CA - Trican Well Service: Best-In-Class Balance Sheet

2023-05-05 11:30:00 ET

Summary

- Trican Well Service Ltd. is a large oilfields services provider in Canada, focusing on pressure pumping and fracking.

- The company has a net cash position, which should help it to navigate through choppy waters.

- Although Trican has been an aggressive buyer of its own shares, it recently announced a maiden dividend.

- The current 5.3% will be "stable and very sustainable" over the next few years, according to Trican Well Service management.

Introduction

Trican Well Service Ltd. ( TCW:CA , TOLWF ) is a Canada-based oilfield services provided focusing on pressure pumping and fracturing activities . Most unconventional oil and gas wells are currently drilled using horizontal holes, and those holes need more fracking, and that’s where Trican comes in. Needless to say, the company’s financial performance is closely correlated to the activity level in the Canadian oil fields, and although a lot of the oilfield services companies run into balance sheet issues during a period of weaker oil prices, Trican’s balance sheet is pretty strong. This helps the company to navigate through weaker periods.

2022 was a good year

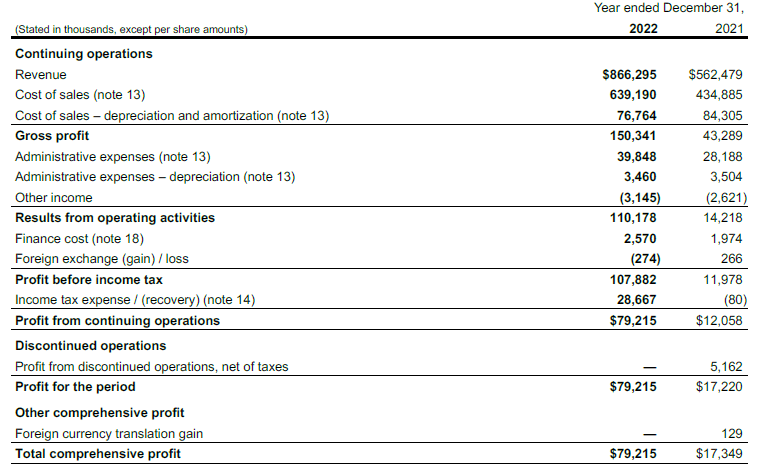

As 2022 was a good year for oil and the oil price, Trican also had a good year. The total revenue in 2022 came in at almost C$867M which resulted in a C$150M gross profit. The image of the income statement below shows how important the additional revenue was compared to FY 2021. The C$304M in additional revenue generated about C$107M in additional gross profit, and about C$96M in additional operating income, an increase of almost 600%.

{kind=link}

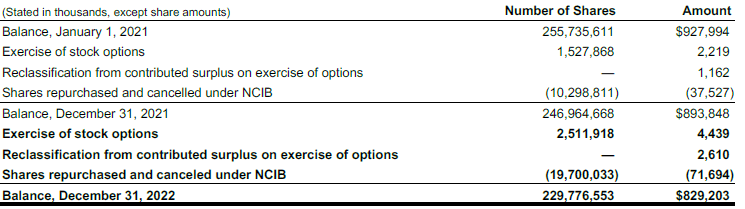

Needless to say this also had a very positive impact on the bottom line of Trican. The pre-tax income jumped from C$12M to C$108M (despite recording a C$2.6M finance cost) and after deducting the relevant amount of taxes the net income was C$79M. This represented an EPS of C$0.33 based on the weighted average share count of 241.4M shares but keep in mind the company ended the year with a net share count of just 230M shares after it spent C$69M on repurchasing 19.7M shares (for an average price of C$3.50). This more than fully compensated the dilution upon the exercise of stock options which increased the share count by 2.5M shares (and resulted in a cash inflow of C$4.4M).

{kind=link}

If we would use the year-end share count rather than the weighted average, the EPS would have exceeded C$0.34.

