CA - Toronto-Dominion Bank: Caution Ahead Of Earnings

2023-11-27 08:30:20 ET

Summary

- The Toronto-Dominion Bank will report full-year results on Thursday, and while I still expect solid results, we should be cautious.

- When looking at history and long-term cycles, this is not the time to invest big - especially not in banks which are very recession-sensitive.

- Not only does it seem we are at the end of a long bull market and long-term debt cycle, but the political situation around the world is also challenging.

- In such an environment, investing in banks seems dangerous and not like a good idea.

My last article about the Toronto-Dominion Bank ( TD ) was published in June 2023 and the stock price increased a little bit in the last few months - in line with the performance of the S&P 500 ( SPY ).

If you read any of my articles about the banks in Canada or the United States, you know that I am very cautious about investing in almost any bank. Right now, I only have my position in Svenska Handelsbanken ( SVNLF ). And I would be very cautious about investing in banks in the days before they release earnings as the risk of a negative surprise is quite high in my opinion. While the Royal Bank of Canada ( RY ) is reporting on the same day as the Toronto-Dominion Bank, the Bank of Nova Scotia ( BNS ) is reporting two days earlier and might give us some hints on what to expect.

Picture Slowly Getting Worse

When looking at the Toronto-Dominion Bank we can slowly see the picture getting worse. Don't get me wrong, we still see a stable and well-performing bank, but different metrics are getting worse from quarter to quarter - starting with the income statement.

9M Results

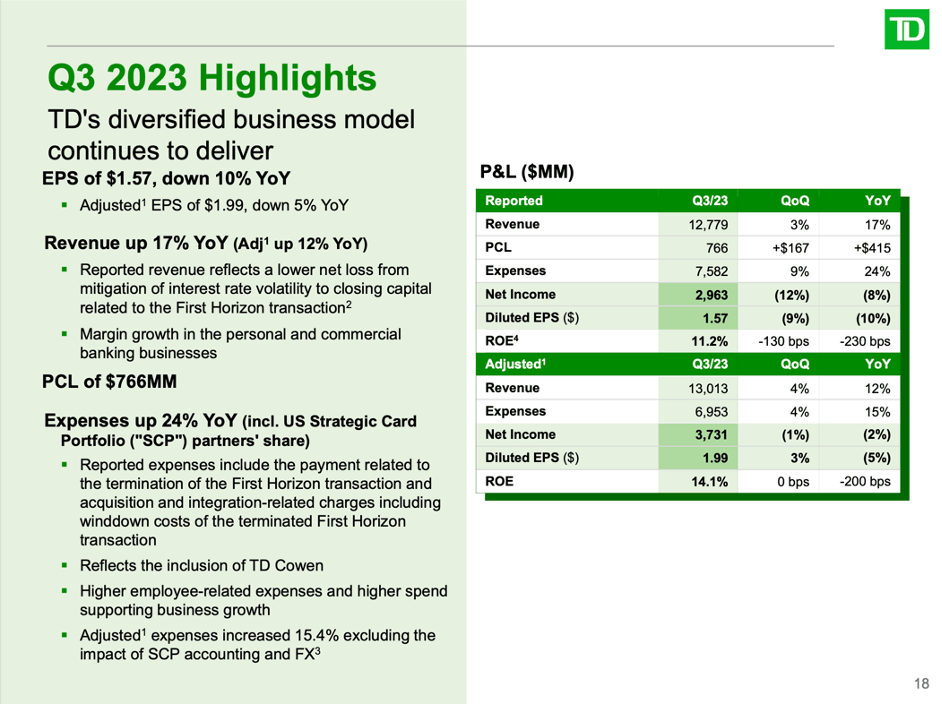

I will not look at the quarterly results, but rather at the nine months' results. This will help us not just to get a snapshot of one single quarter but a little bigger picture. When looking at the reported revenue, we see an increase from $33,469 million in the first nine months of 2022 to $37,371 million in the first nine months of 2023 - resulting in 11.7% year-over-year growth. And net interest income (13.8% YoY growth) as well as non-interest income (8.5% YoY growth) are contributing to top-line growth.

