UBER - Uber: 3 Roaring Growth Engines And Undervalued

Summary

- Uber is the dominant market leader in ridesharing and has accelerated two further "growth engines", its Delivery and Freight businesses.

- The company reported strong financial results for the fourth quarter of 2022 as it beat both revenue and earnings growth estimates.

- Uber is forecast to reach GAAP profitability in 2023 and my intrinsic valuation model indicates the stock is undervalued.

- Uber has launched a Carshare platform in Australia which is poised to disrupt the $100 billion car rental market.

Uber (UBER) has grown to develop a strong market share of ~72% in the ridesharing market in the U.S and, also has sizable market share in many parts of the world. Furthermore, in a market like China, where Uber doesn't have any direct presence, the company owns ~11% stake of the ridesharing leader DiDi (DIDIY). In addition, the company has continued to expand two other major growth engines, its delivery business (Uber Eats), which is estimated to be second by market share in the U.S and its emerging Freight business. I believe these three growth engines offer an amazing opportunity for the company. In this post, I'm going to breakdown Uber's Q4 earnings report, breakdown its competitive advantages, before revealing my valuation model for the company's stock; let's dive in.

Growing Financials

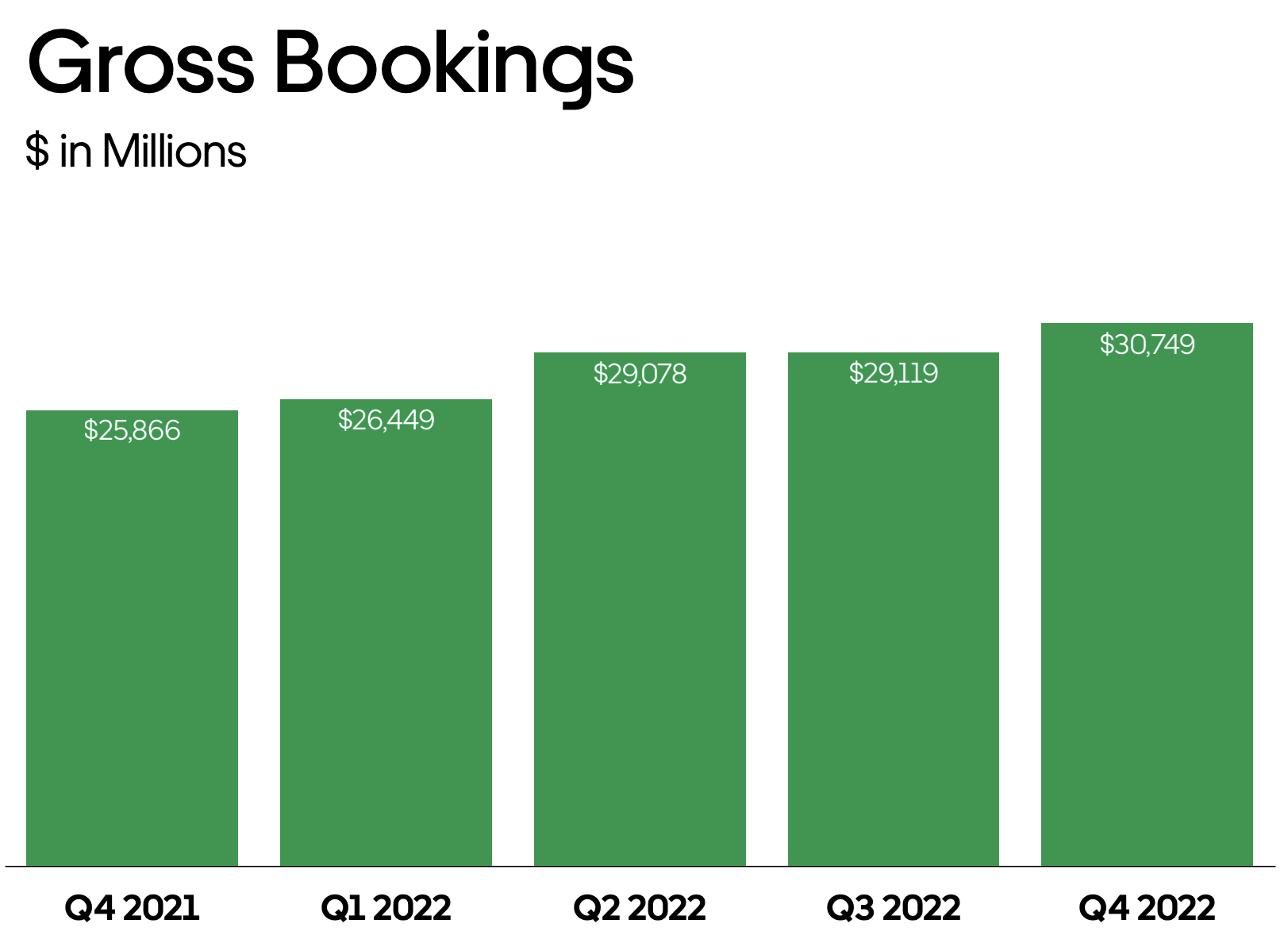

Uber generated strong financial results for the fourth quarter of fiscal year 2022. Its Gross Bookings were $30.7 billion, which increased by 19% year over year or a rapid 26% on an FX neutral basis. Revenue grew at an even faster rate with 49% year over year growth reported to $8.6 billion, this was partially driven by a UK mobility business model restructure and its acquisition of Transplace by Uber Freight. Overall Uber has grown to develop three major growth engines, its Mobility, Delivery and Freight businesses, all which performed well during the fourth quarter.

