CA - U.S. Steel: How High Can You Go?

2023-10-02 06:41:44 ET

Summary

- U.S. Steel is exploring strategic options after receiving bids from several steel manufacturers, including Cleveland-Cliffs.

- The acquisition price for X shares could potentially increase by 10% to 27%.

- The company's valuation remains attractive compared to competitors, and the merger could provide synergy benefits.

Introduction

U.S. Steel ( X ) has announced that it is opening up all strategic options after receiving several bids. Steel manufacturers are looking for synergies and see opportunities at U.S. Steel. What makes U.S. Steel unique are its investments in mini mills and electric arc furnaces ((EAF)). Arc furnaces emit less carbon dioxide than blast furnaces. This reduces emissions that warm the climate. U.S. Steel supplies steel to wind turbines and will benefit from the Inflation Reduction Act (tax credits and other incentives). The IRA is a nice catalyst for the company, which is why I find the current stock price very attractive.

In my article, I first provide the timeline, offers, and opportunities. I examine the maximum acquisition price for U.S. Steel shares based on interest coverage and valuation. Furthermore, I am optimistic about the risk/reward of U.S. Steel. I see upside potential until it reaches the acquisition price.

Timeline

In August , several steel manufacturers announced interest in acquiring U.S. Steel. U.S. Steel is considering all options to create value for shareholders, the company and its stakeholders.

August 13, 2023

Cleveland-Cliffs ( CLF ) announced they are offering $17.50 per share in cash + 1,023 Cliffs' shares, which amounts to $33.50 per share for the entire company. At the current share price, this represents a return of only 3.1%.

However, U.S. Steel rejected the proposal because Cliffs deviates from the usual acquisition process. Cleveland-Cliffs wants U.S. Steel to agree to the price and terms of the proposal before signing the NDA. That poses a problem because U.S. Steel can no longer assess the potential risks and possible upsides and downsides.

August 14, 2023

Several other global steel producers also showed interest. On Aug. 14, the Danish company Esmark made an offer of $35 cash per share. However, Esmark withdrew the bid shortly thereafter. Arcelor Mittal showed interest but did not make an official bid. There was speculation that Arcelor Mittal would offer $38 per share. That's a lot higher than Cliffs'. Arcelor Mittal expects cooperation with the USW to be difficult.

August 17, 2023

The general trade union (USW) informed Cleveland-Cliffs on Aug. 17 that they have the exclusive right to bid for U.S. Steel. This makes Cliffs the only realistic buyer to take over the entire company. Under the terms of the USW, U.S. Steel cannot sell the company without the support of the USW. So the USW's choice weighs heavily in the decision-making process. U.S. Steel said the USW does not have the right to veto the sale of the company. Other bidders are experiencing challenges with the terms of the USW.

Esmark, ArcelorMittal ( MT ), and Stelco ( STLC:CA ) withdrew their bids because of the USW's stringent requirements.

September 22, 2023

On Sept. 22, Canada's Stelco announced its interest in a full acquisition. Stelco's announcement of the bid, however, is unusual. Stelco was acquired by U.S. Steel in 2007 and became the Canadian arm of the company. In 2014, the company ran into trouble again after which U.S. Steel sold the group. Stelco's bid is furthermore not realistic because its market capitalization is only C$2 billion.

Of all the bidders, I see Esmark as one of the financially strongest. U.S. Steel's market capitalization is currently $7.2 billion. Only Esmark has enough cash on its balance sheet to take over the company without taking on debt.

| Company |

| Net Income (2022) |

| Cash, Equivalents, etc. |

| Total debt |

| U.S. Steel |

| $2.5B |

| $3.1B |

| $4.3B |

| Arcelor Mittal |

| $9.3B |

| $5.8B |

| $9.3B |

| Cleveland-Cliffs |

| $1.3B |

| $0B |

| $4.0B |

| Esmark |

| Not listed |

| $0B |

| Stelco |

| C$1B |

| C$0.8B |

| C$0.06B |

However, the big picture makes it clear that the USW is pulling the strings; USW favors Cleveland-Cliffs. Other parties are certainly interested but they expect difficult cooperation with the USW. Therefore, I see Cleveland-Cliffs as the only candidate to take over U.S. Steel.

