TWLO - Twilio: Q3 Was Not Good Enough

2023-12-07 10:56:11 ET

Summary

- Twilio had a decent quarter, with its stock up 25% since earnings release.

- Revenue increased by 5% on a reported basis and 8% on an organic basis.

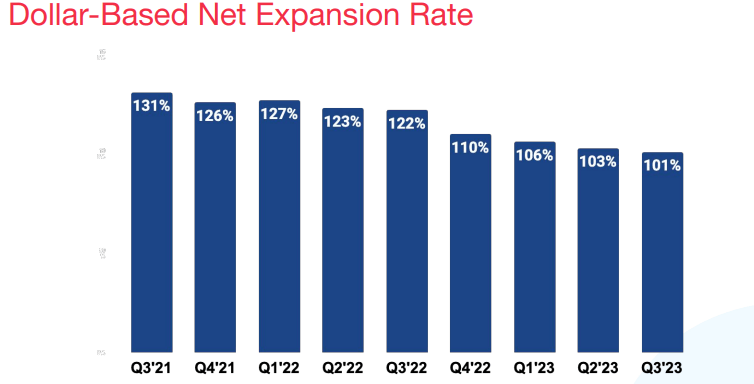

- The Dollar-Based Net Expansion Rate (DBNER) decreased to 101%, indicating challenges in the Data and Applications segment.

- As such, we currently rate Twilio as a sell.

This is my earnings review of Twilio's ( TWLO ) latest quarter.

Overall, Twilio had a pretty decent quarter. The stock is now up close to 25% since its earnings release on the 8th of November, while partially due to the fact the market received the earnings well. On the other hand, the market saw a nice rally during November, with SPDR® S&P 500 ETF Trust (SPY) being up almost 4.50% over the same period.

Ycharts

The Numbers

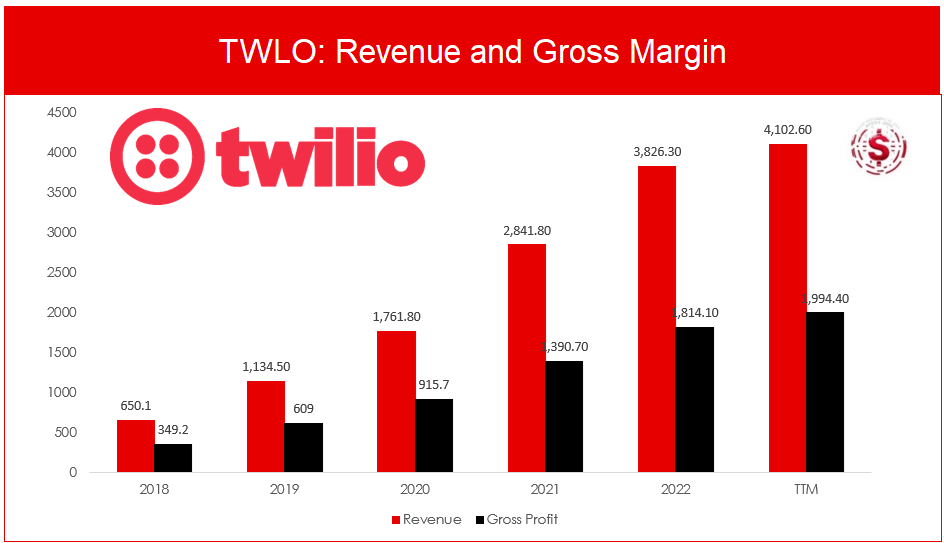

First, let's take a quick look at the historical growth of Twilio. As you can see, Twilio has experienced solid growth over the years but isn't growing as fast anymore. We have seen this with plenty of high-growth companies over the last 2 years.

{kind=link}

In my last article on Twilio , I mentioned that Twilio, like most hyper-growth companies, is now focusing on the shift to profitability.

As such, it is good to see that the company had a double beat this quarter, with revenue being up 5% and 8% on a reported and organic basis, respectively.

This is an increase to $1.034 billion, a beat of $41M or 4.1%. In addition, Non-GAAP EPS came in at $0.58, a beat of a whopping $0.22 or 61%, which is significantly better than expected.