{kind=link}

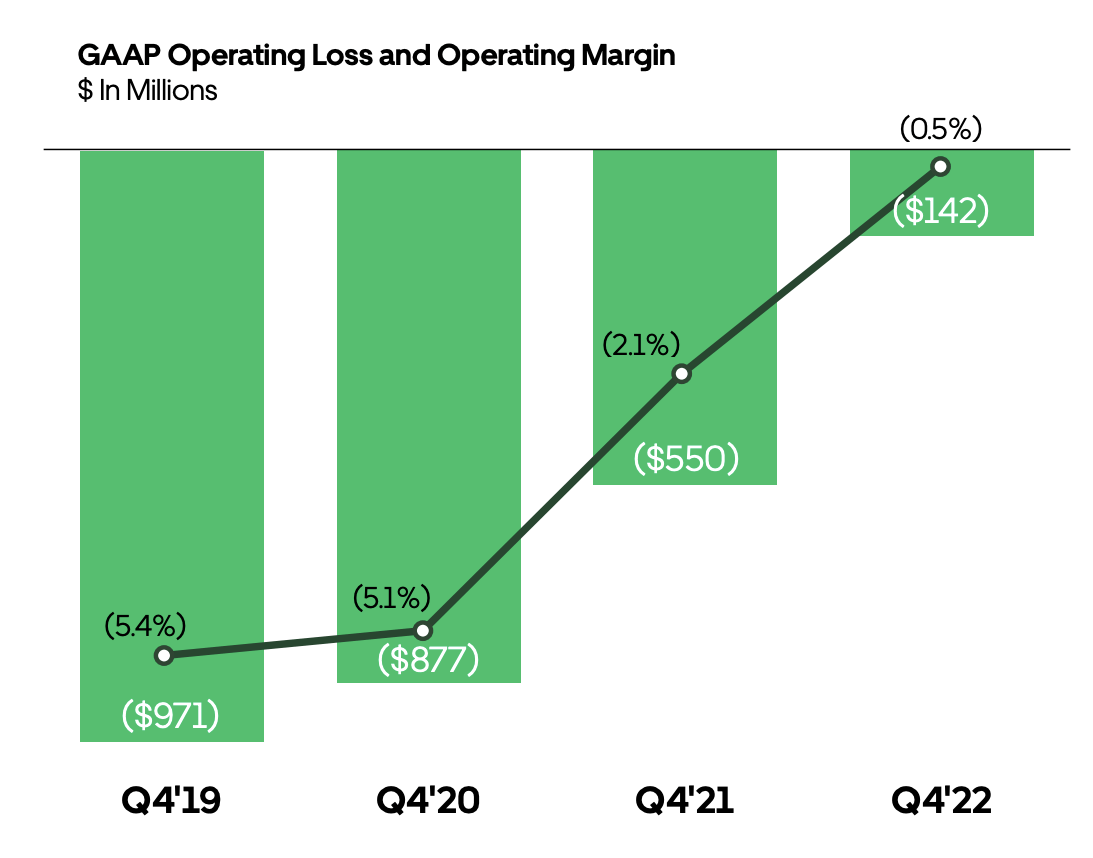

Uber is fast approaching GAAP profitability, as its losses have reduced to negative 0.5% or negative $142 million, an improvement from negative $550 million in Q4,21. Uber's CEO and myself as an analyst both forecast GAAP profitability in 2023.

Operating losses (Q4,22 report)

{kind=link}

Ubers operating expenses as a portion of gross bookings declined from 16.6% in Q4,19 to 11.5% in Q4,21 and 10.5% in Q4,22, which are all signs of operating leverage improvements. I will discuss more about individual segment performance and profitability improvements in the following sections.

Mobility | Growth Engine 1

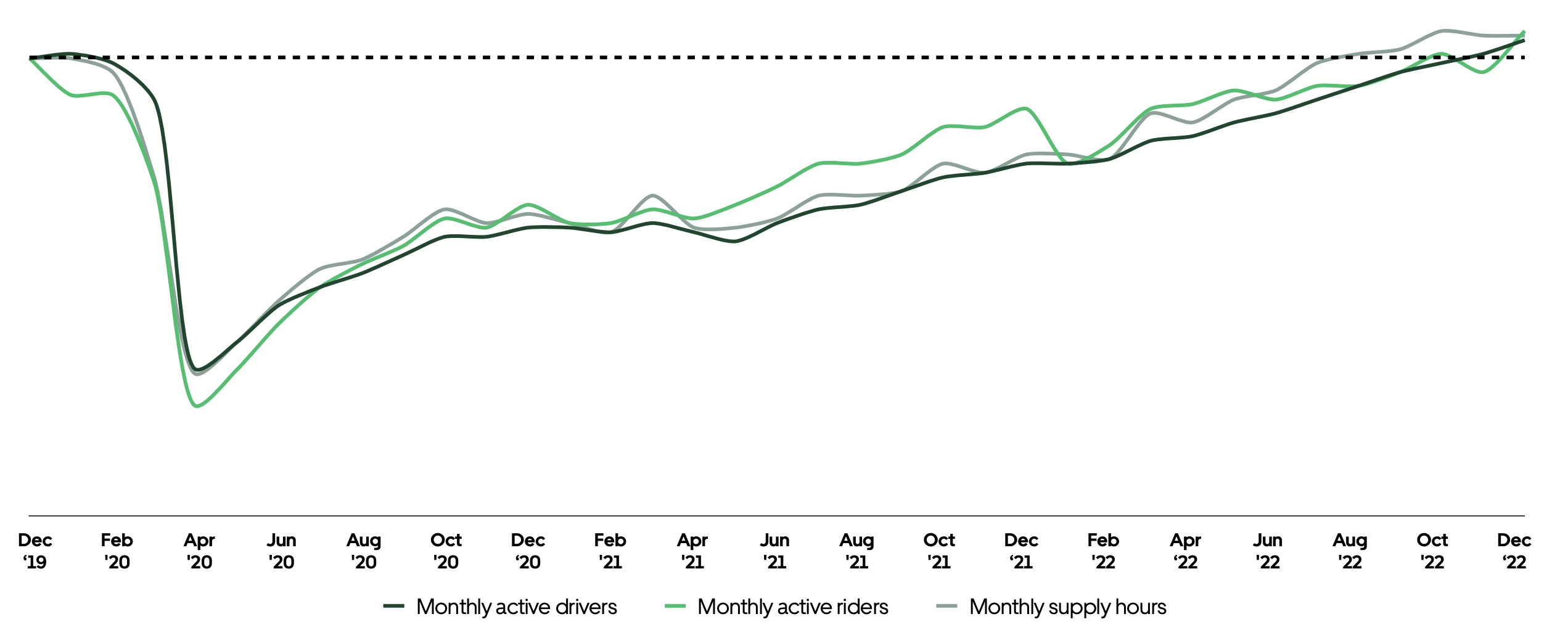

If you recall Uber's mobility segment was decimated during 2020, as consumers were "locked down" in their homes and not traveling as a result. However, as the economy has now "reopened" and consumers are beginning to travel again, Uber grown its rides business to record levels. In the fourth quarter of 2022, Uber posted its highest ever number of monthly active customers and drivers, the chart below shows this story.

