ET - Tourmaline Oil Insider Buying: 3 Oil And Gas Stocks To Consider Now

2023-04-27 15:53:40 ET

Summary

- Insiders have been buying shares at three oil & gas companies lately.

- While there are numerous reasons for insiders to sell company shares, there is typically only one reason they buy.

- Investors who can stomach the short-term volatility and the possibility of lower oil & gas prices this quarter should benefit greatly later on.

- I discuss oil prices and analyze 3 companies with recent insider buying.

Insider Buying: 3 Oil & Gas Stocks To Watch Closely

Insiders from multiple oil & gas companies have been using the recent market downturn as a buying opportunity, acquiring shares of their own companies. I believe this is a bullish sign for each stock price, for obvious reasons.

Here's why: While there are numerous reasons for insiders to sell company shares, there is typically only one reason they buy, and it's a simple one: they believe their company's stock is undervalued, and will rise over time.

Although it's not the only criteria to consider when evaluating a company, tracking and analyzing insider activity has proven valuable. In many cases, I've found that insiders have (mostly) timed their purchases wisely.

Oil price update

YCharts

First, it's worth taking a step back to understand the current oil price action to see why there have been sell-offs in oil & gas stocks in the first place.

Oil prices surged to $80/barrel earlier this month following OPEC's unexpected production cuts . However, oil prices have since declined, nearly erasing the gains from OPEC's decision. Despite a significant decline in U.S. crude stockpiles, the dollar has risen in value and oil has fallen in price, largely due to the likelihood of the Federal Reserve raising interest rates again next month (which could potentially weaken energy demand further).

Oil's short-term outlook remains uncertain for these reasons. But the latter half of 2023 seems more promising for a rally in oil & gas prices due to supply concerns, and in the stocks I mention below.

- First, investors should note that the OPEC cuts have not yet taken effect (they begin in May).

- Second, expect a big oil deficit in H2 2023. According to the International Energy Agency's ((IEA)) Oil Market Report ((OMR)), "Surprise OPEC+ supply cuts announced on April 2 risk exacerbating an anticipated oil supply deficit in 2H23 and bolstering oil prices during a period of heightened economic uncertainty, even as industrial activity slows in the world's largest economies and production growth outside the alliance appears robust."

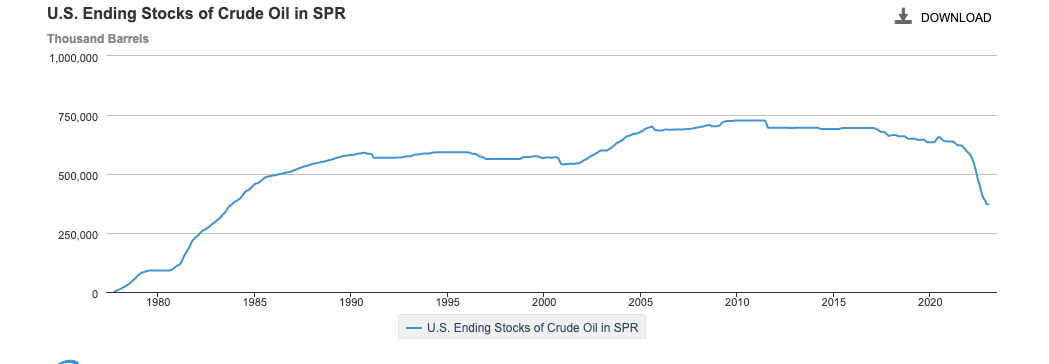

- Finally, remember that the U.S. has stated it intends to refill the Strategic Petroleum Reserve ("SPR") after selling 180 million barrels last year when oil sold at just under $100 per barrel. Refilling the reserve means the U.S. will step back in as a major buyer of oil, increasing its demand (and likely supporting prices). Currently, the reserve is down to 367.96 barrels, its lowest level in nearly 20 years!

{kind=link}

The bottom line: Investors who can stomach the short-term volatility and the possibility of lower oil & gas prices this quarter may be rewarded handsomely in H2 2023 and beyond.

Without further ado, here are three oil & gas stocks that have recently experienced recent insider buying. I detail the insider transactions, provide an overview of each company and its valuation, and offer a bottom line for investors.

3 Oil & Gas Stocks With Insider Buying

| Stock |

| Market cap (billions) |

| P/E ratio |

| Dividend yield |

| Tourmaline |

| $15.0 |

| 4.65 |

| 1.64%* |

| Baytex |

| $2.05 |

| 3.49 |

| N/A |

| Energy Transfer |

| $39.4 |

| 9.0 |

| 9.63% |

*Not including any special dividends.

1. Tourmaline Oil Corp. (TRMLF)

Tourmaline is Canada's largest natural gas producer and its fourth-largest gas processing midstream operator. Currently, 80% of the company's production comes from natural gas, and it also claims to have the lowest capital costs in the Alberta Deep Basin.

Tourmaline's management has guided for 2023 production of 520,000 - 540,000 barrels of oil equivalent per day ("BOE/D"). This should lead to annual operating cash flow just shy of $4 billion and free cash flow of $2 billion, according to company estimates published at its corporate presentation .

