CA - Triple Flag: Growth At A Reasonable Price

2023-03-27 03:51:20 ET

Summary

- Triple Flag has been one of the better-performing names in the miner space over the past 12-15 months, up 25% from year-end 2021 vs. a 2% decline in the GDX.

- I attribute the outperformance to its superior business model (royalty/streaming) vs. producers and a brilliant acquisition that has led to a major upgrade in the investment thesis.

- Unfortunately, we saw a miss on 2022 guidance because of timing delays at Cerro Lindo that weighed on Q1-23 share price performance, but the long-term picture has never looked better.

- Given Triple Flag's solid organic growth profile, high exposure to silver relative to peers, and reasonable valuation, I would view any weakness below US$11.85 as a buying opportunity.

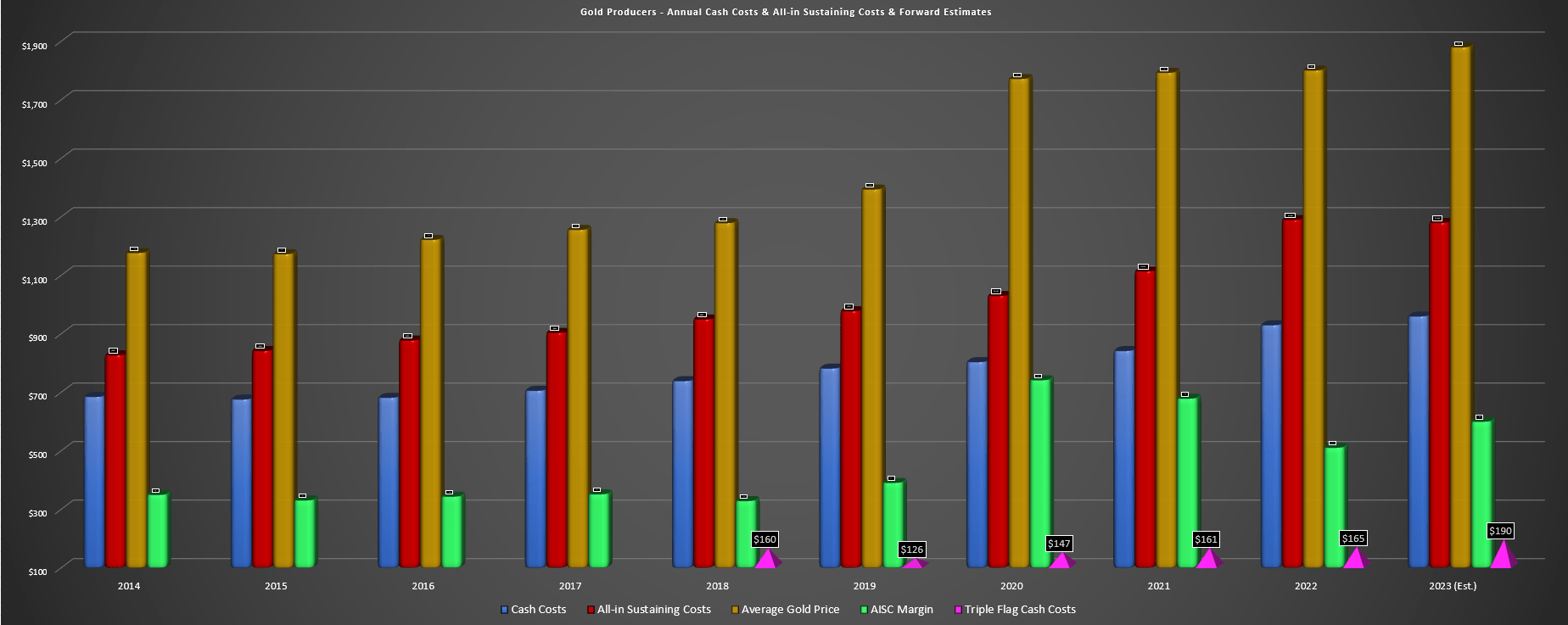

2022 was a tough year for the Gold Miners Index ( GDX ) and although several names rallied to finish the year, we've seen a sharp retracement since the highs. The poor performance on a trailing two-year basis for gold producers isn't that surprising, given that most of the margin benefit from a $400/oz increase in the gold price ($1,800/oz vs. $1,400/oz) was mostly offset by the impact of inflationary pressures (fuel, electricity, labor, steel, cyanide) with minimal margin improvement and higher share counts for many companies because of share-based acquisitions and or capital raises to fund growth projects.

Some investors have argued that the Gold Miners Index has no business trading below $35.00 when it traded as high as $45.00 in July 2020 with the gold price trading just 5% lower. However, I see this as a superficial argument when we have seen meaningful share dilution among producers (and even some royalty/streaming companies) and severe margin compression. As evidence of this, AISC margins sector-wide declined 30% from FY2020 to FY2022 despite a slightly higher average realized gold price reported sector-wide. So, while one might believe gold producers should trade higher if the gold price is at higher levels, this argument is only valid if that benefit actually flowed through to their bottom line (which it didn't).

