TRIN - Trinity Capital: Chance To 'Double Your Dividend'

2023-07-08 01:56:07 ET

Summary

- Trinity Capital is a business development company that's focused on venture capital lending and equipment loans.

- Recently, Jefferies initiated coverage on TRIN with a Buy and a $15 price target.

- The shares rapidly shot higher, and that's where the opportunity to write covered calls comes in for the opportunity to double your dividend for the quarter essentially.

Written by Nick Ackerman.

We previously gave Trinity Capital (TRIN) a look at its Q1 earnings for 2023. Overall, the results were neither spectacular nor were they atrocious. That's okay, though; I view this as a long-term position. The quarter-to-quarter isn't going to be the sole factor in driving my decisions. Besides providing lukewarm results, they still traded at a decent valuation at that time, too.

Analyst Coverage Pushes TRIN To Elevated Valuation

However, since then, shares have been on quite a rise. Even more recently, investors apparently got incredibly excited when Jefferies initiated coverage of this business development company with a Buy rating. They came up with a $15 price target, and that saw shares rise rapidly. That's resulted in some incredible total returns since our prior coverage.

TRIN Performance Since Previous Update (Seeking Alpha)

Bear in mind, though, that with this rapid ascension in the short-term, it wasn't necessarily backed by the actual underlying portfolio of loans for this venture-focused BDC. The next earnings are set to be announced in early August, which will give us a better overview of how things are looking for this latest quarter. For that reason, we are at a last posted NAV per share of $13.07.

This would suggest that Jefferies believes around a 15% premium is justified, and we are at around 11% after the July 6th close. Shares dipped a bit yesterday after the initial spike. That means the latest price has now pushed TRIN to trade at quite an elevated premium.

TRIN Discount/Premium History (CEFData)

{kind=link}

To be fair, TRIN has a relatively limited public history, so we aren't necessarily sure where things could trade long-term. It could very well be the next Main Street Capital ( MAIN ) or Hercules Capital ( HTGC ), two BDCs that regularly trade at premiums to their NAVs.

Double Your Dividend Opportunity

One way to take advantage of this significant spike would be to simply sell shares of TRIN and wait for things to come back down. If they do in the next recession or the next bankruptcy of a holding, then great, initiate another position at a lower cost.

However, if you're a long-term holder, there is another possibility of writing covered calls. That is the route I took on a portion of my position. By overwriting only a portion of my position, if things continue to get carried away, I can still participate in the upside. I initially shared this trade with Cash Builder Opportunities members first:

The Trade : Sell to Open Calls on Trinity Capital (TRIN) October 20th, 2023 - $15 strike collected $0.60

Ticker: TRIN

Expiration: October 20th, 2023

Type: Sold Calls

Strike Price: $15

Price Move Until Strike: 1.90%

Premium Collected: $0.60 or $60 per contract

Days To Expiration: 107 days

Potential Annualized Return: 13.64%

Breakeven: $15.60 - if shares move above this, it would have made more sense to hold the position instead of selling calls

Option Volume: light volume but plenty of open interest

Dividend Equivalent : 1.25x ($0.48 quarterly)

The regular quarterly dividend in the last quarter was $0.48, which actually means collecting the $0.60 in premium is the equivalent of 1.25x the regular dividend paid.

That being said, they've been increasing their dividend and paying out fairly regular supplemental distributions as well. This has all been backed by increasing net investment income that they've been able to generate through growing their portfolio and rising interest rates. The latest raise was around a 2% increase since this chart was provided in their investor presentation .

TRIN Dividend History (Trinity Capital)

{kind=link}

So they still have the capacity, and it could be very likely that they will bump up their dividend with the September Q3 dividend announcement. I base this on the $0.52 diluted NII they reported last quarter, providing coverage of 92% with the anticipation that NII increases in this quarter. Either way, $0.60 in premium will likely be double even the next dividend announcement.

General Risks And Potential Outcomes of This Move

A couple of things to consider with covered calls and how this could play out going forward.

First, I expect this to expire worthless as shares pull back - potentially even closing the trade early when I feel that a sufficient amount of the premium can be locked in.

