UBER - Uber Q4 Earnings: Growth Not As Strong As It Seems

Summary

- Uber's share price is already up nearly 40% year to date.

- A lot of optimism came from its latest earnings which reported strong growth and profitability.

- However, a lot of it came from non-operating benefits.

- The current valuation seems stretched after the rally.

- I rate the company as a hold.

Investment Thesis

Uber’s ( UBER ) performance has been underwhelming since going public. It is currently down over 40% from its all-time high and still trading 20% below its IPO price. The company has recently come alive with shares up nearly 70% from its 52-week low. A lot of optimism came from the surprisingly strong growth and profitability in its latest quarterly earnings. But if you dive deeper into the report, the results might not be as good as claimed. After the rally, the current valuation also looks a bit stretched, especially with revenue growth slowing this year. I like the company’s prospects but I do not see much further upside at the moment. Therefore I rate Uber as a hold.

Q4 Earnings

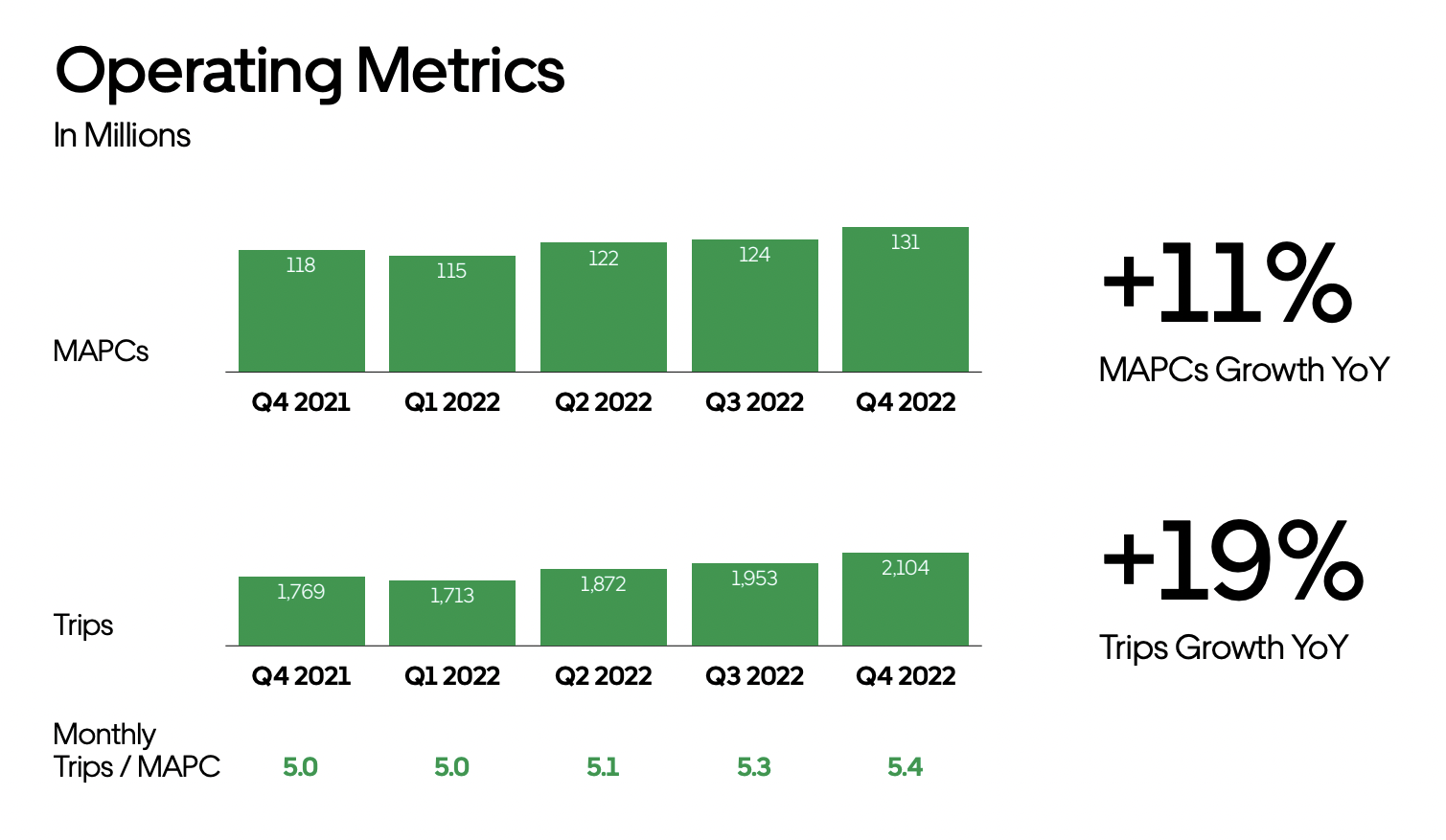

Uber reported its fourth-quarter earnings earlier this month and the results seem very strong, especially on the top line. However, this is mostly caused by multiple business model changes which affected the income statement. Excluding these changes, the result isn’t actually that impressive. At first glance, revenue increased 49% YoY (year over year) from $5.78 billion to $8.6 billion. But you can already tell this is not organic as total bookings and trips only increased 19% YoY. Monthly active platform consumers were up even less with just an 11% increase YoY from 118 million to 131 million.

