USAU - U.S. Gold: Things To Consider Before Jumping On The Bandwagon

Summary

- U.S. Gold looks attractive from a valuation perspective.

- The CK Gold project's Pre-Feasibility Study highlights promising low-cost, long-life gold mining prospects.

- Project permitting and financing are the two key considerations that will impact the future of the CK Gold project.

- The final Feasibility Study on the project will soon be released and will better define key project parameters.

- The stock has strong leverage to gold prices and is a 'hold' in my view.

Thesis

US Gold Corporation ( USAU ) is a US-based gold exploration and development company having stakes in three mining projects located in Wyoming, Nevada, and Idaho. The CK (read: Copper King) Gold project is the company's flagship asset that's in the later stages of exploration and is likely to advance to the development stage soon. Our discussion will be focused on a detailed analysis of the company's flagship asset since developments on this project can have a lasting impact on the share price.

In this article, we look at USAU's valuation based on an NPV analysis of the CK Gold project. If things go as planned (and that's the condition), the CK Gold project alone could provide a significant upside to the share price in the medium-to-long term. That said, we will incorporate in our discussion the important challenges that need to be overcome before the stock could realize its full growth potential. Let's get into the details.

CK Gold - Promising Mining Economics

In November 2022, USAU sold its interest in the Maggie Creek property (in Nevada) to Nevada Gold Mines (or NGM) against an upfront cash payment of $2.75 MM, together with the right to earn a 0.5% NSR (read: Net Smelter Return) Royalty if NGM exercises the option and acquires the Maggie Creek Property. Currently, USAU's focus is to advance the CKG project toward development and the disposal of the Maggie Creek Property strengthened the company's liquidity position when it needed funds for exploration (and possible future development) at the CKG project.

The PFS (read: Preliminary Feasibility Study) on the CKG project was released in December 2021 , and shed light on the project's mining appeal. Let's take a quick look at the key parameters of the CKG project, as mentioned in the 2021 PFS.

| Project Parameters |

| 2021 PFS |

| Type of mine |

| Open Pit |

| Mine Life (or LoM) |

| 10 years |

| P&P Reserves |

| 1.44 Moz AuEq |

| Processing Capacity |

| 20,000 tpd |

| Annual Avg. Production (Years 1-5) |

| 122,000 AuEq oz |

| LoM Avg. Annual Production |

| 108,000 AuEq oz |

| LoM AISC |

| $800/oz AuEq |

| Initial Project CAPEX |

| $222 MM |

| LoM Sustaining Capital |

| $15 MM |

| Payback Period |

| Between 1.8 and 3 years |

The above table highlights the high-margin production potential of the CK Gold project. At the prevailing gold prices of ~$1,865/oz (at the time of writing), the project could generate an operating margin of ~$1,000+ per AuEq (read: gold equivalent) ounce at an AISC (read: All-In-Sustaining-Cost) of $800/oz AuEq . In my view, CK Gold's estimated LoM (read: Life of Mine) AISC is better than the industry average that lies within the range of ~$1,000-1,200/oz.

NPV Analysis

An NPV analysis of the CK Gold Project takes five different levels of gold and copper prices. These numbers are taken from the 2021 PFS. Take a look at the table below:

| Scenario |

| Gold Price |

| Copper Price |

| IRR |

| After-tax NPV |

| Payback |

| Scenario-1 (Worst-case) |

| $1,425/oz |

| $2.85/lb |

| 21.7% |

| $143.5 MM |

| 2.9 years |

| Scenario-2 |

| $1,525/oz |

| $3.05/lb |

| 27.9% |

| $204.8 MM |

| 2.5 years |

| Scenario-3 (Base-Case) |

| $1,625/oz |

| $3.25/lb |

| 33.7% |

| $265.7 MM |

| 2.2 years |

| Scenario-4 |

| $1,725/oz |

| $3.45/lb |

| 39.3% |

| $325 MM |

| 2.0 years |

| Scenario-5 (Best-case) |

| $1,825/oz |

| $3.65/lb |

| 44.6% |

| $383.9 MM |

| 1.8 years |

At this point, it's worth mentioning that USAU's outstanding share count is merely 8.37 MM which can be increased if a certain number of share warrants and employee stock options are exercised. Nonetheless, the existing fully diluted share count is estimated to be ~10.5 MM shares.

For assessing the project valuation, we will assume that all those outstanding warrants and options will be exercised. If we divide the after-tax NPV estimates over the fully diluted share count, we get NPV/share ranging between $13.67 (worst-case) and $36.56/share (best-case). Compare these numbers with the current share price of $4.15, and we can figure out how USAU is trading at an attractive valuation based on the after-tax NPV of its flagship asset.