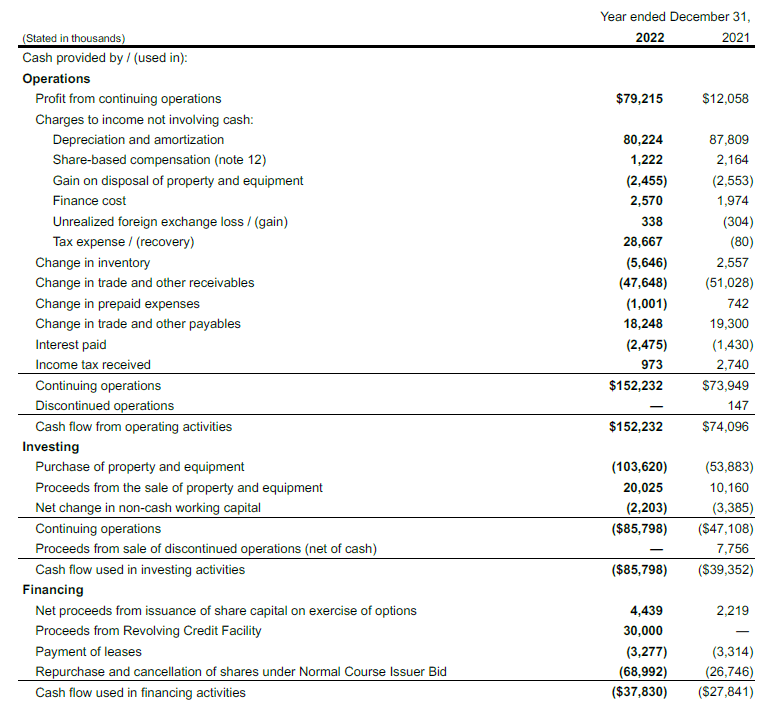

The cash flow statements are also important as oilfield services companies have the financial capacity and flexibility to finetune their fleet with the cash inflow. It does happen quite often to see companies in this sector ‘scaling’ their capital expenditures. During tougher times in the oil sector, the demand for services is lower and companies have to spend less on capex to satisfy the needs of the customers which helps the service providers to conserve cash as well. Trican is no exception. In FY 2021, the total amount of depreciation and amortization expenses came in at C$88M but the company spent just C$57M on capex and lease payments.

This was reversed in 2022. As you can see below, Trican took advantage of a good year with strong cash flows to increase its capex and it spent C$104M on capital expenditures and C$3M on lease payments for a total investment of C$107M which is more than 30% higher than the C$80.2M in recorded depreciation and amortization expenses.

{kind=link}

This was easily funded by the incoming cash flows. As you can see above, the total reported operating cash flow was C$152.2M, but this includes a C$36M net investment in the working capital position. On a pre-WC basis, the adjusted operating cash flow (including the lease payments) was C$185M which means there was about C$81M of net free cash flow after making the C$104M in capex payments.

Keep in mind this includes the complete deferral of the income taxes for FY 2022. The entire tax bill of C$28.7M was deferred and the company received an additional C$1M in tax repayments as Trican was able to apply historical losses against the FY 2022 income. If we would include the normalized tax payments – which is only fair to fully understand Trican’s performance), the underlying free cash flow would have been approximately C$52M or C$0.23 per share. That’s still fine considering the company overspent on capex (and lease payments) to the tune of C$27M or almost 12 cents per share.

One of Trican’s biggest assets is its balance sheet. As of the end of 2022, Trican had a cash position of C$58M and gross debt totaling C$30M (excluding the C$13M lease liabilities) for a net cash level of approximately C$28M or 12 cents per share. That’s a very comfortable position for a company that will per definition be exposed to the cyclical nature of the oil sector.

And while Trican has sworn by a share repurchase program over the past half decade (it has repurchased in excess of 130M shares, or about 38% of the share count since 2017), the company recently announced a maiden quarterly dividend. At the end of Q1, Trican paid a cash dividend of C$0.04 per share, which works out to C$0.16 per year for a dividend yield of approximately 5%. The total cash out flow related to the dividend will be approximately C$37M per year and Trican should be able to cover this. On the Q4 conference call , the management indicated the dividend will be "stable and very sustainable over the next few years."

Investment thesis

That being said, as Trican’s management has been pretty conservative in the past and runs a very conservative balance sheet as well, I don’t think the dividend will be set in stone. I have no doubt the Trican management will reduce the payout when and where necessary to protect the financial health of the company. And that certainly is an approach I support: a dividend is not a "right," it is just a mechanism for a company to share profits with its shareholders. If there is a weak financial year, it only makes sense for the dividend to be adjusted as well.

I currently have no position in Trican Well Service Ltd., as I wasn’t very keen on oilfield services in general due to the cyclical nature of the business and the lack of hedging possibilities (at least oil and gas producers can actually hedge a portion of their production to increase price visibility). But as Trican Well Service Ltd. has a very conservative balance sheet with no net debt, it could be one of the "safer" ideas in the oilfield services industry and its performance should be more balanced than some of its competitors that live by the "boom and bust" cycle.

For further details see:

Trican Well Service: Best-In-Class Balance Sheet