{kind=link}

Uber

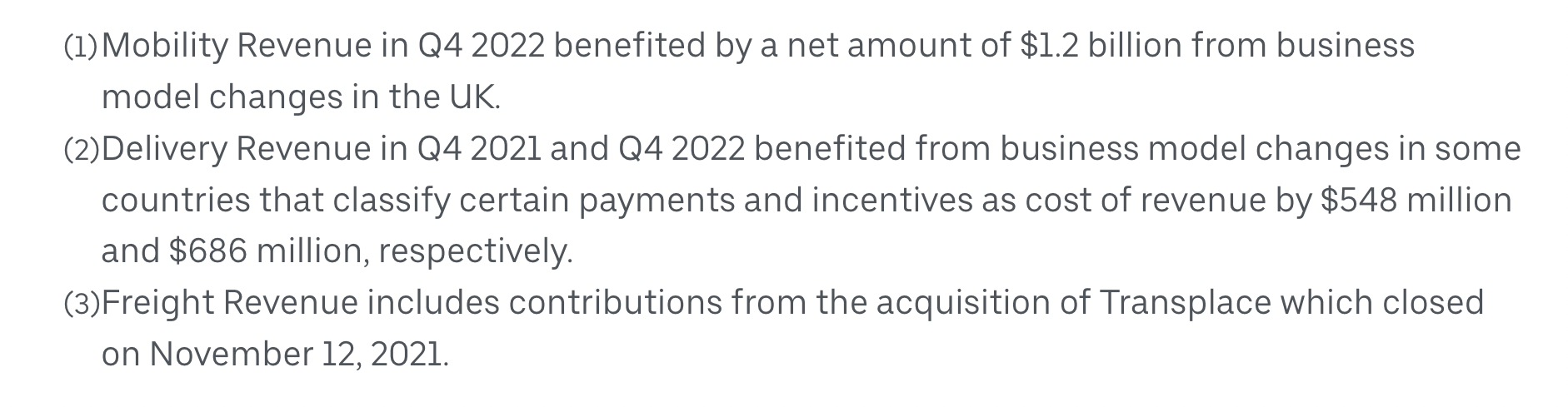

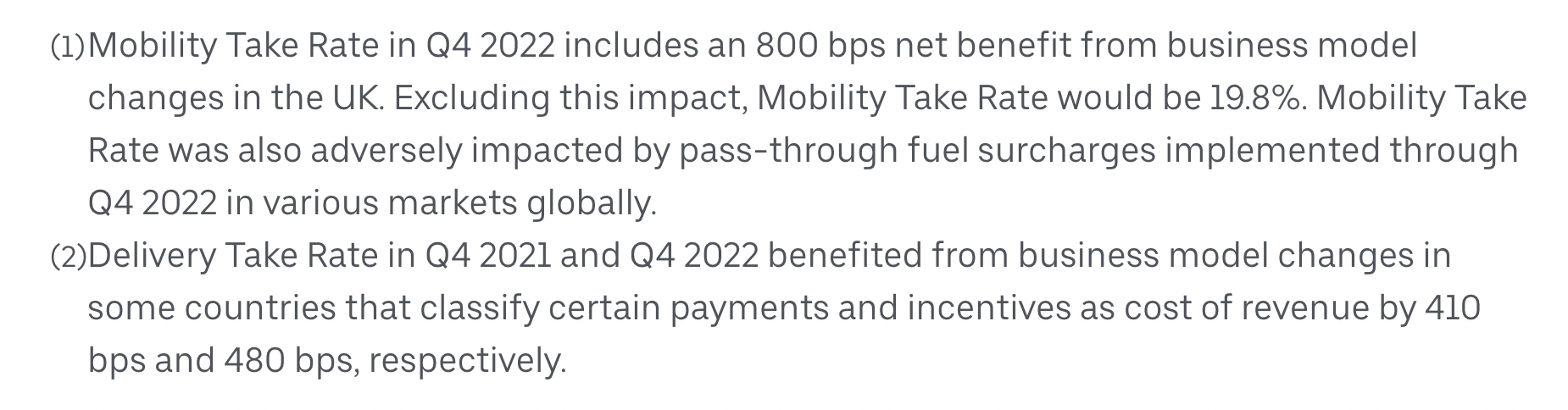

If we dive deeper, mobility revenue benefited by $1.2 billion due to a change in the business model for the UK mobility business. Excluding the changes, mobility would be $2.94 billion rather than $4.14 billion, and the YoY growth increase would be 28.9% rather than 82%. The segment’s take rate would also be 19.8% rather than 27.8%, which would mean a 30 basis points drop YoY rather than a 770 basis points gain.

Due to business model changes in some other countries (not UK), delivery revenue also benefited by $686 million this quarter and $138 million on a YoY comparable basis. The segment’s take rate benefited from a 480 basis points increase and a 70 basis points spread YoY. Excluding this take, the rate would be 15.7% compared to 20.5%. The YoY increase would also be 180 basis points rather than 250 basis points.

{kind=link}

Uber

{kind=link}

Uber

Freight revenue also included the acquisition of Transplace . The company did not disclose its revenue but we can do some calculations and make an estimate. The acquisition was $2.25 billion and assuming it was purchased at a PS ratio of 2x (Uber is currently trading at ~2x), this gives us an annual revenue of around $1.1 billion and quarterly revenue of roughly $280 million. This means excluding the acquisition, freight revenue would actually be $1.26 billion rather than $1.54 billion, which represents a YoY increase of 16.7% rather than 43%. If we exclude all the benefits, the total revenue would be $6.44 billion rather than $8.61 billion. Growth would be 23.2% rather than 49%.

