HEAR - Turtle Beach: Get Out While You Still Can

Summary

- Turtle Beach reported very poor second quarter results. Sales were down by almost half year over year.

- The company slashed guidance. The business is now expected to lose $0.90 to $1.35 per share this year.

- The business has extremely high inventory levels. It will likely have to convert some of it into cash at a discount.

- I have doubts about management’s guidance, even after the latest cut. I think the justifications for fourth quarter revenue reacceleration are insufficient.

Investment Thesis

Like many gaming stocks, Turtle Beach ( HEAR ) saw a huge boost in sales and profit due to the pandemic. Unfortunately, it looks like this spike in demand was transitory. The company is dealing with excessive inventory, heavy guidance cuts, and a deteriorating balance sheet.

The company’s products are solid, and its market share is good in several verticals. But all of these products are tied to a declining market . Management’s current guidance factors in a return to year over year growth before the end of the year. I’m not sure this will happen, and the situation could get ugly if it doesn't.

Severe Sales And Profitability Headwinds

Turtle Beach’s results have fallen just as quickly as they rose. The company reported $41.3 million in revenue for the last quarter, missing analyst estimates by over 16%. This is down by almost 50% from $79 million one year ago. The company’s gross margins cratered by almost half. Management reported the first unprofitable twelve-month period since well before the pandemic. The business is now losing money on its core operations. It’s unclear when things will get better.

{kind=link}

Turtle Beach Second Quarter 2022 Earnings Presentation

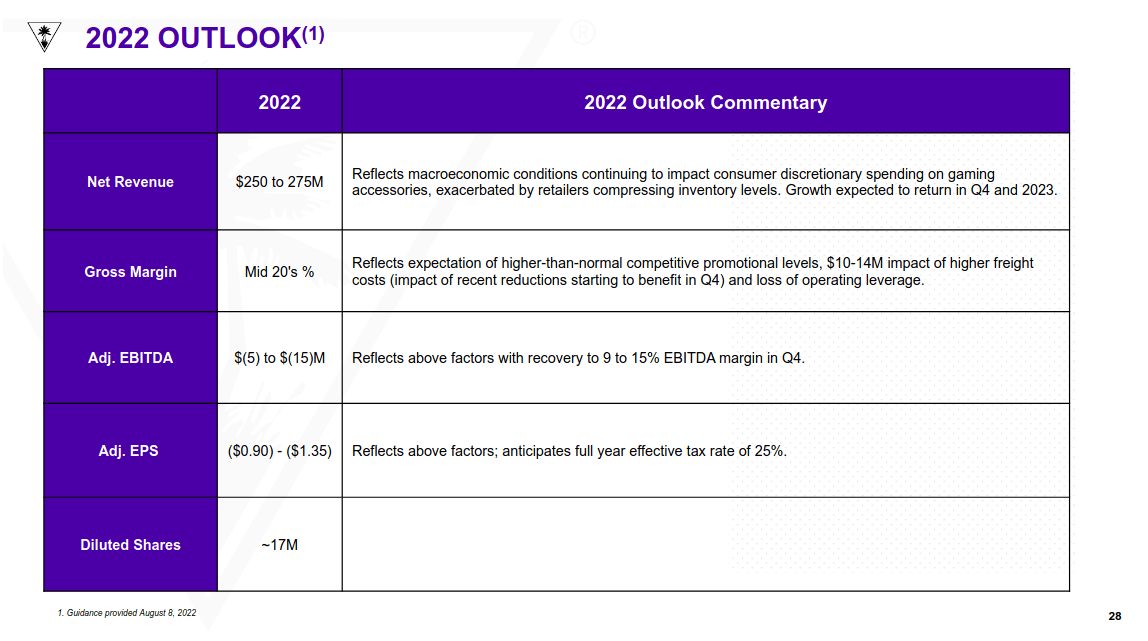

Management’s updated guidance is also finally starting to reflect reality. They slashed their revenue outlook to a range of $250 million to $275 million. This projection is down by as much as 35% compared to the company’s previous guidance.

