VZ - Tower REITs Carriers And Lead-Sheathed Cables

2023-07-20 17:53:34 ET

Summary

- Market reaction appears significantly overdone with regard to concerns tied to lead-sheathed cables.

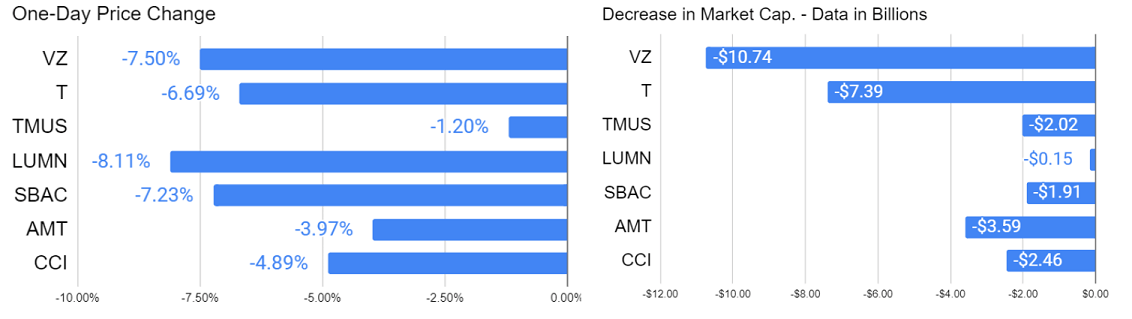

- In one day, market cap for carriers was down $20 billion. For tower REITs, down $8 billion.

- The cost of leasing space from the tower REITs is not substantial. The big costs are equipment and spectrum. Slower growth for now? Maybe. Shrinking footprint? Very unlikely.

- The story should get some headlines for a bit, before many consumers lose interest. T and VZ could afford to clean it up, but probably won't eat the majority of the cost.

- I responded to the drop by adding to my position at SBAC.

July 17, 2023, was a particularly rough day for AT&T ( T ) and Verizon ( VZ ) as further evidence regarding lead-sheathed cables comes to light. T-Mobile ( TMUS ) is doing much better since they don’t own the toxic assets (sorry, that pun was begging to be used).

The damage also is weighing on prices for the three cell tower REITs: American Tower ( AMT ), Crown Castle International ( CCI ), and SBA Communications ( SBAC ).

Note: CCI provided disappointing guidance in the Q2 earnings announcement, which added further pressure to share prices on 7/20/2023. I don't intend to cover that in this article beyond saying that CCI affirmed that they have not seen carriers changing their behavior in response to the negative publicity about lead cables.

A Brief Summary

WSJ (Wall Street Journal) prepared some (paywalled) outstanding journalism .

- WSJ tested for lead around older lead-sheathed cables.

- High lead was strongly linked to old lead-sheathed cables. Correlation established.

- Further testing indicated that the lead near the cables most likely originated from the cables. Causation established.

Some analysts suggested that the total cost to clean up the mess could be around $60 billion . They believe it's unlikely the carriers would actually be forced to pay most of it. Take the number loosely. I cannot vouch for or against the quality of their work.

In addition to T and VZ, they identified “Lumen” as having significant exposure. Is that Lumen Technologies ( LUMN )? That’s my guess, but it wasn’t explicit.

Why It Matters For Cell Tower REITs

Poor management at VZ and T drove poor capital allocation decisions. The carriers might choose to reduce capital expenditures. Whether they actually pay for the cleanup or not, this would be an excuse for reducing capital expenditures.

How would that play out for the financial results at the REITs?

It would reduce the organic leasing revenue growth rate .

That would show up as a reduction in same-property revenue, which would hit same-property NOI, then EBITDA, then FFO and AFFO per share. Consequently, the projected bounce for AFFO per share growth rates in 2024 could be smaller than previously projected.

However, investors absolutely shouldn’t blow this out of proportion.

2023 Guidance

Due to some non-recurring charges and the spike in interest expense on floating-rate debt, 2023’s growth rates were unusually low . Remember, this is about growth rates. Not absolute values.

