UBER - Uber: Poised For Continued Growth

Summary

- Uber Technologies, Inc. has been not been a great investment, with the share price down 40% since the IPO in 2019.

- While the share price decreased, Uber has more than doubled revenue over the same period.

- With excellent growth drivers in place, the company looks set for another decade of strong outperformance.

- Uber will most likely continue to face regulatory hurdles as an industry innovator in addition to facing tough competition across most segments.

- Uber looks like a no-brainer for long-term investors and I am buying while the share price is down.

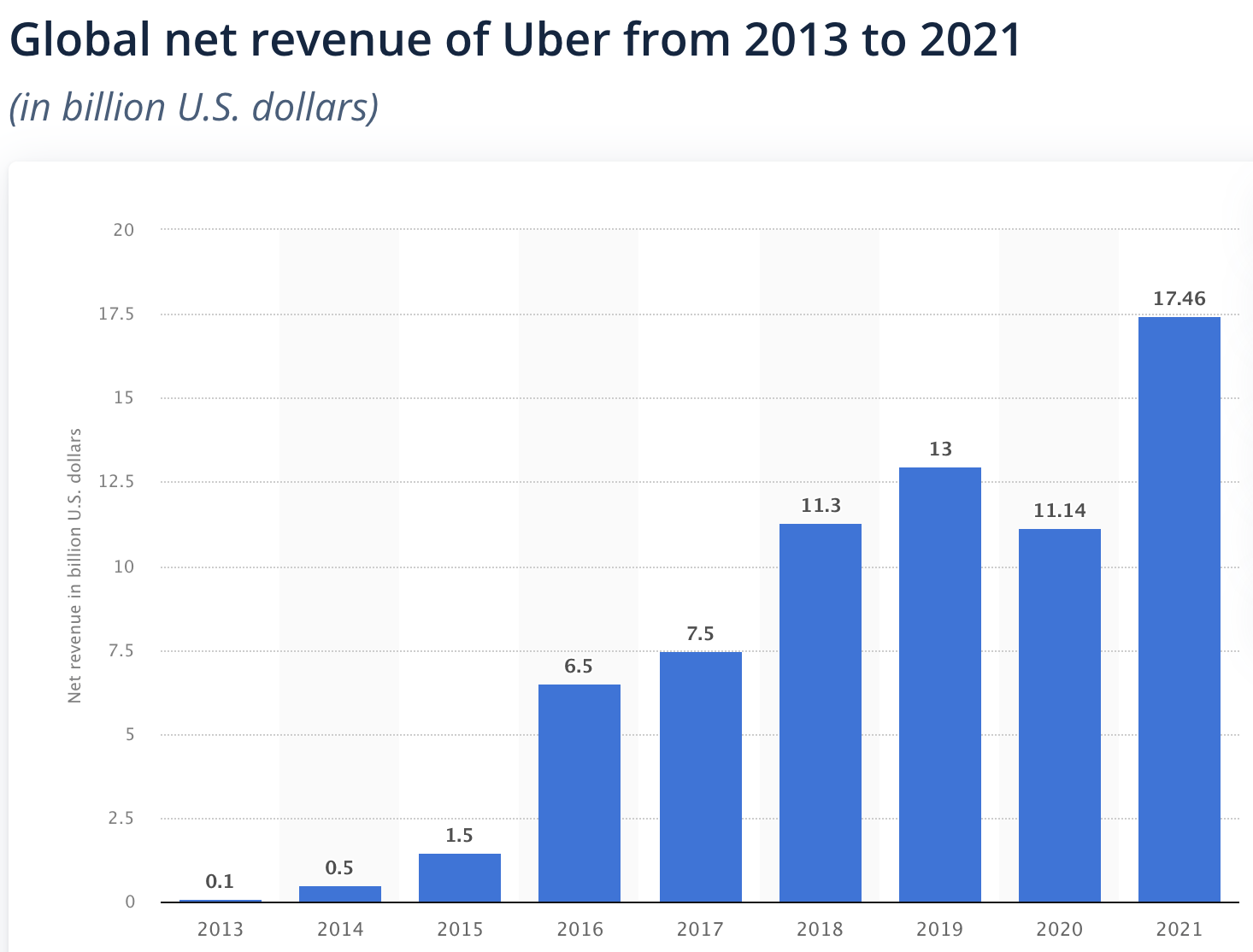

Uber Technologies, Inc. ( UBER ) has not turned out to be a great investment decision at its IPO back in 2019 as the stock price is down by over 40% since then. Does this then mean the company has performed badly? No, not at all. Uber has grown its revenues from $13 billion in 2019 to $17.5 billion in 2021. On top of this, Uber is expected to report a massive increase in revenue for 2022, as it is expected to reach revenue of over $30 billion for the full year, representing an increase of over 80% YoY driven by easing lockdowns and an increase in travel. This means that the Uber share price is down by 40% while revenue more than doubled over the same period. It should be mentioned, though, that Uber is still not profitable and is only expected to report a positive EPS by FY24, according to current analysts’ projections.

{kind=link}

As the decrease in share price indicates, investors in Uber have had a tough period as the company was very much flourishing before the covid-19 pandemic, but was then hit by strict lockdowns worldwide, massively decreasing demand for its services. Yet, Uber did not just sit back and waited, but accelerated their food delivery service and, therefore, still managed to report decent revenue and expanded the business TAM.

Now that the covid-19 pandemic is behind us and people start traveling again, investors in Uber are now facing new issues with rising interest rates, a potential recession, and sky-high inflation resulting in high fuel prices. With margins under pressure and investors less willing to pay for future profits, Uber has seen its share price under serious pressure resulting in a 40% loss in share price over the last year. All of this is despite an 80% increase in revenue, although it should be said that these growth rates are not expected to remain this strong as the company will start lapping tougher comparable YoY quarterly results.

By now, you might very well be asking yourself where I am going with this article. Well, I continue to be very much intrigued by the several business segments of Uber and see great potential for the company over the next decade, as it operates in strong growth sectors while holding a dominant position in all. At the same time, the company has faced significant challenges since it went public in 2019, including intense competition, regulatory issues, and rising costs.