{kind=link}

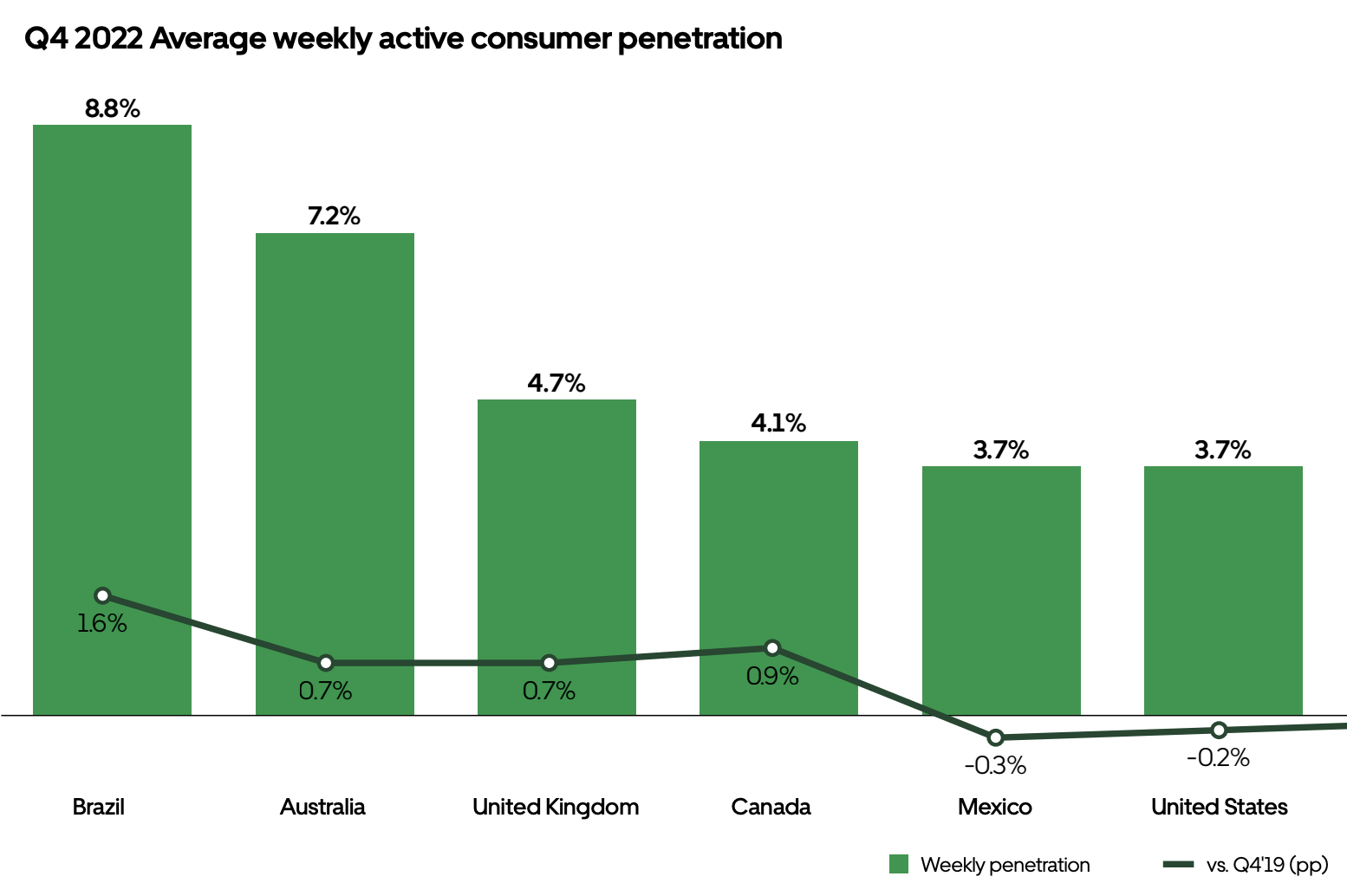

The greater number of rides increased Gross Bookings by a solid 37% year over year (FX neutral basis) to $14.9 billion. Mobility Revenue also increased by a rapid 82% year over year to $4.1 billion, however a $1.2 billion restructuring benefit in the U.K gave this a boost as this converted driver payments and incentives to a "cost of revenue". Its Mobility Take rate also increased by 770bps year over year to 27.8%, which is testament to the company's strong brand and position. A negative of Uber's scale and recovery is you may believe the company is running out of runway to grow, but in fact it looks to be the opposite. A large portion of Uber's growth has come from emerging markets such as Brazil which reported a 16% increase in weekly penetration since 2019. Whereas the United States and Mexico are still recovering with -0.3% and -0.2% versus 2019 reported.

