PTEN - Transocean Q3 2022 Results: Great Performance Keeps This Rig Floating

Summary

- The management team at Transocean announced strong financial results during the latest quarter, with the company beating on the top and bottom lines.

- Backlog is now growing at an impressive rate and this looks set to continue so long as energy prices remain elevated.

- Add on the fact that shares of the firm look attractively-priced right now and it certainly makes for a viable investment prospect.

The long period of oil and natural gas price declines that we saw a few years ago resulted in extreme havoc in the oil and gas exploration and production space. One of the most devastated segments of the market was the offshore drilling niche because of the fact that operators are high-cost in nature, focus on expensive projects, and work on projects that can take a long time relative to other aspects of the industry in order to pay off. One player in the market that survived and is now showing nice signs of recovery thanks to a surge in oil and gas prices over the past year is Transocean ( RIG ). Although it's unlikely that the company will return back to what it was years ago, shares do look cheap and upside potential for shareholders could be quite appealing. And given the most recent data provided, it makes sense for investors to pay close attention to the company moving forward.

A fantastic quarter

The 2022 calendar year is so far stacking up to be a great year for shareholders of Transocean. So far, while the broader market is down, shares of the company are up by 47.1%. This has been driven by a number of factors, with the most recent wave of enthusiasm coming after management reported financial results covering the third quarter of the 2022 fiscal year. In response to this press release, shares of the company rose 15.2% on November 3rd alone before dipping down 2.4% one day later. This surge was driven by performance that exceeded analysts' expectations and was also attributable to other fundamental data that points to a brighter future for the enterprise.

{kind=link}

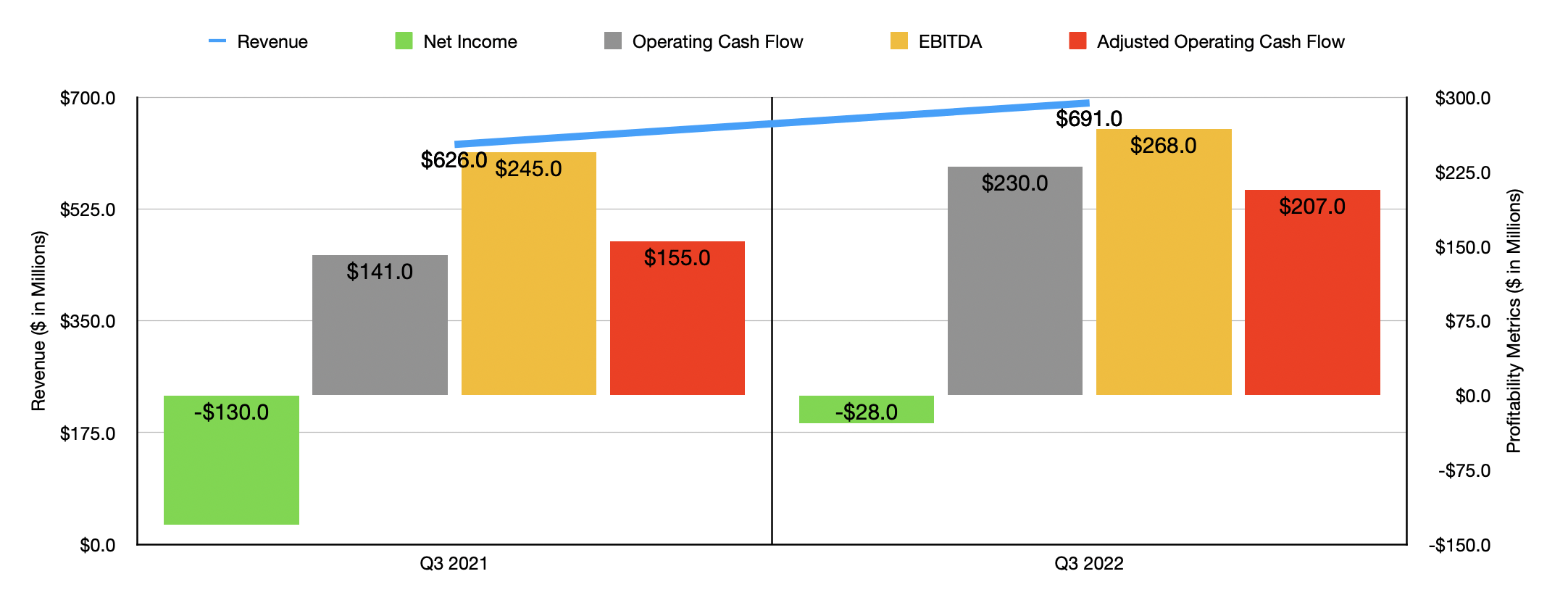

During the quarter, revenue with the company came in at $691 million. In addition to representing a 10.4% increase over the $626 million generated the same quarter last year, the company also beat analysts' expectations to the tune of $25.9 million. What really helped the company on this front was an increase in regularization. This number ultimately rose from 52.8% in the third quarter of the 2021 fiscal year to 59.4% at the same time this year. Even though demand for the company's rigs is rising, it is worth noting that some weakness exists in the form of average daily revenue. In the third quarter of last year, this metric was $367,100. Today, that number is $343,400.