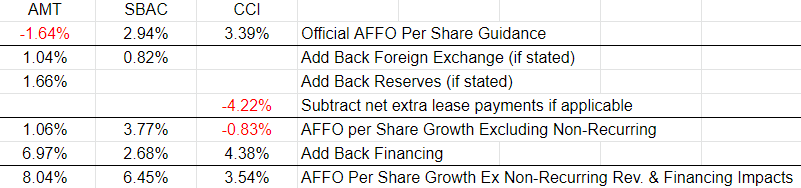

Official AFFO per share guidance ranges for the REITs were significantly impacted by interest expense and non-recurring factors:

{kind=link}

Author calculations using publicly provided guidance from REITs as of Q4 2022 reports

Note: This chart uses the initial 2023 guidance. Adjustments to guidance were small.

If we normalized for all non-recurring factors and stabilized interest rates, the growth rate would’ve been pretty good. The underlying assets for AMT and SBAC were doing well. CCI was having a harder time leasing.

Since 2023 includes much higher interest expense than 2022, it provides an easier base year going into 2024. However, rates have climbed quite a bit in 2023, so there will still be some interest expense headwind for AMT and CCI in 2024. Less than in 2023, but still some.

CCI has larger headwinds for AFFO per share in 2024 and 2025 than AMT or SBAC, which leads to CCI having a lower AFFO multiple.

Target Adjustments and Expected Trade

Slight reduction for three factors (in order of impact):

- Negative sentiment.

- Further elevated short-term rates.

- Potential slight pressure on revenue growth rate.

Factors by REIT:

CCI: All domestic. Greatest percent of total revenue from T and VZ. Significant floating-rate debt.

AMT: Most international exposure. Lowest % of revenue from T and VZ. Significant floating-rate debt.

SBAC: Middle international exposure. Middle % of revenue from T and VZ. All floating-rate debt may be gone as early as the start of 2024.

I decided to increase my SBAC position.

Time for Math

How much exposure to weaker revenue growth could the cell tower REITs have?

It’s hard to nail down a precise estimate because it really depends on how much the carriers need to pay and when. So far, we don’t know if they will actually pay anything.

However, the valuation swings were substantial:

{kind=link}

Author's Calculations

Thanks to LUMN being so much smaller, the drop in market cap there was much smaller despite having the largest percentage decline. In total, the carriers lost just over $20 billion on the day and the cell tower REITs fell by nearly $8 billion.

That seems like an overreaction.

AMT

We will use AMT for this.

Shares are down roughly 4% and the market cap is down $3.6 billion.

What is AMT’s exposure to T and VZ?

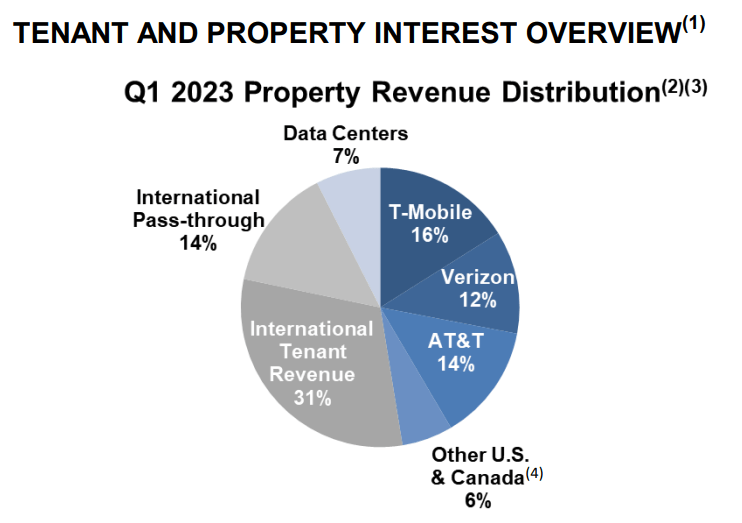

{kind=link}

American Tower

The numbers:

- AMT’s Q1 2023 property revenue was $2,714 million.

- Verizon was 12%. About $325.7 million. Annualized $1,303 million.

- T was 14%. About $380 million. Annualized $1,502 million.

- Combined, they are about 26%. Annualized $2,823 million.

- AMT’s market cap was down $3,590 million. That’s 1.27x the total annual revenue from T and VZ.

T and VZ could reduce their rate of renewals and new leases, but they can’t simply terminate all their leases. Even if they could, it would cripple their network.