Scenario 1: An Increase In The Bid Price

With Cleveland-Cliffs as a suitable candidate, the question arises about what the acquisition price will be. U.S. Steel has expressed its disagreement with the current terms. But because Cleveland-Cliffs has zero cash on its balance sheet, its options are limited.

The current terms of the proposal are as follows:

- Cleveland-Cliffs pays $17.50 in cash + 1.023 in stock to shareholders of U.S. Steel.

Assuming Cleveland-Cliffs' share price remains $15.60, the acquisition price is $33.46 per share ($7.5 billion total). The cash component amounts to $3.9B, and this will be financed entirely with debt.

Assume the financing is at an interest rate of ±8% (interest rate of senior debt). Interest expense will then increase by $312M. Excluding goodwill and synergy benefits for convenience, the consolidated picture looks like this:

| Company |

| Net Income (2022) |

| Cash, Equivalents, etc. |

| Total debt |

| Interest Expense TTM |

| Interest Coverage |

| U.S. Steel |

| $2.5B |

| $3.1B |

| $4.3B |

| $117M |

| 21 |

| Cleveland-Cliffs |

| $1.3B |

| $0B |

| $4.0B |

| $291M |

| 4.5 |

| Consolidated company |

| $3.8B |

| $3.1B |

| $8.3B + $3.9B = $12.2B |

| $408M + $312M = $720M |

| 5.3 |

The interest coverage ratio of the consolidated company is 5.3, which is acceptable. Benjamin Graham recommends an interest coverage ratio of at least 5, especially because of the strong earnings volatility of a steel manufacturer.

Let's see how much the acquisition price can be increased so that the interest coverage is 5. If the interest coverage is 5, the cash component is $4.4B ($19.75 per share). Here we assume that the equity component remains the same to preserve the size of the dilution effect. The total acquisition price then becomes $35.70. This is a small increase of about 10% over the current share price.

This price increase seems realistic to me. The leverage of the consolidated company is within acceptable standards.

The cash on the balance sheet could be used to pay off current debt. So they can save on their interest expenses, which increases their interest coverage. This allows them to raise the bid price further. In the next section, I calculate the absolute maximum.

Scenario 2: Maximum Bid Price (After ABL Facility Is Paid Off)

The large amount of cash on the balance sheet can also be used to reduce debt. However, U.S. Steel's debt maturities are not favorable to take advantage of this.

Debt Maturities (U.S. Steel 2022 annual report)

{kind=link}

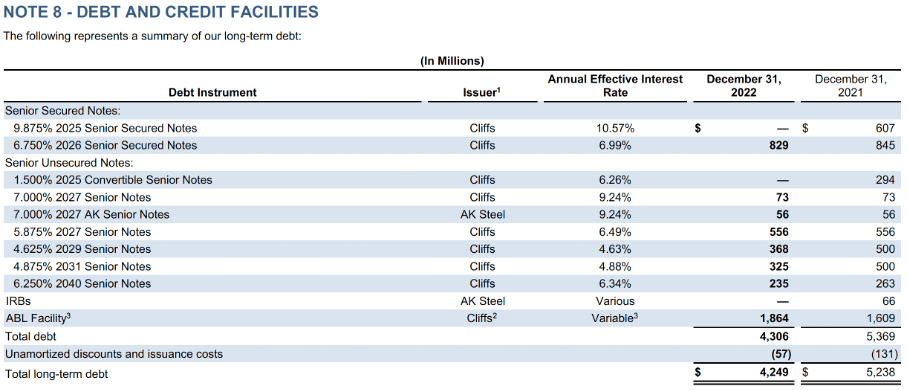

On the other hand, the debt maturities for Cleveland-Cliffs look much more favorable. There is $1.9 billion reserved for 2025 through the ABL facility (variable rate). It is beneficial to pay it off because of the variable interest rates. The annual effective interest rate of the ABL facility was 5.60% as of December 2022. The ABL facility offers up to $4.5 billion in loans and expires at the earliest on March 13, 2025.

