CA - True North: Upgrading To A Hold After Brutal Three Months

2023-05-26 16:41:43 ET

Summary

- We had two bearish/short-sell pieces on True North earlier in the year.

- The distribution cut has played out as expected.

- We look at Q1-2023 results and tell you why we are closing the short sell call.

True North Commercial REIT ( TNT.UN:CA ) has had it rough. The Canadian office REIT has been at the receiving end of a brutal macro environment for office space. It also finally did the overdue distribution cut, which got it a hostile reception. But the stock has indeed corrected to levels we expected since our initial Sell rating.

Seeking Alpha

In our last article we had actually identified a specific price point and that has been exceeded.

If you apply an 8% cap rate, the NAV drops to $3.25 per share. We think this is more realistic for office properties especially with such short leases in troubled markets like Alberta. Yes, the tenants are investment grade. That only means they have better negotiating power and can find a better place if they need to. We think that the stock will actually trade to that $3.25 level very soon.

Source: The First Cut Is The Deepest

We look at Q1-2023 results and tell you how we are reading the tea leaves.

Q1-2023

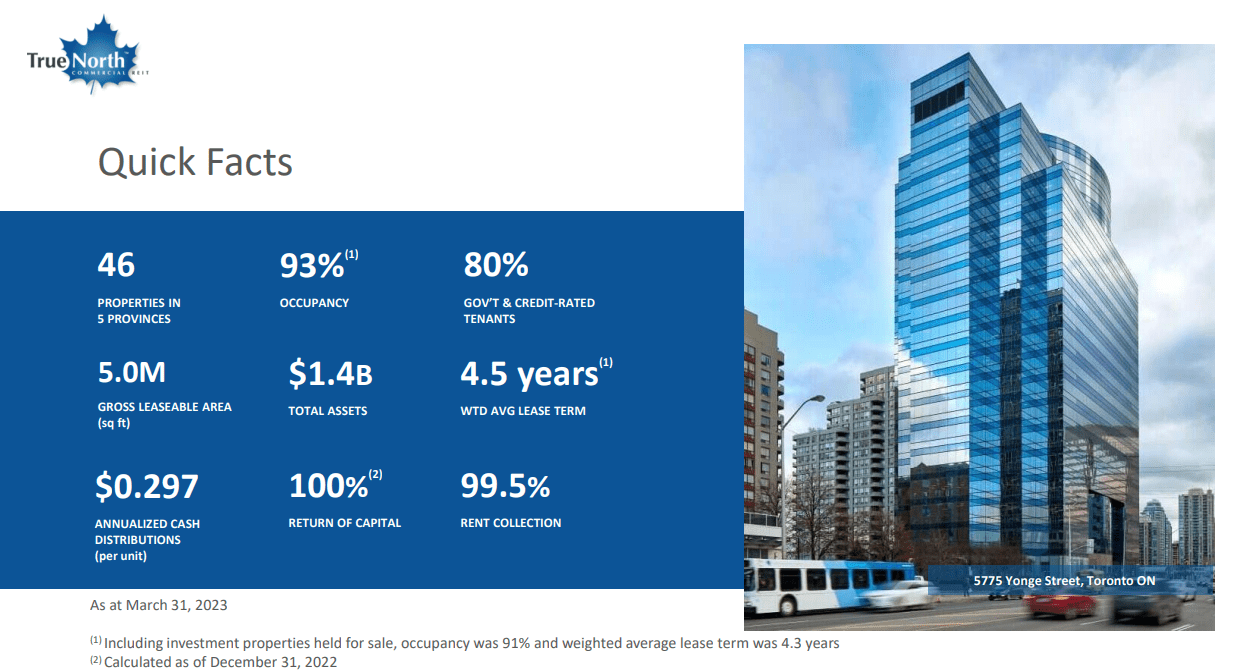

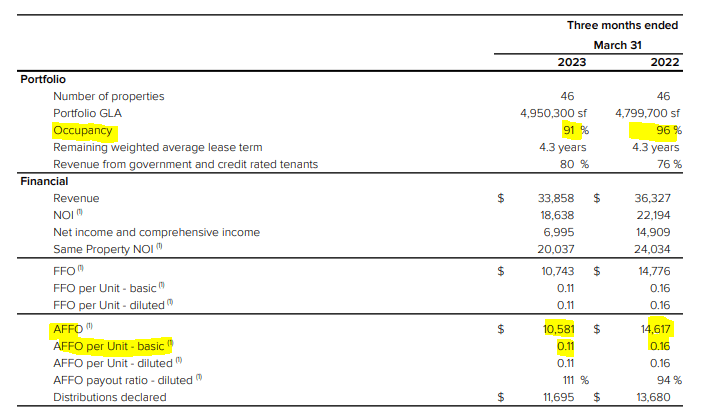

At the end of Q1-2023 True North had 46 properties including the two held for sale. The occupancy levels were stellar at 93%, but the weighted average lease term was 4.3 years (when you consider the impact of pending sales).

{kind=link}

True North Q1-2023 Presentation

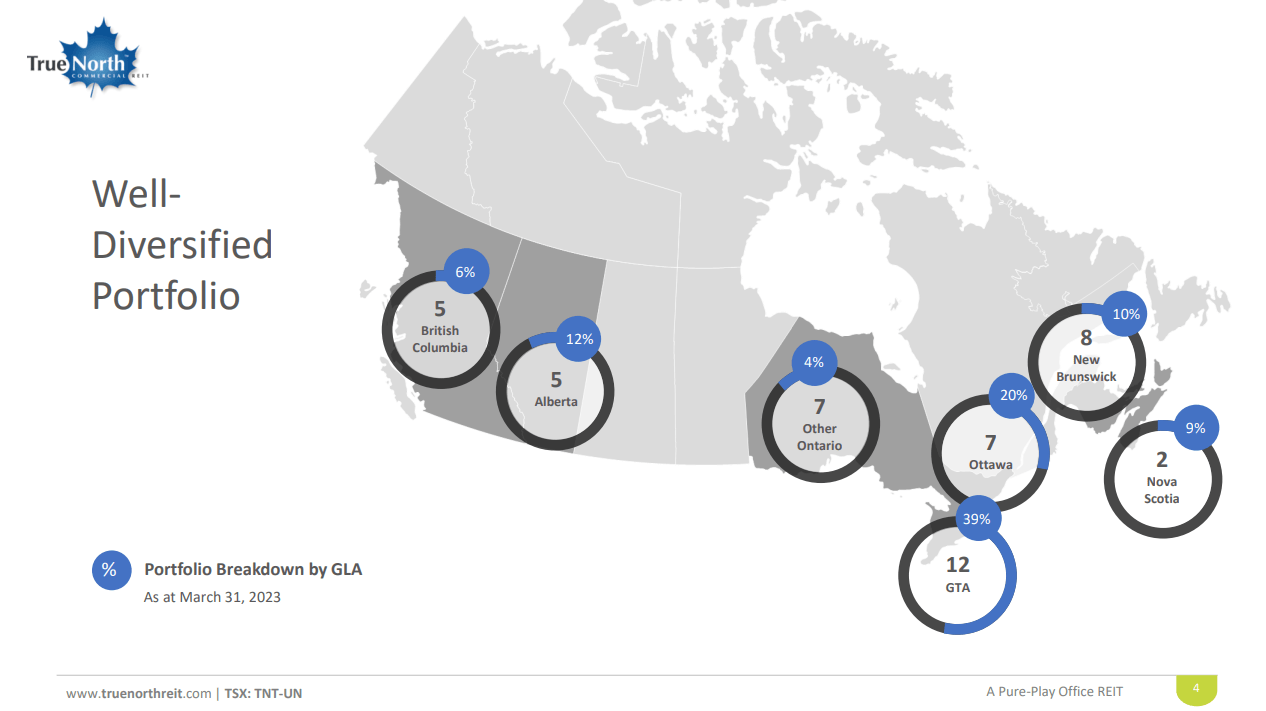

True North's property mix is heavily tilted towards the Greater Toronto Area or GTA, with 40% of gross leasable area coming in that region.

