TRIN - Trinity Capital And TriplePoint Venture: 2 BDCs With Potential

2023-03-20 13:58:43 ET

Summary

- Trinity Capital Inc. and TriplePoint Venture Growth recently released their latest earnings; these two have a lot of similarities with each other currently.

- Net asset value per share for each fell, but these were expected as they dealt with some pains in their portfolios.

- This is reflective of the current environment, but so are the higher interest rates that have been propelling their NII generation.

- With the latest banking failures, we are reminded just how risky business development companies can be.

Written by Nick Ackerman. A version of this article was originally published to members of Cash Builder Opportunities on March 6th, 2023.

Trinity Capital Inc. ( TRIN ) and TriplePoint Venture Growth ( TPVG ) are two venture capital-focused business development companies (BDCs). BDCs generally invest in loans, equipment or even equity of small and mid-sized businesses that can't get traditional financing elsewhere. Due to sizes, these are generally more financially sensitive companies that are susceptible to economic conditions.

When things start to get tighter financially, as they are now with the Fed increasing interest rates, we can start to see some things break. Therefore, it isn't entirely alarming that both of these BDCs had recently experienced some sizeable setbacks. The goal is to keep these setbacks minimal. With these two BDCs, they can be particularly sensitive, as they often focus on ventures that have their own unique challenges, which can include being unprofitable or very limited in profits.

With the latest bank failures, we see just how volatile these sorts of investments can react. Adding high amounts of leverage is really going to juice the upside return potential, but also drives moves to the downside.

While those are the main risks, there is much to like about these BDCs. They are providing growing net investment income due to those interest rate increases. At the same time, both TRIN and TPVG have various degrees of fixed-rate financing, which is typical for BDCs. So they benefit from rising rates due to most of their interest costs being fixed and, simultaneously, their underlying loans being based on floating rates.

Additionally, both are getting over their latest portfolio mishaps. The question going forward is whether these are the canary in the coal mine or just simply missteps that can be looked over. That question can only be answered with time, but both look promising for different reasons. With both reporting earnings lately, it's time for an update on each.

Trinity Capital

TRIN is an internally managed BDC focused on the growth stage of the lifecycle stage of a company. They have loans and equipment financing as their focus.

TRIN Target Investments (Trinity Capital)

While their public life has been relatively short, they have a long history when they were private funds.

On January 16, 2020, through a series of transactions (the “Formation Transactions”), we acquired Trinity Capital Investment, LLC, Trinity Capital Fund II, L.P. (“Fund II”), Trinity Capital Fund III, L.P., Trinity Capital Fund IV, L.P. and Trinity Sidecar Income Fund, L.P. (collectively, the “Legacy Funds”) and all of their respective assets, including their respective investment portfolios (the “Legacy Portfolio”), as well as Trinity Capital Holdings, LLC (“Trinity Capital Holdings”), a holding company whose subsidiaries managed and/or had the right to receive fees from certain of the Legacy Funds. We used a portion of the proceeds from the Private Offerings to complete these transactions.

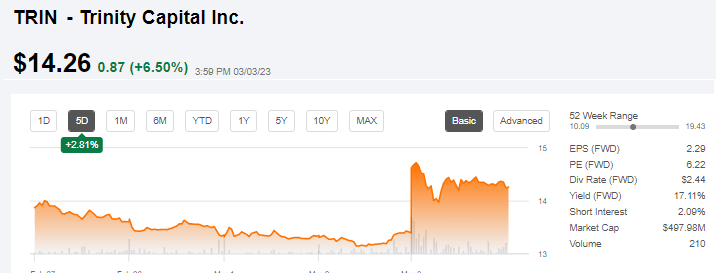

TRIN is the BDC I own currently, and I'm looking to add more when it's opportunistic to do so. At this time, after their earnings, shares jumped significantly. At one point, shares were up over 10% on the day the earnings were release.