While revenue is still growing, provisions for credit losses are also increasing. Compared to $450 million in the first nine months of 2022, the provision for credit losses in 2023 so far is $2,055 million. And this has a negative impact on the bottom line with diluted earnings per share declining from $5.85 in the same timeframe last year to $4.11 in the first nine months of 2023 - a decline of 29.7% year-over-year.

TD Q3/23 Investor Presentation

{kind=link}

And the picture in the third quarter was similar to nine months' results - increasing revenue, but declining bottom line.

Investors and Customer Pulling Funds

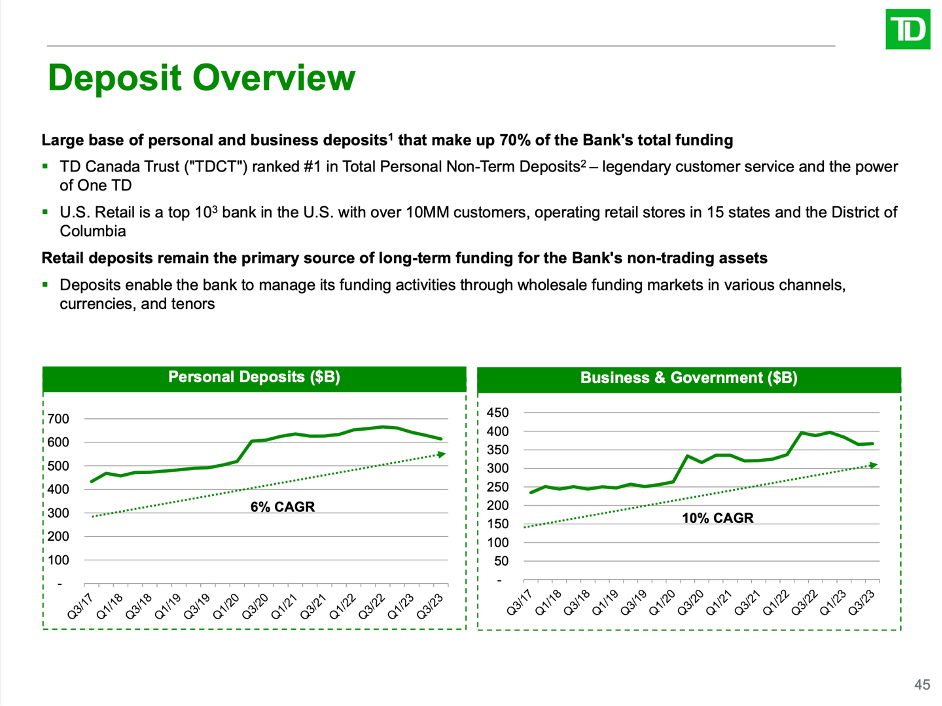

The Toronto-Dominion Bank is still the second-biggest bank in Canada and the 6th biggest bank in North America when looking at total deposits. Nevertheless, the Toronto-Dominion Bank has to report outflows like many other financial institutions.

TD Q3/23 Investor Presentation

{kind=link}

When looking at the different business segments, Canadian Personal & Commercial Banking can still report slightly increasing deposits. The amount increased from the previous quarter ($440 billion) as well as the same quarter last year ($437 billion) to $442 billion this quarter. While we still see a slight increase in Canada, average deposits for the U.S. Retail segment declined 13.9% year-over-year from $388 billion in the same quarter last year to $334 billion right now. Wealth Management and Insurance saw deposits declining from $41.2 billion in Q3/22 to only $30.0 billion in Q3/23 - a decline of 27.2% YoY.