In fact, even at a spot gold price of $1,950/oz, the GDX's position relative to its highs ($32.00 vs. $45.80 or 30% from highs) is consistent with the decline we've seen in AISC margins with AISC margins of ~$670/oz for FY2023 and peak AISC margins of $1,060/oz at the July 2020 highs for gold (37% from highs).

Gold Producers - Cash Costs, AISC, AISC Margins & Triple Flag Cash Costs (Company Filings, Author's Chart & FY2023 Estimates)

{kind=link}

Fortunately, the royalty/streaming companies' superior business models insulated them from these headwinds. This was quite clear in Triple Flag's ( TFPM ) cost/margin profile and its cash flow generation, with operating cash flow just 1% of shy record highs, and its cash costs up just ~3% from FY2018 levels vs. a 26% increase for producers. The result was that the company maintained its industry-leading margins while even the best producers benefiting from economies of scale unfortunately suffered a hit to operating and free cash flow because of higher operating costs and capital expenditures on balance. In this update, we'll look at Triple Flag's Q4/FY2022 results in a bit more detail and whether the stock is getting close to reaching a buy point.

Q4 & FY2022 Results

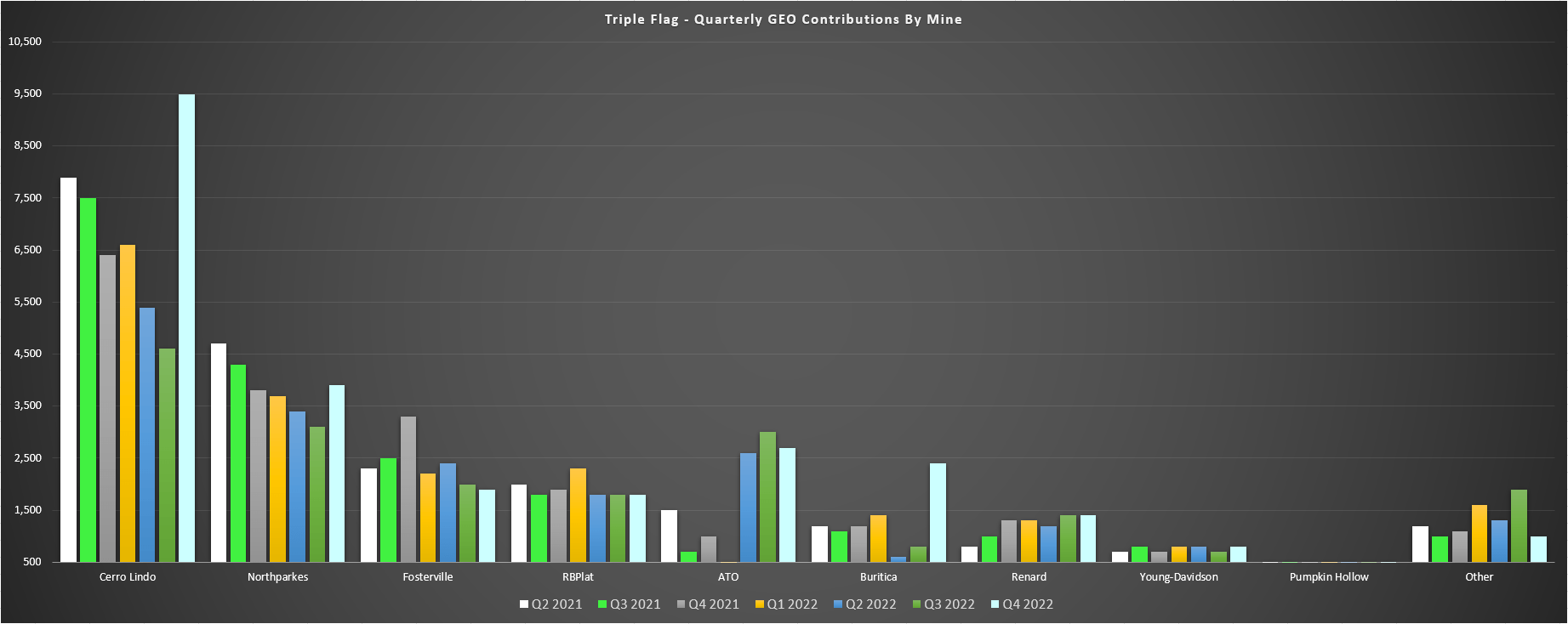

Triple Flag released its Q4 & FY2022 results last month, reporting record gold-equivalent [GEO] sales of ~25,400 ounces, a ~23% increase from the year-ago period. This was driven by higher contributions from Cerro Lindo (~9,500 GEOs), Northparkes (~3,900 GEOs), ATO (~2,700 GEOs), and Buritica (~2,400 GEOs), with the only major offset being lower ounces from Fosterville which saw its annual production slide from ~509,600 ounces to ~383,300 ounces related to lower grades and operating restrictions, with just ~8,500 attributable GEO sales in 2022 for Triple Flag. Fortunately, despite a significant decline in production profile at Fosterville, Triple Flag still put up a record year, reporting ~84,700 GEOs sold, a 1% increase from the year-ago period.