{kind=link}

True North Q1-2023 Presentation

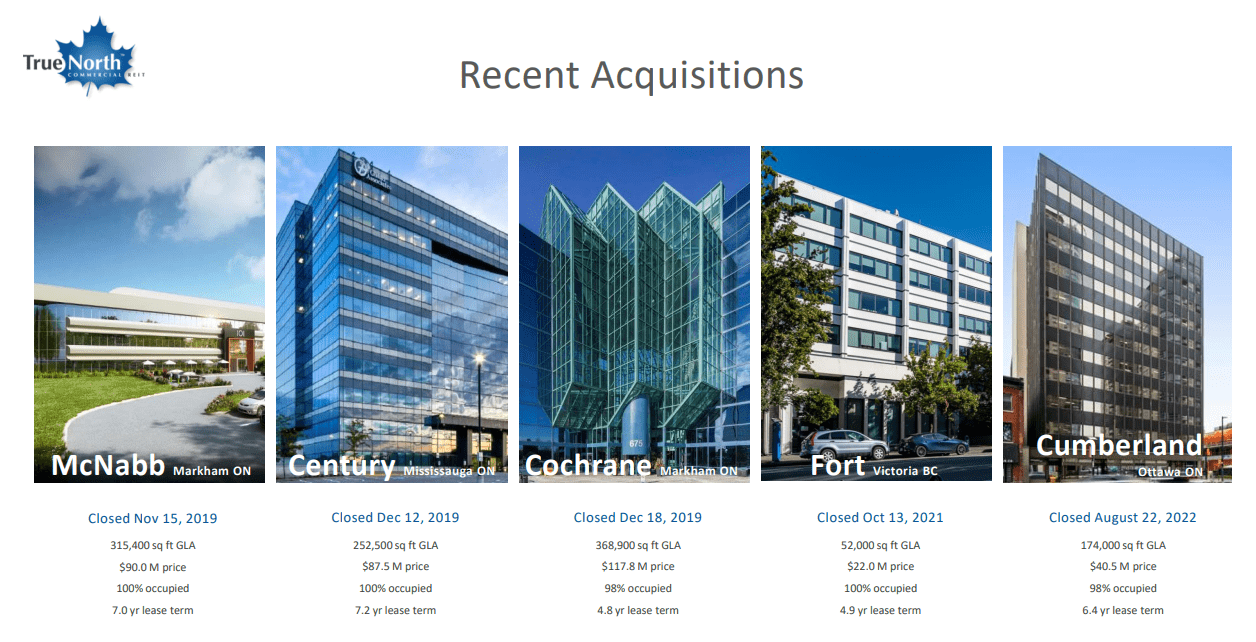

Till rather recently, True North was expanding its office property portfolio.

