UBER - Uber: You Won't Regret Holding For The Long Term

Summary

- In spite of a stock price that has sunk 40% this year, Uber's fundamentals have held up incredibly well.

- Ridership is now back to pre-COVID levels, and overall company bookings are growing at a ~30% y/y clip.

- Revenue is growing much faster at a ~80% y/y clip, thanks to a huge jump in take rates.

- At the same time, the delivery business has now reached adjusted EBITDA profitability.

I can't say it often enough: now is exactly the time that long term-oriented investors should roll up their sleeves and buy "underwater" stocks. The market this year has shunned almost all growth stocks in spite of strong fundamental performance from many, and investors who are able to shoulder some short-term volatility have an excellent opportunity to nab excellent rebound plays.

Uber ( UBER ), in particular, is a stock worth revisiting. The global rideshare giant has seen a 40% decline in its stock price this year - despite operating results that demonstrate both post-pandemic resilience and excellent future growth trajectory. It's worth noting that now in the mid-$20s, Uber stock is now trading below where it was at the start of the pandemic - despite the fact that the ride business has fully recovered, and the delivery business has scaled tremendously to profitability.

Uber remains a core holding in my portfolio, and I remain very bullish for the company's prospects in 2023 and beyond. When I take a step back from the short-term noise, I continue to see secular tailwinds playing out in Uber's favor: more migration toward dense urban centers, a decline in car ownership, and the convenience of micro mobility solutions like Uber continuing to dominate.

Here is the full long-term bull case for Uber:

- Huge $13.8 trillion TAM- Mobility and Delivery each carry $5 trillion market opportunities, and nascent Uber Freight is another massive $3.8 trillion market that is heavily underserved and ripe for tech disruption.

- Formidable market leadership- In most of the markets that Uber operates in, the company has a leading market share, and usually by a substantial margin. The company has selectively exited markets where it lost share to a local incumbent (Grab in Singapore is a good example), so it can focus on turf where it has the advantage.

- The sharing economy is gradually taking precedence over ownership- Even pre-pandemic price inflation caused many to rethink buying cars, many consumers were already questioning the wisdom of car ownership over rideshare. Owning a car comes with maintenance costs, insurance costs, and in urban areas, often hefty parking costs. Gradually, I expect car ownership to decline and for rideshare to become the preeminent form of transportation.

- Uber One- Uber recently unveiled a $10/month subscription membership that offers, among other benefits, free deliveries on Uber Eats and a 5% discount on rideshare. In my view, this move will help to boost rider loyalty and frequency on top of generating a new subscription revenue stream.

- "Other bets" are numerous- Uber Freight is the best example of a new initiative to drive growth, but grocery and package delivery are others as well. Uber's focus on anything involving mobility gives it a massive greenfield market to operate in.

- Profitability is sinking back in- Driven by the uptick in rideshare volumes plus higher take rates in both the rideshare and delivery businesses, Uber is driving tremendous Adjusted EBITDA growth.

Over a ten to twenty-year timeframe, I continue to see Uber's dominance in our daily routines growing. Take advantage of recent volatility as a tremendous buying opportunity.

Q3 showcases vibrant operating trends and surging profitability

The big paradox with Uber: even though its share price has slid dramatically this year, its actual financial results demonstrate tremendous strength.

