CA - Tricon Residential: Expected Growth Consistent With Housing Recovery Theme And Scale Expansion

2023-05-25 11:20:57 ET

Summary

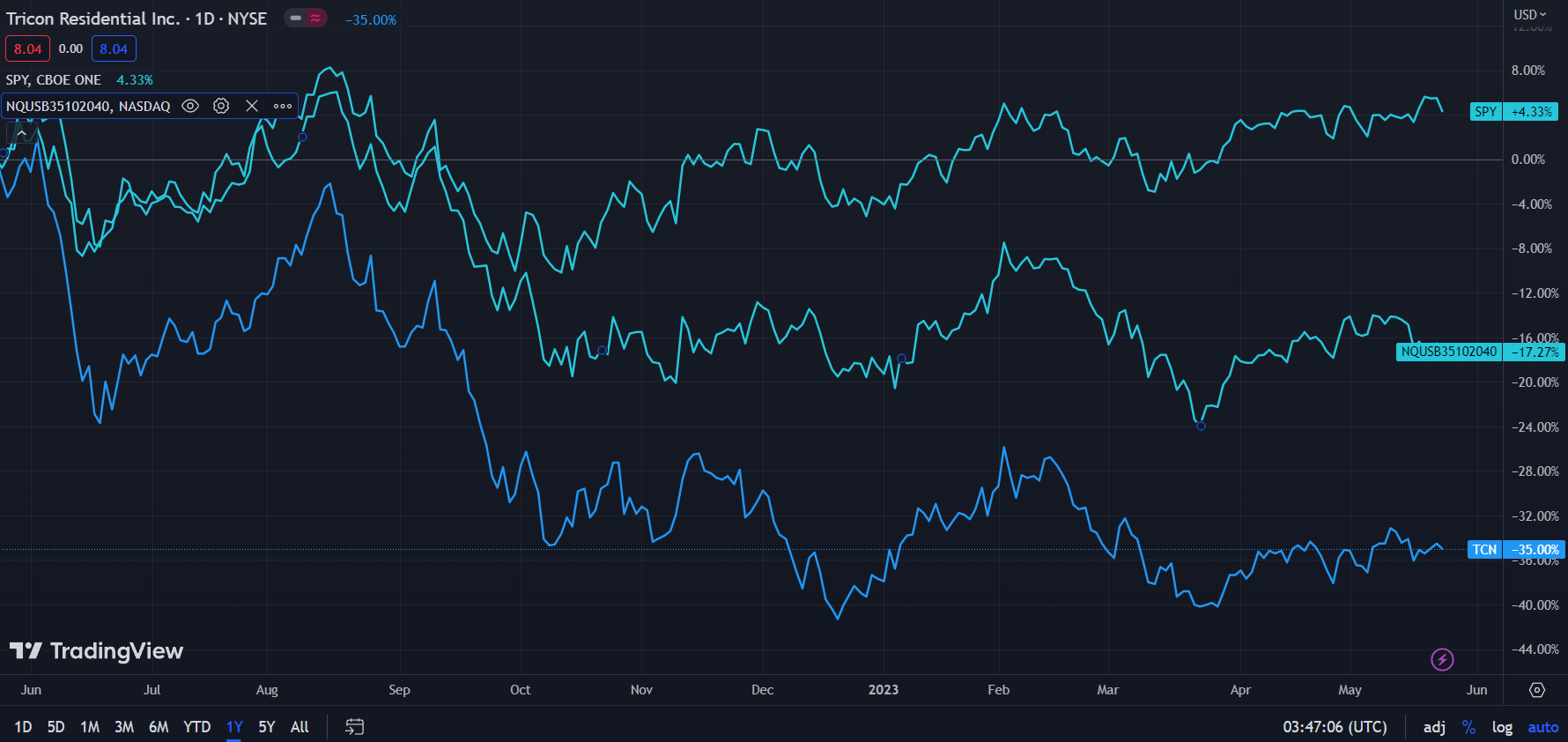

- Over the past year, Tricon (-35.00%) has trailed both the general market (SPY: +4.33%) and the NASDAQ US Benchmark Residential REITS Index (-17.27%).

- This reflects the inverse convexity between interest rate hikes and residential property values and subsequent investor anxieties about Tricon.

- However, the company has seen 105.12% growth in free cash flow and a 56.90% increase in revenues for the past year, running inversely to share price action.

- To further boost scale growth, the company has expanded organically- on a geographic basis, for instance- and inorganically, via M&A and partnerships.

- Due to this operational excellence, a general undervaluation, and a disciplined capital deployment strategy, I rate Tricon a 'buy.'