Tourmaline stands out to me as a super-attractive oil & gas stock for several reasons:

Insider buying: Three insiders at Tourmaline Oil Corp. have bought C$6 million (US$4.45 million) worth of shares over the past year, according to MarketBeat . Here's a summary of insider transactions this year:

-

On April 17, Janet Weiss, Director, bought 350 shares at C$45.58.

-

On March 7 and 13, Mike Rose, Senior Officer, bought a combined 10,000 shares at C$55.70 and C$58.77. Rose also purchased 5,000 shares at C$62.77 on January 25.

-

On January 23 and 25, Jill Angevine, Director, bought 1,120 shares at C$62.63 and C$65.94.

-

Currently, 5.47% of its stock (18.5 million shares) is owned by insiders, which is the largest insider ownership among senior E&P peers, according to the company.

Valuation: The stock trades at dirt cheap levels, with a P/E ratio of 4.65, and EV/EBITDA of 4.23, both below the sector median. It also carries a book value per share of over $40, just shy of its current share price.

Balance sheet strength: Tourmaline has one of the strongest financial positions of any oil & gas stock I've evaluated. It's common to see an oil company of its size carry billions in debt on the balance sheet in this capital-intensive industry. But Tourmaline ended 2022 with just $494 million in debt. And, it expects to end the year with a cash positive position.

That gives the company enormous financial flexibility - it can ramp up its shareholder returns via increased dividends and buybacks, or use its firepower to complete accretive deals, should it desire to, for example.

Dividend: The company paid a $7.90 per share dividend last year, which equals a trailing yield of 17.56% based on its current stock price of $45. That includes its regular quarterly dividend and a special dividend.

Its current quarterly dividend of $.25 equals a 1.62% current stock yield. However, the company issued a $2/share special dividend earlier this year, and it's highly likely the company issues another special dividend again this year, based on its past track record.

Bottom line: Tourmaline is one of the lowest-risk energy stocks I've analyzed. It's a proven operator with strong, diversified production in North America, low cash costs, and one of the strongest balance sheets in the oil & gas sector.

Note: The lower trading volume on the U.S. OTC exchange, and the potential for high trading fees on brokerage accounts, is a risk for U.S. investors to consider.

2. Baytex Energy Corp. ( BTE )

Baytex Energy Corp. is crude oil and natural gas producer with operations in the Western Canadian Sedimentary Basin and in the Eagle Ford in the United States. Baytex's vision is to grow into a top-tier North American oil producer focused on per share value creation, according to the company.

2022 was a great year for Baytex, as it says it generated record free cash flow of $622 million ($1.11 per share) on the back of strong production of 83,519 boe/d. It used its cash flow to focus on reducing its net debt (30% reduction last year, to $987 million) and reward shareholders with an aggressive share buyback (24.3 million shares, of 4.3% of shares outstanding, were repurchased in 2022).

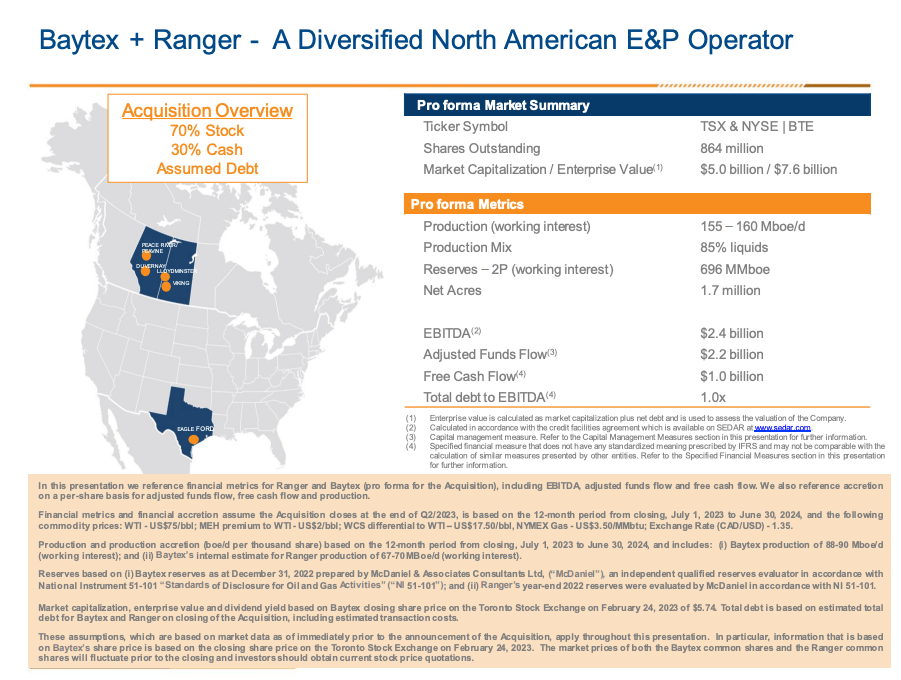

While Baytex appears to be highly leveraged with close to $1 billion in debt, investors should note that $410 million of this debt does not mature until 2027. And recently, Baytex announced $800 million in unsecured notes , not due until 2030, to fund its merger with Ranger Oil (expected to close in Q2).