On top of benefiting on the top line, the company also benefited on the bottom line. During the quarter, for instance, management reported a net loss of $28 million. Although any sort of loss is negative, it is far better than the $130 million net loss reported last year. On a per-share basis, the company generated a loss of $0.04. That represents a significant beat over the $0.18 per share loss that analysts were expecting. The increase in revenue obviously helped the company. The company also benefited though from a reduction in depreciation and amortization expense, as well as a reduction, relative to sales, in general and administrative costs. A $14 million reduction in interest expense also helped the company, as did a $7 million gain on the retirement of debt that the company achieved in the third quarter of this year. Other profitability metrics also came in stronger year over year. Operating cash flow, for instance, rose from $141 million last year to $230 million this year. If we adjust for changes in working capital, the improvement would have been from $155 million to $207 million. Meanwhile, the EBITDA of the company rose from $245 million to $268 million.

{kind=link}

The strength the company saw during the quarter from a revenue and profitability perspective was not the only good news. Management also reported robust backlog of nearly $7.3 billion. That stacks up favorably compared to the $6.2 billion reported in July and the $6.1 billion worth of backlog the company had in April. For those who follow the company closely, such an improvement in backlog would not have been a surprise though. In early August, for instance, the company announced a $915 million contract for the ultra-deepwater drillship Petrobras 10000. On that same day, the company also landed a $321 million contract for its ultra-deepwater drillship called the Deepwater Conqueror. And in early September, the firm landed a $181 million contract for another one of its rigs.

Transocean

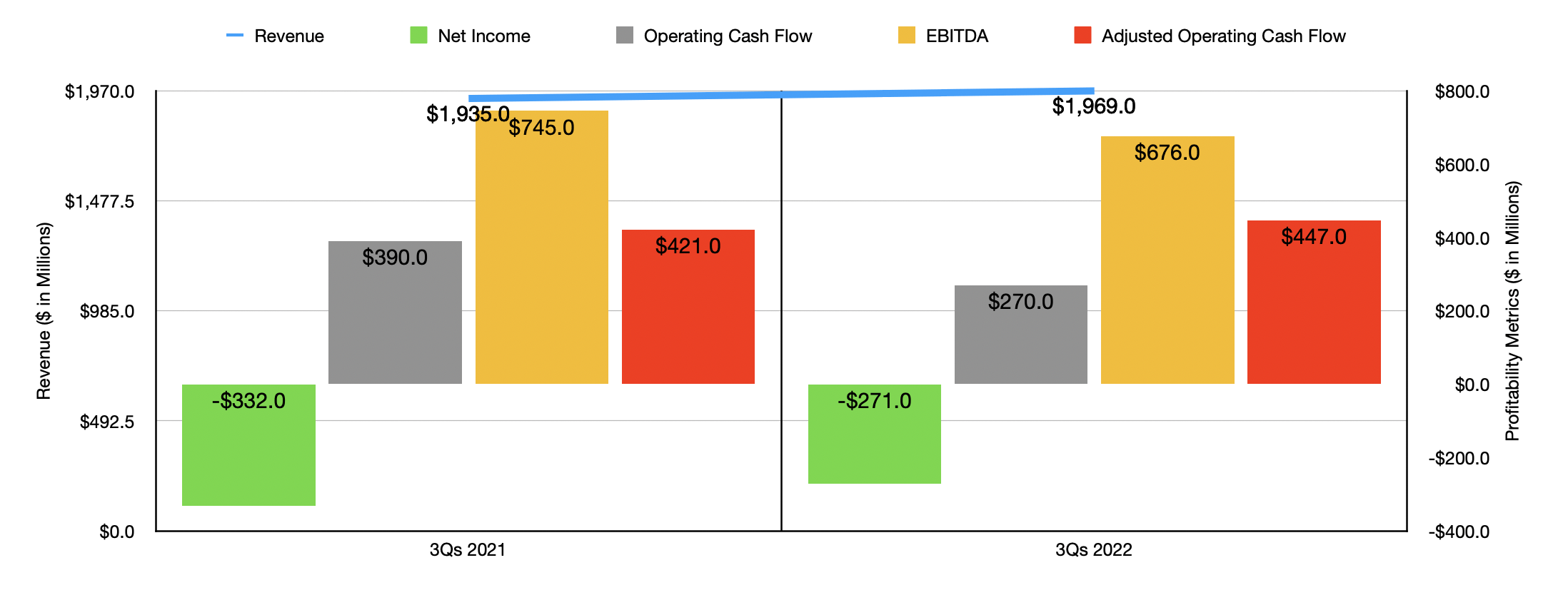

Despite the strong third quarter, there is still some weakness for the year as a whole. Yes, revenue in the first three quarters of 2022 has come out to $1.97 billion, an increase over the $1.94 billion reported the same time last year. In addition, the company's net loss has declined from $332 million to $271 million. But operating cash flow has dropped from $390 million to $270 million. Of course, on an adjusted basis, we did see an improvement from $421 million to $447 million. But during that same window of time, EBITDA for the company shrink from $745 million to $676 million.