Triple Flag - Quarterly GEO Contributions by Mine (Company Filings, Author's Chart)

{kind=link}

Looking at the results on a full-year basis, the company's top assets saw lower GEOs on a year-over-year basis (Cerro Lindo, Northparkes, Fosterville, RBPlat), but smaller assets like Young-Davidson, Dargues, Buritica, Renard and ATO saw higher production to offset these declines. Unfortunately, it wasn't enough to deliver into FY2022 guidance of 90,000 to 95,0000 GEOs when combined with a less favorable gold-silver ratio. That said, this was an unusual year for key assets, with Fosterville impacted by operating constraints (low-frequency noise emitted by surface fans resulted in the EPA of the Victoria Government disallowing fans from running from midnight to 6 AM, which impacts mining rates), a tragic fatality at RBPlat that resulted in lower production, and unfavorable delivering timing at Cerro Lindo.

{kind=link}

Despite these unfortunate headwinds, Triple Flag had an exceptional year financially (especially relative to producers where we saw significant margin compression), with Triple Flag reporting cash costs of $157/oz in Q4 2022 and $165/oz for the year, with cash costs actually lower on a year-over-year basis. Although this figure will increase following the acquisition of Maverix, cash costs should remain below $200/oz in FY2023, with these costs being far lower than Royal Gold ( RGLD ), Franco-Nevada ( FNV ), Sandstorm ( SAND ), and Wheaton Precious Metals ( WPM ) with average cash costs of ~$350/oz. So, not only does Triple Flag stand out for having a very enviable jurisdictional profile (62% of consensus NAV in Australia/North America), but its margins are superior to nearly all of its peers.

{kind=link}

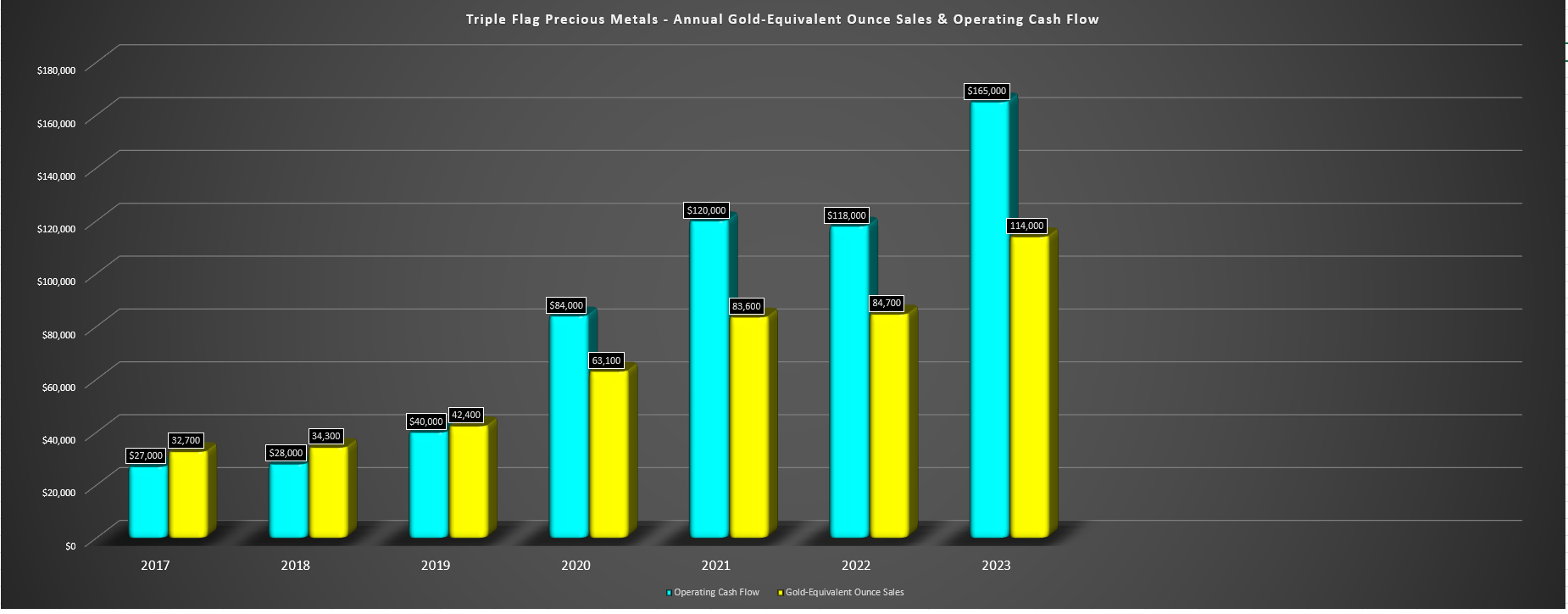

Looking at the below chart, we can see that despite the miss on guidance and no help from gold and silver prices which declined year-over-year, Triple Flag reported annual operating cash flow of $118.4 million, only a 1% decline from the year-ago period. This compares quite favorably to the world's largest gold producer, Newmont ( NEM ), who saw operating cash flow decline 25% year-over-year and ~35% from FY2020 levels (~$3.2 billion vs. ~$4.9 billion). And on a forward basis with the acquisition of Maverix that will add several solid assets like Beta Hunt, La Colorada, and Camino Rojo, we should see ~40% growth, with the potential to generate upwards of $165 million in operating cash flow if metals prices remain favorable. Let's dig into recent developments below:

