TWLO - Twilio: Stunning Recovery Too Fast For My Liking (Rating Downgrade)

2023-12-24 09:30:00 ET

Summary

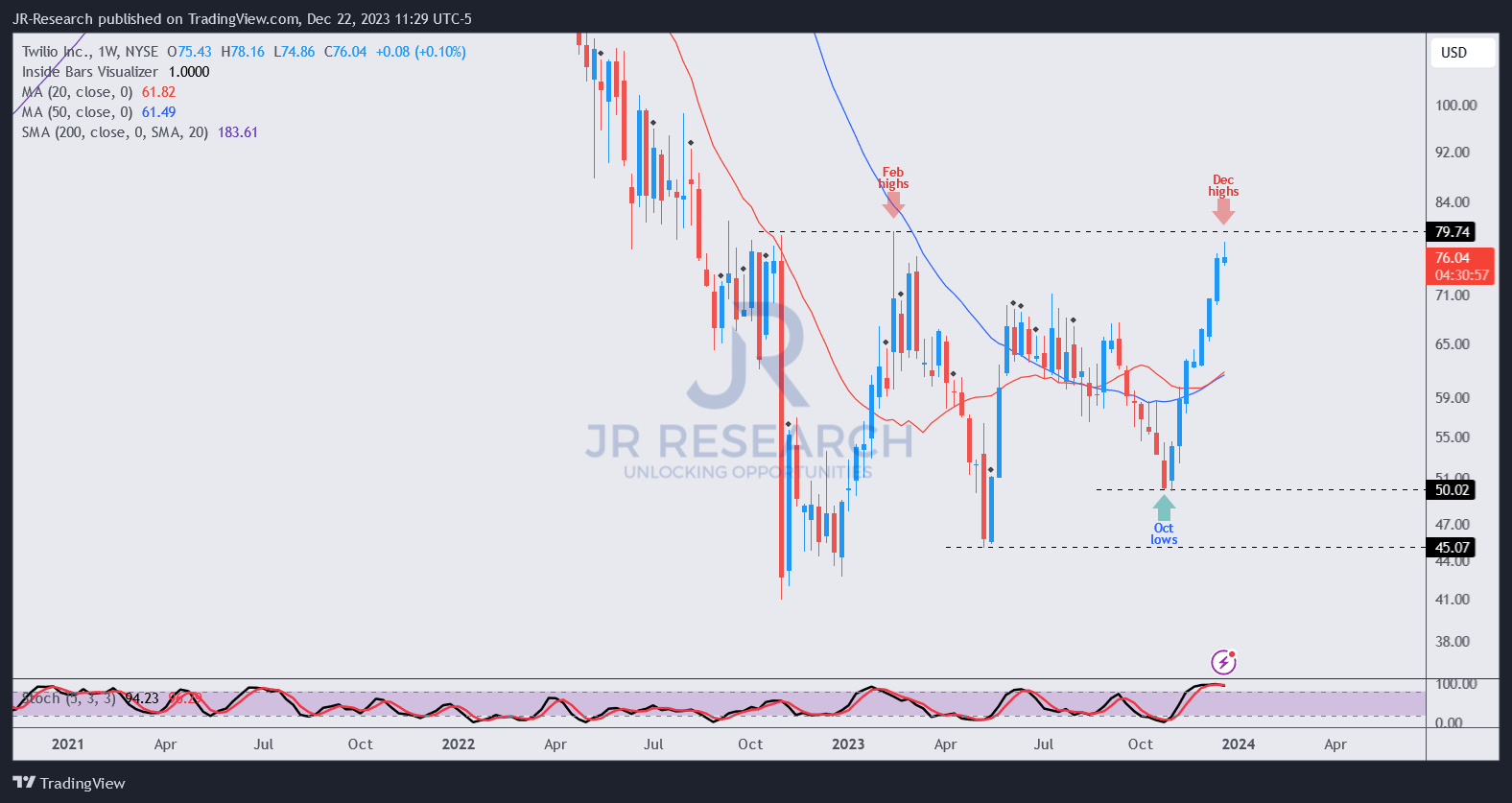

- Twilio investors have witnessed a significant recovery in TWLO over the past three months, as it bottomed out resoundingly in late October, gaining nearly 55% through this week's highs.

- Twilio is turning up the heat as it continues its sustainable growth phase, focusing on operating leverage.

- The company is undergoing a leadership change in its smaller data and applications segment, which is critical to driving its margin accretion.