Cleveland-Cliffs' Debt and Credit Facilities (CLF 2022 annual report) Cleveland-Cliffs' Debt Maturities (CLF 2022 annual report)

{kind=link}

{kind=link}

With $3.1 billion in cash, the ABL facility can be paid off, reducing interest expenses by $104 million. An additional benefit is that it reduces earnings volatility. Some financial highlights of the consolidated company:

| Company |

| Net Income (2022) |

| Cash, Equivalents, etc. |

| Total debt |

| Interest Expense TTM |

| Interest Coverage |

| Consolidated |

| $3.8B |

| $1.2B |

| $10.3B |

| $720M - $104M = $616M |

| 6.2 |

The interest coverage of 6.2 shows that there is room to increase the bid price.

Again, assume as a guideline that an interest coverage of 5 is acceptable. Also assume that the equity component (1,023 Cleveland-Cliffs shares) remains the same. It appears that the cash component could be $5.7B to arrive at the price limit (at an interest coverage of 5). At Cleveland-Cliffs' current share price, we arrive at an acquisition price of $41.20, which represents a 27% premium.

Discussion About The Bidding Price

In both scenarios, it is possible to raise the bid price. In the first scenario, we discussed the maximum bid price when the ABL facility isn't paid off. In the second scenario, we see that the bid price can be increased significantly. However, the leverage is then fairly high.

Of course, in the first scenario, the company can also pay off its ABL facility. This is beneficial because interest rates have risen sharply this year. This is favorable for both shareholders and the leverage ratios of the consolidated company.

The calculation shows that the bid limit is $41.20 per share of U.S. Steel. This is a 27% premium to the current share price. However, I think the leverage then is very high. The interest coverage may be acceptable, but the company will struggle if demand for its steel products declines. Therefore, I don't think Cleveland-Cliffs will offer a 27% premium. But I do see an offer that is about 10% higher (scenario 1) happening.

Cleveland-Cliffs is in a position that almost forces it to merge with U.S. Steel. The company barely has any cash on its balance sheet, and rising interest rates aren't helping its bottom line either. Right now, I label Cleveland-Cliffs as a high-risk stock because of its heavy debt load.

I expect U.S. Steel to agree to a merger with Cleveland-Cliffs. The scenario 1 bid stands at $35.70, up 59% from before the acquisition announcement. And for scenario 2, it represents an 83% increase. Both are big premiums.

The activities of both companies complement each other well due to the great diversity of steel production processes. For Cleveland-Cliffs, this means supplementing their manufacturing processes with exposure to mini-mills and electric arc furnaces. This allows it to process scrap into valuable steel products. This is necessary for an energy-efficient future. The acquisition is therefore of great importance for Cleveland-Cliffs.

Valuation Is Cheap Compared To Competitors

After examining the maximum bid price, it is interesting to examine how U.S. Steel is priced in the market. U.S. Steel's market value adjusted for net debt is equal to 5.3 times forward EBITDA. For Cleveland-Cliffs, this ratio is 5, and for two competitors Nucor and Steel Dynamics it is 6.9 and 5.8 times. We therefore see that the shares remain attractively valued even after the price rally. The merger provides synergy benefits. And the consolidated company will also be attractively valued on the market.

Takeaway

U.S. Steel could be acquired because of the synergy benefits, the diversification of the production process and to better position itself in the market. Several global steel producers have expressed interest, but the USW seems in control. Candidates have indicated that good cooperation with the USW proves to be a challenge. The USW has already announced that Cleveland-Cliffs is the only candidate with the exclusive right to bid for U.S. Steel. U.S. Steel disagrees with the current terms of Cleveland-Cliffs' offer. Cleveland-Cliffs has limited financial resources. Looking strategically at what is possible, I expect that U.S. Steel's offer price could be increased by a minimum of 10% and a maximum of 27%. A higher bid will result in a consolidated company that may struggle to meet its debt obligations. The stock valuation also looks favorable at the current share price. Because of the favorable valuation and possibility to increase the bid price, I think there is room for a better offer. However, the calculation assumes Cleveland-Cliffs will be the candidate. This could be another company, but I think the chances are small. In all cases, the risk/reward is favorable to U.S. Steel shareholders. Therefore, in my opinion, U.S. Steel is worth buying. When the acquisition price is reached, I will sell my position. The share price of Kraft Heinz, which was also highly leveraged, tanked after its merger. But for now, U.S. Steel is worth buying at the moment.

For further details see:

U.S. Steel: How High Can You Go?