This assumes Triple Flag is able to deliver at the top end of its FY2023 guidance range of 100,000 to 115,000 GEOs, and I would argue that this outlook is conservative given that it does not include Omolon Hub (acquired in Maverix transaction), and assumes similar timing lags, a higher gold/silver ratio, and assumes no resolution to operating constraints at Fosterville, where we could see an additional 500+ GEOs if we do see a timely resolution by summer.

Triple Flag - Annual GEO Sales & Operating Cash Flow (Annual GEO Sales & Operating Cash Flow)

{kind=link}

Recent Developments

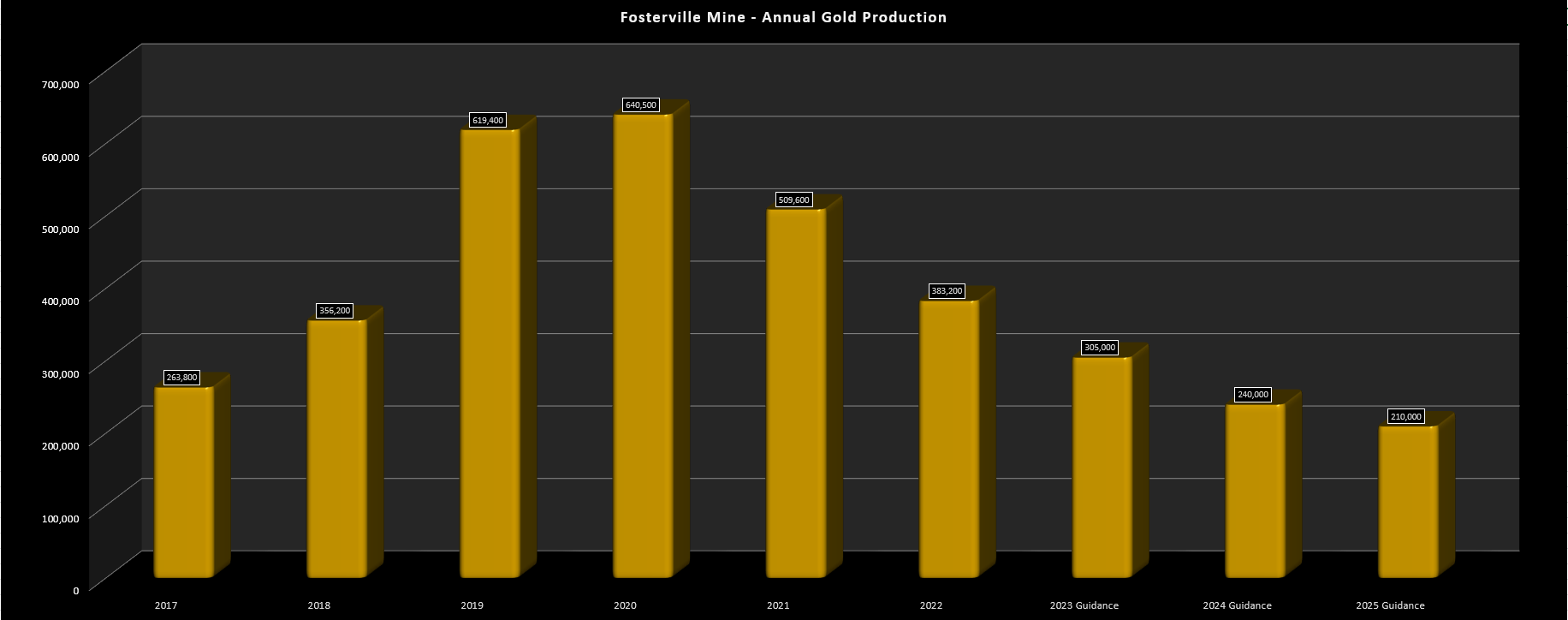

Moving over to recent developments, the major news since the preliminary sales update provided in early February was that the outlook at Fosterville has become much less attractive from a production standpoint which doesn't bode well for Triple Flag given that this is a top-5 asset. As shown in the chart below, the guidance mid-point provided by the operator points to average three-year production (2023-2025) of 251,700 ounces, a significant decline from trailing three-year average production of 511,100 ounces. Much of this decline is related to grades given that the 1.0+ ounce per tonne ore at the Swan Zone certainly wasn't going to last forever, but it's also impacted by lower than planned mining rates due to operating constraints described earlier.