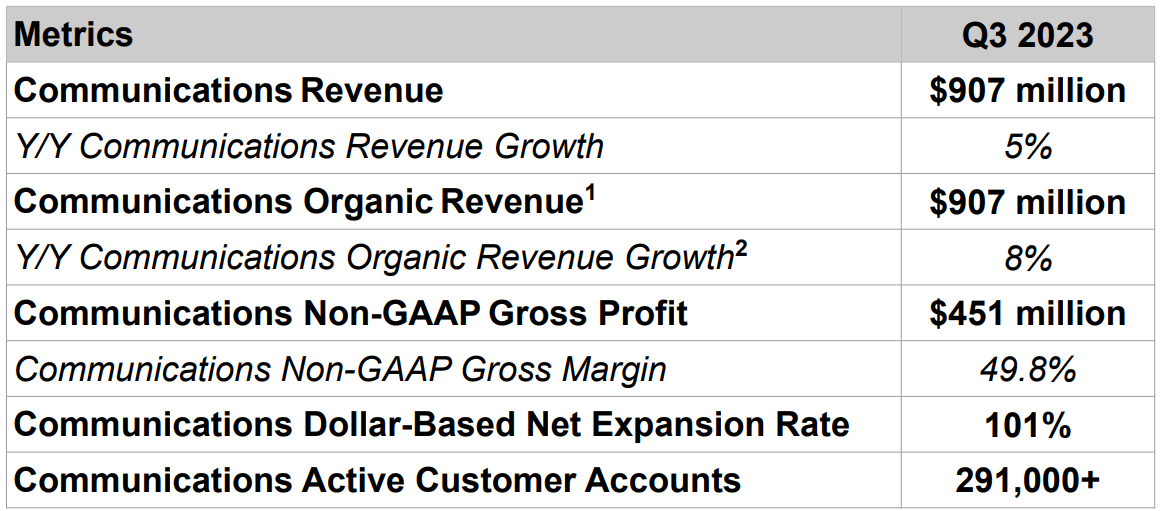

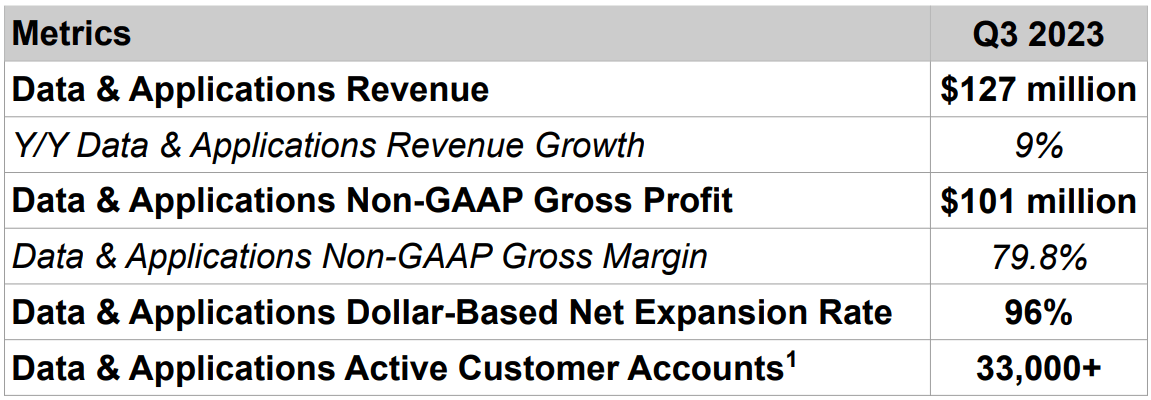

Revenue total of $1.034B consists of $907 million from the communications business, which is up 5% year-over-year. The remaining $127 million can be attributed to TD&A, which experienced 9% growth year-over-year.

TWLO Q3 Earnings Report

All in all, TWLO delivered a record quarter of non-GAAP income from operations and free cash flow. Furthermore, the company exceeded its YTD target of $250 to $350 million in non-GAAP net income, as the company reported $360M year-to-date.

Now, on to the pain point, the Dollar-Based Net Expansion Rate, also known as the DBNER. Unfortunately, the DBNER decreased further to 101% in Q3 of 2023, down 21% compared to the same quarter last year.

The DBNER of 101% is simply not good enough if we are being honest. I looked deeper into it and found out that the communications business had a DBNER of 101%, which is 104% if we exclude crypto consumers. The weak link was the Data & Applications (DT&A) DBNER, which came in at 96%.

{kind=link}

The weakness here was mainly driven by higher contraction and churn among Segment users. One analyst asked how the macro is still impacting Twilio and how they are trying to mitigate these challenges.