Profitability has also suffered tremendously. In its fourth quarter guidance , the company projected $30 to $40 million in adjusted EBITDA. This would translate to $0.70 to $1.20 in earnings per share. Now, the company expects an adjusted EBITDA loss of $5 million to $15 million and $0.90 to $1.35 earnings per share loss.

Management blamed the bulk of their underperformance on a rapidly deteriorating macroeconomic environment. On their earnings call , the company cited data indicating that console headset demand was down 30% year over year. This is a frightening result for the company. The company has established strong products and a high market share in this category . The small product segment makes up about 75% of the company’s revenue.

{kind=link}

Turtle Beach FY 2021 10-K Filing

The PC gaming accessories market has been hit hard as well. The company had relied on this segment for a lot of their growth projections. The company said that demand is down by 20% and cut guidance accordingly. I like the company’s acquisitions of ROCCAT and Neat Microphones . But they don’t provide the revenue diversification the company needs during a time like this.

Excess Inventory And Retailer Risks

The most concerning challenge facing the company is their extremely high inventory levels. This is made worse by the company’s heavy exposure to retailers.

At the end of the last quarter, the business had 328 days of inventory on its books. This is one of the company's highest levels on record. Turtle Beach's own historical average over the past eight years is just 103 days. It’s over three times the inventory levels of Corsair ( CRSR ), a company that is in a similar financial situation. All of this inventory has holding costs, which may further hurt the company’s cash flows.

Turtle Beach’s heavy exposure to retailers compounds the problem. The company’s latest 10-K revealed that five retail customers make up almost two thirds of sales. The business is heavily exposed to Walmart, Target, and Amazon. This is when retailers are reporting excess inventory and an unexpected decline in consumer spending . Electronics, appliances, and gaming are some of the worst performers .

On their last earnings call, management said that they expect to convert much of this inventory into cash over the remainder of the year. They specifically discussed the elevated promotional environment.

Well, in a period like this year, where competitors and retailers have high inventories everybody’s been active and running promotions in all forms; discounting as well as, again paying for additional shippers and promotional activity with retailers. And we’ve participated as well, but we’ve tended to be a bit more conservative and going into the second half as has been now fully reflected in both the revenue guidance range and the gross margins which get impacted by the promotional level. That our guidance there reflects us competing more actively in what we believe will be above normal promotional environment for the rest of the year.

I think the demand environment will be a persistent headwind across the next year. A lot of consumer electronics companies have very high inventory levels . This is especially true of those in the gaming space, like Corsair . I believe that investors should exercise caution in this space right now. It looks like gaming peripheral businesses may have to cut prices just to generate cash. I think this will introduce sustained downwards margin pressure across product categories.

Uncertain Guidance

Even after heavy cuts, I think there’s a risk that management’s current guidance is too optimistic. The company’s guidance is assuming a huge sales reacceleration in the back half of the year. Management is forecasting a return to year-over-year growth by Q4.