Fosterville Mine - Annual Production & Forward Guidance Midpoint (Company Filings, Author's Chart)

{kind=link}

While this could be solved in a timely manner, it's important to note that this has been an issue since 2021 when Kirkland Lake Gold received a notice for investment and improvement by the Environmental Protection Authority [EPA] of the Victoria Government. This noticed determined that the low-level frequency noise ( below the level of normal human hearing at 16-20 hertz) was being emitted by the Fosterville Mine and that " additional action may be taken by the EPA that could result in restrictions on the use of certain equipment, primary surface vent fans and surface drill rigs in the south portion of the mining lease. " Fifteen months later, Agnico ( AEM ) is now dealing with these issues are the merger despite accredit noise/acoustic specialist firms in Australia concluded that the noise was within regulatory limits.

Even ahead of this news, Agnico's new CEO Ammar Al-Joundi had expressed that the company is operating a much larger portfolio and that some assets could be considered non-core in countries where there's a much lower production profile unless Agnico can find a way to add additional production in that region, given that it specializes in regional mining. Ahead of the operating constraints, Agnico might have looked at adding an additional operation through M&A in Australia to make it worthwhile to stay in the country given that no miner wants to give up an asset with ~$1,450/oz cash margins. However, it's possible that Agnico is a little frustrated and may not see the same future for Fosterville is this isn't resolved by 2024. So, in this case, adding another operation to justify staying in Australia may not make sense.

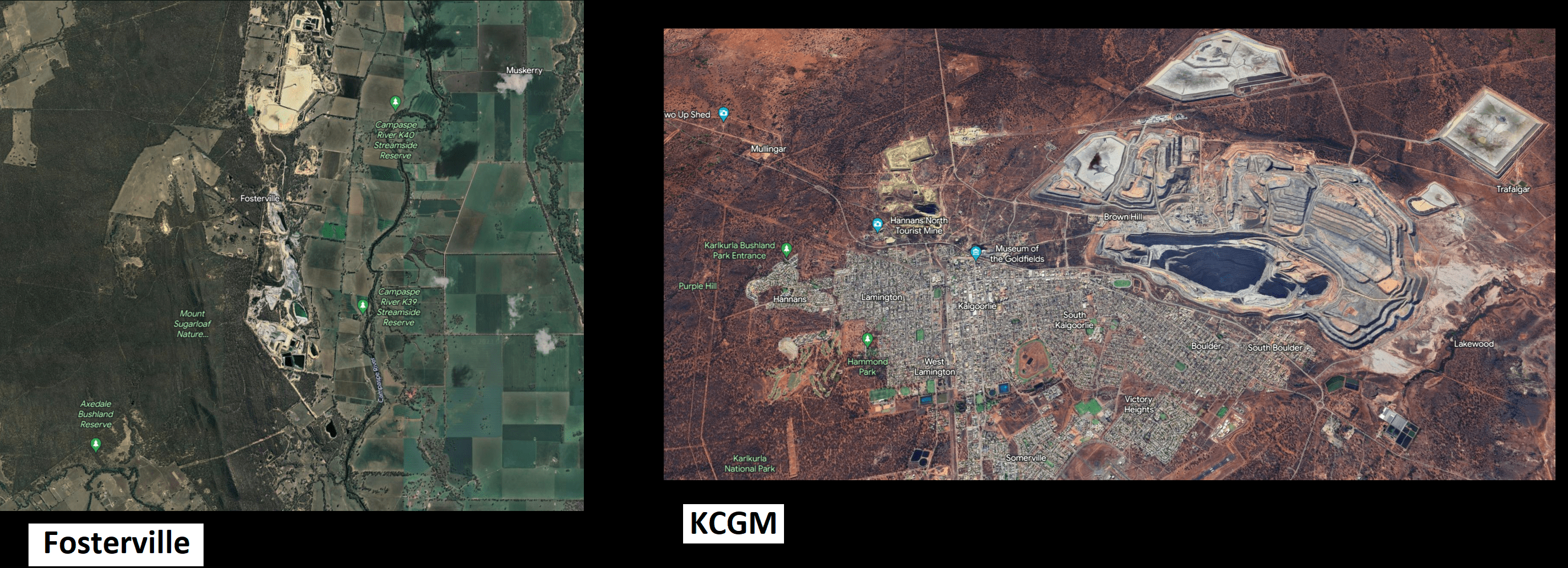

Obviously it's quite early to speculate on what Agnico will do with Fosterville and the company made clear that it expects to return to full capacity once restrictions are lifted which could add 50,000 ounces per annum of incremental production in 2023 and 2024. That said, it appears that the company is getting somewhat unfair treatment when we consider that Fosterville is a remote operation 20 kilometers from Bendigo, while the massive open-pit KCGM operation sits right next to a residential area and is a much more significant earth-moving operation (80+ million tonnes per annum) with plans for a potential expansion to 22-24 million tonnes per annum of processing capacity vs. Fosterville at a mere ~700,000 tonnes per annum.

