its flagship Cote Project temporarily, Argonaut ( OTCPK:ARNGF ) that saw considerable share dilution, and Marathon Gold ( OTCQX:MGDPF ) which also diluted heavily to help fund a capex blowout at Valentine.

{kind=link}

Assuming all goes to plan, and based on Torex's five-year outlook, the company expects to maintain a 425,000+ ounce production profile (gold-equivalent ounces) out to 2027, with what should be record production in FY2027 based on a guidance mid-point of 475,000 ounces. However, depending on exploration success at ELG Underground and improved mining rates we're seeing, there could be some upside to this ~425,000 GEO estimate. So, regarding financing risk, execution risk, and maintaining a similar production profile to current levels, we continue to see these points de-risked as Torex gets closer to first production and works to optimize operations across its Morelos Property.

Valuation & Technical Picture

Based on ~87 million fully diluted shares and a share price of US$12.60, Torex trades at a market cap of ~$1.10 billion, which is a very attractive valuation for a ~450,000-ounce gold producer. Comparing this figure to a conservative estimated net asset value of ~$1.38 billion, Torex trades at ~0.80 P/NAV. While this is one of the lower multiples sector-wide among mid-tier and intermediate producers, this is partially related to Torex being a single-asset miner in a Tier-2 mining jurisdiction, making it a little riskier than more diversified producers like Perseus Mining ( OTCPK:PMNXF ) and Eldorado Gold ( EGO ) and or those that also have significant Tier-1 jurisdiction exposure like Alamos ( AGI ) and SSR Mining ( SSRM ). Of course, these negatives are balanced by Torex having one of the better margin profiles among its peer group.

Using what I believe to be a more conservative P/NAV multiple of 0.85x given that Torex is a single-asset producer in Guerrero State, Mexico, I see a fair value for the stock of ~$1.19 billion or US$13.70 per share. This points to minimal upside from current levels, and I prefer a minimum 40% discount to fair value for starting new positions in small-cap producers. So, while Torex may have upside to fair value, I don't see any margin of safety currently, and the stock would need to dip below US$8.25 to move back into a low-risk buy zone. Obviously, there's no guarantee that the stock suffers a correction of this magnitude, but I prefer to buy at the right price or pass entirely.

{kind=link}

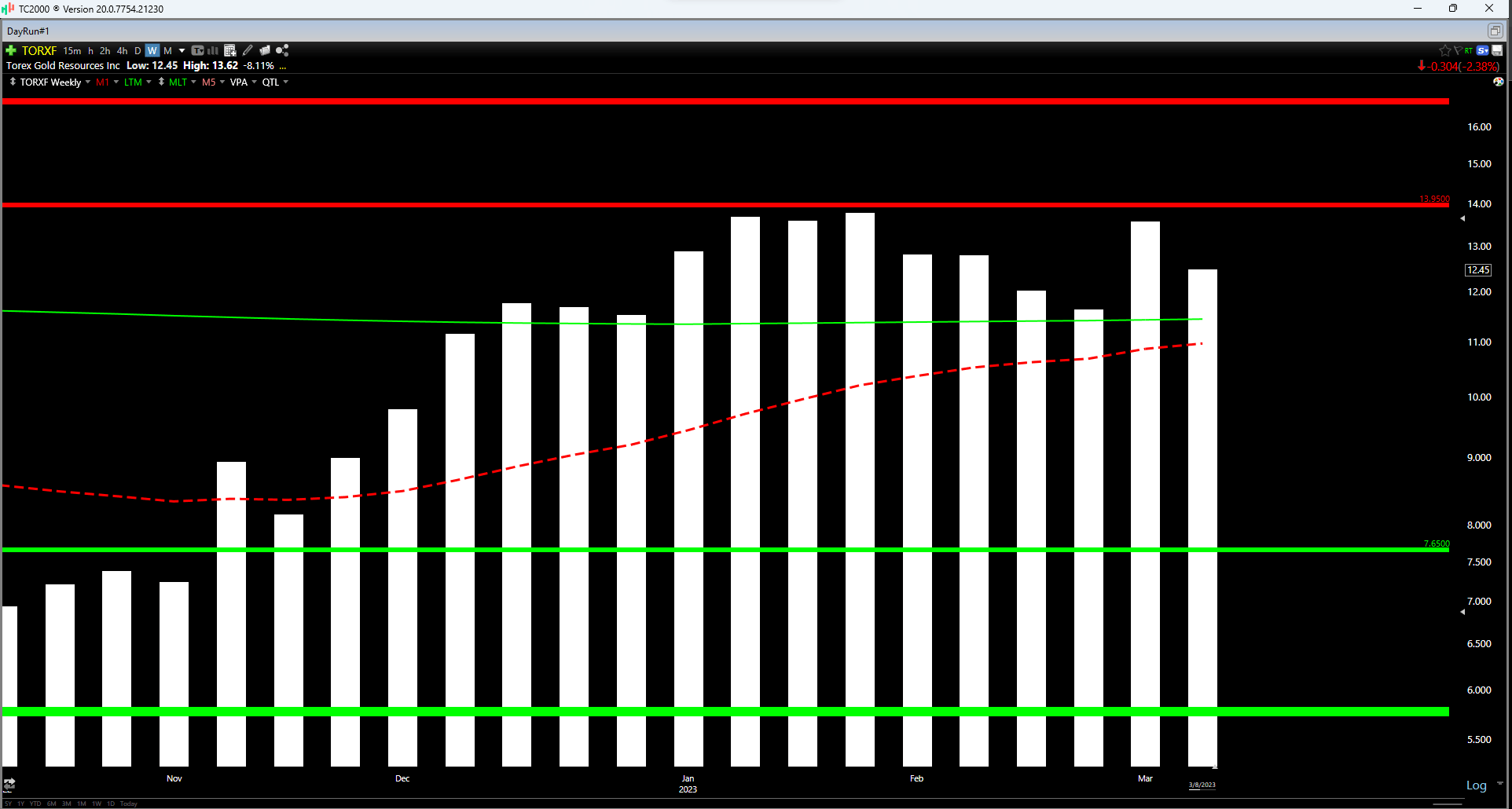

Finally, if we look at the technical picture, this corroborates the view that Torex is no longer anywhere near a low-risk buy zone. In fact, despite the stock's recent correction, it remains in the upper portion of its support/resistance range, with resistance at US$13.95 and no firm support until US$7.65. If we measure from a current share price of US$12.50, this translates to a reward/risk ratio of 0.30 to 1.0, which is well below 5.0/1.0 reward/risk ratio I'm looking for to start new positions in cyclical names. So, while Torex had an exceptional 2022 and continues to release blockbuster drill results from both sides of the Balsas River, I don't see any way to justify paying up for the stock at current levels.

Summary

Torex Gold was one of the few producers that trounced production guidance and delivered into cost guidance in FY2022, an impressive feat given that the sector had a rough year, as did its neighbor, Equinox Gold. While I expect 2023 to be another solid year, Torex is in the less favorable position of being up against very difficult comps after a record year and a full year of elevated unit costs because of inflationary pressures, making it more challenging to keep AISC below $1,100/oz. If achieved, these would still represent industry-leading margins and Torex is known for being conservative.. Still, the setup isn't nearly as attractive as it was below US$7.00 with Torex now set to see a moderate decline in output and margin compression with the stock sitting near multi-year highs.

To summarize, I see more attractive opportunities elsewhere from a relative valuation standpoint, and I don't see any way to justify chasing the stock here at US$12.60.

For further details see:

Torex Gold: Patience Required