Ridesharing Penetration (Q4,22 report)

{kind=link}

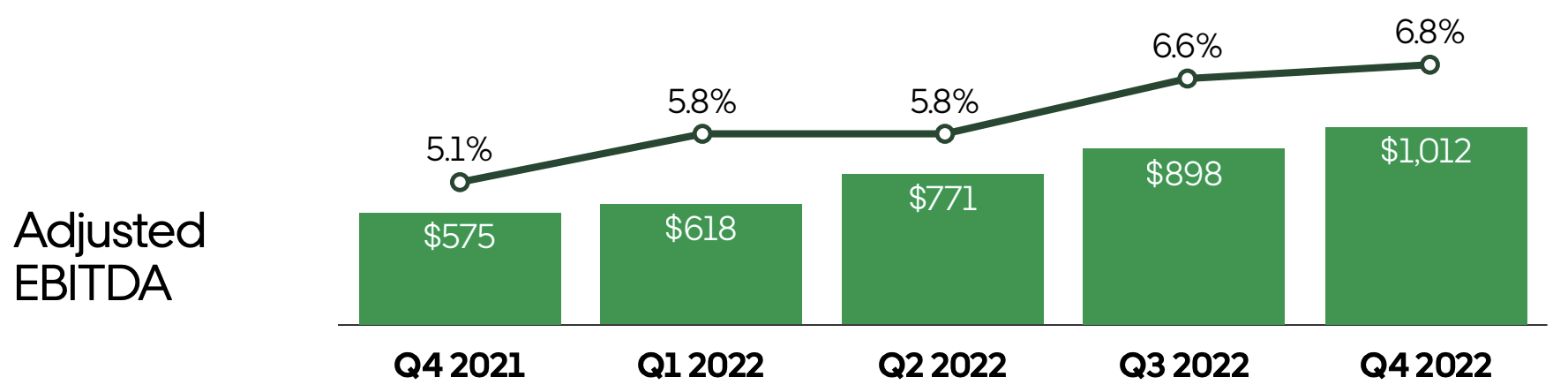

Its rides adjusted EBITDA increased by a rapid $437 million year over year as it adjusted EBITDA Margin expanded to 6.8%, which is a positive sign as profitability has always been a major issue for Uber, as the company voraciously had to sacrifice margins to offer "loyalty discounts" to drivers. However, as the company has scaled, its cost structure has started to make a lot more sense. In addition, the 2020 demand plummet in rides was actually a blessing in disguise as the company reduced its headcount by over 20% and slashed its infrastructure costs by over $1 billion. Since that point, Uber has focused on driving efficiency and credit to Uber CEO Dara Khosrowshahi, the company achieved its targets of EBITDA profitability in 2021.

{kind=link}

User Experience/Scale Advantage

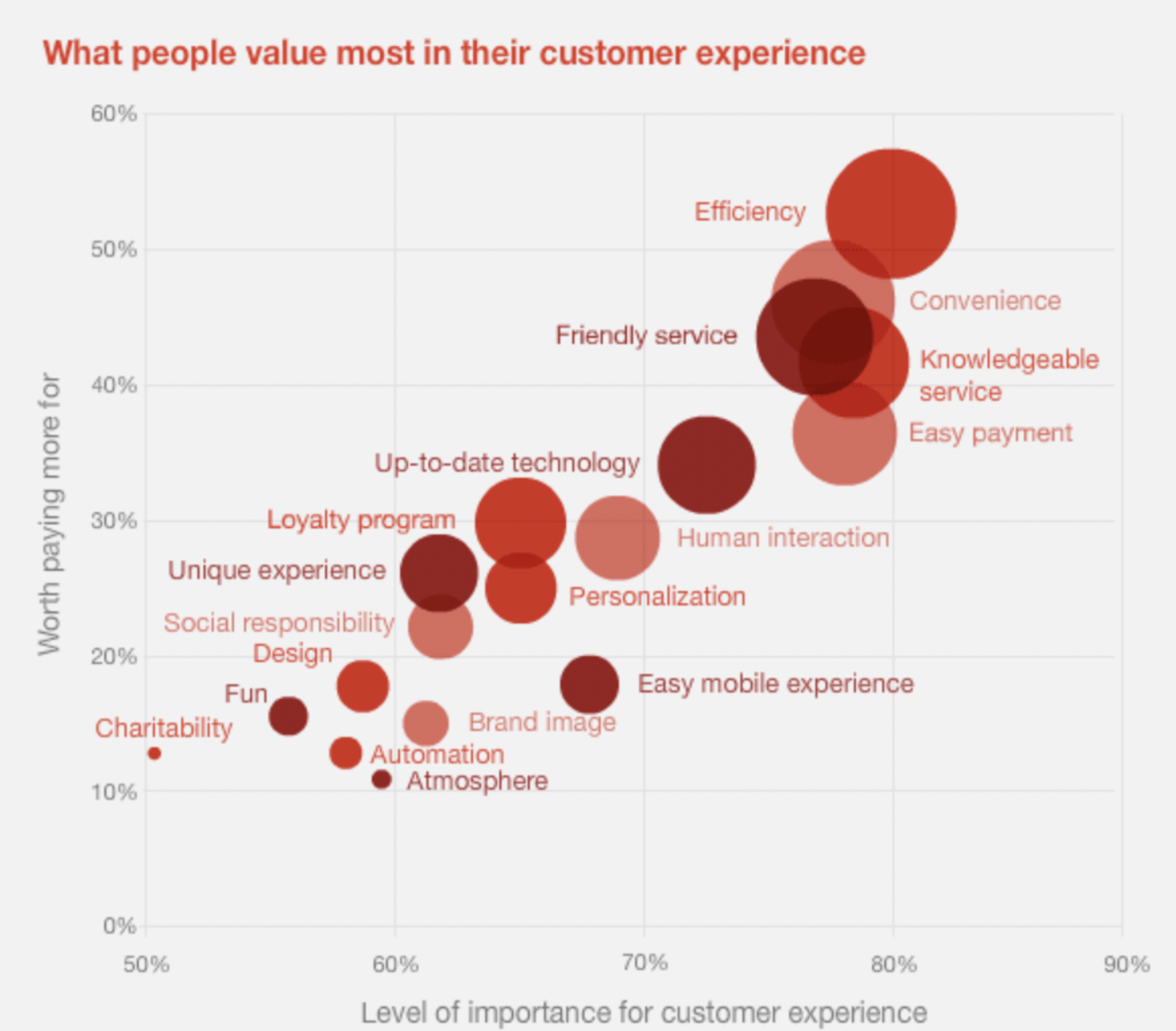

There has been a lot of talk about "competition" for Uber from its legacy rival such as Lyft, to companies such as Bolt and Via which are growing fast in Europe and the U.S respectively. However, Uber has a few competitive advantages; its scale, its brand, its expertise in the sector and its app usability/rapid innovation. According to a study cited by InVerita, 8 out of 10 customers are willing to pay more for a better customer experience. In addition, a PwC study indicates that efficiency, convenience, easy payment, friendly service, personalisation and human interaction are all rated highly by customers in terms of what they would pay more for.