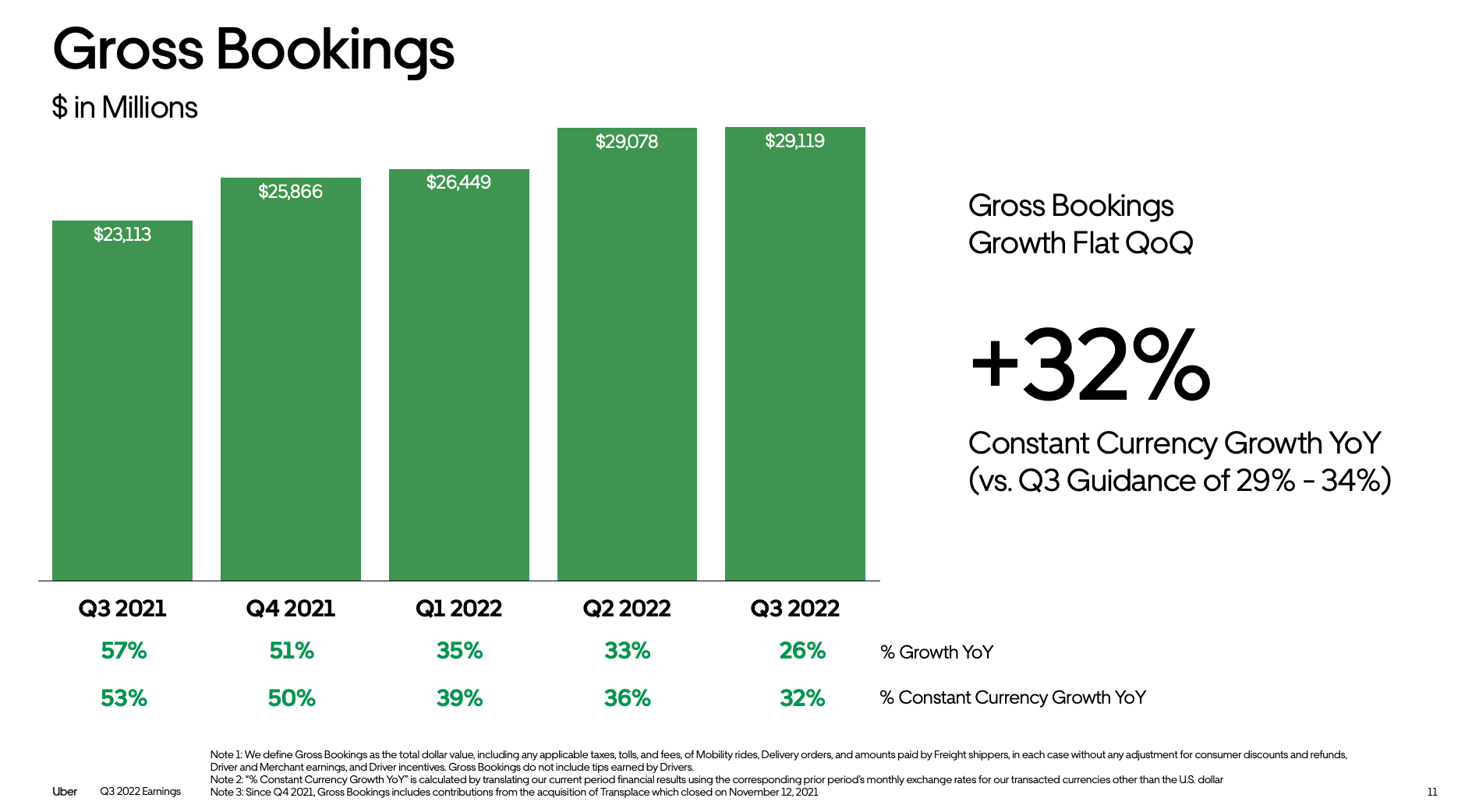

In early November, the company released results for the September quarter. Bookings grew 26% y/y on an as-reported basis, weighed down like many other companies by the strengthening dollar. On a constant-currency basis, bookings grew 32% y/y:

{kind=link}

Revenue grew even sharper at 81% y/y on a constant currency basis, driven by an eight-point y/y increase in take rates: the result of fee increases including fuel surcharges.

