BCLYF - UBS: Feasting Off The Credit Suisse Carcass

2023-03-22 15:36:04 ET

Summary

- UBS bought $65 billion of equity value for $3 billion.

- Loss backstops from the Swiss government can add more than another $9 billion of value.

- Day 1 tangible book value will be around $25/share versus the current $21 stock price.

- The remaining business will be comprised of 80% one of the largest asset managers in the world and the other 20% the largest bank in Switzerland.

- Chance for long-term value creation from a mix of cost cuts and future growth.

Deal of the Century?

Barclays ( BCS ) bought parts of Lehman Brothers, after the latter filed for bankruptcy in 2008. They got a first-class investment bank for $250 million and its New York headquarters building for $1.5 billion. The investment bank was acquired for the tiniest of fractions of where it would have traded only weeks before. Barclays got that deal because they were one of the only firms, if not the only firm, that could absorb Lehman at the time.

I see similarities in UBS's ( UBS ) acquisition of Credit Suisse ( CS ) over the weekend. UBS was probably the only possible buyer for CS, and it got an even sweeter deal than Barclays got. This deal will pay off for UBS immediately and then drive gains for years to come. I see around 20% in short-term upside with over 50% gains over the next 2-3 years and extremely limited downside.

Swiss Government Picking Pockets

Credit Suisse had over $48 billion of equity at the time of the transaction. Furthermore, about $17 billion of AT1 paper (categorized under debt) was wiped out by the SNB (Swiss National Bank), which moves dollar for dollar to equity.

That means that UBS is adding $65 billion of equity for the cost of $3 billion of stock. My quick math tells me that's $62 billion of added value, almost 21x. It immediately adds 75% to UBS's tangible book value to $25/share (versus the current price of $20.50/share as of the time of this writing). Now there will undoubtedly be losses as UBS writes down the value of CS's assets and absorbs some operating losses and restructuring costs. UBS is getting a sweet deal here too. They are on the hook for the first $5 billion of these losses, and then the SNB takes on the next $9 billion of losses. Any losses above that total of $14 billion is split 50/50 between UBS and CS. If you just add the initial loss absorption and the entry cost/benefit, UBS is paying a total of $8 billion for $71 billion of value.

