CA - Tourmaline Oil: One Of The Best Natural Gas Companies Out There

2023-10-27 10:30:00 ET

Summary

- Tourmaline Oil's share price has performed well despite weak natural gas prices, thanks to exposure to multiple markets and a credible growth plan.

- The company generated strong cash flows and reported a net income of C$511M in the most recent financial results.

- Tourmaline has acquired Bonavista Energy in a cash and stock deal, which is expected to increase production and generate significant free cash flow.

Introduction

It has been a while since I discussed Tourmaline Oil (TRMLF) (TOU:CA) here on Seeking Alpha. Despite the very weak natural gas prices and given Tourmaline's high exposure to those prices (in excess of 75% of its oil-equivalent production actually consisted of natural gas), the company's share price has performed quite well. One of the reasons for the strong performance likely is Tourmaline's exposure to the natural gas prices in several markets and the fact that it has a credible and self-funded growth plan. The market likes it when a company actually does what it said it would do.

The company still is a cash flow machine

Before looking at the most recently announced acquisition - which I think will prove to be a good move - I briefly wanted to have a look at the company's most recent financial results. After all, its balance sheet and cash flows are fundamental elements in the decision-making process on the M&A front.

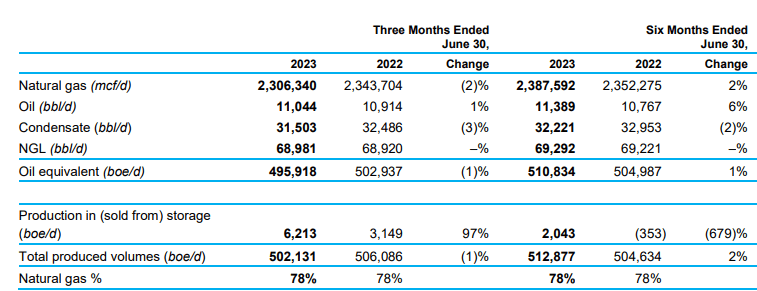

The company produced an average of just under 500,000 barrels of oil-equivalent per day which was quite a bit lower than in the first quarter of the year due to wildfire-related production disruptions. This also resulted in a downgrade in the full-year production guidance which is now set at 520,000 boe/day. That's the lower end of the initial range of 520-540,000 boe/day but this still implies the company needs to produce an average of almost 530,000 boe/day in the second semester to meet this guidance.

{kind=link}

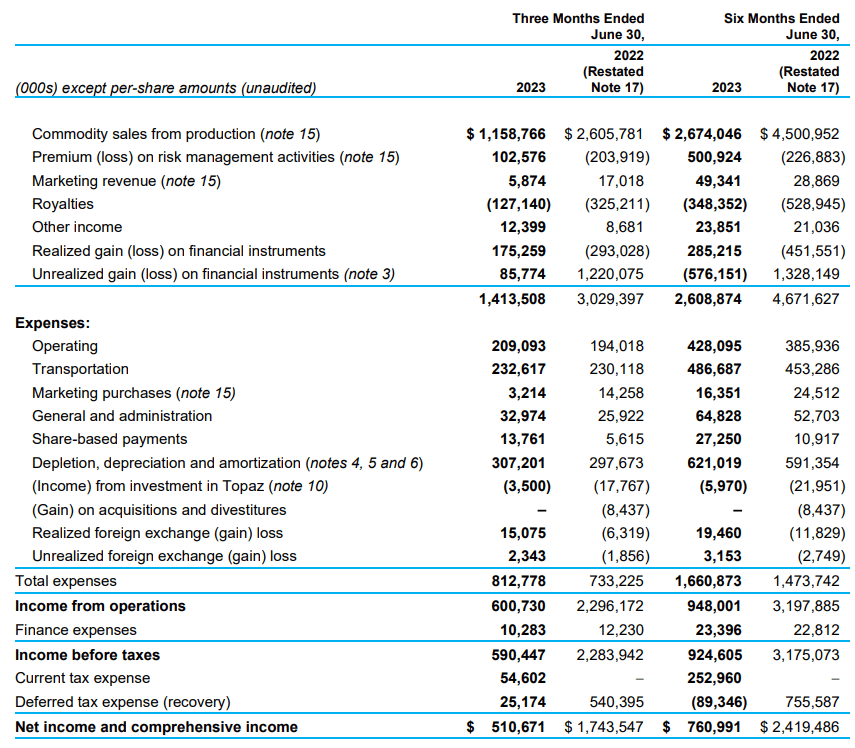

The company generated a total revenue of C$1.4B and this resulted in a total income from operations of approximately C$601M, as you can see below. The net finance expenses remained exceptionally low - a testament to the financial strength and capital management of the company), and this ultimately resulted in a net income of C$511M. This represented an EPS of C$1.51 per share.