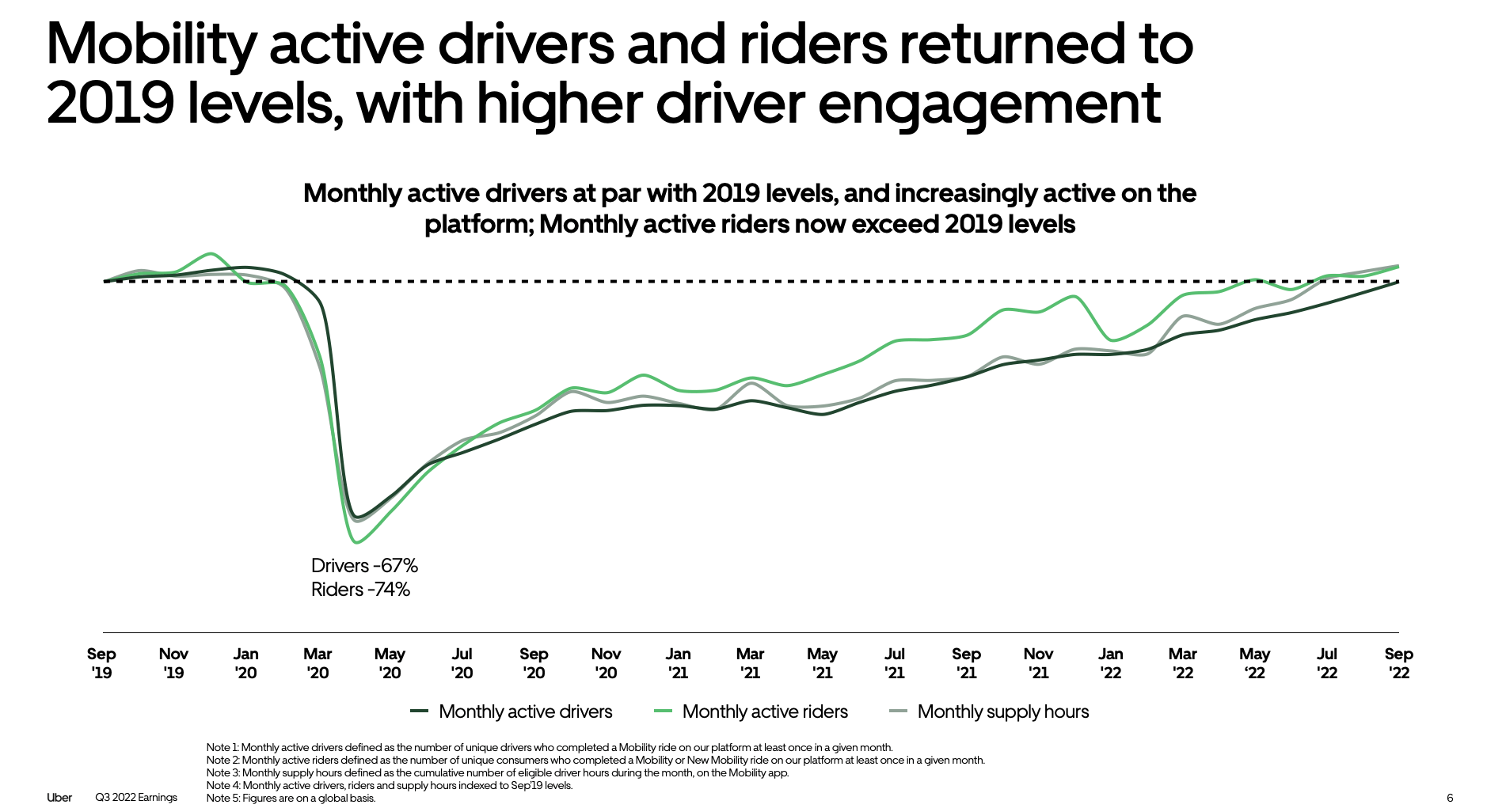

We note that in spite of price increases, Uber ridership has continued to be robust. The chart below shows that monthly active drivers and riders have returned to 2019/pre-pandemic levels:

{kind=link}

The company notes as well that membership on Uber One is now at over 10 million global members, providing a healthy $100 million/month revenue stream. Here's some additional color on the drivers for ridership taken from CEO Dara Khosrowshahi's prepared remarks on the Q3 earnings call:

Underlying this performance are several trends that represent tailwinds for us. Cities are reopening; travel is booming and more broadly, a continued shift of consumer spending from retail back to services. We've seen these trends continue into the fourth quarter with October tracking to be our best month ever for mobility and total company gross bookings. With over $1 billion in adjusted EBITDA of $693 million in free cash flow so far this year, we've demonstrated how our global scale and unique advantages of our platform are combining to generate meaningful profits and we're confident in our ability to build on this momentum."