Tricon Residential ( TCN ) is a Toronto-based North American real estate company, with >36,000 single-family and multi-family rental properties across Canada and the US. The company maintains $12bn of real estate assets, with 98% of its asset value derived from US operations and 2% from Canada.

{kind=link}

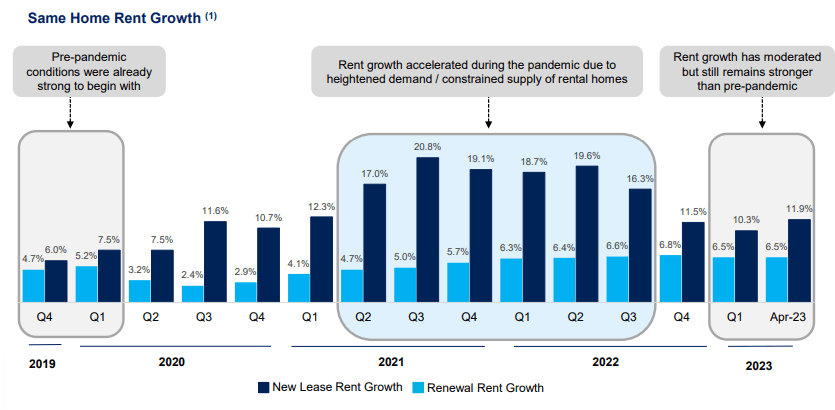

The REIT has demonstrated considerable resilience through the headwinds of COVID-19, inflationary pressures, rising interest rates, and so on, with strong pre-pandemic fundamentals carrying on into rental and retention growth across the past three years.

Introduction

Tricon operates in the dual business of real estate investment and operation; to best support scale growth and optimize customer experiences, Tricon has employed a sixfold strategy; the firm puts a premium on developing corporate culture, segueing into growth, it aims to expand into new geographic and demographic markets, with a focus on the Sun-Belt, increase accessibility through scalable technology platforms, deliver growth to investors, maintain industry-leading operating metrics, and support value creation opportunities through adjacent businesses.

{kind=link}

Tricon has demonstrated its commitment to these goals over the past few years, with $1.4bn, and $1.3bn acquisitions of Silver Bay Realty Trust and a US Sun Belt multi-family portfolio alongside multi-billion dollar partnerships and joint ventures to expand the company's Sun Belt, Build-to-Rent, and geographic and vertical presences.

Valuation & Financials

General Overview

In the TTM period, Tricon- down 35.00%- has experienced poorer price action than both the broad market, represented by the S&P 500 ( SPY )- up 4.33%- and the NASDAQ US Benchmark Residential REITS Index- down 17.27%.

{kind=link}

This price action reflects investor concerns about residential asset values in light of rising interest rates as well as scale growth reductions with inflationary pressures and supply chain constraints. Additionally, Tricon maintains a relatively high debt/equity of 1.51, accelerating worries about interest rate impact- though, Tricon generates more than enough free cash flow to cover its liability obligations.

Comparable Companies

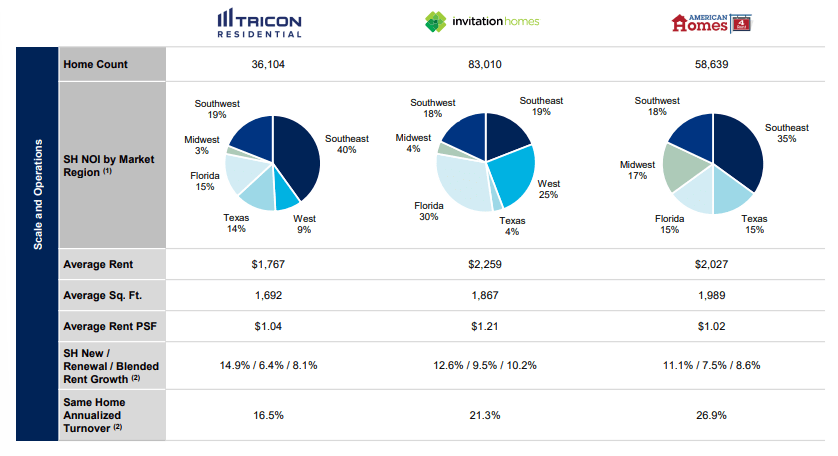

The residential housing market is highly fragmented, with market share chiefly held by individual homeowners or small-scale individual real estate investors. However, among residential REIT firms, Tricon can count peer companies with similar scale and comparability to be Invitation Homes ( INVH ), the largest owner of single-family rental homes in the US, American Homes 4 Rent ( AMH ), and Sun Communities ( SUI ), a firm with a larger focus on manufactured housing communities, RV communities, and marinas.

barchart.com

As demonstrated above, Tricon has experienced the poorest yearly growth and second-poorest quarterly growth, a trend which reflects the anxieties of investors not only regarding residential home portfolios, but Tricon's significant debt obligations. That said, Tricon's $249.74mn in 2022 free cash flow means the firm is more than capable of deleveraging adequately.