{kind=link}

That is an excellent result although the income statement above also clearly shows the second quarter was positively impacted by a C$261M realized and unrealized gain on financial instruments while there was a very substantial unrealized loss in the first quarter of the year. That's also why the EPS in the first semester was just C$2.24 as the H1 results include a net unrealized loss of C$290M.

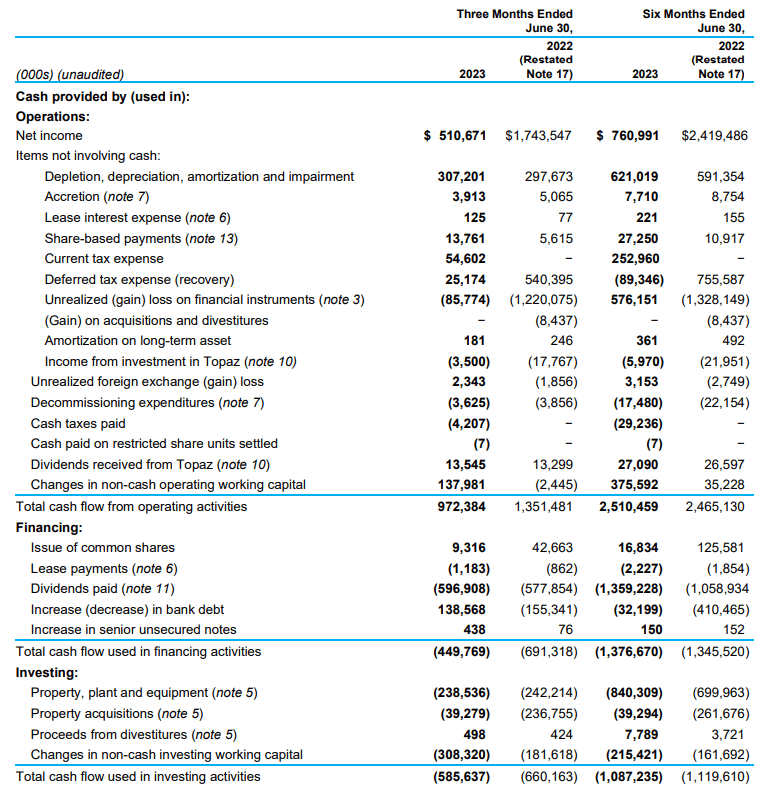

From a cash flow perspective, the company still is a very strong performer. The reported operating cash flow in the second quarter of the year was a positive C$972M but this includes a C$175M realized gain on the commodity prices and a C$138M contribution from changes in the working capital position. On the other hand, we still need to deduct in excess of C$1M in lease payments.

{kind=link}

The adjusted operating cash flow (including the realized hedging gains but excluding the working capital changes) was C$833M. And as you can see in the image above, the total capex was just C$239M while the company spent an additional C$39M on acquisitions. The underlying free cash flow (excluding acquisitions) was almost C$600M and that also is almost exactly the total amount of cash that has been spent on the dividend payments.

{kind=link}

Tourmaline is guiding for a full-year capex of just under C$1.7B which means the normalized quarterly capex is approximately C$425M. Using that number in combination with the Q2 operating cash flow, the underlying free cash flow was C$400M or C$1.18 per share. Definitely not bad for a company whose production profile was impacted by the wildfires as this meant the normalized operating cash flow would likely have been C$50-75M higher.