Increasing Provision for Credit Losses

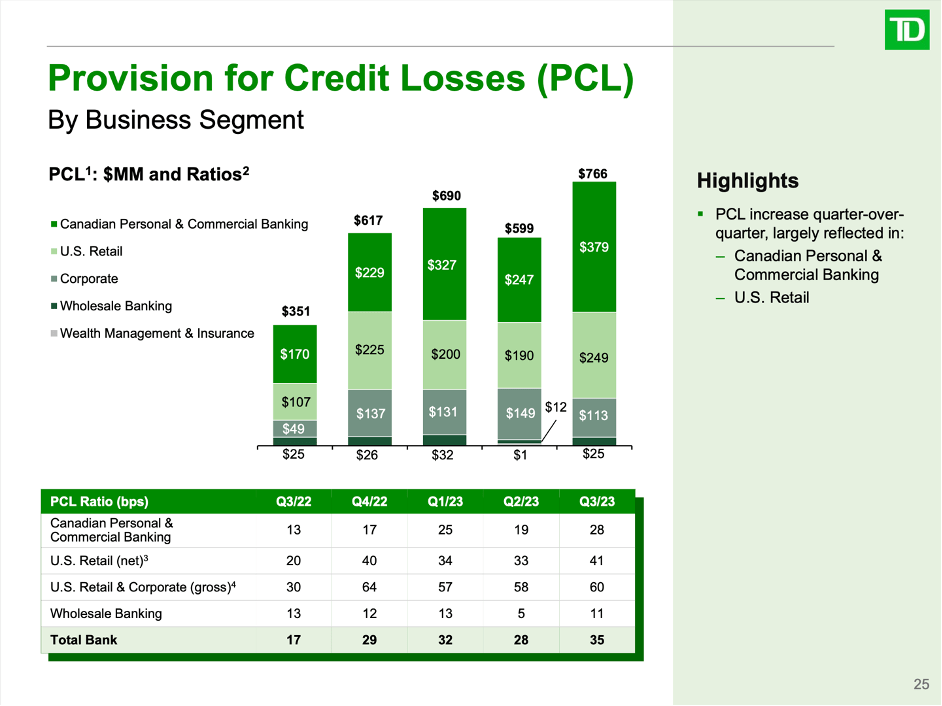

Aside from decreasing deposits, we see also increasing provision for credit losses. And while we could interpret this as a positive sign as the bank is trying to take precautions for more difficult times, it is also showing us that management is expecting more difficult times ahead.

TD Q3/23 Investor Presentation

{kind=link}

In the third quarter of fiscal 2023, provision for credit losses was $766 million - higher than in the previous quarter ($599 million) and much higher than in the same quarter last year ($351 million).

TD Q3/23 Investor Presentation

{kind=link}

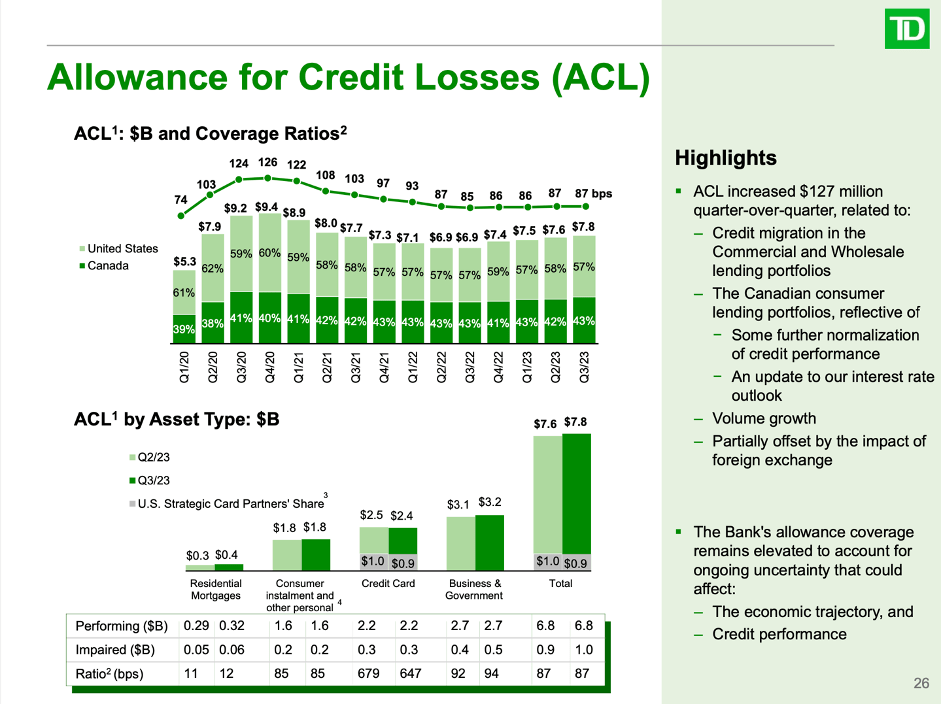

Allowance for credit losses is now $7.8 billion resulting in an ACL ratio of 87 bps. And while the ACL amount has increased only slightly the ACL ratio has remained more or less the same in the last few quarters. I am certainly aware that almost all banks have gotten more restrictive in their lending practices (see here for data in the United States), but I don't know if the Toronto-Dominion Bank is well prepared for default rates rising (if that should happen).