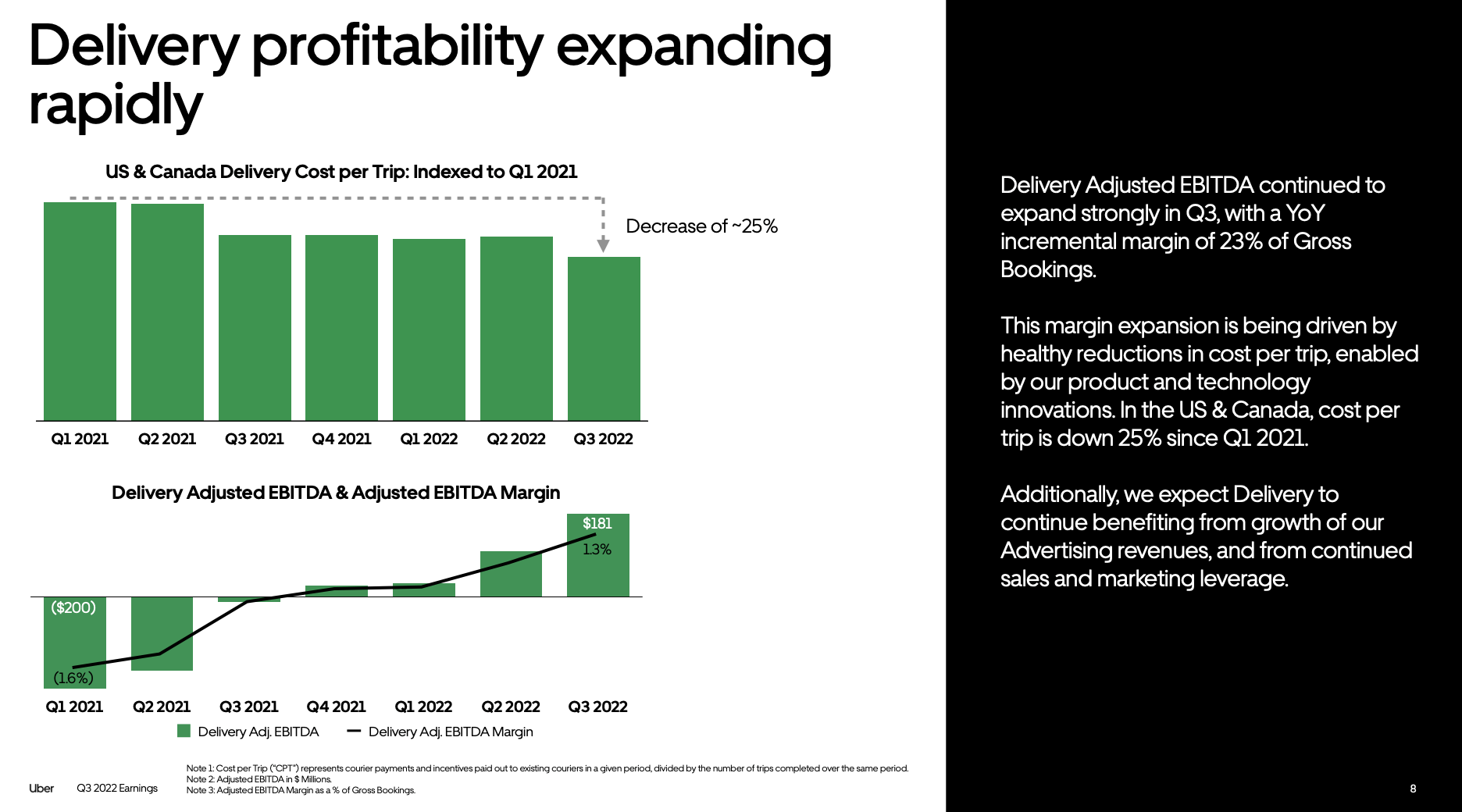

The company noted as well that it doesn't see any signs of delivery bookings slowing down - many had expected that delivery orders would decline post-pandemic as normal routines resumed. This has turned out not to be the case: delivery gross bookings grew 13% y/y to $13.4 billion, while revenue grew 33% y/y to $2.77 billion.