The company also isn’t as profitable as it looks. Gross profit only increased 23.6% from $2.67 billion to $3.3 billion as costs of sales were up 71% to $5.3 billion. The gross profit margin declined significantly from 46.2% to 38.3%. This quarter’s income included a net unrealized gain of $756 million related to the revaluation of Uber’s equity investments (which is likely due to stocks rallying in January). Excluding this, the company would’ve posted a net loss of $(161) million rather than a net income of $595 million. It is also worth noting that the company’s operation still isn’t actually profitable, as it posted an operating loss of $(142) million. Not to mention revenue benefited from all these changes. The operating/net loss would be much larger if it didn't.

{kind=link}

Uber

Overall, I don’t think this quarter's financial result truly reflects the company’s operating performance as external changes heavily impacted the financial statement.

Investors Takeaway

After the massive rally, Uber seems fairly valued in my opinion. The company is currently trading at a fwd PE ratio of 37.6x (on a Non-GAAP basis) which is not cheap by any means. This would be justified if the revenue growth truly is 49% but 23.2% on an adjusted basis is not enough to support further multiple expansion. Not to mention revenue growth is expected to slow to the mid-teens in FY23, according to Seeking Alpha’s analyst estimate .

Uber is not a bad company at all and I do like its prospects, especially with Lyft ( LYFT ) struggling which could reduce competition. However, I do not think now is the right time to buy yet. The latest earnings result was affected by too many changes and it is hard to see the company’s real operating performance. I would like to see more clarity in regard to profitability and operating leverage. The valuation is also a bit stretched after the rally and with slowing growth, I do not see much further upside potential. Therefore I rate the company as a hold.

For further details see:

Uber Q4 Earnings: Growth Not As Strong As It Seems