So, is Uber Technologies, Inc. a buy right now? To determine this, let’s start by taking a look at the company in general for those not quite so familiar with Uber.

Uber Technologies

Uber is an American technology company providing mobility as a service, ride-hailing/ride-sharing, food delivery, package delivery, and freight transportation solutions. The company is headquartered in San Francisco, California.

Uber's business model is based on providing a platform that connects riders with drivers who are hired by Uber. When a user requests a ride through the Uber app, the company uses GPS to locate the nearest available driver. Uber charges a fee for this service, which is calculated based on the distance and duration of the trip, as well as various other factors such as demand for rides and the type of vehicle being used.

Uber takes a percentage of each fare as its cut. The remainder of the fare is paid to the driver, who is considered an independent contractor rather than an employee of the company. This business model has allowed Uber to scale rapidly and expand into new markets, but it has also led to legal challenges and controversies over workers' rights and benefits across many countries. The company has been accused of flouting local transportation laws and underpaying drivers.

In addition to the ride-hailing service, Uber also offers food delivery and freight solutions to complement the three different company segments. Uber nowadays supplies over 21 million trips a day, has 124 million active paying customers, is active in over 70 countries and 10,500 cities, and has so far paid over $185 billion to its drivers.

Uber was founded in 2009 and has since become a household name in many countries around the world. Uber has a strong moat and continues to be the number one service for food delivery and ride-hailing while expanding its business into new directions thanks to its easy scalability and large user base.

Thanks to this, Uber has been able to grow the business at a rapid pace over the last couple of years, as shown by its most recent quarterly results and outlook.

Financial results

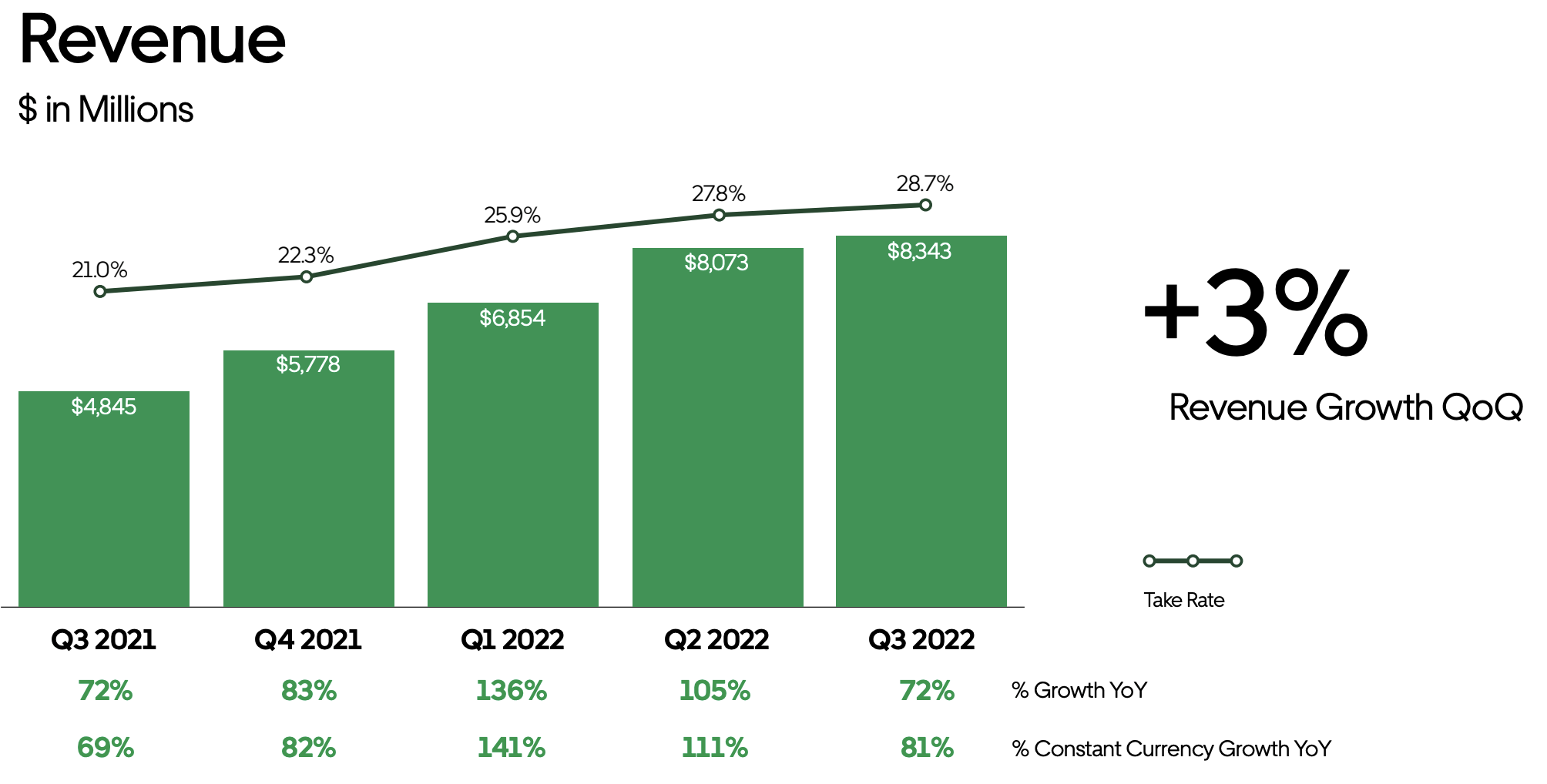

Uber delivered decent results back in November 2022 when it reported its third-quarter results . Gross bookings increased by 26% YoY to $29.1 billion. The mobility (ride-sharing) segment delivered the strongest growth driven by the ongoing recovery from covid-19 impacts and lockdowns. The segment saw gross bookings increase by 38% YoY to $13.7 billion. Whereas delivery was expected to start reporting negative growth with covid-19 lockdowns all pretty much gone, the segment continued to grow by 7% to $13.7 billion. The freight segment saw gross bookings of $1.75 billion.