{kind=link}

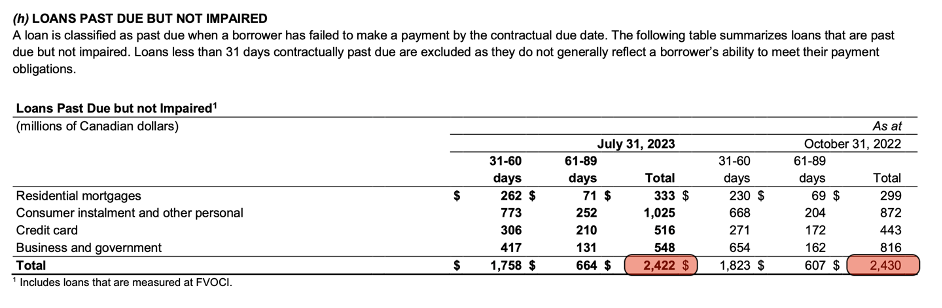

And when looking at the loans past due but not impaired, the amount on July 31, 2023 was almost the same as on October 31, 2022. This is a hint that the situation did not really get worse so far and the loans Toronto-Dominion has on its portfolio perform similarly as in October 2022.

{kind=link}

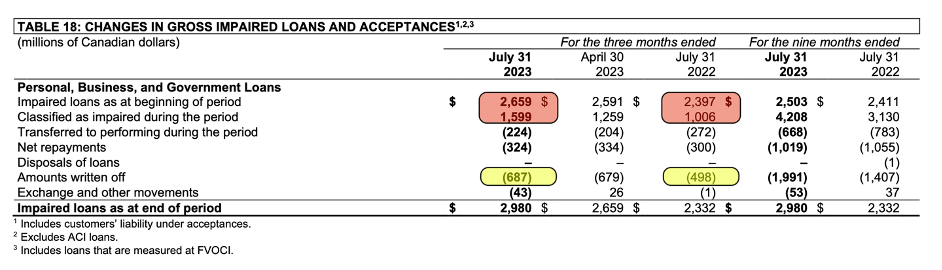

However, when looking at the amounts written off, we can see an increase compared to the same quarter last year - $687 million this quarter compared to $498 million in the same quarter last year. And while the amount seen as impaired loans at the beginning of the third quarter was already a bit higher than one year earlier, Toronto-Dominion Bank had to classify $1,599 million as impaired loans during the quarter (compared to $1,006 million in the same timeframe last year). And these are still not amounts that should make us worried, but the picture is slowly getting gloomier.

Stock Performance

Of course, we can argue that investors are already taking into account that the fundamental picture is getting worse. When looking at the trailing twelve-month numbers, earnings per share declined about 21% for the Toronto-Dominion Bank so far while the stock price already declined 23% in CAD and 28% in USD since its previous peak. Based on this data we could argue that investors are already discounting lower earnings in the stock price (by the way, the picture for the Royal Bank of Canada or the Bank of Nova Scotia is similar - in both cases, the stock declined steeper than earnings per share).

Great Recession or Great Depression?

When looking at the results, the Toronto-Dominion Bank is reporting so far, we have reason to be cautious, and the performance is not the best, but at least when looking at the numbers we also should not expect the worst. And after an already 30% stock price drop, why should we expect further stock price declines?