{kind=link}

I believe Uber ticks virtually all the aforementioned boxes. Firstly we have its automated payments, which make the entire experience frictionless. In addition, we have the Uber car on the map which reduces the uncertainty and anxiety of waiting for a cab. More recently, I have done a user test/review of the app and noticed extra intuitive features such as the ability to send an automated message to the driver telling them your "on your way", (improving the customer and driver experience). Also recently, I was in a small town which didn't have Uber and had to call up a standard taxi on the phone. The company had setup an automated system which used voice recognition to ask me where I wanted the taxi to and from. However, this was an extremely clunky system and it took me multiple attempts to confirm the correct address (not a great experience). After I got into the taxi I found it to be dirty and it smelled a little funny. Whereas Uber's review system self polices this because if drivers don't clean their cars, likely they will get bad reviews. In the car I wished to pay with Apple pay or credit card, the cab had a system for this but it "wasn't working", as often smaller cab companies are poorly resourced technically. Thus I had to stop at an ATM and pay in cash, all while trying to be on-time for a train and a business meeting. The reason I've told you this story is because, what may feel a "normal" service provided by Uber is actually extraordinary. In fact , our brain gets a "dopamine" hit when things just work and we feel like we are moving forward, studies show this helps improve customer loyalty and retention. When a user has a great experience, they want to come back and are unlikely to switch to a different product just to save a couple of dollars.

Now of course you may say that many of Uber's features can be copied and I agree. However, let's not forget Uber has been a pioneer in this space and thus when one company launches a feature copy, Uber is already onto its next feature or improving its back end efficiency which can't be "copied" as simply. In addition, Uber has the greatest scale and thus you are likely to find solid technology performance and a greater selection of nearby cabs.

Car Share Opportunity and Products

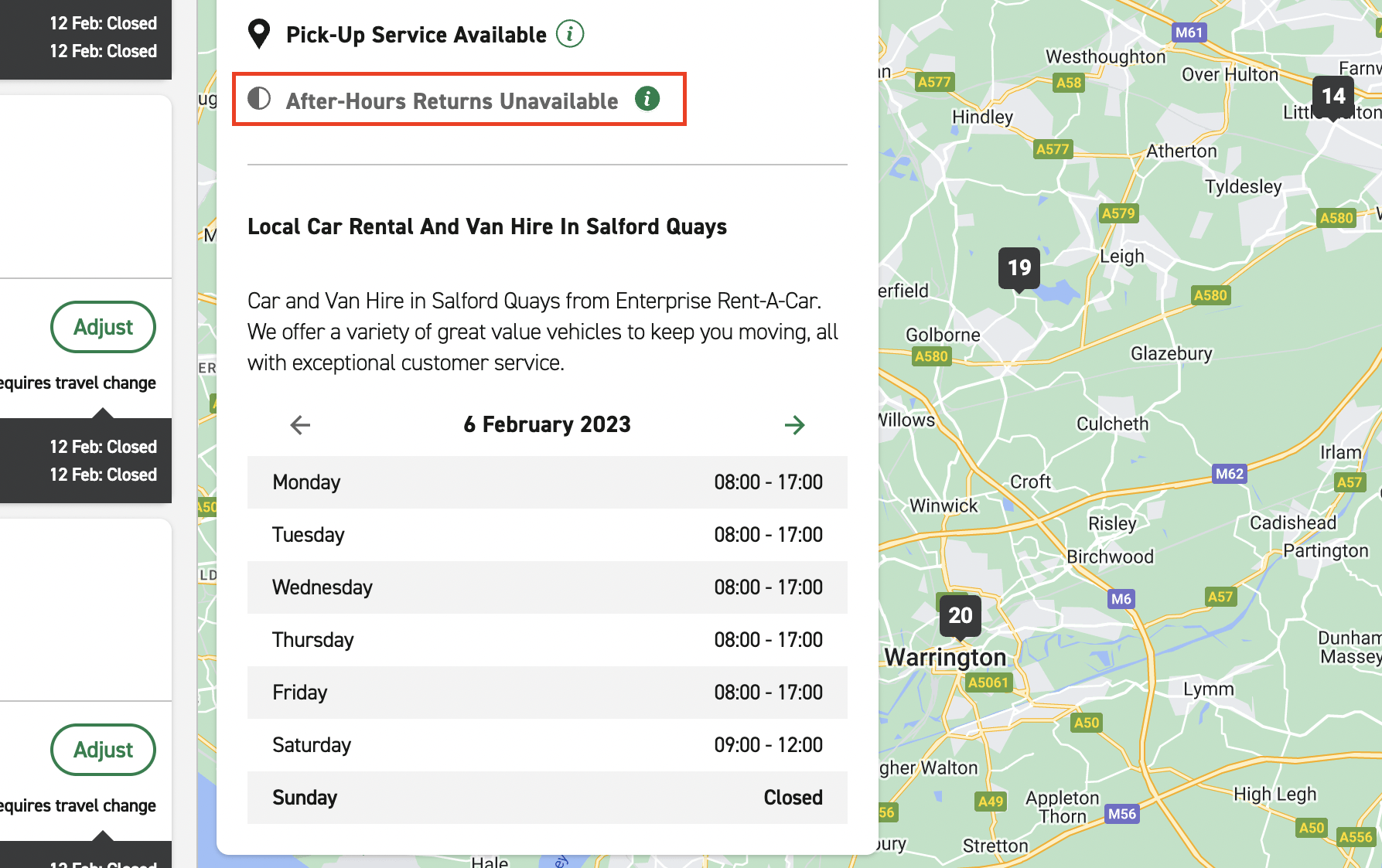

In terms of features/products, Uber has recently launched a Carshare platform in Australia, which was as a result of an acquisition of "Car Next Door". I believe this offers a major market opportunity, which is set to disrupt the $100 billion car rental market. Uber Carshare is basically "Airbnb for cars", this enables an average user to rent out their car to earn extra money, while customers can rent a cost effective car from just a few hours to multiple days. A quick cost comparison online showed me that the lowest cost car rental on Enterprise (a popular rental car company) was £111 or $135 for a day, for an economy 2 door Vauxhall Corsa, which isn't exactly a fancy car. Whereas, on an Uber Car Share equivalent in the U.K (Hiya), I found the price to be £45/day ($55), for a much better vehicle (BMW). Thus the value proposition could be enticing for this business, despite it being in its early stages. I noticed also popular rental car provider (Enterprise) is closed on a Sunday and renters must return the car within working day hours. Whereas, individual citizen renters could be much more flexible which could be an advantage to this business model. I expect more acquisitions by Uber in this industry as the car share model is further built out and the public warms to the idea.