As a result of this strong growth in gross bookings, Uber managed to increase its revenue at an even faster clip as revenue increased by 72% YoY to $8.3 billion. Growth was 81% on a currency-neutral basis but was impacted by a stronger dollar. This outperformance compared to gross bookings growth was due to the acquisition of Transplace by Uber freight and a new business model in the UK.

{kind=link}

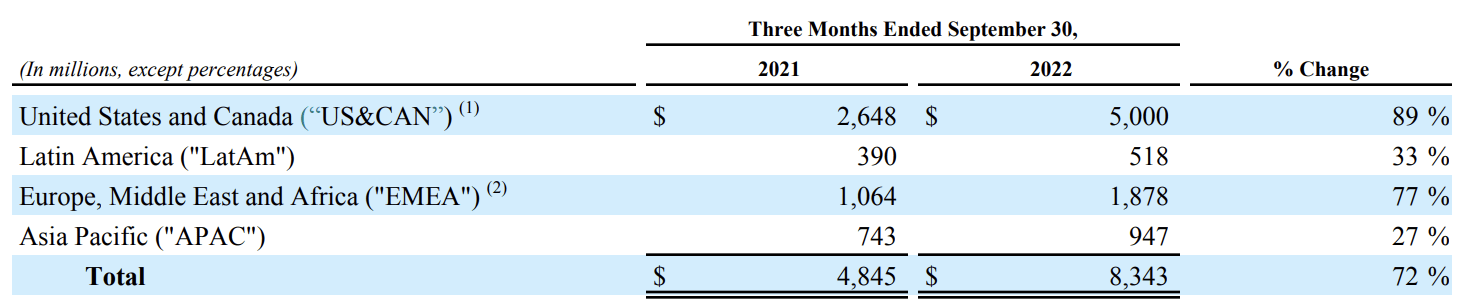

If we look at revenue by region for the first 9 months of the year, we can see that the U.S. and Canada still represent the majority of revenue for Uber while also being the fastest-growing region. The EMEA region also continued to see strong growth as illustrated below.

Revenue split by region (Uber)

{kind=link}

EBITDA grew from zero last year to $516 million this quarter thanks to a slight increase in margins. EBITDA margin for the quarter was still just 1.8%. Free cash flow for the period was $358 million. Uber also saw its take rates increase YoY, as illustrated below, mainly due to changes in the business model across several regions.

{kind=link}

This all looks extremely strong, but it was not all positive. Uber continues to report a net loss of $1.2 billion, although it should be mentioned that $512 million of this was due to equity investment losses. In addition to this, the net loss includes $482 million of stock-based compensation. Still, it is remarkable for a company expected to report over $30 billion in FY22 revenue to not be profitable on the bottom line. The reason seems to be mainly attributable to continued investments in growth, expansion, and marketing in order to attract new riders. Analysts are projecting Uber to start reporting a positive FY EPS by FY24.

Uber guided for 4Q22 to see gross bookings increase by 23% - 27% on a constant currency basis showing a slight decline in growth. EBITDA is expected to be around $615 million at the midpoint. This puts FY22 revenue between $30 and $31 billion. Analysts currently project revenue to come in at close to $32 billion which seems like quite lofty expectations. It could turn out to be a hard task for Uber to outperform these expectations, but with oil prices trending lower and the dollar weakening, Uber looks poised to outperform its own projections. Still, the main question for investors seems to be how long Uber can continue to grow at a strong clip now that all covid-19 impacts have faded.

Growth drivers

So, how can we expect Uber to grow going forward? I am not particularly worried about growth for Uber as the company has a strong position in all three of its segments and looks to have plenty of opportunities to grow over the next several years. Let’s go through some of these opportunities.

Segment expansion

Uber has been able to scale the business at a rapid pace over the last decade with Uber only operating in just 8 cities 10 years ago (now over 10,500). Uber continues to be easily scalable, and I believe it will continue to do so over the next years.