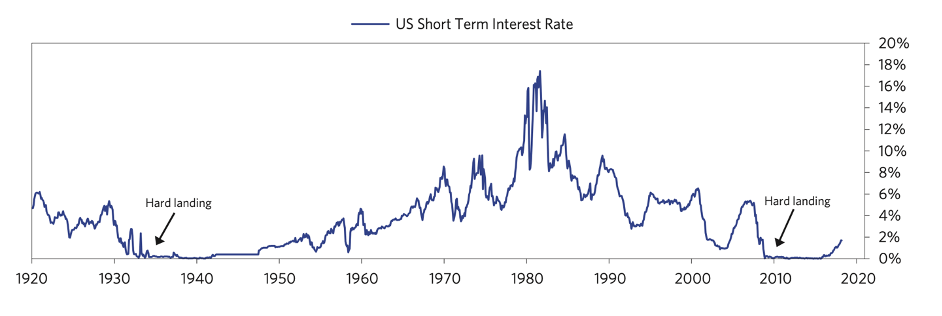

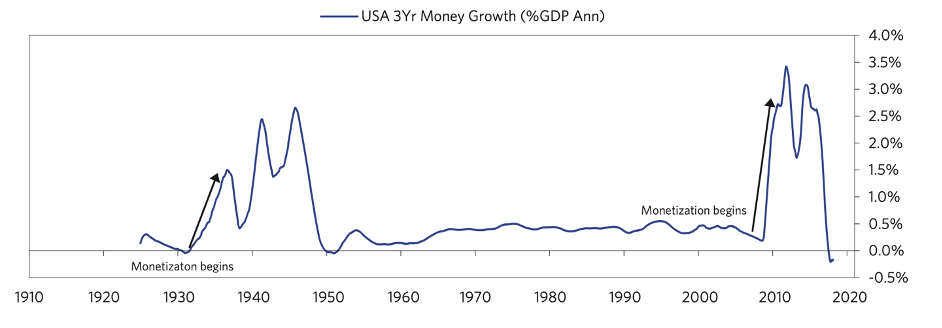

The answer to why further stock price declines for the Toronto-Dominion Bank (and many other stocks) are likely is rather simple: The risk for a recession is extremely high in my opinion (see here for further information) and as the chart below shows, the bank (its earnings per share) and the stock price are reaction to recessions.

Banks can be seen as "recession-sensitive" and are usually reacting to the performance of the economy: If the economy is booming, banks usually perform well, and if the economy is struggling, so are banks. As the headline is implying, I see the risk for another recession not only extremely high, but the question is actually if we are "only" heading towards a recession or if it is getting even worse.

Elliott Wave Theory

Of course, such a statement is extremely speculative, and nobody knows what the future will bring, but we have several hints for the world (economy) heading towards challenging times. One of these hints is technical analysis - especially the theory based on Ralph Nelson Elliott. The so-called Elliott Wave Theory is predicting another major correction similar to the Great Depression in the coming years. The best analysis one can find on Seeking Alpha on this topic is by Avi Gilburt. In a recent article , he wrote:

Our expectation is based on the completion of a long-term bull market; a long-term bull market which was actually called for by Ralph Nelson Elliott back in 1942. But, we're now approaching the conclusion of that bull market, which will then likely usher in the longest bear market we have experienced over the last 100 years.

(…)

So, of course, while the market has been up during the last 43 years, with only one nine-year period of sideways market action (2000-2009), I want to point out that the next bear market we expect is of a degree higher than the one seen in 2000-2009. In fact, it is of the same degree as the Great Depression, based on our analysis.

The theory is quite simple. We are very close to the end of a long-lasting bull market - the bull market that began in 1932 at the bottom of the crash following the Great Depression. And in the next few years (or maybe the next decade) we will see the correction of this 90-year lasting upward wave.

Long-Term Debt Cycle

While I have only limited knowledge about Elliott Wave Theory, I believe in market cycles - and these market cycles are not only visible in the stock market and investors' sentiment. Cycles are also visible when looking at other economic data. It is not surprising that long-term cycles for interest rates or debt levels go hand in hand with the cycle described by the Elliott Wave Theory.

When looking at interest rates, we see a hard landing in the 1930s with interest rates being close to zero. In the following decades, interest rates increased (until the peak in the early 1980s) and then declined to zero in the 2010s again (another hard landing during the Great Recession).