Car Rental Closed Sunday (Author research Enterprise)

{kind=link}

Uber has also expanded its "Charter" business to over 20 major cities which enables the booking of a large van, coach or even a "party bus", directly via the Uber App. Uber Travel has also expanded to over 10,000 cities globally, which enables the seamless booking of hotels, flights and even restaurant reservations from the Uber App etc, through its partnerships with Viator (Travel) and OpenTable (Restaurants).

Uber is continuing to invest into its Electric Vehicle partnerships and in January 2023, the company expanded its Hertz partnership to include over 25,000 EVs for drivers in Europe by 2025.

Delivery | Growth Engine 2

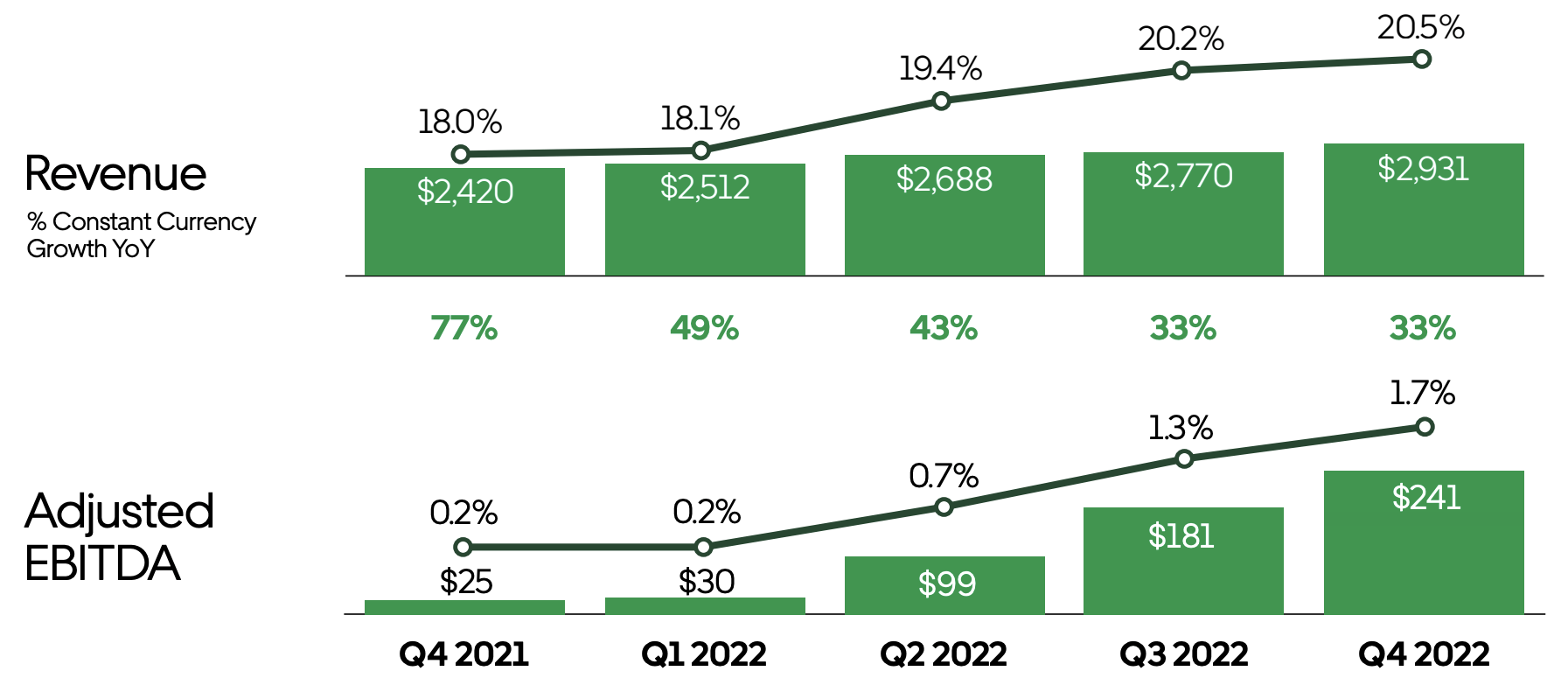

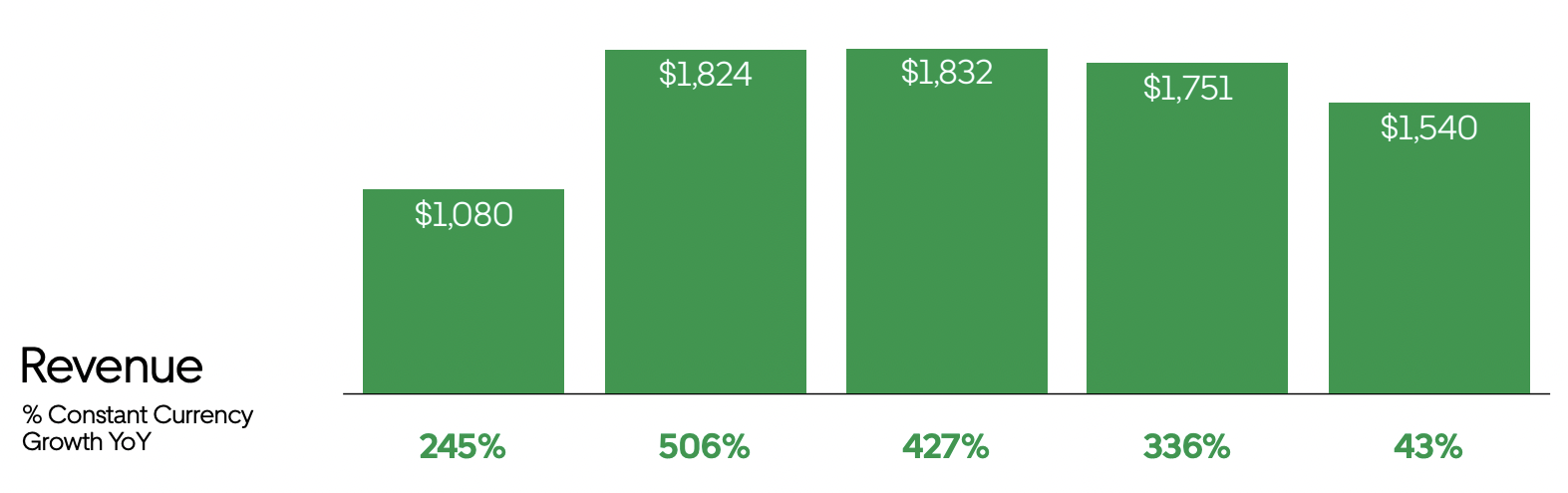

Uber's delivery segment scaled massively during the lockdown of 2020 and has become a major growth engine the company. In Q4,22 its revenue was $2.9 billion, which increased by a solid 21% year over year and contributed to 33.7% of the total. The business model change in certain countries such as the U.K, did increase its Delivery Take Rate by 480 bps in Q4,22.

The company reported positive leading indicator metrics such as basket size and order frequency which increased by 1% YoY and 4% year over year respectively. Both sides of its marketplace continue to grow as active merchants increased by 8% YoY to exceed 890,000 and its active couriers increased by 5% YoY, and 10% YoY in the U.S.A. I believe this is a major positive as Uber operates a two sided marketplace. Therefore, more merchants equals more selection for customers, equals better experience, equals more loyalty etc. This is a virtuous cycle, which continues to grow and strengthen Uber's market position.

Delivery Revenue (Q4,22 report)

{kind=link}

In terms of delivery its Adjusted EBITDA increased by a solid $216 million year over year. This was driven by higher volumes, coupled with improved network efficiencies and increased advertising revenue.

Uber's mission is to become the go to provider for the delivery of everything one needs. The company is fast expanding into alternative categories such as "quick commerce" which involves the delivery of alcohol, snacks and groceries. In the U.K the company partnered with GoPuff, Grocery Outlet across 300 locations in the U.S and even Walgreens. I believe this is a positive strategy as it effectively offers upsells and cross-sells, while also increased the number of times a user is likely to use the Uber Application. For example, let's say a user is using the Uber app to order a cab in the