{kind=link}

The combined co. will command a higher market cap ($5 billion), stronger production, more liquidity, and a greater ability to return capital to shareholders. The company currently estimates the move will be 20% accretive to its free cash flow per share, for example.

Insider buying: Four separate insiders have purchased C$283,312 worth of stock over the past 12 months, according to MarketBeat . Most recently, Kendall Douglas Arthur, Senior Officer, bought 10,000 shares at C$5.50 (US$4.08) on March 7.

The Ranger Oil acquisition looks like a transformative move for the company, and, I think it's a good sign that insiders have been buying ahead of the closing of the acquisition.

Valuation: Like Tourmaline, Baytex shares look like a bargain here. Its shares carry a P/E of 3.49 (below the sector median of 7.59), and an EV/EBITDA of 2.76 (vs. 5.53 sector median), according to data from Seeking Alpha. It also carries a book value per share of $5.56, higher than its current stock price.

Dividend: One potential downside of owning the stock is the fact that it (currently) does not pay a dividend. That'll likely change following closure of the Ranger Oil transaction, but it's something to consider when evaluating your current investment options.

Bottom line: Baytex's stock is down 28.59% over the past year, but the worst of it may be behind it.

3. Energy Transfer LP ( ET )

Energy Transfer Partners is one North America's largest midstream energy companies, with approximately 120,000 miles of pipelines and energy infrastructure assets located across 41 states. It owns a diverse portfolio of assets, including pipelines and storage facilities.

The company essentially transports various commodities across the country, namely, crude oil (17% of its adjusted EBITDA), natural gas and refined products (23%), and midstream (nat gas, crude oil, and nat gas liquids (25%). Its earnings are supported by its "fee-based" contracts it has signed with its clients.

Energy Transfer is definitely a lower-risk bet in the oil & gas sector due to these fee-based contracts, as its earnings are not as affected by commodity price fluctuations. The contracts often involve "take-or-pay" agreements, which means the clients pay a pre-determined fee to transport, store, or process the oil or gas, regardless of volume.

As a Master Limited Partnership ("MLP"), Energy Transfer also benefits from certain tax advantages. For example, the company is not taxed at the corporate level as it's considered a pass-through entity, and unitholders report their share of the company's income and expenses on their personal tax returns (using form K1's).

Here's why Energy Transfer looks like an attractive investment opportunity.

Insider buying: Insiders have been buying shares aggressively over the past year. In fact, there have been 34 open market buys compared to only 6 sells in that timeframe, according to Nasdaq . Insiders have purchased 14.86 million shares. Most recently, Kelcy Warren, Chairman, bought 1.33 million shares at an average price of $12.99 on Feb. 22, according to MarketBeat .

The following insiders have purchased ET shares in the last two years, according to MarketBeat (with dollar value):

- Kelcy L Warren ($201 million),

- Michael K Grimm ($5.65 million),

- Ray W Washburne ($2.79 million),

- Richard D Brannon ($1,802,980)

- Bradford D Whitehurst ($606,101)

- Thomas E Long ($600,068)

- Matthew S Ramsey ($250,029).

Approximately 3.28% of its stock is owned by insiders. While that sounds like a small percentage, Energy Transfer is a $39 billion company, so it represents a huge investment worth more than $1 billion.

Valuation: Energy Transfer looks like a reasonably priced MLP, with a P/E of 9, an EV/EBITDA of 7, and a price-to-sales of .44. Additionally, its shares look even more attractive looking out 12 months, as it carries a forward P/E of just 6.86, according to Yahoo Finance.

Distribution: One of the key reasons to invest in its stock is for its distribution. Energy Transfer is currently paying out $1.23 annualized (back to its payout levels before the pandemic hit), after its recent distribution increase . Its shares now yield 9.78%, as of writing.

This distribution looks very sustainable here given that Energy Transfer is producing close to $2 billion in distributable cash flow on a quarterly basis, and is paying out ~$950 million in distributions per quarter to maintain its yield (see its Q4 2022 financial results for more details).

Risks to consider: Energy Transfer has stable, consistent cash flow and earnings from its largely fee-based contracts. But the company does carry quite a bit of debt. Even after reducing debt by $800 million last year, it has total long-term debt of $48.2 billion. Commodity prices tanking in a worse-than-expected recession, for example, could put pressure on its earnings, and make it harder to service that debt, or at least maintain its distribution payout.

Bottom line: Energy Transfer Partners is a lower-risk stock to own in the oil & gas sector, as its earnings and cash flow are far less dependent on commodity prices. The stock is a high-yielder that should continue to pump out consistent distributions every quarter, and its near-10% yield looks sustainable, despite the company's debt load.

But, I will also point out that the stock is only worth considering if you fully understand the tax implications and potential drawbacks of owning an MLP.

For further details see:

Tourmaline Oil Insider Buying: 3 Oil And Gas Stocks To Consider Now