Ray Dalio - Principles for navigating the big debt crisis

{kind=link}

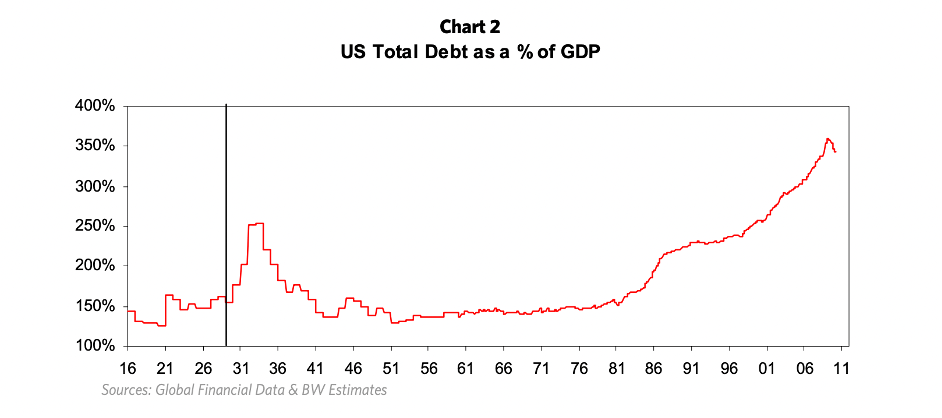

Aside from looking at interest rates, we can also look at debt levels and we will see the same cycle. Debt levels peaked before the Great Depression hit the United States and declined in the following years before debt started increasing again until this day.

Ray Dalio - Economic Principles

{kind=link}

Aside from high debt levels, a typical sign that we are near the end of a cycle is the printing of money. When central banks don't seem able to get the situation under control by just lowering interest rates (and rates are already close to zero), monetary easing is the next "instrument" they use.

Ray Dalio - Principles for navigating the big debt crisis

{kind=link}

I know we can interpret the data above in a way that the big crash already happened (the Great Recession) but I would argue the worst is still upon us. When looking at the Global Debt Monitor by the IMF for example, we see debt levels around the world higher than in 2004 (before the Great Recession) and higher than in the 2010s and these debt levels have to come down one way or another (as it has happened at the end of every cycle).

Changing World Order

Aside from the financial situation and interest rates and debt levels giving us strong hints that we are at the end of a long-term debt cycle, the political situation in the last few years (or maybe the last decade) is also a strong hint that we are at the end of a long-term cycle (and that the worst is still upon us). In this case, it is the cycle of one superpower (the United States) dominating the world.

In his book Principles for dealing with the changing world order Ray Dalio is describing the decline (see pages 49-51). Aside from the already mentioned high debt levels and monetary easing, we typically see populism rising on the left and right and conflicts within the country are escalating. Often, we see a rising power challenging the existing power and we see hot wars.

While we can look at hard data regarding interest rates, debt levels or monetary easing, it is not so simple to "measure" conflicts or populism. We must be cautious not to fall victim to the confirmation bias (seeing signs for a Great Depression and changing world order as long as we are searching for these signs), but I would argue it is difficult to ignore and Dalio makes a compelling case in his book. Dalio is not the only one (and not the first) to describe such a cycle and the rise and fall of nations (see, for example, The Rise and Fall of the Great Powers by Paul Kennedy).

We see huge internal conflicts among nations that had to be described as stable one or two decades earlier. This is clearly visible in the United States, but also in many European countries including Germany, my home country. And that conflicts between nations are increasing again also seems obvious in my opinion.