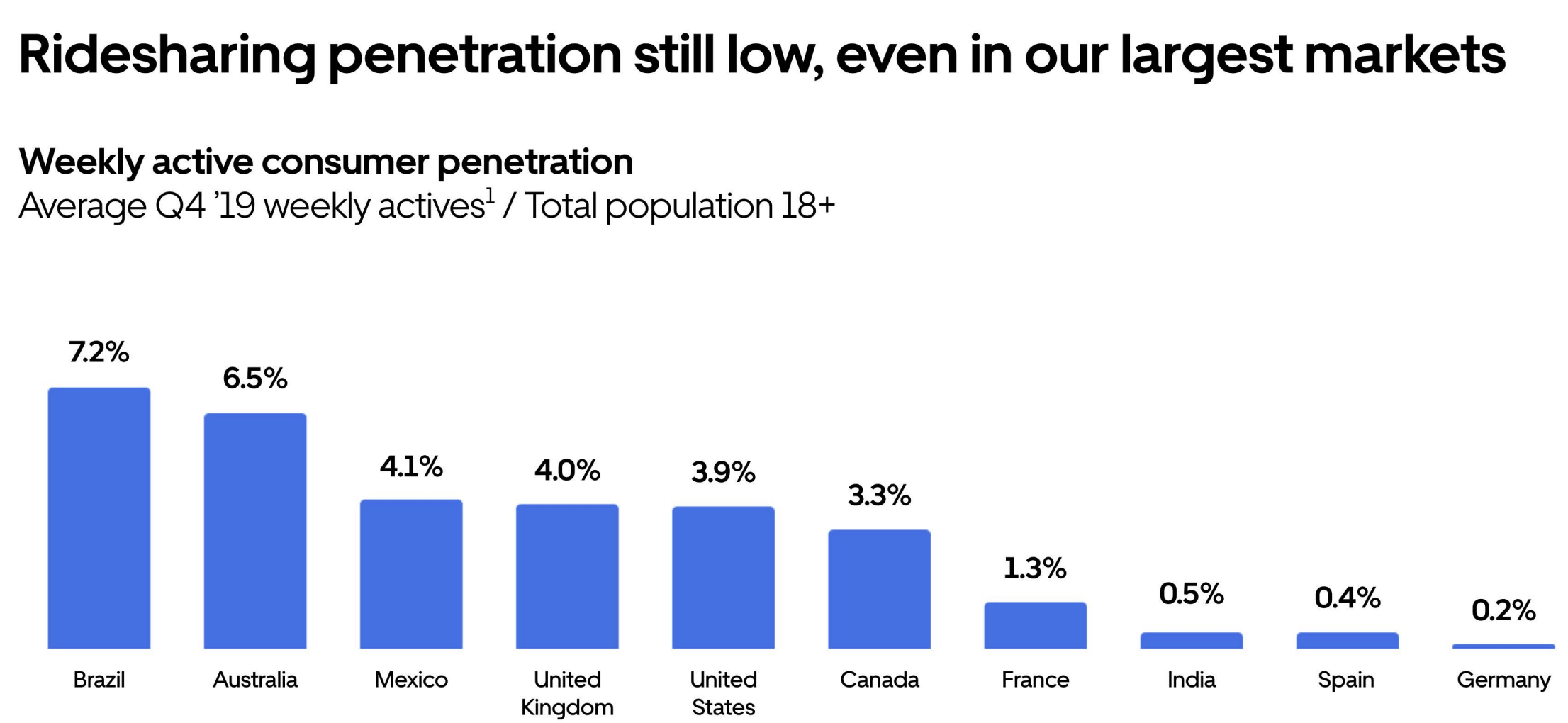

The most obvious expansion for the company will come from the general increase in ride-sharing. With ride-sharing becoming increasingly more accessible, Fortune Business Insights projects the ride-sharing market to grow at a 16.3% CAGR until 2028 with Uber on the pole position. Even in the largest markets for Uber, the adoption of ride-sharing is very low, as shown below, and therefore has plenty of growth potential with it being a cheaper alternative than owning a car (although not for everyone).

{kind=link}

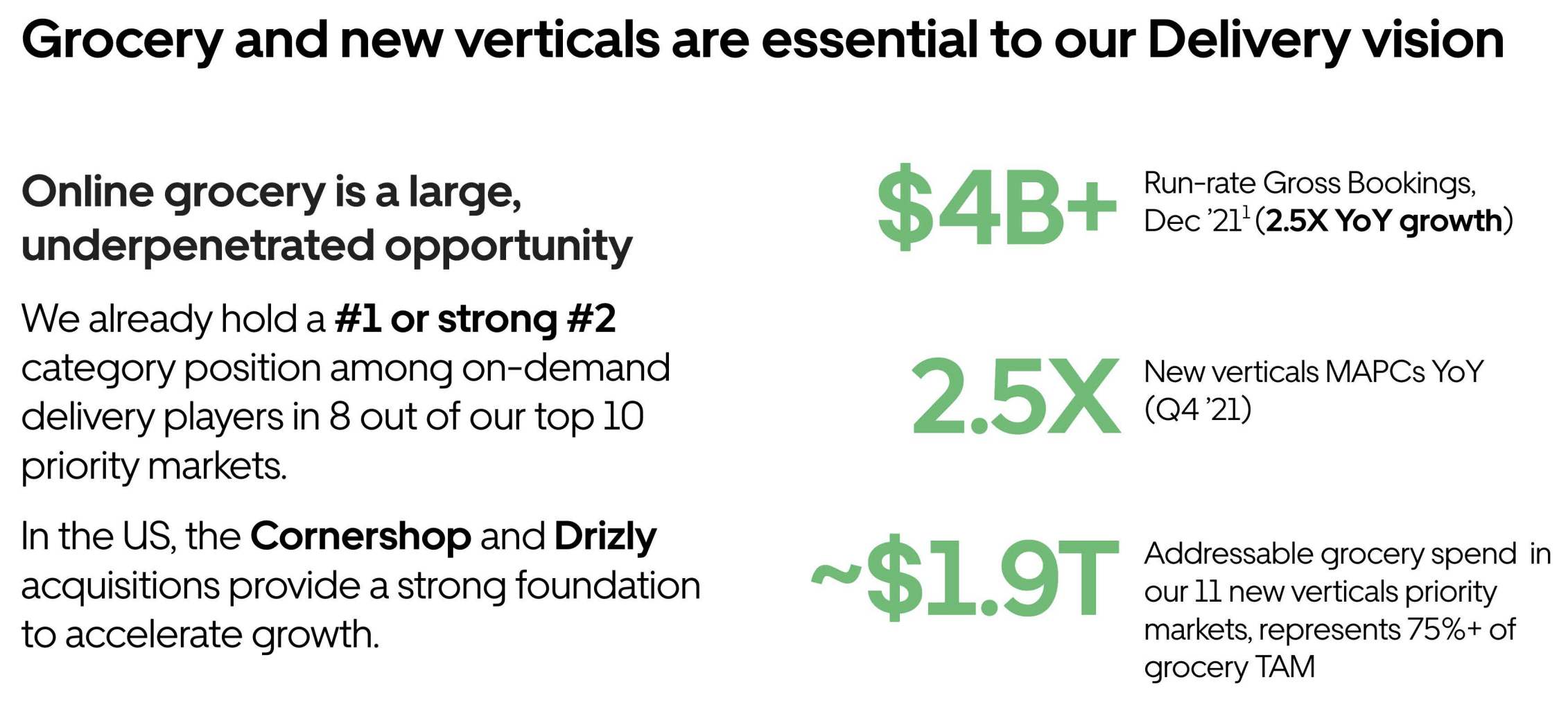

Another business expansion opportunity lies in the delivery segment, UberEATS. The company has already made significant inroads in this market, and it could continue to expand its presence in the food delivery industry in the future. Uber held a 26% market share in the food delivery industry in the US as of the end of 2021. The US food delivery market is expected to grow at a 13.56% CAGR until 2027 with the grocery delivery part of the industry growing at a faster 24% CAGR . The industry is expected to be valued at $384 billion by 2027. I honestly expect Uber to expand its market share, but let’s be conservative and assume the market share to decrease to 20% by 2027 as competition intensifies. This would give Uber’s delivery segment a gross booking value of $76.8 billion, which is more than double that of 2022 while only including the US. Uber acknowledges the grocery delivery opportunity as shown by the slide below from their 2022 investor day presentation. Expansion of its delivery segment offers a strong growth opportunity for Uber. Yet, the food delivery industry is also a very competitive one, so Uber will need to execute to perfection to keep a leading market position.