{kind=link}

If Agnico were to sell Fosterville or stop operating it if it can't justify running the operation at ~600,000 tonnes per annum post-2026 at lower grades, both of these developments would be negative for Triple Flag. In the latter case, production would cease and Triple Flag would no longer see contributions. In the former case, Triple Flag may have an operator, but certainly not likely one with as much expertise as Agnico and Fosterville would no longer be owned by the sector's most aggressive driller. To summarize, this is a development worth monitoring, and one that could hurt the investment thesis if not resolved by mid-2024 when grades decline further.

So, is there any good news?

While the Fosterville developments are disappointing and somewhat overshadow the recent exploration success by Agnico Eagle at the mine, several of Triple Flag's partners continue to see material exploration success at some assets. This includes near-mine and regional exploration success at Railroad South and Camino Rojo by Orla Mining ( ORLA ), continued exploration success by Skeena ( SKE ) at Eskay Creek, and increases in nickel and gold resources at Beta Hunt. In addition, the second decline at Beta Hunt has been completed on budget and schedule, de-risking the company's plans to grow Beta Hunt into a 140,000+ ounce per annum gold mine. Lastly, in Nicaragua, Calibre ( OTCQX:CXBMF ) confirmed that production is on track for Q2 2023 at Eastern Borosi where Triple Flag holds a 2.0% NSR on gold and silver.

Finally, Steppe Gold ( OTCQX:STPGF ) is confident that it can become a 200,000+ GEO per annum producer which will give it more capital to support exploration at ATO, with much of this expansion coming from Phase 2 at ATO which will push production to 100,000 ounces per annum by 2025. The most recent news out of Steppe was that the Phase 2 Expansion is planned for Q2 2023, it is planning to acquire Anacortes Mining ( OTCQX:XYZFF ) to add its Tres Cruces Project in Peru, and the mine life at ATO has been extended to 2036 (29.1 million tonnes of reserves at ~1.30 grams per tonne gold-equivalent), providing strong visibility into future production from this steadily growing contributor for Triple Flag.

For those unfamiliar, Triple Flag holds a 25% gold stream and 50% silver stream on ATO, subject to an annual cap of 7,125 ounces per annum of gold once 46,000 ounces have been delivered (and additional cap on silver after deliveries of 375,000 ounces). To date, ~19,200 ounces of gold had been delivered and ~40,200 ounces of silver, suggesting three years of additional production until the gold cap is hit when we see a step-down. Triple Flag also holds a 1.50% NSR on Tres Cruces, meaning it would hold royalties/streams on both of Steppe Gold's future producing assets.

Long-Term Outlook

In regards to Triple Flag's long-term outlook, 2023 sales guidance might be a little lighter than some hoped with Fosterville operating constraints, and a portion of Northparkes production deferred from 2023 until 2024 related to a change in plans for mill feed blending, with the high-grade E31N open pit expected to start in Q4 2023. According to Triple Flag, this is related to working to optimize cave productivity with plans to mine higher volumes at the E26 Lift 1 North Cave. However, Triple Flag will benefit from higher production post-2023 when higher grade grades head to the mill from E31N (2024) and E22 later this decade.