{kind=link}

True North Q1-2023 Presentation

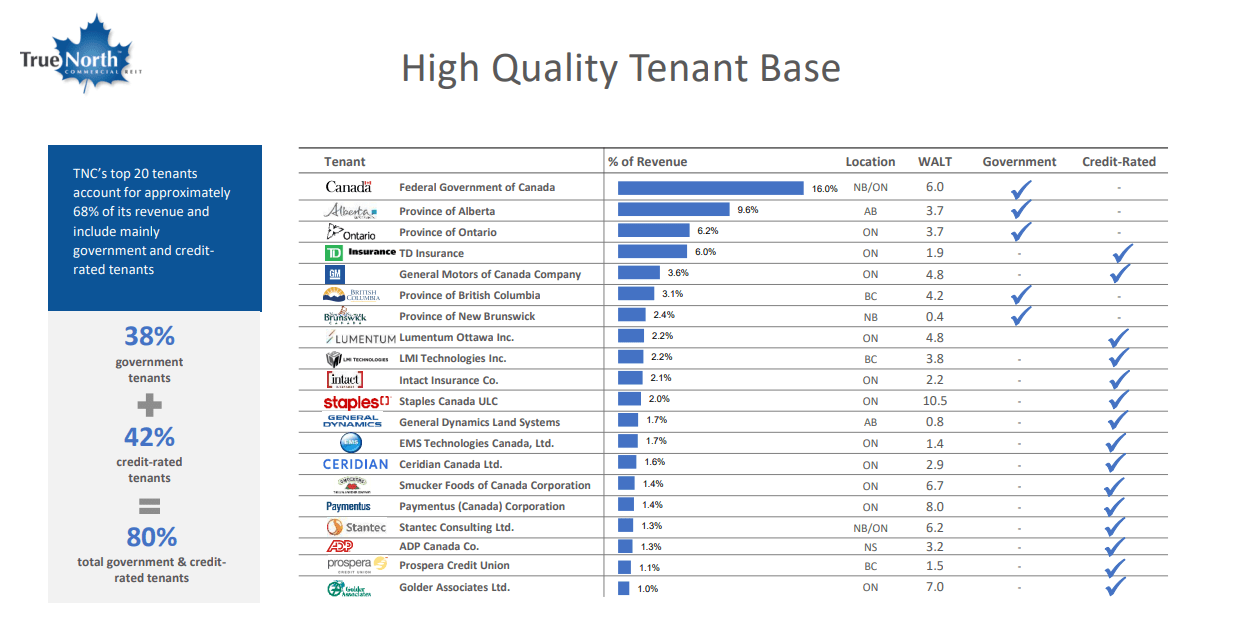

The tenant base continues to be exceptional, with 80% being Government entities or credit rated.

{kind=link}

True North Q1-2023 Presentation

Of course, as we have argued in the past, credit rated tenants are generally only good as far collections of rents are concerned. This was helpful in the earlier stages of the pandemic, where True North did better than most other REITs. But today this is a mild negative. Highest rated tenants have the widest selection of properties and maximum leverage to negotiate. This could include lower rent, larger space, more tenant incentives, or a combination of the three.

In Q1-2023, True North did renewals of about 125,000 square feet.

{kind=link}

True North Q1-2023 Presentation

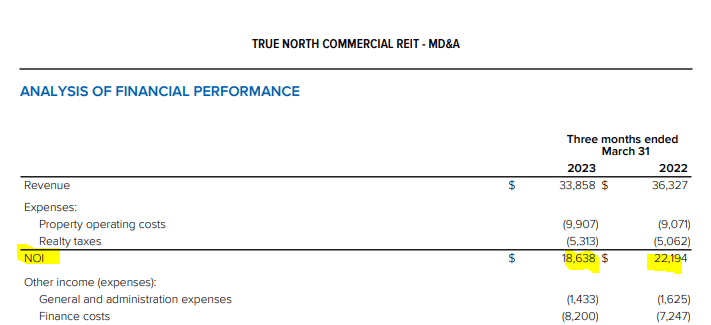

The weighted average term for those combined numbers was about 3.83 years, which is under the current weighted average for the whole portfolio. We also want to add to this the fact that the total portfolio is close to five million square feet and to keep things steady, you should see annual renewals of about 1.00-1.1 million square feet. On a quarterly basis, this works out to about 250,000 square feet. This is where True North has been falling painfully short. It is really not their fault here. Tenants are being wooed across the board, and they can often find smaller spaces that work better for them. These are now coming with big tenant incentives and usually lower rates per square foot as well. The lower occupancy levels are now bleeding into the revenue and net operating incomes.

{kind=link}

True North Q1-2023 Financials

NOI has dropped 17% year over year, which is pretty substantial when you hold has much debt as True North. Adjusted funds from operations (AFFO) is down 28% year over year.

{kind=link}

True North Q1-2023 Financials

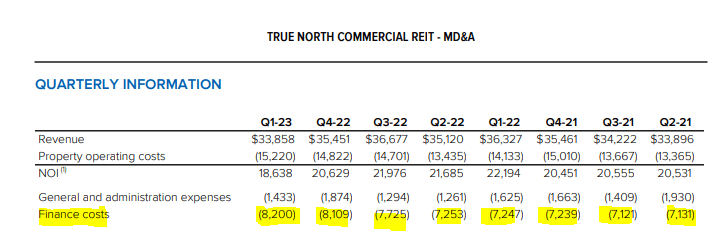

The culprit here is the rising finance costs, and the REIT has seen this expense rise steadily quarter after quarter.