On a pure multiples basis, Tricon rejects market sentiment, with the lowest trailing and forward P/E ratios, the lowest P/CF, and the lowest P/B ratios. Moreover, the firm has recorded the best ROE and ROA among peers, enabling Tricon to maintain a solid dividend at a significantly lower payout ratio than the given peer group.

{kind=link}

And Tricon records industry-leading metrics while maintaining competitive rent PSF and with minimal annualized turnover, manifesting Tricon's dual ability to satisfy shareholder and consumer demands.

Valuation

According to my discounted cash flow valuation, at its base case, Tricon is undervalued by 7%, with a fair market price of $8.49, up from $7.86 today.

My DCF model assumes a discount rate of 10%, in line with the higher cost of debt and equity, with relatively high implied volatility- thus leading to a higher equity risk premium- and debt levels. I additionally incorporate a conservative growth metric into my valuation, projecting non-perpetual 5-year revenue growth of 4%, much lower than historic growth levels.

{kind=link}

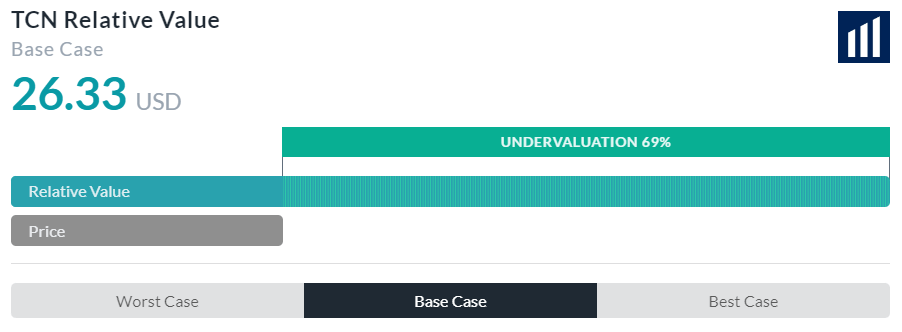

AlphaSpread's multiples-based relative valuation tool, at its base case, calculates the fair value of Tricon to be $26.33, a 69% undervaluation from today.

However, AlphaSpread's model fails to account for Tricon's elevated debt levels and thus misconstrues the true value of Tricon's stock.

Therefore, using a weighted average skewed towards my DCF analysis, the fair value of Tricon should be $9.55, with the stock currently undervalued by 17%.

Combined Organic & Inorganic Growth Support Recovery Theme

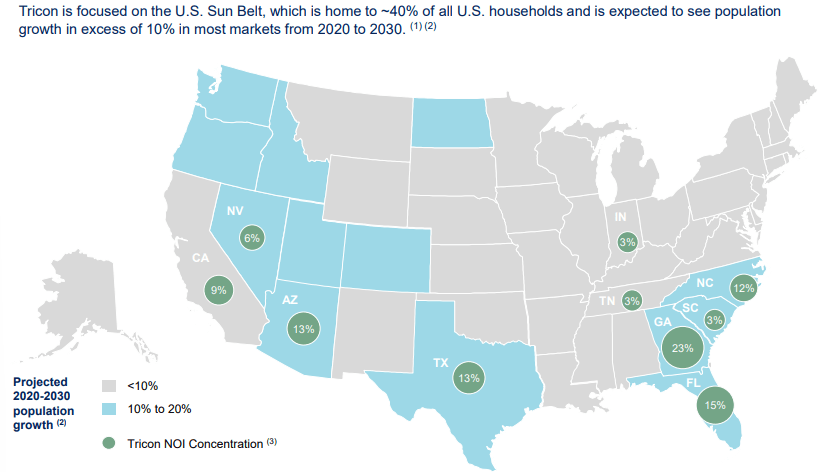

The Tricon growth story continues to be predicated upon the three-fold strategy of geographic growth, disciplined portfolio management, and fulfilling consumer engagement. For instance, Tricon is investing significantly in the US Sun Belt regions, which includes ~40% of all US homes and is expected to see upwards of 10% in population growth till the end of the decade.