{kind=link}

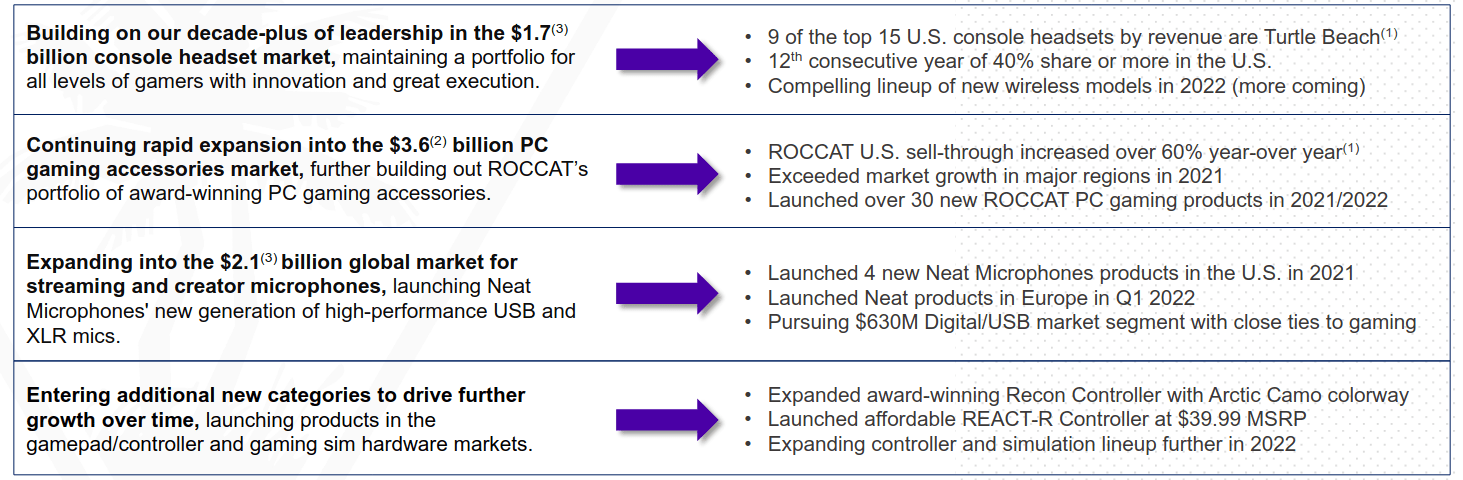

Turtle Beach's Growth Strategy (Turtle Beach Second Quarter 2022 Earnings Presentation)

I don’t think management has provided sufficient evidence of this dynamic. Their justification seems to be that the video gaming industry as a whole is growing, and therefore their specific accessories will inevitably see massive sales growth. Their earnings calls repeatedly cite projections of various products’ total addressable markets. This is their primary evidence of long-term revenue growth. It may be relevant to their flagship console headsets. But having a large market doesn't necessarily translate to sales.

Management’s credibility is already strained due to excessively optimistic guidance. During their first-quarter earnings call, they maintained their revenue and profitability guidance. By that point, there should have been ample evidence of the current bearish trends. I think we could see further guidance cuts from here.

Cash Burn, Acquisitions, And Valuation

In the long term, I think that Turtle Beach’s prospects look a little bit better. In spite of my criticism, the company does have solid products. Its brands maintain market leading positions in multiple key verticals. For example, the company has nine of the top 15 console gaming headsets on the market. If the business survives these headwinds, they could come out fairly strong. The question is how dire the current situation is.

{kind=link}

Turtle Beach Second Quarter 2022 Earnings Presentation

The business is trading at about 0.5 times forward sales. I think this is an acceptable price for a company with this margin profile. The company’s long-term growth targets would even make shares seem reasonably valued. But I can't take this information at face value. It would require believing management’s current guidance. That guidance has been wildly inaccurate in past quarters.

Turtle Beach’s cash position is deteriorating. The last balance sheet showed $10.9 million in cash compared to $15.7 million in borrowings. In the past, management has bragged about their low net debt levels. But their cash has dwindled, and the company has started to take on debt. In fact, the last quarter marked the first time in years that the company's debt exceeded cash on hand.

The business is burning over $20 million a quarter in free cash flow. It looks like the company is going to have to sell their inventory in order to fund operations. If the demand environment doesn’t improve, that may require taking a loss on some of their holdings.

Turtle Beach has strong products and a relatively cheap valuation. Because of this, I think the company could be a good strategic acquisition. But this doesn't seem likely at the current time. The company announced that they had received interest from multiple buyers. All of these buyers backed out, likely due to market volatility and the company’s worsening financial position. This is disappointing to investors who may have taken management’s decision to decline a $36.50 per share cash offer as a bullish sign.

Final Verdict

Turtle Beach’s sales and profitability have rapidly deteriorated. At this point, a lot of the company’s bullish case relies on a large spike in demand. I acknowledge that this is possible. But I think most evidence points to a sustained pullback in consumer gaming spending. I think there's limited upside compared to the very high risk of this investment. For these reasons, I strongly recommend avoiding this stock.

For further details see:

Turtle Beach: Get Out While You Still Can