CFO Aidan Viggiano responded with the following :

So we continue to see volumes remain stable in the quarter. So that's been two quarters in a row, second quarter and third quarter, we've seen volumes stabilize, and that played out through the third quarter. Now, when you look at it at an industry level, we do see some verticals presenting a headwind. We talked about crypto and social and messaging.

But when you look at the other kind of larger industry verticals, we are seeing growth in those. And so our overall growth rate is somewhat masked by the headwinds that we are seeing on crypto and social media as well. So we do feel good about where the business is. I'd also say, as you think about the dollar based net expansion rate for that business. So it's lower than it historically has been. It's 101% in the quarter, and it's an 8% growth rate overall, right. So the vast majority of the growth is coming from the new customer base.

Important to mention is that churn is historically low, according to Viggiano, but contraction is higher and expansion is lower relative to historical levels.

All in all, Twilio is experiencing some industry-specific headwinds, but they are seeing stabilization.

CEO Jeff Lawson pointed out that crypto is the main headwind as of now. Furthermore, it is important to mention that Mr. Lawson said the following, which is encouraging to hear:

But I think if you look at several of the other industries in which we participate; we are seeing pretty good growth and I think that generally makes us feel pretty good. As Aiden alluded to volumes have been stable. That certainly feels pretty encouraging and I think the way that we've dialed the business and the way that we've addressed our cost structure, I think in spite of whatever it is that kind of comes at us for the foreseeable future, we feel pretty good about the way that the business is sized. And so I think now we're prepared to kind of execute through whatever that environment is.

This shows that he is confident that Twilio is now weathered against whatever macro environment is coming at them.

Furthermore, Twilio has now executed $620 million of share repurchases as part of the $1 billion share repurchase program they announced in February. This means they bought back an additional $130 million worth of shares since July.

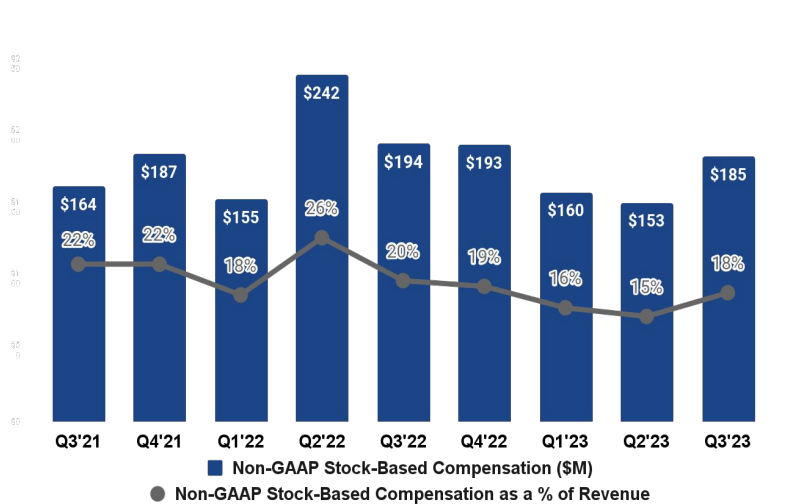

On the other hand, we see that Non-GAAP SBC as a percentage of revenue is increasing again, which is something we don't like to see.

As you can see below, the SBC as a percentage of revenue increased to 18% or $185 million, this is similar to Q3 of last year. As such, we can say that the share repurchases this quarter were merely used to offset dilution caused by the SBC, and they don't even cover the dilution of Q3.

{kind=link}

Communications Business

The communications business revenue came in at $907 million, which corresponds with 8% organic growth.

Interesting to see is that Twilio keeps on innovating, and they launched a bunch of new products and tools, they are working on integrating more artificial intelligence ((AI)) into their ecosystem. For example, the company announced some new product innovations in customer AI, including Voice Intelligence, Traffic Optimization Engine, Branded Calling, SendGrid Engagement Quality, and Fraud Guard.

Furthermore, they also streamlined their go-to-market model and expanded some of their global partnerships, most notably they reached an agreement with SoftBank ( SFTBY ) to offer Twilio's services in Japan.

{kind=link}

TD&A Business

Now, let's take a look at one of the most important parts of the TWLO growth thesis, the TD&A business. The revenue came in at $127 million, which corresponds with a 9% YoY growth.

In the last earnings review, I mentioned that the TD&A business was in a significant downtrend as Q2 2023 revenue only showed 12% growth year-over-year and that this isn't really confidence-inspiring. Unfortunately, this decline further continued in Q3.