{kind=link}

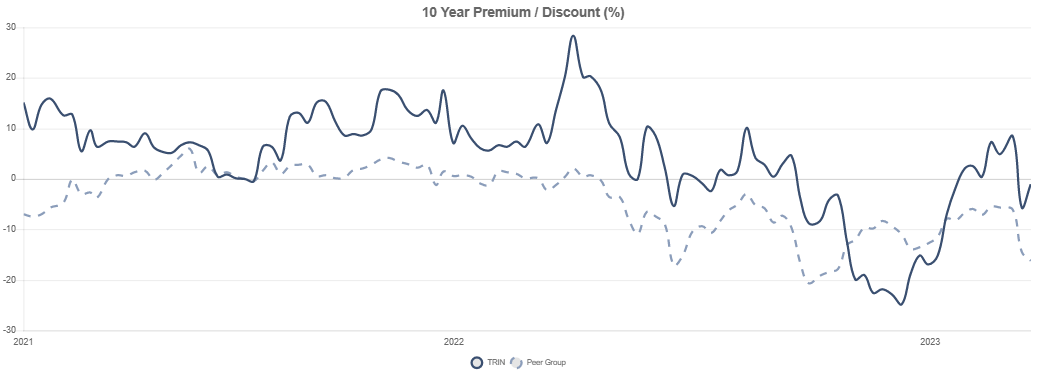

This is both a positive and a negative. Positive for those that might already own shares, but it's also pushed us back up into a premium to the NAV. Their last reported NAV was $13.15. Internally managed BDCs tend to trade at premiums.

That being said, the volatility brought on by the SVB Financial Group (SIVB) and Signature Bank (SBNY) failures produced explosive moves for TRIN. Shares are currently sitting at a slight discount.

{kind=link}

It should also be noted that TRIN has shown that they are aggressively trying to grow its operations. With a focus on growth, secondary offerings become one of the main tools. If done at a premium, it is accretive to NAV - so it's definitely beneficial, but in the short term, it generally causes price volatility. So we can enjoy the higher price now, but that might not last for too long if they pull a secondary.

Other examples of them being more aggressive with growth levers include receiving exemptive relief from the SEC for their registered investment adviser business. They also created a joint venture. They believe that this will positively contribute to returns starting immediately this year. I won't remark on these two topics specifically yet, as we don't have much information to go off of for now. They are in the early stages of getting set up, but the management team suggests they are promising developments.

We continued our strategic approach to growth with the recent announcements regarding our joint venture and the exemptive relief for our RIA by the SEC. We believe these two investment vehicles will provide accretive returns to our shareholders beginning in 2023.

That latest NAV dropped from $13.74 in the prior quarter. I noted that the NAV could hit $13.15, assuming a complete write-off of Core Scientific ( OTCPK:CORZQ ). That was one of the main portfolio pain positions, as well as FemTec Health.

Their next earnings are expected to be on March 2nd, 2023. At that time, we should get more color on the whole situation and the exact impact on the BDC and, more specifically, the NAV. My estimate is that NAV could be around $13.15, assuming a complete write-off of CORZ equipment financing. That would be a decline from $13.74, which should mean we are still looking at a discount to the NAV.

While I nailed the NAV estimate, they hadn't written off the equipment financing completely. They brought the fair value level down to $8.24 million at the end of December 31st, 2022. They believe that's exactly what it is worth and what they could sell the equipment for that day. However, since then, Bitcoin's price has increased. Being that it's crypto mining equipment, that should be beneficial to the valuation.

All that being said, other valuations were dropping here too, but for the most part, it was completely expected due to the current environment. However, those two positions primarily were the main driver of the decline in NAV, as noted in their earnings call .

...realized losses recognized during the fourth quarter, approximately 75% of the unrealized depreciation was related to two portfolio companies, FemTec Health and Core Scientific, previously identified as troubled credits in prior quarters.

One area that's also likely to cause uncertainty or concern amongst investors was the decline in the portfolio quality that they presented. In the grand scheme of things, it went from a weighted average risk rating of 3 down to 2.8 year-over-year. However, investors might note that there was a meaningful drop from "very strong performance" and "strong performance."

{kind=link}

That's not something we want to see generally, but once again, it reflects the territory we are in. That's one of immense uncertainty as the Fed raises interest rates. Additionally, that still leaves the majority of the portfolio at "performing."