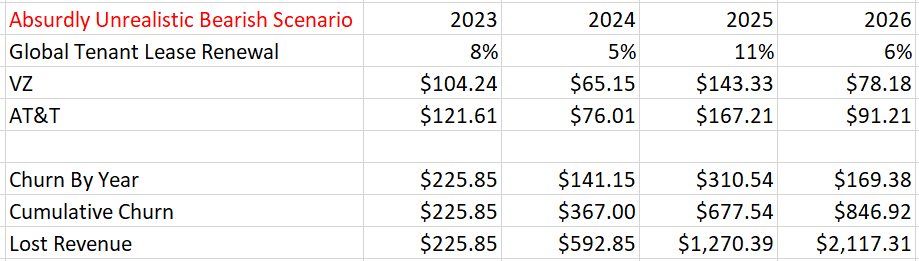

Regardless, we’re trying to examine worst-case scenarios. We can approximate when leases renew using the overall data for AMT’s portfolio:

- 2023: 8% of leases

- 2024: 5% of leases

- 2025: 11% of leases

- 2026: 6% of leases

- 2027+: 70% of leases

Assuming zero new leasing and zero renewals from T and VZ (a completely unrealistic bear scenario), we can create a hypothetical. I’m calling this one:

"An Absurdly Unrealistic Bearish Scenario."

Here’s the reduction in cash flows:

{kind=link}

Author Calculations

After four years in this laughably unrealistic scenario, AMT still hasn’t missed out on enough cash to offset the one-day drop in the share price.

Has this scenario helped the carriers? Not significantly.

Verizon’s Annual GAAP Expenses

Let’s use Verizon as our example. GAAP expenses are slowly but consistently trending higher.

The numbers:

- Annualized payment from VZ to AMT is $1.3 billion.

- Last year VZ’s total operating expenses were $106.4 billion.

- Excluding depreciation and amortization, the remaining expenses were $89.3 billion.

Therefore, rental payments to AMT are about 1.22% of VZ’s total operating expenses. Excluding depreciation and amortization, 1,45%.

The payments to CCI and SBAC are an even smaller percentage of Verizon’s operating expenses. Here’s the chart:

Author Calculations using data from 10-K and 10-Q filings

That’s the total payment. It's not the portion up for renewal. Tough luck, bears.

If all three tower REITs decided to give Verizon completely free rent effective immediately, it would reduce Verizon’s total operating expenses by about 2.69%.

I’ll buy the idea that the carriers may reduce their growth rate to conserve capital. Will it actually go negative? I find that doubtful.

Remember when Verizon spent $53 billion on spectrum ? That was slightly over two years ago. Did they buy it to just sit on it?