{kind=link}

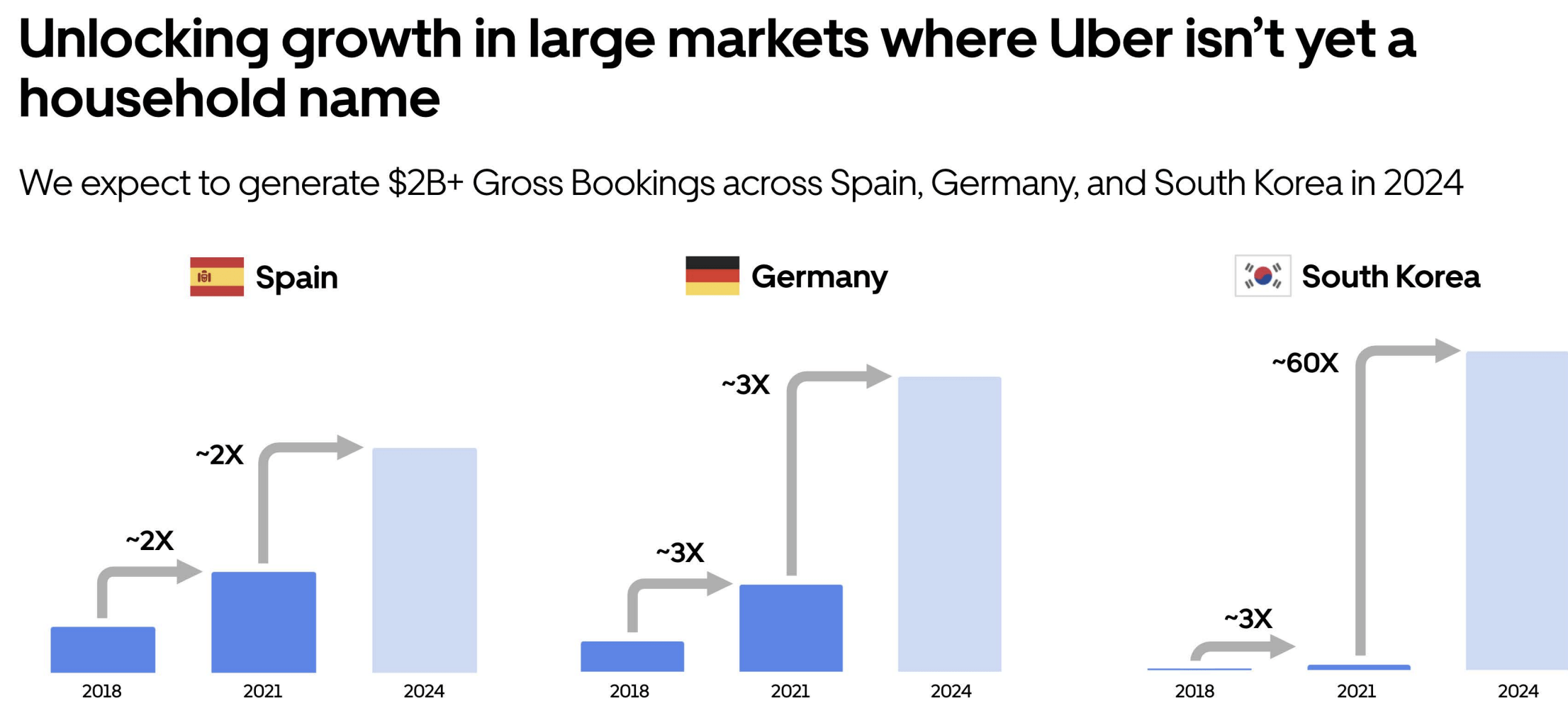

Expanding into new markets could be another revenue driver for Uber. Uber has already expanded to many countries around the world, but there are still many untapped markets that the company could potentially enter or markets that offer great expansion potential. Mainly in Europe, the company still has large markets where the company is not yet a household name as the slide below shows. Management expects to be able to significantly increase gross booking value across these markets, which gives the company plenty of growth runway to go. I believe management will be able to execute on these plans as they have done over the previous decade.

{kind=link}

In addition to this, Uber plans on increasing the attractiveness of its platform by getting every taxi on Uber by 2025. This should provide Uber with an additional supply of drivers for its customers, unlock new markets, and lower costs. All while giving taxi drivers a platform to increase their service. Uber reported $400 million in gross bookings originating from taxi services on the platform but expects this to increase to a more meaningful $3+ billion by 2024. Right now, Uber taxi is live in 27 countries and the company saw 122,000 new taxi drivers join the platform in 2021 (4x YoY). This is likely one of the larger growth contributors for Uber over the next 2 years and is a great focus area for Uber to expand its presence and service.

Growth through cost reduction

With Uber not being able to generate a positive EPS and only recently managing to report a positive EBITDA margin, margin expansion is a priority for Uber. The recently reported free cash flow is a positive sign, but investors are looking for more. Luckily, Uber has plenty of ways to accomplish this.