As such, I believe the company's primary focus should be on reaccelerating growth in TD&A. The management mentioned that they are seeing encouraging signals, but unfortunately, the numbers aren't really showing it so far.

Nonetheless, there were some positives for the TD&A business as well. Twilio gained some exciting new customers across both Flex and Segment, including a competitive seven-figure deal with a leading insurance company.

When we take a look at Segment's performance, Twilio processed over 12 trillion data events in the last 12 months, resolving those data points into over 100 billion customer profiles on behalf of brands. Jeff Lawson mentioned the following regarding this:

This is the basis of our market share leadership recognition and underscores the need for a real-time CDP in the market, which Segment delivers. In Q3, the Segment team signed a deal with a leading fintech company and long-standing Communications customer who is driving a product-led growth initiative.

It is good to see that the company is making some big deals and continues to expand its business. Nevertheless, I have to admit that the TD&A business needs to reaccelerate its growth soon as it has been disappointing over the last year.

{kind=link}

Challenges and Focus

The main challenge remains the much-needed switch to profitability. The company is on the right track operating margins came in at 13%, which is better than the expectations of 10%.

In addition, Twilio generated $206 million in operating cash flow and the financial position of Twilio remains strong with cash (and cash equivalents) of $677.9 million and ST investments of $3,179.5 million, in total this provides a $3.86 billion war chest, which is over 1/3rd of the company's current market cap.

As mentioned earlier, Twilio acknowledges macroeconomic challenges and specific headwinds, especially in the crypto and social media sectors.

Nonetheless, Twilio maintains its growth-oriented approach, with a dollar-based net expansion rate of 101% in the quarter. This figure, although lower than historical levels, signifies a focus on new customer acquisition, contributing to an 8% overall growth rate.

Notably, the company addresses the evolving landscape by proactively managing costs. CEO Jeff Lawson and COO Aidan Viggiano detailed structural changes that include a disciplined, focused approach to cost reduction, without compromising operational efficiency.

Nevertheless, there is no other way about it, TWLO is experiencing some issues with growth and a DBNER of 101%, which simply isn't good enough. This is the main reason for our sell-rating right now, the DBNER isn't showing any signs of improvement.

Twilio mentioned that it stays committed to achieving profitability, which is evident with a non-GAAP operating profit for two consecutive quarters. They have been struggling to find a balance between growth and financial stability, but it looks like the company is making moves in the right direction.

In addition, the company raised its guidance for the remainder of the year. Q4 and Full-year non-GAAP income from operations is now expected to be between $115 million to $125 million and $475 million to $485 million, respectively.

Revenue guidance for Q4 is $1.03 billion to $1.04 billion, which is pretty similar to the Q3 results.

Twilio.com

Conclusion

All in all, this is a solid quarter from Twilio. Nonetheless, we must admit that growth, especially for the TD&A component of the business needs to reaccelerate as the management mentions. In addition, the DBNER of just 101% simply isn't good enough and that must improve as soon as possible.

While the communications business exhibited an 8% organic growth, the TD&A business faced headwinds with a 9% YoY growth, necessitating a reacceleration for sustained growth.

Twilio's management emphasizes a shift towards profitability, evident in the achievement of non-GAAP operating profit for two consecutive quarters.

The Dollar-Based Net Expansion Rate (DBNER) of 101% in Q3, which is a decrease of 21% YoY, highlights challenges, particularly in the Data and Applications (DT&A) segment.

The TD&A business's growth trajectory, while showing some positive signals with significant deals, needs acceleration. Twilio's strategic focus on integrating artificial intelligence into its ecosystem and global partnerships, such as the agreement with Softbank, reflects its commitment to innovation and market expansion.

Nonetheless, the company showed resilience with a double beat showing efficiency gains, and further focus on customer AI and other AI initiatives. In addition, the significant war chest of 1/3rd of the company's market cap further helps the company in the current environment.

To conclude, Twilio is a growth company that is currently struggling due to unforeseen headwinds. Nonetheless, it remains a leader in its business and has plenty of potential once these headwinds pull away. For example, declining interest rates would more than likely help Twilio's growth to accelerate.

Still, after the recent run-up and the bad DBNER Twilio isn't attractive at this moment in time. As such, we currently rate the company as a sell. Once we see DBNER improve and growth reaccelerate Twilio will be on our radar once again, but for now we believe there are better opportunities out there.

For further details see:

Twilio: Q3 Was Not Good Enough