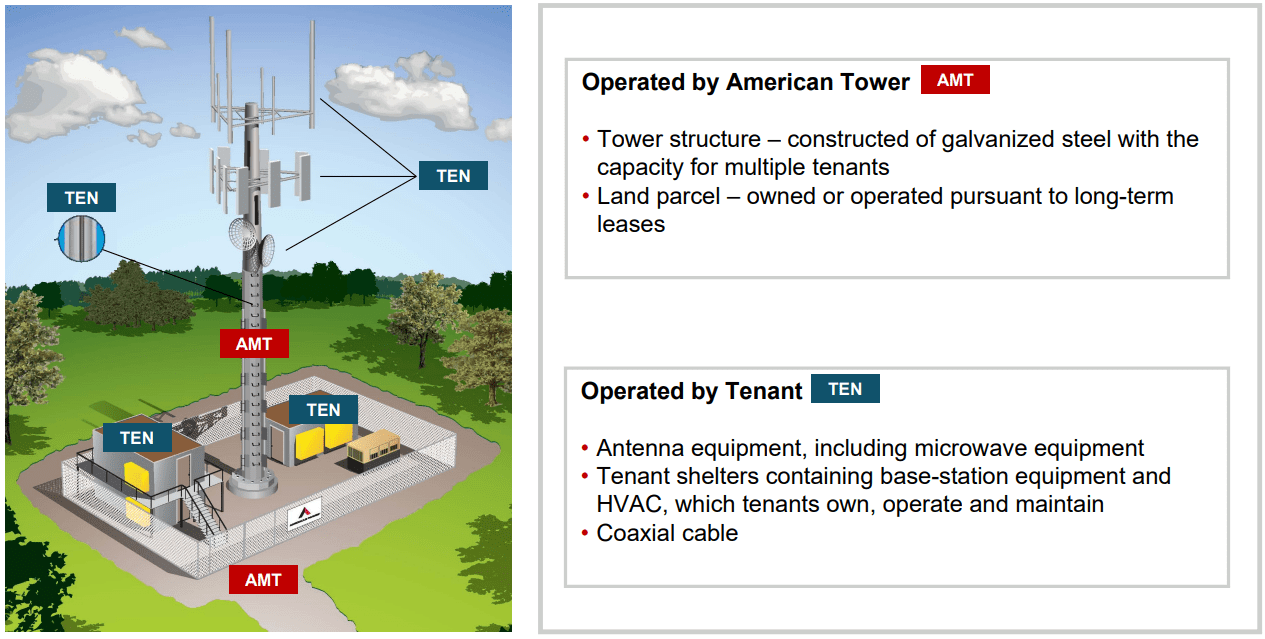

If they stop leasing the tower, where will they put all the physical equipment that was on the tower?

{kind=link}

American Tower

Are they really going to pull down (expensive) existing equipment and let even more of that spectrum go to waste? Would they store it in a warehouse? Dump it five feet away and claim they don’t own it anymore?

Assuming an average of 10% of leases expiring per year, Verizon could shave off $286 million from annualized operating expenses by letting more of its $53 billion spectrum purchase remain idle. They made bad decisions, but were any of them that bad?

At worst, this should be a reduction in the growth rate.

SBAC

SBAC is the smallest tower REIT. Biggest dip in percentage terms.

Guidance for 2023 called for $1.84 billion in domestic revenue.

The market cap declined by $1.91 billion.

That’s insanity. Bad event? Sure. A year of domestic revenue? No.