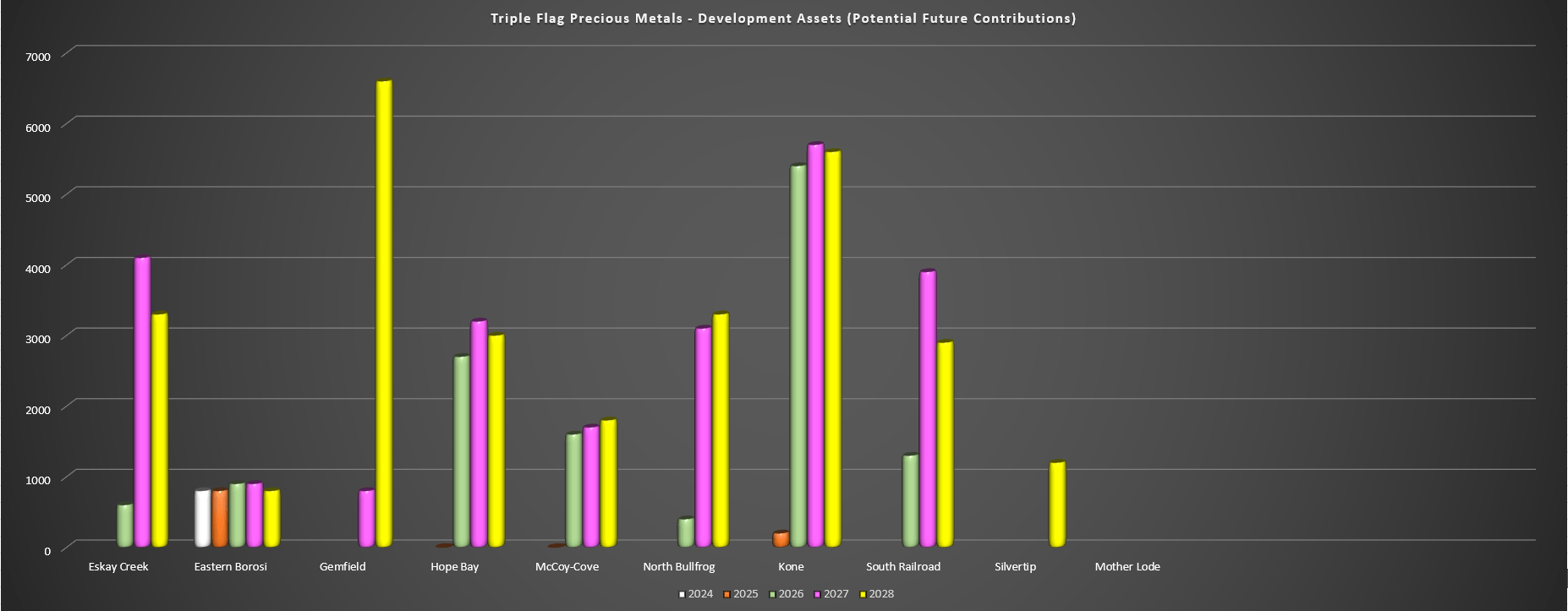

Combined with new mines coming online and organic growth and what should be a restart at Hope Bay at a minimum 300,000-ounce production profile post-2026, Triple Flag could easily boast a 175,000 annualized GEO production profile by 2029. This would represent ~63% growth from the midpoint of FY2023 guidance, and we can see the several assets that could contribute to this GEO growth below. The most significant of these assets are Hope Bay, Gemfields, Kone, Railroad South, North Bullfrog, and Eskay Creek, and I would argue that there's a high probability that at least five of these six assets are in production by 2028. This is important for Triple Flag because not only does it provide growth, it also provides added diversification, placing Triple Flag just behind the Royal Gold of today, which has 40 producing assets.

Other assets I have not included given that it's harder to put a timeline on first production are DeLamar (Idaho), Cerro Blanco (Guatemala), Agua Rica (Argentina), Hasbrouck (Nevada), Mother Lode (Nevada), Kemess (British Columbia), Enchi (Ghana), Bullfrog (Augusta), Buffalo Valley (Nevada), Dixie Creek (Nevada), and Fenn-Gib (Ontario). In summary, this is a very deep portfolio following the Maverix acquisition, and there are well over a dozen assets at solid projects of varying quality that could contribute to future growth entirely separate from newly acquired royalties/streams which appear likely given that the company sees lots of opportunities and has over $600 million in available liquidity to put to work.

Triple Flag - Select Development Royalty Assets - Potential Future Contributions (Company Filings, Author's Chart & Estimates)

{kind=link}

Valuation

Based on ~207 million fully diluted shares and a share price of US$13.60, Triple Flag trades at a market cap of ~$2.78 billion and an enterprise value of ~$2.80 billion. As I noted in my January update , while this was a very reasonable valuation for a portfolio of Triple Flag's quality, I saw the more attractive opportunity being Osisko Gold Royalties ( OR ) and Sandstorm ( SAND ), given that they were more attractively valued, even if perhaps Triple Flag is higher-quality than Sandstorm. Since then, Osisko Gold Royalties has gained 23%, Sandstorm is up 4%, and Triple Flag is actually down 4% in the same period. And the good news is that this recent underperformance is making the stock more interesting on a relative value basis.