morning, then for lunch in the afternoon and groceries in the evening, a habit is more likely to be formed with that consumer. An interesting area which Uber didn't mention in its earnings call, was the delivery of pharmaceuticals. In 2020, Uber launched a pharmacy delivery, which included the delivery of prescriptions. More recently I have noticed a partnership with U.K pharmaceutical giant Boots. I believe this offers another huge market for Uber Eats to address. A company which specializes in this is Hims & Hers Health ( HIMS ), which went public in 2020 and has a $1.75 billion valuation, after a major pullback.

Freight | Growth Engine 3Uber Freight reported revenue of $1.5 billion, which increased by a rapid 43% year over year. This was partially driven by acquisition of Transplace, which closed in November 12th 2021. Logistics has become a vital industry, which has been driven by the major growth in the ecommerce and delivery industry . It is great to order everything online, but somebody has to delivery all these packages and given many studies indicate a global shortage of truck drivers, I forecast Uber Freight could help plug this gap.

Uber Freight Revenue (Q4,22 report)

{kind=link}

The company reported an Adjusted EBITDA improvement of $17 million year over year, with a margin improvement of 1.8% to -0.5%. This isn't too bad given this segment is still in its early stages of growth.

Uber Freight scored a major partnership with Volvo a leader in trucks for an autonomous driving solution, which would be available on the Uber Freight network in early 2023. This builds upon Uber's partnerships with Google's Waymo, which has been testing autonomous trucks around Texas and Aurora (of which Uber also has an investment). These are all fantastic partnerships and mean Uber is poised to benefit from the 17% growth forecast in the autonomous trucking market.

Valuation and Forecasts

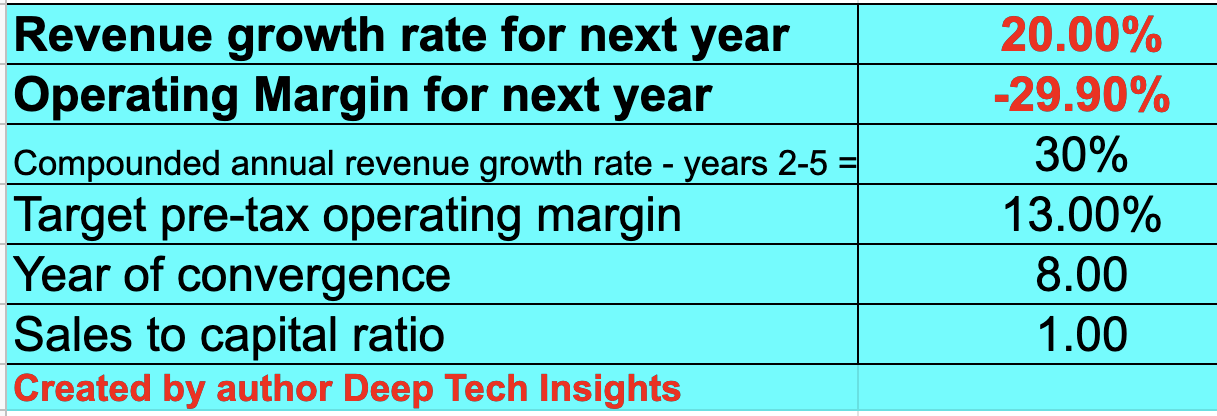

In order to value Uber, I have plugged its latest financial data into my valuation model which uses the discounted cash flow method of valuation. I have forecast 20% revenue for next year. This is based upon an extrapolation of managements guidance for 20% in Gross Bookings, which I have forecast will drop down to a similar growth rate in revenue. This is assuming continued foreign exchange rate headwinds. In years 2 to 5, I have forecast a faster revenue growth rate of 30% per year, as I expect economic conditions to improve, due to the cyclical nature of the economy. In addition, I expect continued growth in Rides, Delivery and of course Freight.