{kind=link}

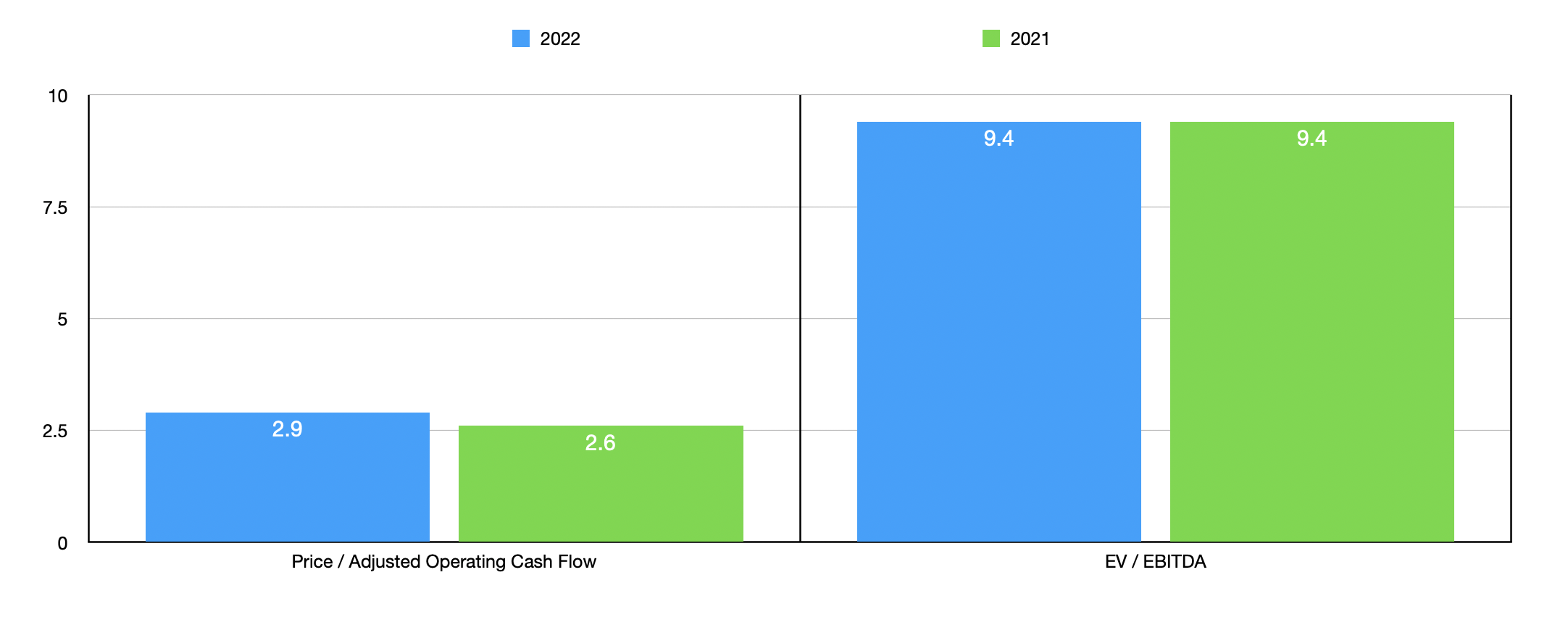

It's really difficult to know what to expect for the rest of the 2022 fiscal year. But if we annualize results experienced so far, we can anticipate adjusted operating cash flow of $571 million and EBITDA of $903 million. Based on these figures, the company is trading at a forward price to adjusted operating cash flow multiple of 2.9 and at a forward EV to EBITDA multiple of 9.4. To put this in perspective, using the data from 2021, these multiples would be 2.6 and 9.4, respectively. As part of my analysis, I did look at some other offshore drillers. Unfortunately, most of them had negative cash flows and EBITDA. Of the two that were positive, one was trading at a price to operating cash flow multiple of 12.8. The other firm did not have a positive price to operating cash flow multiple. When it comes to the EV to EBITDA approach, the multiples ranged between 9.5 and 65.8. Clearly, Transocean was cheaper than its relevant peers.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Transocean |

| 2.9 |

| 9.4 |

| Borr Drilling Ltd. ( BORR ) |

| N/A |

| 65.4 |

| Patterson-UTI Energy ( PTEN ) |

| 12.8 |

| 9.5 |

Takeaway

Fundamentally speaking, Transocean seems to be recovering nicely from the years of pain it experienced. This is not to say that everything will be sunshine and rainbows moving forward. But right now, backlog is growing, revenue is climbing, and cash flows are showing some signs of strength. Given how cheap shares are now, I could understand investors gravitating toward them. But it is also important to keep in mind that if energy prices tank from here, Transocean will still be one of the first to take the hardest hit. Because of this, I would be cautious in the long run. But for now, I think we have a complete enough picture for me to comfortably rate the business a ‘buy’.

For further details see:

Transocean Q3 2022 Results: Great Performance Keeps This Rig Floating