Other Considerations

Nonetheless, the above valuation assessment is subject to the following additional important considerations:

1) Discount Rate: The project's after-tax NPV is calculated using a discount rate of 5%, which is a conservative rate in my view. The company's PFS states that the fact that the bulk of revenue is split between sales of gold and copper suggests that the project may be less sensitive to cyclical swings in the prices of either individual metal .

{kind=link}

Although the company favorably views this revenue split as a hedge against cyclical swings in metal prices, I see things differently. In my view, mining projects whose future revenues are largely based on precious metals (such as gold, and silver) may be discounted using a rate between 6-8%. In such a case, a readily available market for metal output supports a low discount rate.

In contrast, hybrid-resource projects that entail notable revenue generation from both precious metals (gold in this case) and base metals (copper in this case) should be discounted using a rate between 8-10%.

Other factors that impact the discount rate must also be considered, including the following:

- Mining jurisdiction - The United States is generally considered a safe mining jurisdiction provided that the underlying project is permitted. The CKG project is located in the State of Wyoming, which has an average Mining Attractive Index Score of 72.46 versus the United States' average score of 72.61, based on the Fraser Institute's 2021 report . In my view, this factor points in favor of selecting a low discount rate.

- The project owner's size and prior working experience - A lower rate suits those mining companies which have prior experience in successfully advancing a project from exploration to development/construction. Since USAU is a junior exploration/development company, I believe this factor points against selecting a low discount rate.

- Stage of project development - Likewise, a lower discount rate suits those projects that are in the later stages of the mining life cycle. In the case of CKG, the company released the PFS in 2021 and is in the steps of preparing the final FS. Based on a favorable FS, it could be expected that the company's board will approve project construction, however, obtaining requisite regulatory permits and project financing will remain the key challenges (more on this later). In my view, this factor also points against selecting a low discount rate.

Based on the above discussion, I assume that the 5% discount rate is too low, and a more realistic rate should lie between 6-8%.

2) Project Permitting: Obtaining project permits could be a difficult task for mining companies (even in the US). In an uncommon development , the US Environmental Protection Agency blocked Northern Dynasty's ( NAK ) promising Pebble project in Alaska, and paved way for a potentially long legal battle between the company and the regulator.

Fortunately, USAU believes that its CKG project will not require any federal permitting. The company states in the PFS that two streams flowing through the Project site have been classified as "Waters of the United States" by the US ACoE (read: Army Corps of Engineers), however, none of the planned project infrastructure would impact these surface waters, therefore no federal permitting will be required .

In my view, the company is justified in its above-mentioned stance especially since the project was deemed non-jurisdictional by the ACoE based on a wetland survey and site inspection conducted in February 2021. Nonetheless, the company still needs the following permits for the CKG project:

- Permit to Mine

- Air Quality Permit to Construct and Operate

- Industrial Citing Construction Permit

- Stormwater Permit

- Permit to Construct Water Supply and Wastewater Facilities

- Operator Certification for Drinking Water Systems

- State Engineer's Office Permits for Water Use and Water-Related Facilities

- A permit from State Historical Preservation Office

- A permit from State Fire Marshall

- A permit from Laramie County where the CKG project is located

In September 2022, USAU submitted the Permit to Mine (along with the Mine Reclamation Plan) with the WDEQ (read: Wyoming Department of Environmental Quality). The Permit to Mine is an operating level permit but it's required before the commencement of project construction activities. The company expects to obtain a decision on this permit application within a year of filing the same. The company states in its September 2022 press release,

The Company understands that this permit has the longest lead-time and other permits can be obtained in a shorter period. Several other permit applications are either in-hand or in process, including applications with the State Engineer's Office for small impoundments for sediment and runoff capture, and wells.

The Company intends to submit an Industrial Siting Permit application in February 2023. Through this process, more specific information related to noise, traffic and social impacts of the areas affected by the proposed Project will be considered.

Keeping in view the above, I think it's likely that USAU will pass through the project permitting process. However, the timelines are important as they stretch well over a year. The project's mining dynamics could change based on the then-prevailing metal prices (more on this later).

3) Project financing: The CKG project's initial CAPEX is estimated at $222 MM. US Gold's financial statements for Q2 2023 (that ended on October 31, 2022) revealed that the company had cash worth $4.2 MM, which was further enhanced by Maggie Creek's disposal proceeds worth ~$2.75 MM. It's pertinent to mention here that US Gold's authorized share capital comprises 200 million ordinary shares and 50 million preferred shares, both with a par value of $0.01/share. As noted below, US Gold's fully diluted share count includes ~2.2 million warrants/options, having a strike price ranging between $5 and $14.50.