UBS Future Earnings Power

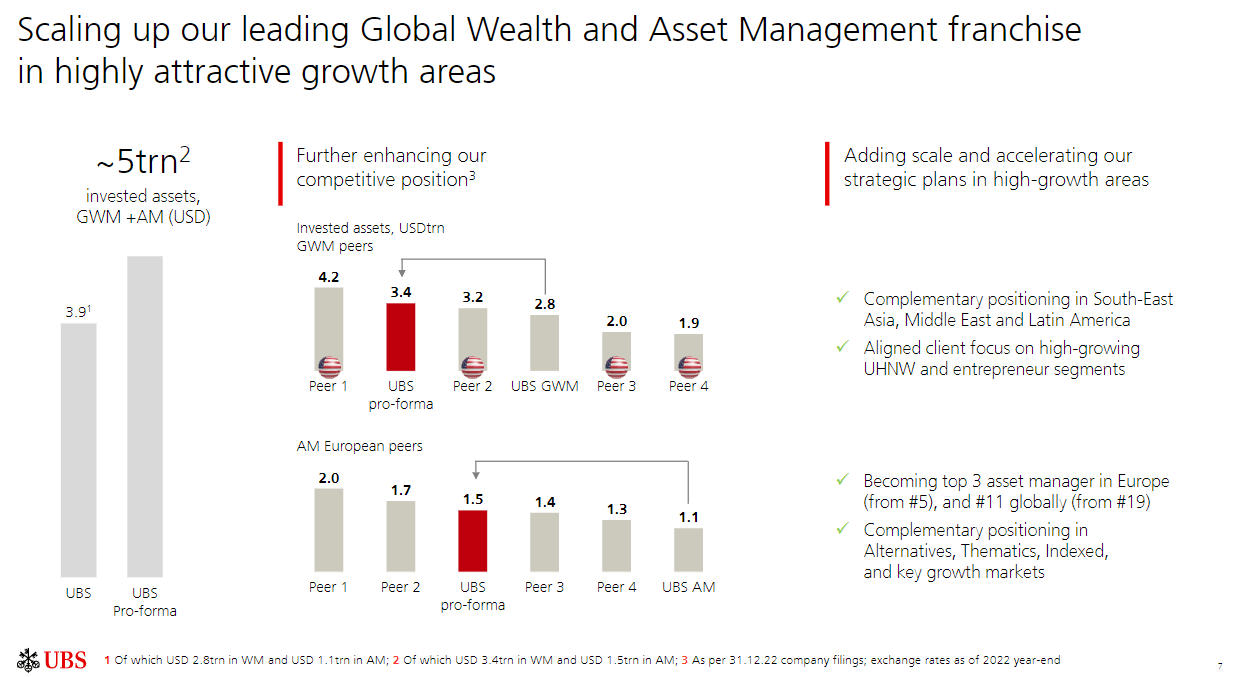

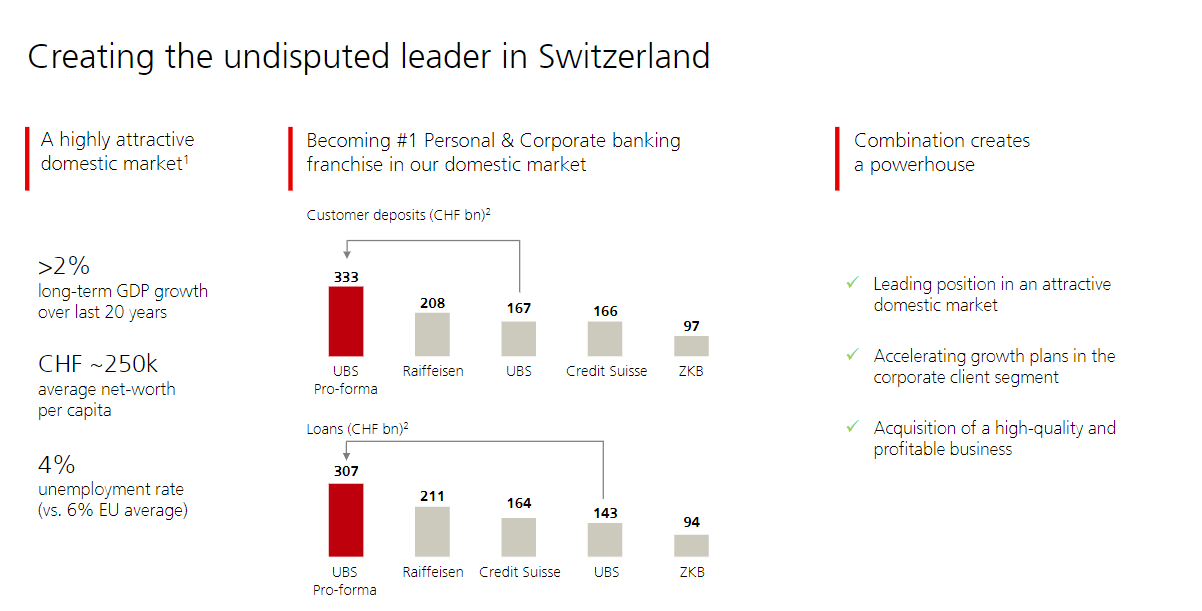

UBS will almost certainly shrink the investment bank at CS. The company laid out that, post-merger and clean-up, it will be a $5 trillion wealth manager and the largest retail bank in Switzerland (50% larger than its next largest competitor).

{kind=link}

{kind=link}

The new bank will be 80% wealth management and 20% this Swiss retail banking giant. That mix ought to gain a nice multiple bump from 9x to 12x, where Morgan Stanley ( MS ) trades.

Any multiple would be a plus. UBS is estimating that this deal will be earnings accretive by 2027. I think they are sandbagging here. They estimate that they will be able to realize about $8 billion of cost savings by 2027. If we straight line that over four years, it's an incremental $0.57/share per year of earnings power pre-tax starting year one and growing to $2.25/share. This will be offset initially by markdowns and losses, which will cap out at $5 billion. I think that the market will look through these writedowns and focus on the operating profit growth. Just putting a 9x multiple on that incremental earnings power is about $20 of value. More than double where the stock is right now.

Risk

There will be operational risk here, particularly with integration issues. There's also just the normal risk of UBS's current exposure to worldwide asset values. Lastly, the crushing of CS AT1s will hurt UBS's cost of funding as people assume risk with UBS's paper. Once again, however, the SNB is backstopping UBS with $100 billion of available liquidity. Their funding is secure.

Conclusion

Overall, gifts like this are rarely available in the market and even more rare for governments to play such a huge role in creating value for a private enterprise. I think any risk of loss from CS assets or operational snafus is way more than compensated for by the day-one boost in tangible book value and then future growth in profitability (without assuming any revenue synergies). I see a 20-25% short-term upside to the new $25 book value and potential for a 100% upside over the next few years as earnings grow without considering potential multiple expansion.

For further details see:

UBS: Feasting Off The Credit Suisse Carcass