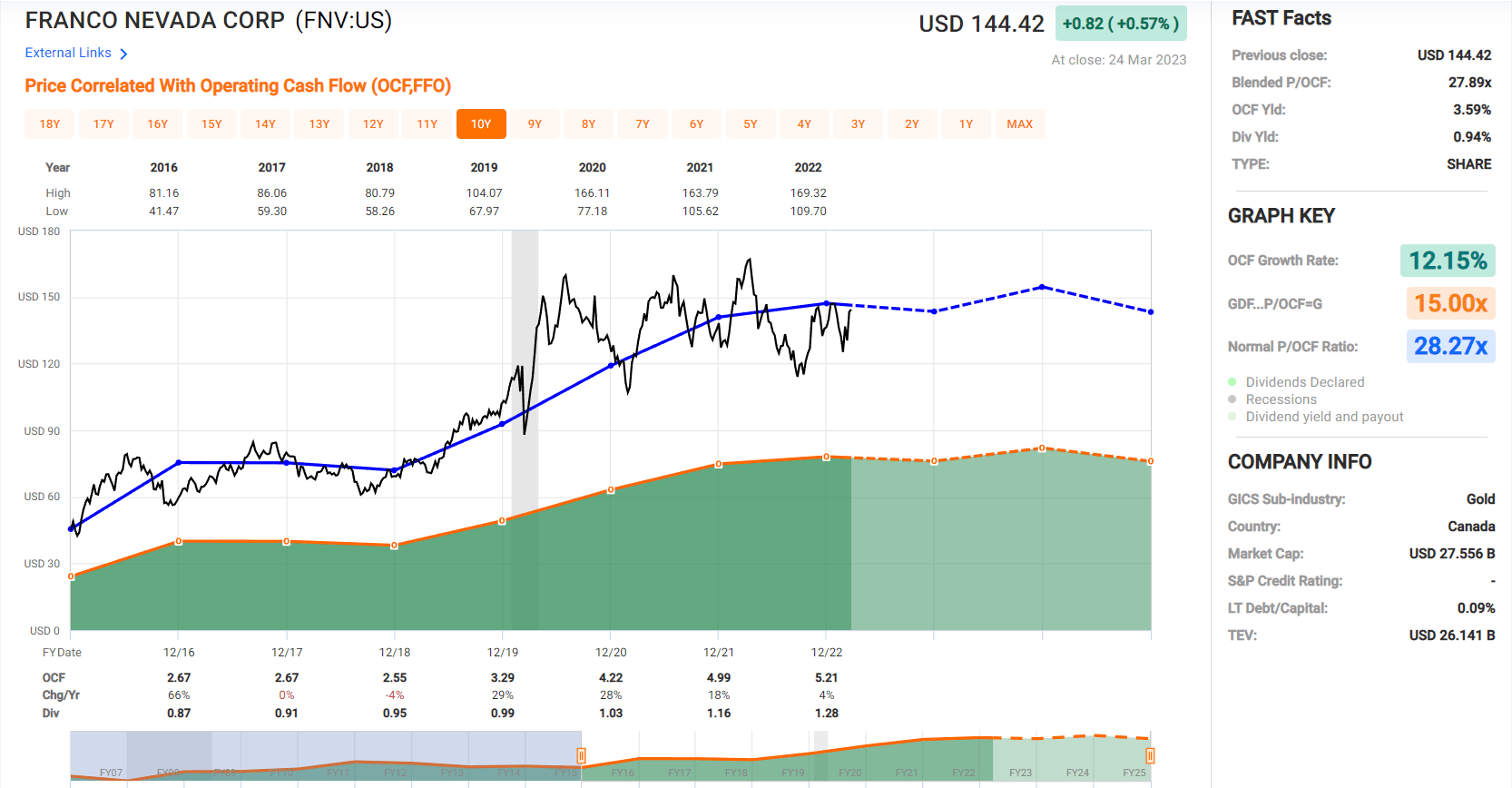

If we compare Triple Flag to larger peers like Wheaton Precious Metals ( WPM ) and Franco-Nevada ( FNV ), Triple Flag now has a superior jurisdictional profile to the two and its concentration to its two primary assets (Northparkes, Cerro Lindo) has reduced materially following the acquisition of Maverix, especially if several new mines can come online post-2025. This doesn't mean that Triple Flag should trade at the same cash flow multiple at these two companies or its larger peer group, but if one sees a path to Triple Flag eventually earning 200,000 GEOs per annum, these premium multiples could become a reality sometime later this decade. As it stands, FNV and WPM trade at an average of ~27.5x FY2023 cash flow estimates, respectively, vs. TFPM at ~17.0x cash flow, a huge discount to the sector's top-2 names.

Franco-Nevada - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Using what I believe to be a fair multiple of 21.0x cash flow at its current scale, given Triple Flag's improved diversification and jurisdictional profile (offset by smaller scale and less diversification than FNV), I see a fair value for the stock of US$17.65. This points to a 28% upside from current levels, which is certainly attractive regarding gaining exposure to a relatively low-risk and high-margin business like Triple Flag. That said, I prefer a minimum 33% discount to fair value when investing in mid-cap royalty/streaming names, which would translate to a low-risk buy zone for Triple Flag of US$11.85 or lower. Of course, there's no guarantee that the stock gets this low, but this is where I would become more interested in TFPM from an investment standpoint and where there would be a significant margin of safety present.

Summary

Triple Flag has continued to fire on all cylinders and has launched itself into the #4 spot in the precious metals royalty/streaming sector with the timely and accretive offer to acquire Maverix Metals. As noted in a previous update, this not only adds considerable GEOs earned per annum, but patches up any holes in its armor under TFPM 1.0 (pre-Maverix), when the company had heavy concentration to two assets and while it had a phenomenal production profile, it lacked a strong development pipeline. In this sense, Maverix and Triple Flag were a near-perfect match, with Maverix bringing several solid development-stage royalty assets to the table (Hope Bay, Eskay Creek, Gemfields, McCoy-Cove, North Bullfrog, Mother Lode, Silvertip, South Railroad, Kone) and most of these are in Tier-1 jurisdictions, an additional bonus.

Given this significant upgrade to the investment thesis, when coupled with organic growth in Triple Flag's portfolio, I have warmed up considerably to TFPM, and see the stock as a solid buy-the-dip candidate if investors can get the right price. As noted, I see the right price that would offer a meaningful margin of safety at US$11.85 or lower, and I would strongly consider starting a position in the stock at these prices. For investors that are long the stock, key developments to watch will be Fosterville exploration and any developments with the EPA in Victoria, permitting news at South Railroad/North Bullfrog, Eskay Creek financing/permitting, and exploration success and an updated economic study for Kone later this year.

For further details see:

Triple Flag: Growth At A Reasonable Price