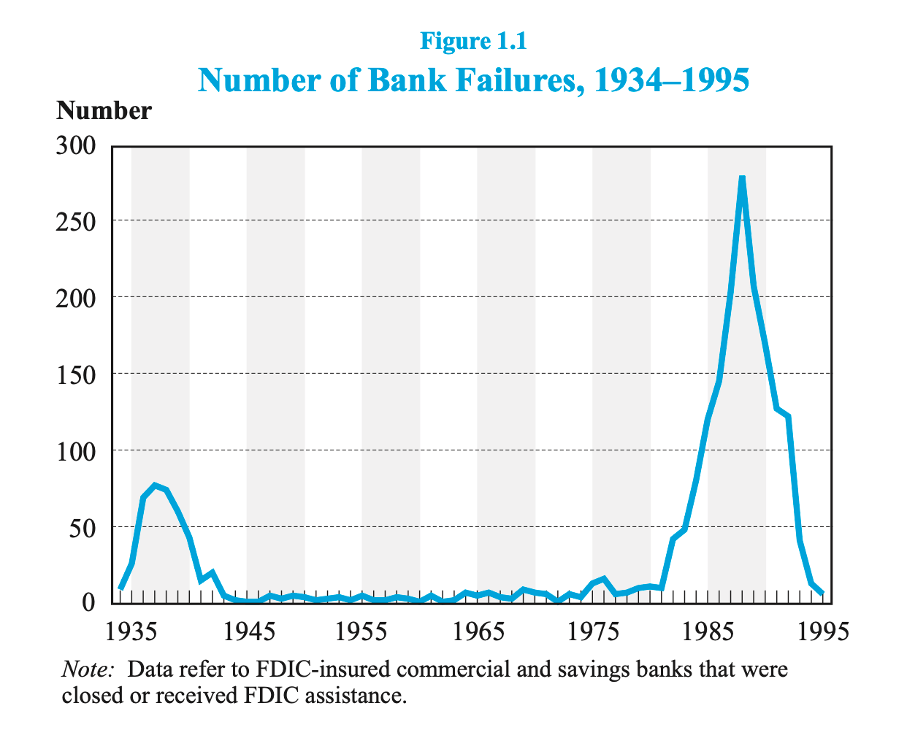

Banks During a Recession/Depression

When assuming that we are headed towards another crisis similar to the Great Depression, we have to ask what such a scenario means for banks and financial institutions. And the answer is as simple as scaring: during the Great Depression, banks were failing all over the United States. In 1930, about 1,350 banks failed, in 1931 about 2,300, in 1932 about 1,500 and in 1933 about 4,000 (see here for a short overview). Nevertheless, I don't think we will see banks failing with such a high rate once again. Following the Great Depression, regulations improved, and the FDIC was created in June 1933 leading to a much lower rate of bank failures. Nevertheless, a scenario similar to the Great Recession or the Savings & Loan Crisis in the 1980s is possible and hundreds of banks might fail once again - not only in the United States.

{kind=link}

In my article Bank Crisis: A short history I described these three banking crises in more detail.

Expectations for the Toronto-Dominion Bank

Finally, the question remains what such a scenario means for the Toronto-Dominion Bank. My expectations for the fourth quarter and upcoming earnings are not easy to summarize. I am still expecting solid results (analysts are expecting earnings per share to be $1.35) but also assume that the provision for credit losses will be higher again and deposits might continue to decline. The huge problem is that we must look deeply into the financial statements to see the hints for upcoming problems and as banks are extremely complex corporations, it is very difficult to see these problems before they are really obvious to everyone.

In the earnings report, we should pay close attention to loans impaired, loans past due between 30 and 90 days, and the provision for credit losses.

I would also not be surprised if, at some point in the next few months, one or several bank(s) will report terrible results - and it could be a Canadian bank as well. Basically, the "Lehman moment" of 2023 or 2024. I know this is very speculative - nevertheless it is a scenario I am trying to prepare myself for - by not buying banking stocks right now. And in case of The Toronto-Dominion Bank, I see it as a likely scenario for the stock to break its support level around $77-78 (or about $55 in USD) in the next few months. On the other hand, I don't think the Toronto-Dominion Bank will be among those banks that could collapse in the next few years (but this is speculation once again).

Bottom Line

We are at a challenging time in history. Global superpowers seem to fight for a new world order. External and internal conflicts are on the rise and interest rates near zero combined with extremely high debt levels are making it difficult for governments to act properly (or in a way to raise the living standards for everybody). Based on historical knowledge and patterns we saw again and again, I can't invest in banks right now.

I will also admit that investing (and especially trading) based on the theory that we are close to the end of a long-term cycle is difficult. People (including myself) have been stating this for several years, but if you actually think we can time the end of a cycle lasting for 80 to 100 years to a certain month or quarter, I don't know what to tell you.

I mentioned Avi Gilburt above and I also like to point out his opinion that there is a chance for the stock market to go higher again (and make new all-time highs) before it collapses. I personally don't see new all-time highs anymore and think we are already in a long-lasting bear market and it might make sense to wait a few years before investing huge amounts of cash again into the stock market.

For further details see:

Toronto-Dominion Bank: Caution Ahead Of Earnings