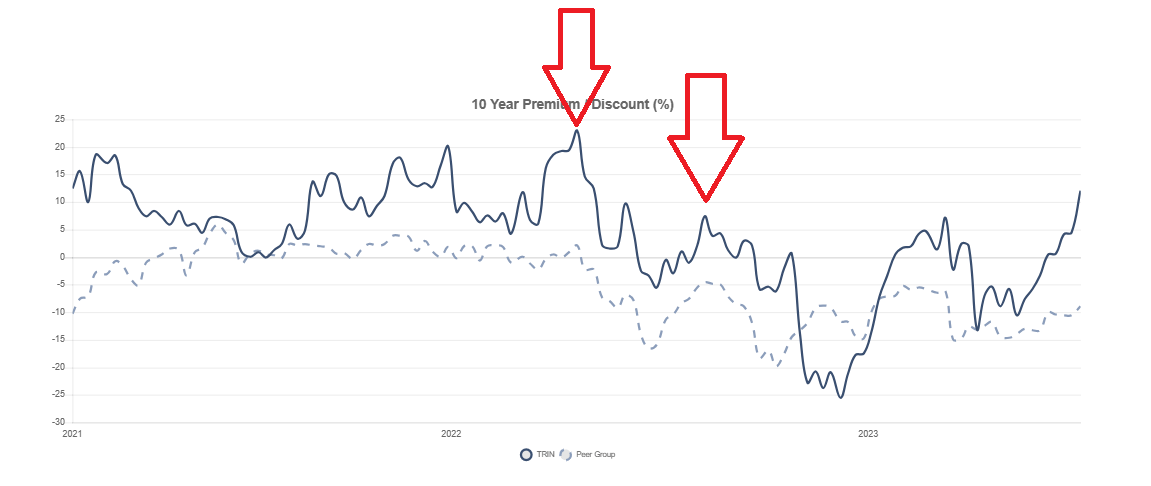

To help potentially prod this decline along, I believe that TRIN management might initiate a share offering. Last year they offered shares in both August and April. That was roughly where I placed these red arrows on their discount/premium history. As we can see, the premiums were around the same levels when they were initiated. The premiums then dropped after announcing these offerings as the price fell lower.

TRIN Discount/Premium History (CEFData (arrows included by author))

{kind=link}

To be fair, 2022 had been quite a volatile year not only for broader markets but it was tough for smaller companies where IPOs were quite limited. Interest rates are rising, which continues to pressure these venture companies today. With negative or limited cash flows, the rising costs of their borrowings become burdensome. That big dive to a discount in Q4 2022 resulted from Core Scientific announcing bankruptcy , as TRIN had sizeable equipment loans with them. That's still working to be resolved, though; with higher Bitcoin prices, it's more promising.

Further bankruptcy, as the Fed looks to weaken the economy further to combat inflation, can be quite expected. And we all know how rate hiking cycles end with a recession. The question only becomes how long and deep a potential recession is. TRIN is in the riskier space of BDCs as some companies they invest in don't have any cash flow at all, so that's a general risk.

However, I digress. My main point here is that a share offering could cool this recent rally in a quick hurry, allowing us to close out the covered call position sooner than letting it even reach the expiration date and expire worthless.

The second consideration would be what to do if shares continue to rally. Let's say that shares climb to above $15. Well, my expectation is that even if we get a fantastic quarter and NAV rises, it's unlikely to be by a material amount. Remember, with the latest dividend announcement; they paid out a supplemental $0.05. That isn't massive, but every cent paid is a cent that won't be retained, and therefore NAV won't be rising.

Let's assume they have a blowout quarter, and valuations rise substantially by 5%. These were around some of the increases we saw in valuations when valuations didn't matter in 2021, and the only thing that mattered was growth and pushing unprofitable companies to IPO.

A 5% increase from the prior quarter would suggest NAV could come in at $13.72. Personally, if NAV holds flat, I'd be tickled pink. Perhaps I have low expectations, but I'm trying to be realistic and allow myself to be surprised by the upside. An increase of 5% would mean NAV increased by $0.65 while they also paid out $0.53, meaning between NII and appreciation in the fund, it would have provided $1.18 a share. Off a NAV of $13.07 would mean a ~9% performance in a single quarter. This is to help illustrate how optimistic such a scenario would be.

Anyway, that would still suggest I'm letting go of a portion of shares at around a 9.3% premium. Adjusted for the premium collected at $15.60, breakeven would mean the premium is at 13.7% in the optimistic scenario. Not a bad result and one I'd be happy with. Based on a flat NAV suggesting that the NAV stays around $13.07 puts the $15.60 (strike price plus premium collected) at a ~20% premium. That's historically where TRIN had topped out in terms of its premium.

Of course, if we are above $15, come expiration in October, which is the scenario I find less likely, the position could always be rolled as well. That would include closing out the position potentially at a loss and writing another covered call out at a later date and/or the same or higher strike price.

Conclusion

Overall, I remain optimistic about my TRIN position. While it's a riskier BDC, I believe that it's still worth holding in one's portfolio if one can handle such risk. They continue to benefit from increased interest rates, and the latest ADP jobs data suggests the Fed still has more work to do. However, the official BLS showed a miss on the expectations for jobs. That could mean the economy is weakening, which also may not put small companies in a great position.

All that being said, I'm also trying to be realistic. By overwriting some of my position, I believe that's an attractive way to exploit this latest rally.

I ultimately believe that a move to a "Hold" rating at this time is more appropriate than a "Buy." Other more tactical investors could take advantage by selling their positions or trimming. Then revising when potential lower prices come or looking for alternative BDCs to put their capital to work in for now.

For further details see:

Trinity Capital: Chance To 'Double Your Dividend'