Q4 NII came to $0.62 or a diluted NII of $0.57. Either way, this was well above the current quarterly distribution of $0.46 that they had paid. They had also been paying specials over the last year every quarter in the amount of $0.15 due to gains they realized in investments previously. Despite those supplemental payments, spillover stood at $1.73.

Looking at the NII, I believe we can continue to expect further dividend increases. I'd also guess that we could see supplemental again this year - potentially every quarter again. While that's speculative, we'll find out more when they announce the next dividend later this month.

(Author Note: It turns out since the original publication that, they did raise the regular to $0.47 but have not committed to any specials/supplementals. I wanted to leave the above paragraph in for transparency that I was wrong. I think that's smart of management, given the environment).

TRIN Dividend Growth (Trinity Capital)

At the end of 2022, they had nearly 70% of their outstanding borrowings based on fixed rates. At the same time, they had 67.5% of their portfolio in floating rate investments.

TRIN Fixed/Floating Debt Investments (Trinity Capital)

TriplePoint Venture Growth BDC Corp

TPVG is likely to be more familiar with more investors, as it has a long public history. That's one place where TPVG might have the upper hand against TRIN. While TRIN's history is more opaque due to the consolidation of several different private funds, TPVG's history is more well-known. That means we know they've at least survived for longer with relatively strong results.

TPVG is different from TRIN in that they are externally managed. However, they're also similar in that they are investing in the growth stages of companies. TPVG invests primarily in debt investments but also includes equity and warrants in fairly meaningful amounts.

{kind=link}

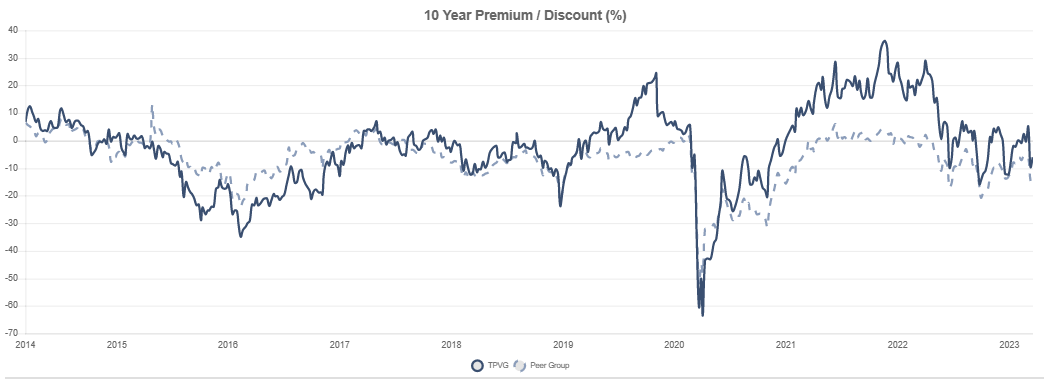

Despite being externally managed, that hasn't stopped TPVG from trading at premiums to its NAV per share. We actually aren't even near the high levels of premiums we saw through 2021 and 2022. Even pre-COVID, TPVG commanded a premium on occasion. I believe that makes it a consideration at this time. Similar to TRIN, we've seen a wild ride.

{kind=link}

The pain position for TPVG was Medly Health declaring bankruptcy. However, they've written that position down and are moving on. Additionally, they reaffirm the main point I try to present with BDCs, non-accruals and bankruptcies aren't anomalies that happen; they aren't an "if," they are "when" events.

I'd like to provide a short footnote on former portfolio company, Medly, which is now behind us and with last year's event. While all venture lenders deal with credit challenges and market downturns, it's a hardwired part of the business and not a question as to if but when.

This one was a bit tougher to spot because there were some financial misreporting that they clearly wouldn't have been able to help if they were being lied to.

As stated in the bankruptcy filings, this was precipitated by the loss of anticipated financing and the discovery of certain operational, financial and accounting irregularities and improper activities conducted by former employees, including the original founders. Including the full write-off of Medly last year...