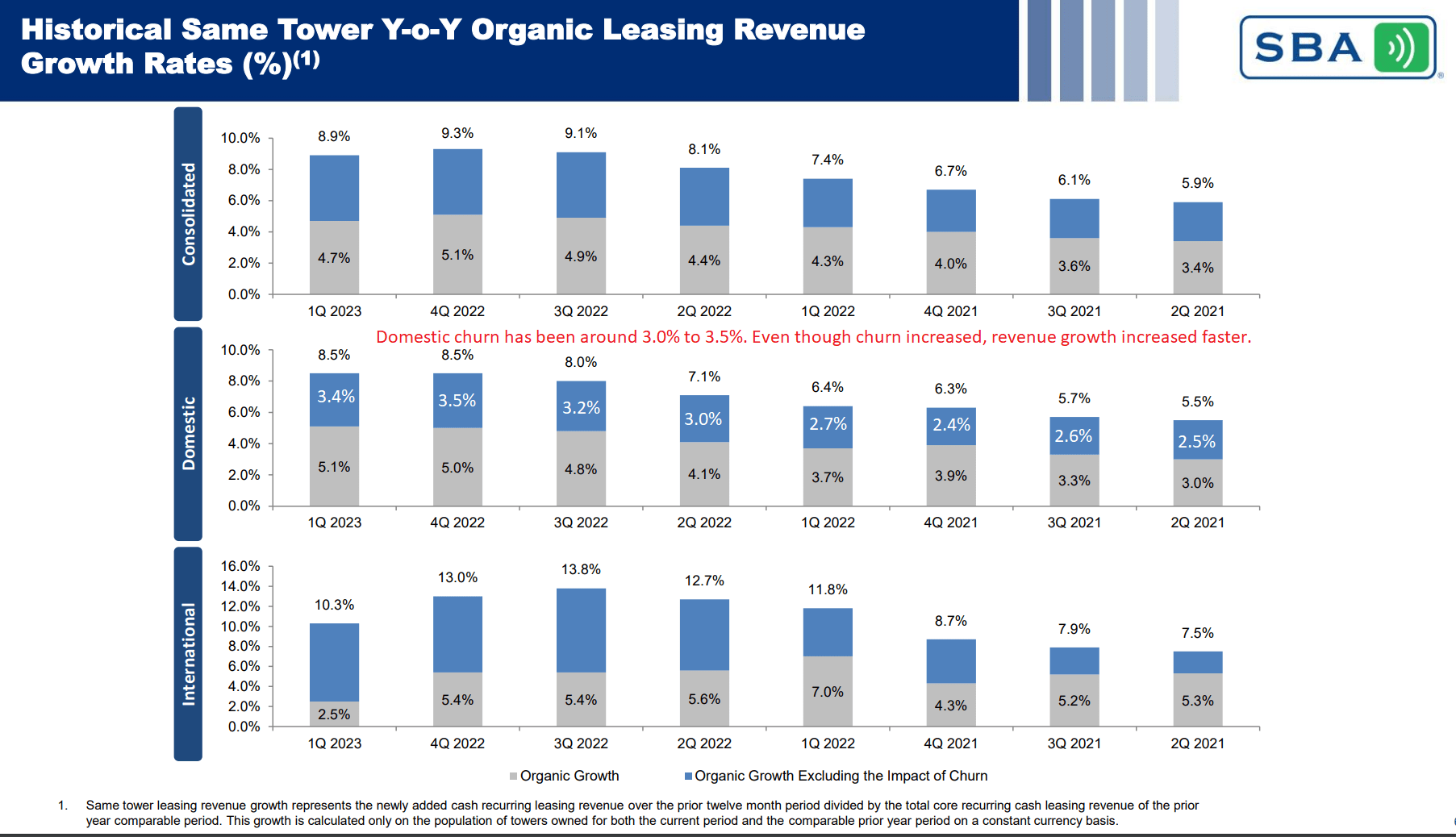

We can consider SBAC’s history in leasing assets:

{kind=link}

SBA Communications

Domestic churn lately has been in the 3.0% to 3.5% range.

Domestic organic growth after churn has been in the 4% to 5% range. That’s solid growth. However, it isn’t material to the operating expenses at any of the major U.S. carriers. Tower REIT prices have been in decline, but those fundamentals have still been good.

Historical Correlation

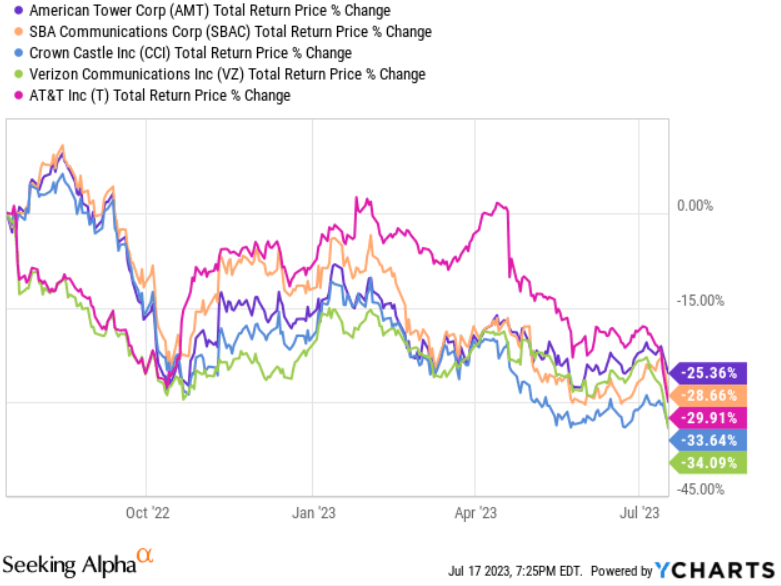

Over the last year, the carriers and cell tower REITs have endured a similar price decline:

{kind=link}

Seeking Alpha, YCharts

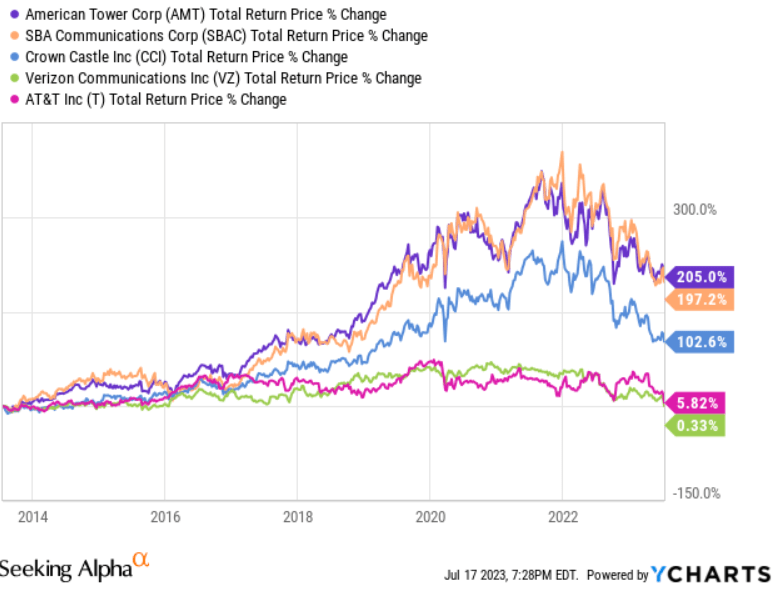

They had no connection around July of 2022, but they sure have been connected lately. What happens if we zoom out?

{kind=link}

Seeking Alpha, YCharts

The connection goes away. The cell tower REITs need the carriers to survive . Survival is not in doubt for T or VZ. Not at all.

What Are Lead-Sheathed Cables? (Story About Telecom Resumes)

The term “lead-sheathed” isn’t really clear enough. Is the lead in a sheath? Generally, no.

Is the (extremely toxic) lead serving as the sheath? Generally, yes.

In particular, we’re mostly talking about cables designed from the 1800s to the 1960s. At the time, there was relatively little knowledge about the magnitude of lead problems.

Because lead is the outermost layer, the lead is exposed. That’s bad.

Why Do They Still Exist?

Once it was widely accepted that lead was bad, it also was going to be expensive to clean it up. Doing a poor job could result in dumping more lead into the area. Doing a good job costs more money upfront.

Further, some of the cables are still in use today. Would it be difficult to serve those customers in an alternative way? Probably not. However, many of the cables are no longer in use.

Who Owns The Cables?

According to New Street Research (the analyst estimating $60 billion), the biggest owners are T, VZ, and Lumen.

However, ownership is in question. Large sections of lead-sheathed cables that are not in use produce zero revenue. If any maintenance is done on them, they would have negative cash flow. Further, any cleanup could potentially be expensive.

That begs the question:

If a company previously owned an asset and never registered a sale of that asset, do they still own it?

Alternatively, we could ask:

If a company abandons miles of lead-sheathed cables, can they make taxpayers eat the bill?

It’s no surprise then that Braden Allenby, former AT&T executive for environmental health and safety , told WSJ:

It was standard operating procedure to abandon those cables in place. We kept the discussion internal and informal. We didn’t try to quantify the problem or speak to the economics overall.

Conclusion

While it seems clear the cables represent a problem, I doubt that the carriers will pay for the lion’s share of the cleanup. What if they did? Verizon’s pre-tax income for 2022 was $28.2 billion. That’s about half of the theoretically projected total cost for the entire industry. Keep in mind those estimates might or might not be accurate. We use pre-tax because I assume they would be able to expense it, and Verizon is one of the corporations that actually pays taxes (over $6 billion for 2022).

For the cell tower REITs, it represents a potential headwind for growth rates. I find it extremely unlikely that the carriers would reduce their tower presence. It only makes sense that they might delay some expansions to avoid buying the equipment needed to utilize those towers.

As it stands, I find all three tower REITs very attractive. As of initial publication:

- AMT: $182.47

- CCI: $109.98

- SBAC: $225.76

As of submitting to the public side:

- AMT $184.71

- CCI: $107.51

- SBAC $222.86

After preparing this article for members, I increased my position in SBAC at $225.89. Shares were bouncing back, until CCI's weak guidance this morning (July 20, 2023) brought all tower REITs back down. However, CCI's weaker guidance still left site rental revenue unchanged. The reduction in guidance was related to services and interest expense.

My outlook on all three tower REITs (AMT, CCI, and SBAC) is set at Strong Buy. If the prices rallied hard, my rating would change. Ratings are based on valuation at the present time, so I will often be looking to buy REITs that have recently gone on sale. I believe this portion of the REIT market has been beaten down too much. It reflects the very short-term growth rates for the sector, rather than the longer-term growth rates. I do not have ratings on the carriers.

For further details see:

Tower REITs, Carriers And Lead-Sheathed Cables