Uber stock valuation 1 (created by author Deep Tech Insights)

{kind=link}

In an attempt to increase the accuracy of my model I have capitalized R&D expenses which has boosted net income slightly. In addition, I have forecast a pre tax operating margin of 13% over the next 8 years. This may seem optimistic but given the improvements in both EBITDA and forecasted GAAP profitability in 2023, this is possible. A core reason for this is lets remember Uber is a software company at heart, and thus doesn't need to buy more (or any) cabs to expand. Therefore as it scales, operating leverage becomes more pronounced which is a positive. I still think the company will have its margins squeezed by competition and incentives in certain markets, thus I have estimated the 8 year operating margin to be substantially lower than the 21%-23% average for the software industry.

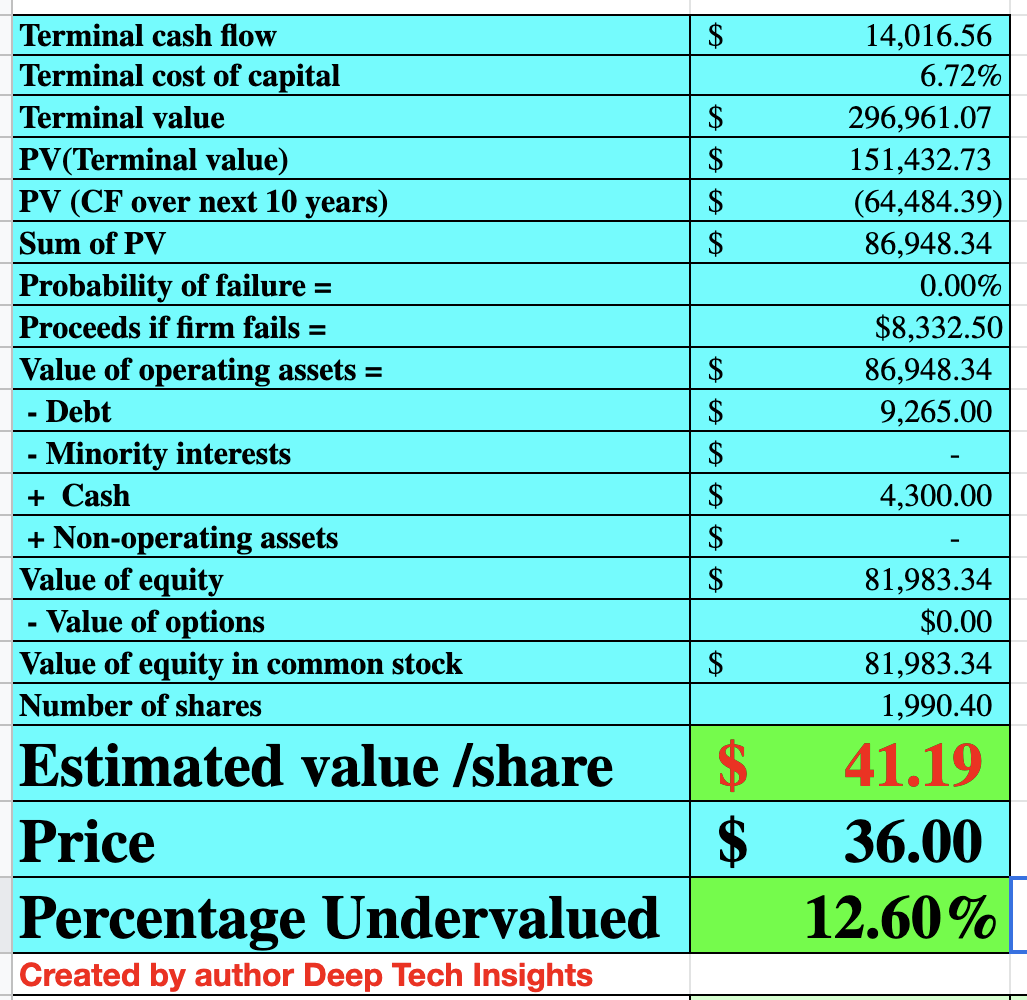

I have also taken into account Uber's solid balance sheet which has $4.3 billion in cash, cash equivalents and marketable securities. In addition, the company has $9.265 billion in long term debt, which is manageable as not due within the next two years.

Uber stock valuation 2 (created by author Deep Tech Insights)

{kind=link}

Given these factors I get a fair intrinsic value of $41.19 per share, the stock is trading ~12.6% undervalued, according to my forecasts and model.

As an extra datapoint, its forward price to sales ratio is ~1.99, which is ~41% cheaper than its 5 year average.

Risks

Recession/Competition

The forecasted "recession" in 2023 is a risk to most businesses as it will likely cause a drop in consumer demand. For example, many consumers will likely switch from expensive food delivery, to cost effective home cooking to save money. In addition, people may also start to go out or travel less, which would impact Uber's rides business. We are not seeing major signs of these trends yet, but it is a possibility. Competition is also still popping up in both the aggressive food delivery market and even rides. This could impact margins due to incentives, although the tough economic environment may actually help squeeze competitors more than Uber, as it has greater scale.

Final Thoughts

Uber has bounced back from the 2020 disaster in tremendous style. The company has developed three major growth engines, with both mobility and delivery running at full throttle. Freight is an emerging business but offers huge opportunity for Uber to continue its growth. My valuation model indicates the stock is undervalued intrinsically and thus it could be a great long term investment.

For further details see:

Uber: 3 Roaring Growth Engines And Undervalued