While I don't own TPVG, I sold puts shortly after the Medly Health news as a way to start a position potentially. Those puts now look set to expire worthless this month as the shares recovered sharply.

In total, for the year-end 2022 , they recognized net realized losses of $46 million across Medly Health, Pencil and Pixel.

They reported a NAV per share of $11.88 in the last quarter. That was above my estimate of $11.77 NAV that they would report, but a pleasant surprise doesn't hurt. Still, that was a decline from the previous quarter of $12.69 and is only expected again due to the current environment.

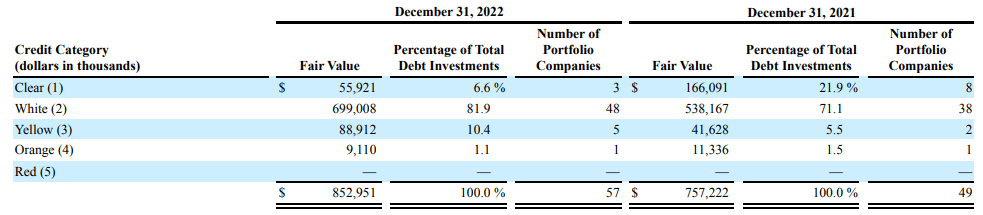

With that, it comes with little surprise that we've seen a downgrade of the quality in their ratings for their portfolio as well. Similar to TRIN, we've seen a material drop for the higher rating grades. Although still relatively strong overall, the portfolio rating went from 1.87 to 2.06.

{kind=link}

These can sometimes be harder to draw strong conclusions from since they are internally rating their own portfolio and they don't use a standard scale. With TPVG, we have color categories where TRIN shows designations with various "performing" ratings. In fact, for TPVG, a lower number is better as 1 is performing above expectations, and a 5 is default or about to. For TRIN, a higher rating number is better due to 5 being the best and 1 being the default. The idea is still the same amongst most of the categories, though.

All that being said, we see here that TPVG's portfolio is largely "performing" as they expected. Not a bad thing during these sorts of uncertain economic times.

They are performing well enough that the NII jumped to $0.58 for the latest quarter. A year ago, they reported an NII of $0.42. That is allowing them to bump up their quarterly distribution to $0.40 per share , despite the headwinds and challenges in the latest quarters, which gives a lot of confidence from management going forward. That's after they had increased in the previous quarter as well and paid a $0.10 special.

TPVG has a bit less of their portfolio invested in floating rates, but we've already seen the results of higher NII that they've benefited from nonetheless. It could also be argued that some of this fixed-rate debt could be beneficial for these BDCs when rates eventually fall.

TPVG Fixed/Floating Loans (TriplePoint Venture)

This BDC is carrying around 70% of its debt in fixed rates as well, as they noted in their earnings call .

Now just a quick update on the balance sheet, leverage and overall liquidity. As of the end of the year, an aggregate of $570 million of debt was outstanding, $395 million in the form of fixed rate investment-grade term notes and $175 million outstanding on our revolving credit facility.

It's those two factors that are contributing to BDCs being particularly attractive investment options at this time. TPVG breaks down the benefit of rising rates; however, this also includes the negatives should interest rates decline.

TPVG Prime Rate Change Impact (TriplePoint Venture)

Conclusion

Trinity Capital Inc. and TriplePoint Venture Growth have reported their latest earnings; while we knew NAVs would take a hit, they remain interesting investment choices at this time, regardless. They are working through their latest challenges; only time will tell if more come up later this year with a potential recession.

That being said, both have such strong distribution coverage that even these potential headwinds seem unlikely to derail either of these BDCs in terms of having to cut payouts. In fact, the way things are looking, we may continue to expect growing dividends from both and/or additional supplemental.

With the latest bank failures, we're certainly in a precarious situation for the overall macro outlook bringing about a lot of uncertainty. The upside is that valuations then have come down with this volatility. Considering a dollar-cost average approach or selling puts could also be a fairly strong consideration. That being said, selling puts on BDCs comes with the challenges of generally low volume and interest and low premiums unless they are near the money.

For further details see:

Trinity Capital And TriplePoint Venture: 2 BDCs With Potential