US Gold Presentation - February 2023

At the prevailing stock price of ~$4.17 (at the time of writing), all the above options/warrants seem 'out of the money'. However, a sustainable increase in gold prices could drive USAU's share price higher, and we could then see some of those options/warrants being exercised. This in turn would improve the company's liquidity position. Nonetheless, even if all the warrants/options are exercised, the company would still need funds for financing the initial project CAPEX. The company could go for equity financing (preferred option under the 2021 PFS), debt financing, or a mix of both.

In my view, an equity financing model will cost dearly to the existing shareholders because of potentially significant value dilution that would accrue from a sizable increase in the outstanding share count. In contrast, if the company goes for debt financing (on favorable terms), the principal repayments could be deferred to later years (year 5 and onward) in order to minimize cash outflows in the starting few years (in terms of future interest payments), thereby enabling the company to fund ongoing exploration activities/ sustaining CAPEX.

4) Feasibility Study: The company has completed field work related to the final FS on the CKG project, and the results are pending. It's expected that USAU will release the project's final FS soon.

The important question is, what improvements should we expect in the FS compared with the PFS?

2021 PFS highlighted P&P (read: Proven and Probable) reserves of ~1.44 Moz AuEq at an average AuEq grade of 0.7 g/t. This resource was based on the drilling results of 160+ drill holes spanning an area of 28,500 meters. The initial study also highlighted high-grade mineralization at the surface surrounded by a large, lower-grade zone with potential for expansion (in a bullish metal price environment).

The final FS would better define the CK Gold project's key parameters including reference metal prices, resource estimate, initial CAPEX, after-tax NPV, any resulting changes in the expected payback period, project IRR, the expected mine life, and LoM AISC. In addition to the above, the FS aims to incorporate an improvement to the gold recovery rate. Note that gravity and floatation test work conducted during the 2021 PFS showed copper recovery rates between 55-60% and gold recovery rates between 65-70%. Preliminary cyanidation of the flotation tailings indicates that gold recovery rates could be increased to 90%. Generally, a higher recovery rate helps a mine's cost performance. It is expected that the FS would shed more light on the project's potential recovery rates.

Another positive catalyst (though unrelated to the FS) is the fact that the project contains ~30 million tons of non-mineralized rock which is expected to be sold for ~$16-18/ton, providing for potential cash inflow between $480-540 MM in the future. These cash flows are in addition to the cash flows from the processing/sale of mineralized rock.

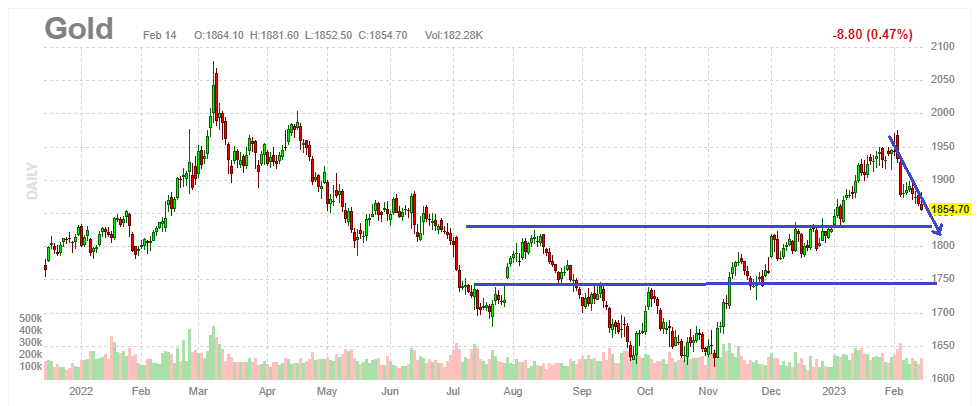

5) Gold prices: USAU's share price is highly leveraged to changes in gold prices, particularly when CK Gold's near-term milestones stretch well beyond a 12-month horizon (as discussed earlier). At present, gold prices are in the correction phase and could find near-term support within the range of ~$1,750-1,800/oz.

{kind=link}

The downward trajectory in gold prices was triggered by a strong US jobs report for January 2023 , which resulted in an expectation of enhanced spending and possible inflation. The Fed's response is to potentially increase interest rates to contain inflation. This, in turn, impacts the demand and prices of precious metals (including gold). Bottom line is, I expect this correction in gold prices to continue in the near term.

Investor Takeaway

The preceding discussion highlights US Gold's attractive valuation based on the NPV analysis of its flagship project (the CKG Project). Two key considerations will impact the share price trajectory in the medium-to-long term namely, project permitting, and financing. If USAU can overcome these challenges, the share price will witness a significant upside. In the near term, however, the prevailing volatility in metal prices (especially gold prices) will limit any notable upside in USAU's share price. Since I anticipate near-term consolidation in gold prices within the range of ~$1,750-1,800/oz, I believe the stock is a 'hold' at present.

For further details see:

U.S. Gold: Things To Consider Before Jumping On The Bandwagon