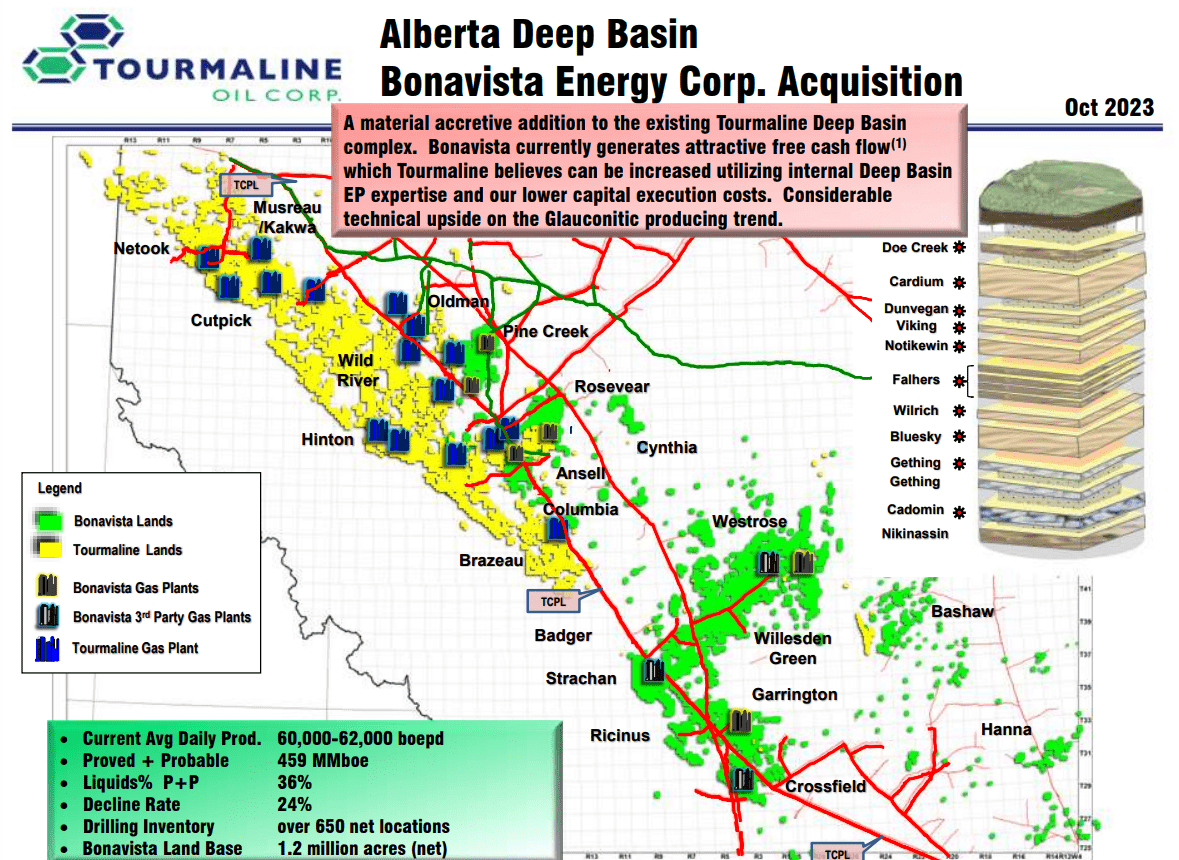

A closer look at the recent acquisition of Bonavista Energy

A strong financial performance also allows a company to pursue strategic M&A options. Tourmaline has been spending the majority of its free cash flows on dividends and special dividends but recently pulled the trigger on a C$1.45B acquisition .

It is acquiring all outstanding shares of Bonavista Energy in a 50/50 cash and stock deal. A very interesting move as this will increase the production rate by an average of 60,000 boe/day. Based on strip pricing, the asset is expected to generate C$450M in net operating income In 2025. As Tourmaline expects to spend 'under C$225M per year' on capex, the free cash flow from this asset will likely come in at at least C$225M which means Tourmaline is paying less than 7 times the free cash flow based on strip pricing.

{kind=link}

While that is not exceptionally cheap, we also shouldn't forget about the potential synergy benefits here. As the image above shows, the Tourmaline and Bonavista land packages are very complementary and are further strengthening Tourmaline's position as a leader in the Canadian natural gas space.

Investment thesis

I have a small long position in Tourmaline as the company simply is one of the best-managed natural gas producers out there. Its management team continues to show it is making the right decisions and I think the acquisition of Bonavista Energy makes a lot of sense too. Unfortunately, the share price ran away from me before I could build out a meaningful position, but I keep on hoping for a pullback as I think Tourmaline is a buy at the current levels, and even more so at a slightly lower share price.

Cash is expensive these days and my need to be careful with my investment decisions (at least until the cash from the acquisition of Textainer Holdings hits my account) is the only reason why I am not adding to this position right now.

For further details see:

Tourmaline Oil: One Of The Best Natural Gas Companies Out There