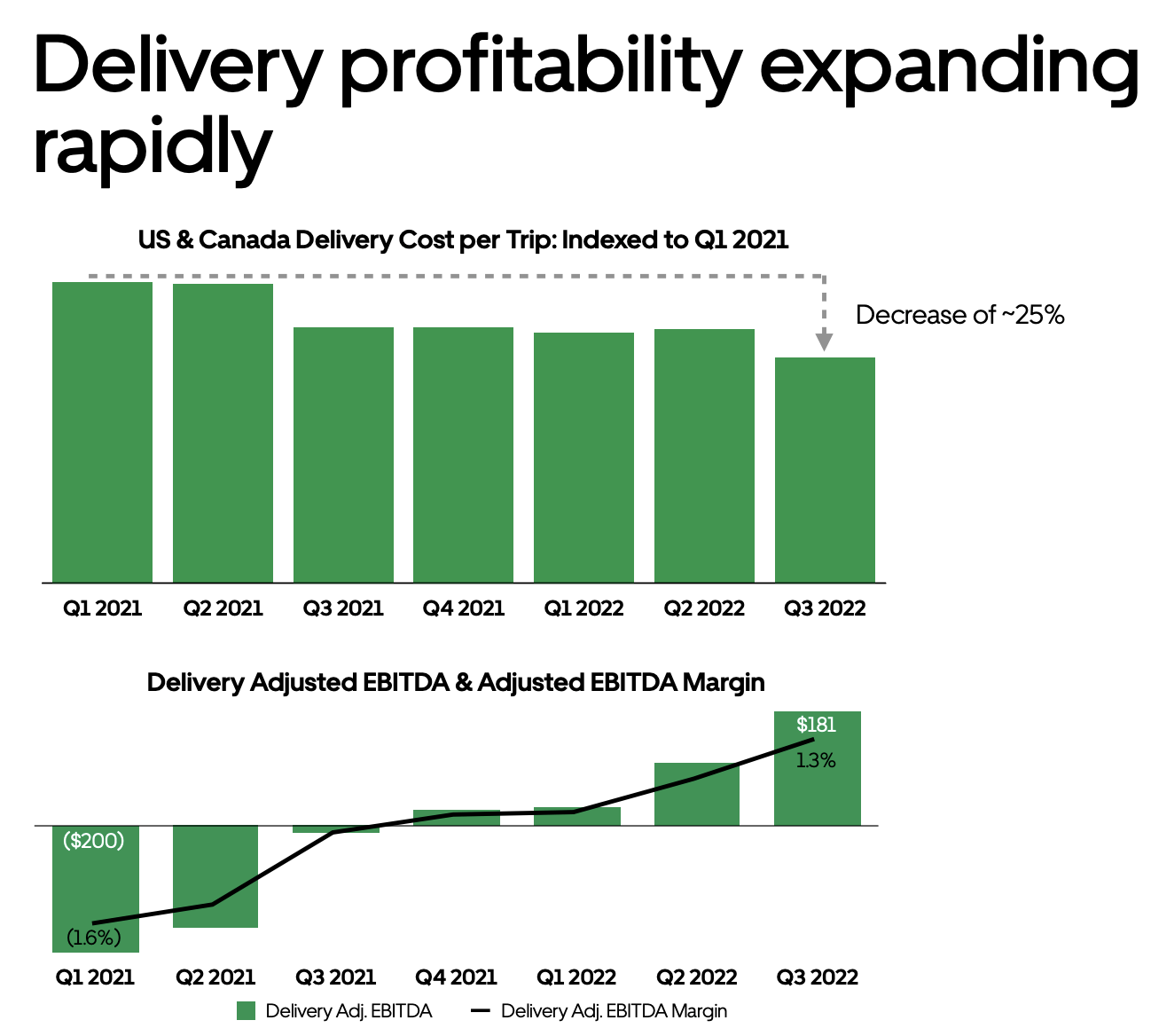

Uber has seen its EBITDA margins improve massively for its delivery segment due to healthy reductions in cost per trip which was enabled by product and technology innovations. In North America, cost per trip is down 25% since Q1 2021. Additionally, they expect Delivery to continue benefiting from the growth of advertising revenues and from continued sales and marketing leverage. With the segment continuing to grow and advertisement revenues expected to increase rapidly, I believe we will see much stronger margins going forward and the company could start reporting a positive EPS within the next 4 quarters.

{kind=link}

One of the more long-term opportunities for Uber is the deployment of self-driving vehicles for its ride-hailing service. Uber currently pays the driver over 70% of the gross booking dollars, massively eating up its margins. If Uber would be able to successfully deploy self-driving cars it would only need to pay for fuel/electricity costs, and this would meaningfully increase its margins. Uber collaborates with Alphabet-owned Waymo ( GOOGL ) to use its self-driving technology for the use of trucks for Uber freight services. Uber acknowledges the self-driving opportunity and acts on it. Yet, as long as there is no possibility of launching a fleet of self-driving taxis or trucks, I won’t value it too much when considering an investment in Uber as I am not willing to pay for innovations that are most likely still many years away. I will, therefore, not go too deep into this opportunity within this article.