- I explain why TWLO isn't expensive and remains a solid stock to add at steep pullbacks.

- With the surge leading TWLO toward its early 2023 highs, I assessed earlier buyers could use the opportunity to take profits, leading to more intense selling pressure. It's better to wait patiently now.

Twilio Inc. ( TWLO ) investors have witnessed a significant recovery over the past three months since my previous update in September 2023. While my Buy thesis was tested in the market downdraft in October 2023, high-conviction dip-buying returned at TWLO's October lows. Observant investors familiar with Twilio's communications platform likely aren't surprised that TWLO bottomed out about two months ago.

TWLO had already traded at an attractive valuation at my previous update, bolstering its appeal further as it collapsed toward its October lows. With TWLO up more than 55% through this week's highs, I gleaned it timely to reassess whether adding exposure at the current levels is still reasonable.

Twilio has two key segments driving its topline growth. The company's main communications platform remains its most important growth driver, accounting for nearly 90% of its revenue base in Q3 . In addition, it has a data and applications layer that delivered 9% YoY growth in Q3. Notably, Twilio's operating leverage improvement is predicated on the success of its much smaller business, which generated an adjusted gross margin of nearly 80%, compared to the corporate average of about 50%.

However, that business is undergoing a leadership transition, with the former head Elena Donio's resignation effective on December 15. As a result, CEO Jeff Lawson has stepped up to helm the unit as the company looks for a long-term replacement to drive growth further. Lawson's decision to steady the ship suggests the criticality of this segment as Twilio diversifies from its lower-margin communications business into a higher-margin layer to drive profitability further.

While there could be near-term execution risks, Twilio's decision to shake up its executive leadership could suggest that the company may not be satisfied with the current growth cadence. At a recent conference , CFO Aidan Viggiano stressed that the company is focused on "analyzing and improving sales dynamics." As a result, there could be a fundamental shift in its go-to-market strategy, aligning its GTM toward "a more technical buyer persona, which aligns better with [Twilio's] product strength." Consequently, I urge TWLO investors to watch this space closely, given its importance in driving medium-term profitability growth.

Wall Street analysts remain confident in Twilio's ability to improve its bottom line. Twilio has a distinct network effect moat that spans over 180 countries worldwide. As a result of its global platform, Twilio's scale and coverage also impose switching costs on its users as they contemplate the need to search for a more cost-effective platform to replace Twilio's offerings.

Moreover, Twilio has moved past its aggressive topline growth phase to focus on delivering a more sustainable approach. The execution has been remarkable, which continued in Q3. Accordingly, Twilio is expected to deliver an adjusted EBIT margin of 14.1% by FY25, up from this year's estimated 11.7%. The conversion to free cash flow or FCF remains robust, with an estimated FCF margin of about 11.9% in FY25, up from 5.7% this year. As a result, I believe Twilio's moat advantage could improve as it scales, sustaining its ability to fend off competition in its lower-margin comms layer. Therefore, investors must assess the impact of possible changes to its GTM as it searches for a new long-term leader to replace Donio.

TWLO last traded at a forward EBITDA multiple of 13.4x, below its IT services peers' median of 16.4x. Seeking Alpha assigned TWLO an attractive "B" valuation grade, notwithstanding the surge over the past two months. In other words, I believe the market has likely reflected adequate execution risks on its FCF growth inflection, given the uncertainties elucidated earlier. As a result, I believe the opportunity to get on board TWLO remains in the earlier stages, even though a welcomed pullback shouldn't be ruled out.

{kind=link}

TWLO's price action has signs of a surge that could precede a steep pullback if the upward momentum stalls again at the $80 zone. While I remain confident that TWLO's valuation isn't expensive, its price action isn't constructive, suggesting earlier dip-buyers could look to unload more aggressively if TWLO fails to sustain a decisive breakout above the $80 zone.

Therefore, TWLO holders looking to add more shares should consider waiting for a welcomed pullback first and assess its subsequent consolidation zone before pulling the buy trigger. Does it matter? Of course, it matters. Remember that the investors who bought at its February highs are still underwater, while those who bought at its October lows were up more than 50% through this week's highs.

Taking on attractive risk/reward setups is a critical guiding principle that investors shouldn't throw caution to the wind, particularly after such a massive surge attracting buyers in a hurry.

Rating: Downgraded to Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Twilio: Stunning Recovery Too Fast For My Liking (Rating Downgrade)