Scale, in turn, has helped the delivery segment reach levels of profitability that were thought elusive in the pre-pandemic era. Since 2021, the company notes that cost per delivery trip has decreased 25%. As a result, the delivery segment has reached a record adjusted EBITDA margin of 1.3% in the third quarter:

{kind=link}

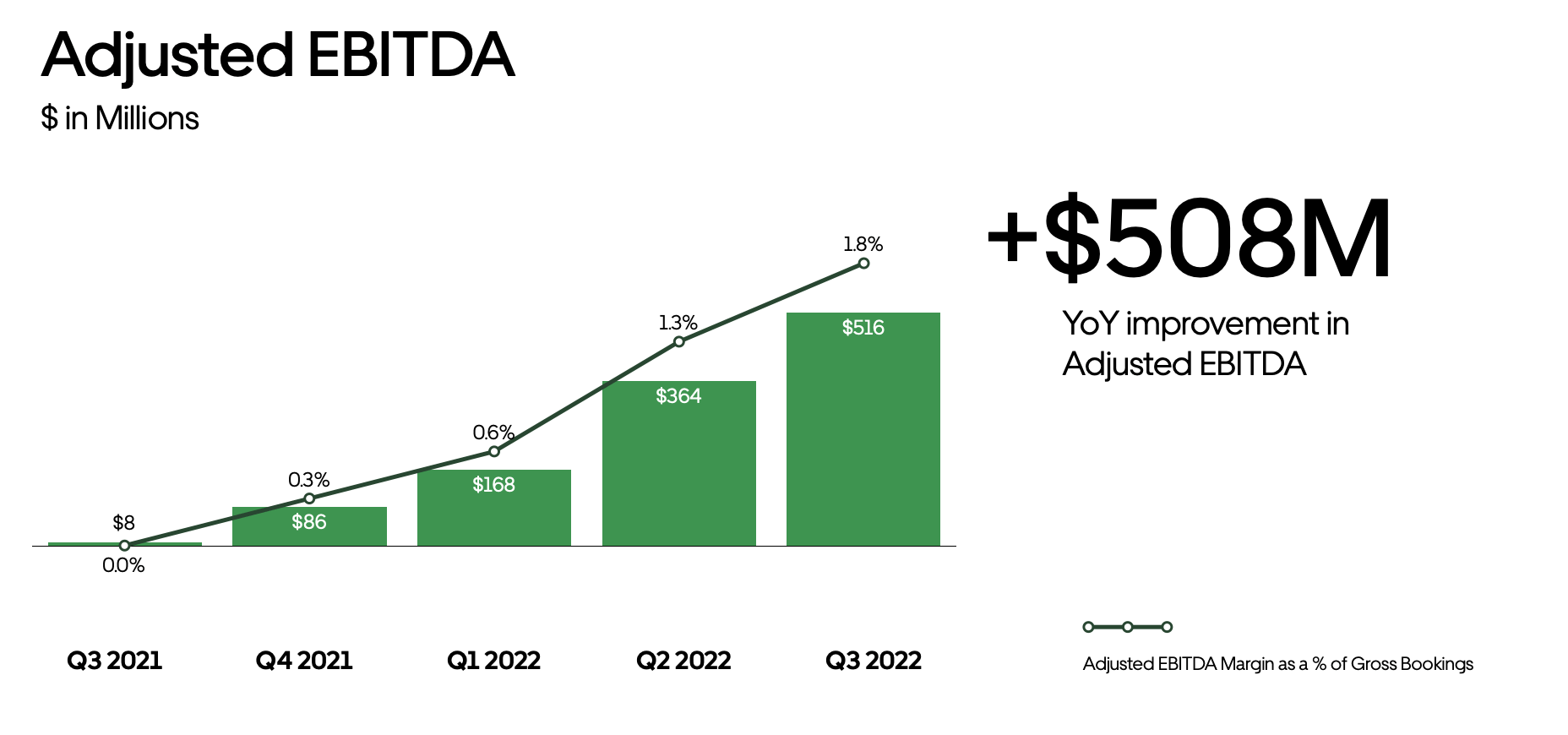

Overall, Uber's adjusted EBITDA soared to $516 million in the third quarter, representing a 1.8% margin.

{kind=link}

The company expects adjusted EBITDA to continue scaling sequentially, guiding to $600-$630 million in adjusted EBITDA for Q4.

Key takeaways

I see nothing but strength in Uber's most recent results, which makes its YTD stock declines look out-of-step with the reality of its fundamentals. I've ignored the company's recent day-to-day fluctuations and am confident holding onto this name for the long haul.

For further details see:

Uber: You Won't Regret Holding For The Long Term