Freight

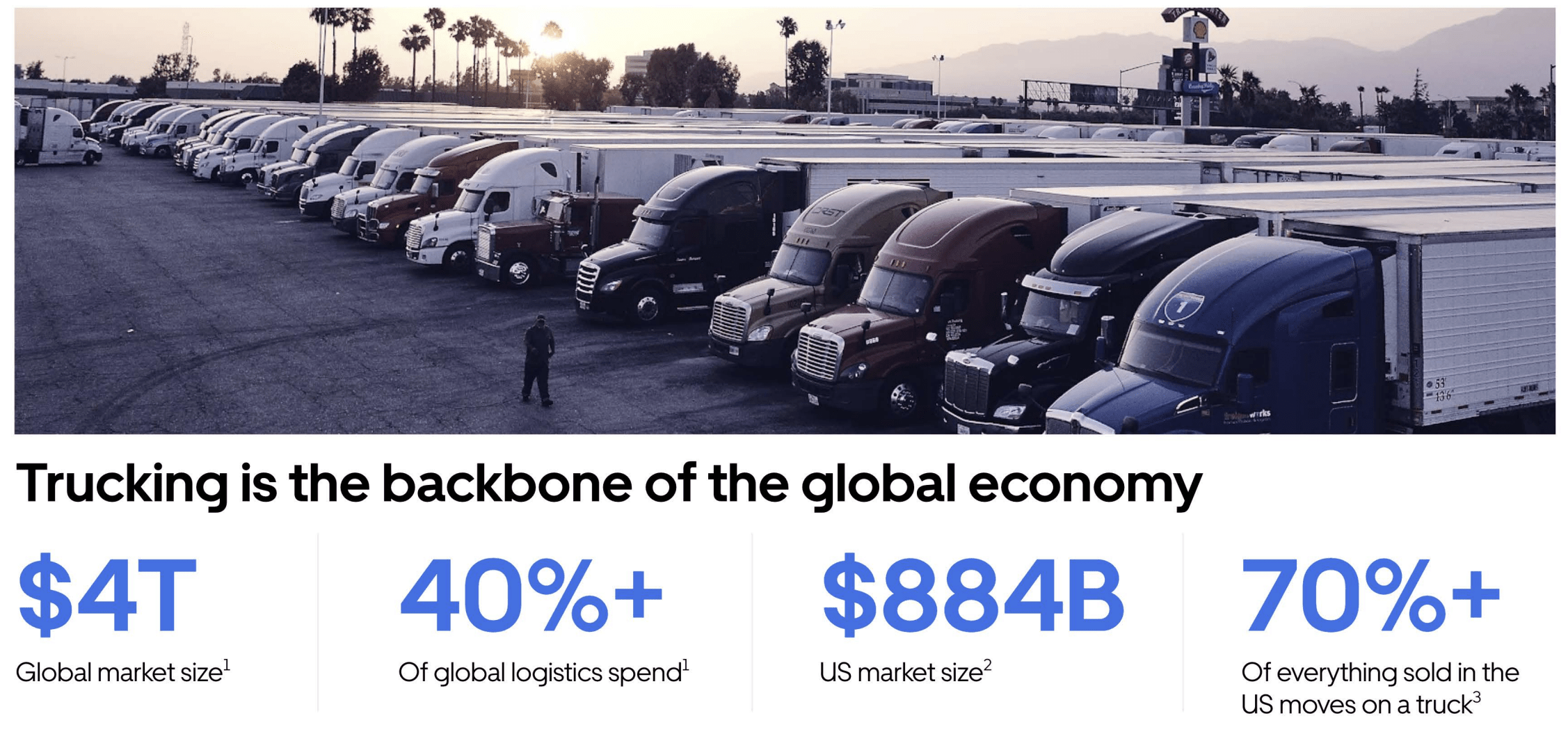

One of the less well-known segments of Uber is the freight segment, which also sees great growth potential. Uber showed this by using the slide shown below from their investor presentation at the start of 2022.

{kind=link}

Uber Freight is a platform that connects trucking companies with shippers who need to transport goods. The platform allows shippers to request quotes for trucking services and to book and pay for shipments online. Uber Freight was launched in 2017 as a way for Uber to enter the $800 billion trucking industry. The platform is designed to make it easier for shippers to find and book trucking services and for trucking companies to find and fill available capacity.

An Interview from McKinsey with Lior Ron, head of Uber Freight, gave us a good insight into just how Uber expects the freight segment to grow. Uber takes a technology-first approach to solve inefficiencies in the business and drive profitability for trucking companies. In the interview, Ron explained that the trucking industry is still very old-fashioned as it mainly works by phone, fax, or paper instead of digital planning solutions. As a result, 30% of the trucks you see on the highway are most likely empty. In a time where energy and fuel prices are high and shipping costs are elevated, efficiency is key.

This push for digitalization has made Uber one of the largest logistics companies in the U.S., as the network manages $17 billion in freight. Almost half of all carriers are using the platform nowadays and Uber plans to massively expand by making acquisitions and penetrating new markets. When asked about his expectations in 5 years, he answered the following:

In five years, I envision a true end-to-end platform for logistics, probably cloud based, where we are connected at scale with every carrier and every shipper and every warehouse across the world. We’ll have built a digital representation of the entire complex physical infrastructure. This capability will allow us to reduce costs for shippers and increase utilization and earnings for carriers.

This platform will also cover all transportation modes horizontally—rail, truck, and last mile—and with the Transplace acquisition, we’ll also have the most comprehensive vertical proposition.

We’re also going to see the critical adoption of both electric and autonomous vehicles in our network. We want to make a real impact in terms of sustainability, and this would also help with the shortage of truck drivers.

We’re still in the early days. Even though we’ve built $17 billion of freight under management, there’s $800 billion in the US logistics market. Our vision will stay the same: simplifying the movement of goods to help communities thrive. We’ll still apply a tech-first approach to the market and simplify processes to no end.

I expect Uber to increase the revenue contribution of the freight segment over the next few years and therefore drive growth in this very large and growing industry. As Uber increases its presence and importance, take rates are expected to go up and drive solid profitability.