{kind=link}

True North Q1-2023 Financials

It still has the Herculean task of refinancing on a regular basis in this tough macro environment. All things considered, the last quarter's refinancing rates were rather low.

During the quarter, the REIT refinanced a total of $31,121 of mortgages, one with a fixed interest rate of 4.83% (five-year term) and one with variable interest rate at prime plus 1.5% (one year term). The refinancings provided the REIT with additional liquidity of approximately $5,700. The REIT's weighted average term to maturity of its mortgage portfolio is 3.14 years with a weighted average fixed interest rate of 3.63%.

Source: True North Q1-2023 Financials

What we mean by that is 4.83% seems low for office properties today, but it will still crimp True North's cash flow. You can note that their weighted rate is still a good deal below their new mortgage rates. They also have an extremely short weighted average term to maturity. This seems to be a Canadian thing, where most REITs abused the length of their debt terms. All of them had been grazing the short end, with Artis REIT ( AX.UN:CA ) ( ARESF ) being the worst of the bunch . This feature makes them generally non- investable in an hostile environment.

Outlook & Verdict

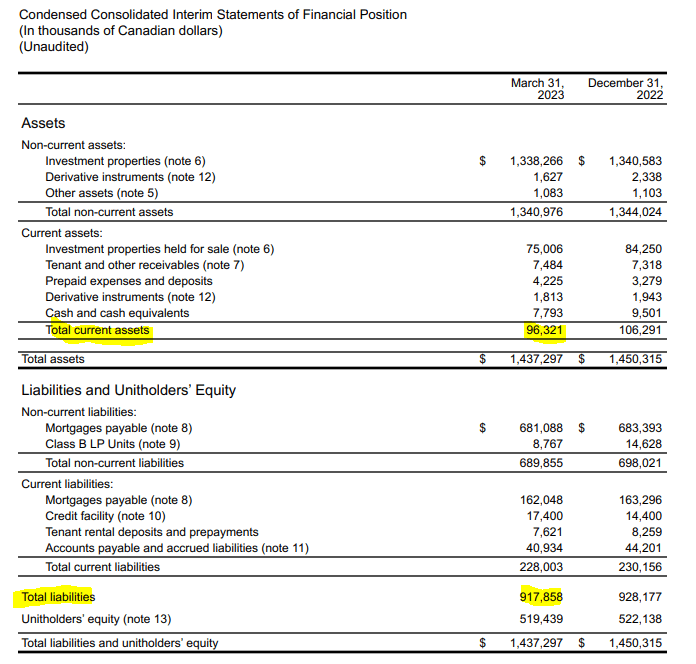

The 11-cent quarterly AFFO rate gives the REIT a price to AFFO ratio of near 6.0X. Is that cheap? Possibly in a pre-2020 world. Today, not at all. Most office REITs in the US are trading at low single digit multiples. We argue that that is not cheap, as most have existential risks. On the Canadian side we highlighted Slate Office REIT which we think gets wiped out eventually. On the US side we highlighted the risks for Hudson Pacific Properties Inc. ( HPP ) where even a 4X multiple was not enough for us to get excited. In the case of True North, there are secondary complicating factors like a very high debt load and very short-term leases and debt maturities. We also have $800 million off of net debt (defined by us as total liabilities less current assets) and we don't think the current properties could comfortably wipe out even that amount in a distressed asset sale.

{kind=link}

True North Q1-2023 Financials

Obviously, we are using different cap rates than management. That difference comes from what we are valuing these properties at when the current leases expire, rather than where they stand today. So we see a grinding path lower. But from a trading standpoint, it is not a slam dunk short as it was previously. We are hence upgrading it to a hold and noting that we have closed out our short position as well. We think anyone wanting office exposure should consider H&R REIT ( HR.UN:CA ), ( HRUFF ) as it has the best complementary assets to allow a chance of success.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

True North: Upgrading To A Hold After Brutal Three Months