{kind=link}

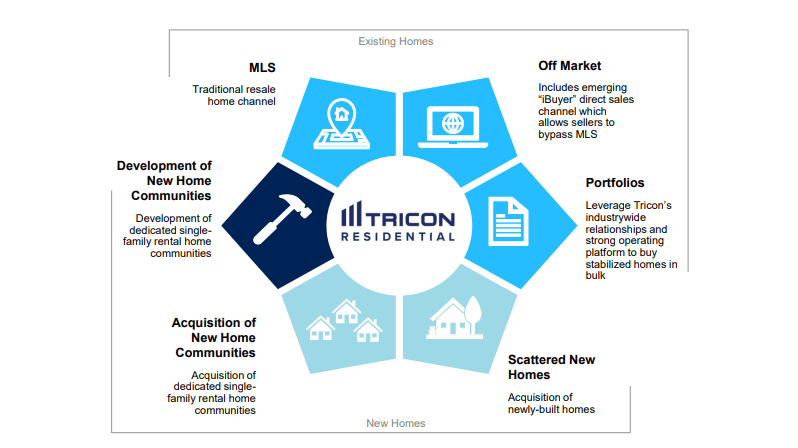

Beyond geographic scale growth, Tricon aims to accelerate portfolio growth and efficacy through a combination of accessibility expansion via traditional and novel sales channels, contribution towards the actual development of new home communities- indicating a willingness to engage in backwards integration, and a diverse mix between scattered homes and home communities.

{kind=link}

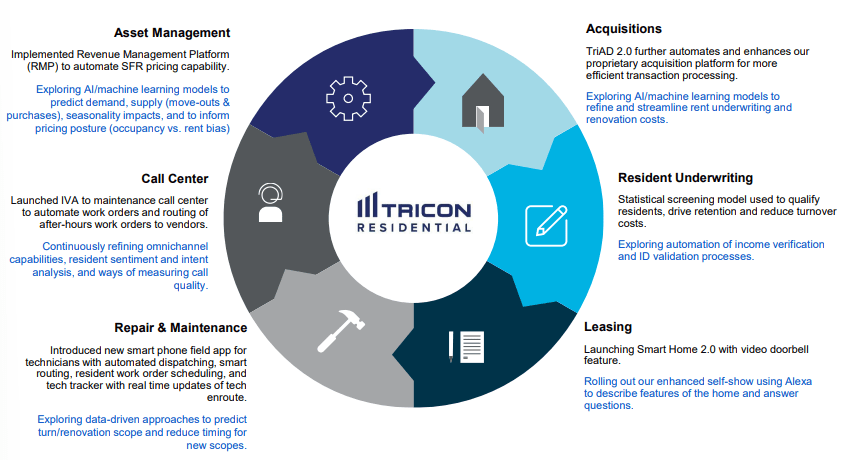

And to further support the accessibility motif and support superior profitability, Tricon has accelerated its technology deployment strategy, enabling superior revenue management to automate SFR pricing, establishing digital and calls-based service centres to support consumer engagement, developing better product quality with smart home, and ultimately support cash flow generation.

{kind=link}

Wall Street Consensus

Analysts echo my positive outlook on Tricon's stock, projecting an average 1Y price increase of 23.59% to a price of $9.94.

{kind=link}

Even at the minimum price forecasted, analysts predict a 5.72% increase to $8.50, indicating that analysts also believe that the stock has unfairly been punished for macro headwinds, which it has successfully navigated.

Risks & Challenges

Poor Debt Management

With some of the highest debt levels among peers, Tricon must divert significant cash flow towards deleveraging which could otherwise be returned to shareholders, used for acquisition, or reinvested into the core business. Moreover, high debt levels indicate high levels of risk given increased interest rates or general declines in free cash flow.

Asset Value Declines

At the same level, either through interest rate increases or through general market movement, significant declines in asset value can result in poorer investor sentiment, and increase the cost of equity while simultaneously reducing the ability of Tricon to take on debt. This would ultimately reduce the ability of the firm to generate additional cash flows and return value to shareholders.

Increasing Competitive Intensity

Though the industry remains highly fragmented, the increase in SFR and other property management REITs will increase levels of price competition and reduce Tricon's ability to remain profitable. Additionally, it may drive up non-investor-owned asset prices at an increasing rate and reduce Tricon's ability to scale further.

Conclusion

In the short term, I expect Tricon to revert to fair value and continue to achieve growth in line with macro residential real estate recovery.

In the long term, I project Tricon's dual consumer and shareholder orientation to yield organic growth alongside bullish projects in the Sun Belt and beyond.

For further details see:

Tricon Residential: Expected Growth Consistent With Housing Recovery Theme And Scale Expansion