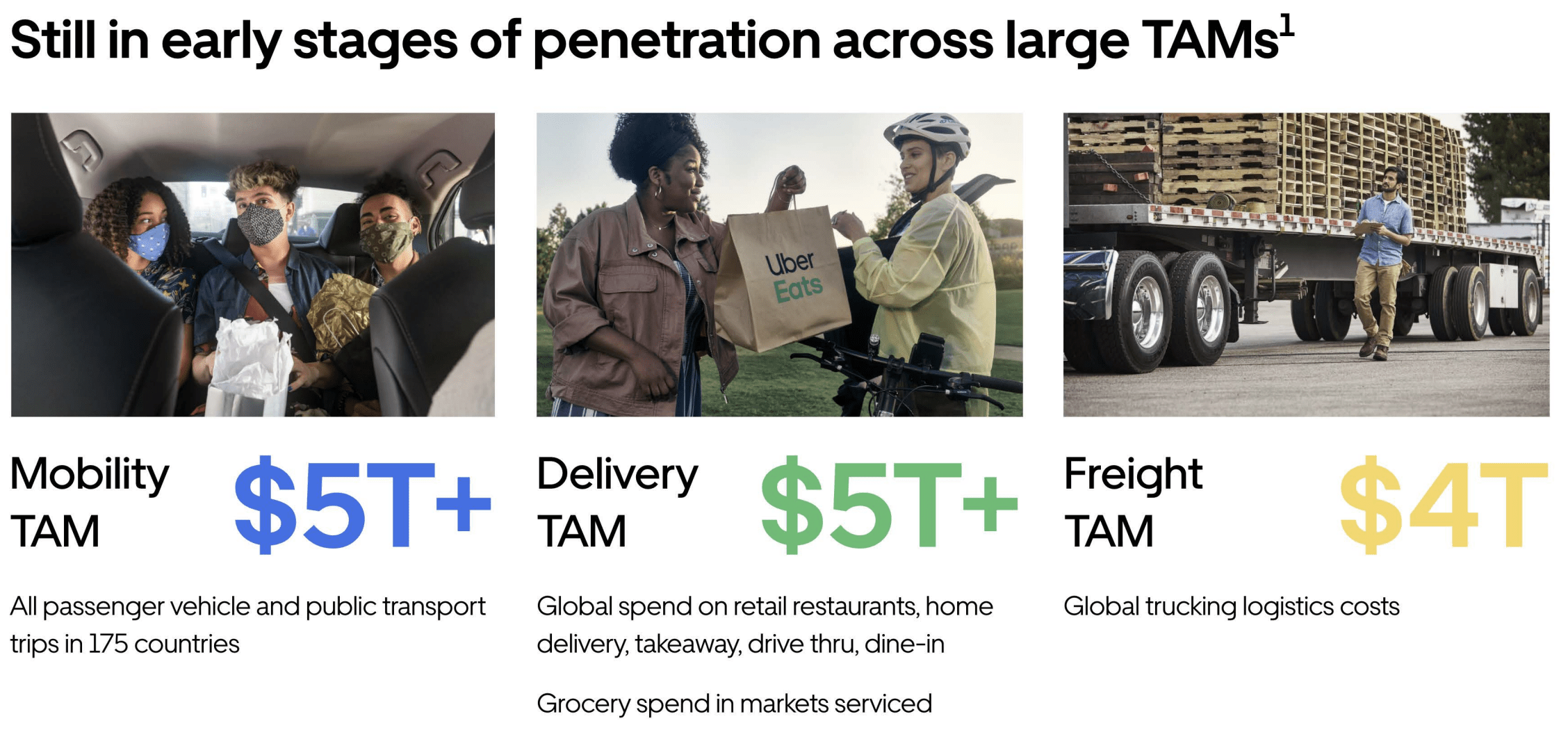

All in all, Uber looks set for strong growth going forward as the company has plenty of levers to pull and the ability to easily expand. With margins increasing and profitability simply a matter of time, I believe the company is very well positioned for continued growth and expansion of the total addressable market ("TAM"). Still, this does not make the company a risk-free investment. It is never that simple.

{kind=link}

Risks

While the company has very strong growth drivers and looks well-positioned to expand its business and financials, Uber is also facing significant risks and headwinds.

Competition

One of the most important ones to consider is the issue of intense competition. Whereas Uber has a leading position in many of its segments, most segments are relatively young and see high competition from start-ups. Take the delivery industry, where there are many alternatives to Uber, sometimes cheaper, like Just Eat ( JTKWY ), Grubhub, or Deliveroo ( DROOF ). It is most of the time the more local competitors that are the toughest to beat. Also, in the ride-hailing industry, Uber is having serious competition, mainly in the U.S., from Lyft ( LYFT ). It will be important for Uber to stay ahead of the competition, but this could result in higher promotion costs which in turn are bad for margins.

Regulatory hurdles

Uber has also seen many regulatory hurdles in the past and these are not expected to ease any time soon. While there is not much use in bringing up past lawsuits, it is important to be aware of the risk that Uber will most likely face more lawsuits over the next couple of years as it increases its presence. Still, lawsuits and regulatory hurdles are nothing new as these are often witnessed when companies disrupt traditional models and challenge existing laws and regulations. I do not foresee Uber getting in any serious trouble, but at the same time, these lawsuits are often hard to foresee. Right now, the biggest regulatory issues for Uber seem to be around the subjects of the classifications of its drivers and transportation regulation. Back in October Seeking Alpha reported that the Biden Administration issued a proposal that could result in gig economy workers becoming full-time employees. This would include ride-share drivers. Quickly after the news, Lyft released a blog post which stated that they would not be impacted by the new regulations as it would not require them to reclassify their drivers as employees. Still, it does create some uncertainty for the industry, and this could pressure the share price of Uber.

Probability of a recession

Finally, one risk that needs to be discussed for any investment right now is the probability of a recession. I can’t see the future and so it is hard to predict whether we will enter a recession somewhere in 2023. The economy seems to be resilient but is being pressured by high inflation and rising interest rates. Right now, I do not believe we will be entering a recession and if we will, this will most likely be a mild one. Still, this could have an impact on Uber as unemployment might rise slightly and consumer spending growth will slow down. Although I do not foresee this to have a huge impact on Uber, lower consumer spending could result in a slowdown in growth for Uber as people will look for more affordable ways of transport such as public transportation.

Balance Sheet

Uber had a strong cash position at the end of the latest quarter with $4.9 billion in cash and cash equivalents. Total debt was $11.27 billion, and Uber, therefore, holds a net debt position. While this is not ideal with the company not being very profitable yet, it is generating positive free cash flow, and the profitability is expected to significantly increase over the next few years. The cash position allows Uber to explore M&A opportunities to expand the business and TAM.

Conclusion

With Uber now down close to 40% over the last year, I believe the share price is now attractive enough to warrant a buy rating on the company. Uber has significant growth potential driven by increasing profitability, great scalability, and a strong competitive position. The ride-sharing service is in an excellent position now that the world has fully reopened and new initiatives such as advertising, ride-sharing, and expansion into new markets will drive revenue growth and operating margins for Uber. Also, the delivery segment will likely continue to grow at a solid pace as delivery of groceries and meals is here to stay. The main threat to these business segments seems to be regulatory scrutiny and competition, but Uber has shown to be able to fight of these threats in the past.

Current analysts' estimates predict Uber to report a positive EPS for FY24. I believe this is a fair estimate. At the same time, the revenue projections seem to have priced in an economic downturn already with 16% growth projected for the current calendar year. Uber could be able to grow at a faster clip and beat current estimates to report growth of above 20% for the next year, but this looks challenging.

To conclude, I believe Uber is a no-brainer to any long-term investor with a time horizon of at least 5 years. Yet, as long as Uber is not reporting solid profits, I would recommend limiting the size of any position in Uber.

I rate Uber Technologies, Inc. a buy on strong fundamentals and a fair price.

For further details see:

Uber: Poised For Continued Growth