UCL - uCloudlink Group: Not A Good Time To Get In

2023-04-10 23:27:43 ET

Summary

- Just when you thought things were going to get better for UCL: Likely recession.

- While important markets are opening up their borders in 2023 and 2024, an expected weakening global economy is likely to offset growth potential in the near term.

- Once markets do sustainably recover, the company should have sustainable and consistent growth on the top and bottom lines, led by international connectivity.

The share price of uCloudlink Group Inc. ( UCL ) has been soaring since October 11, 2022, when it hit its 52-week low of $0.46 per share, and since jumping to its 52-week high of $6.60 on February 1, 2023, before pulling back to trade at $3.80 per share as I write.

With the company operating in the mobile data traffic sharing sector, it was hit hard by travel restrictions associated with the travel industry in particular, but as many countries start to open up their borders again, it's providing an opportunity for the company to boost revenue while improving its bottom line, primarily from a more favorable service mix from growing its international connectivity business.

Since many countries like China and those in Southeast Asia are expected to recover to pre-pandemic travel levels of 40 percent to 50 percent in 2023, according to management, and be 100 percent recovered by 2024, it sees this as a solid growth opportunity going forward.

While I believe that's true, I don't share management's optimism in the near term, primarily because I believe the economic conditions in 2023 and early 2024 are going to get worse, which will have a negative impact on corporate and consumer spending on travel - both locally, regionally, and internationally.

For that reason, I think its opportunity will be pushed out further into the future, and as economic conditions worsen the share price of the company will take a big hit because of how quickly it has rebounded in anticipation of the increased opening of borders.

In this article we'll look at some of its latest earnings numbers, profitability metrics, and why it's probably going to get worse before it gets better for UCL.

{kind=link}

TradingView

Some of the numbers

Revenue for the fourth quarter of 2022 was $19.6 million, compared to revenue of $17.6 million in the fourth quarter of 2021, up 11.6 percent. Revenue for full year 2022 was $71.5 million, compared to revenue for full year 2021 of $73.8 million.

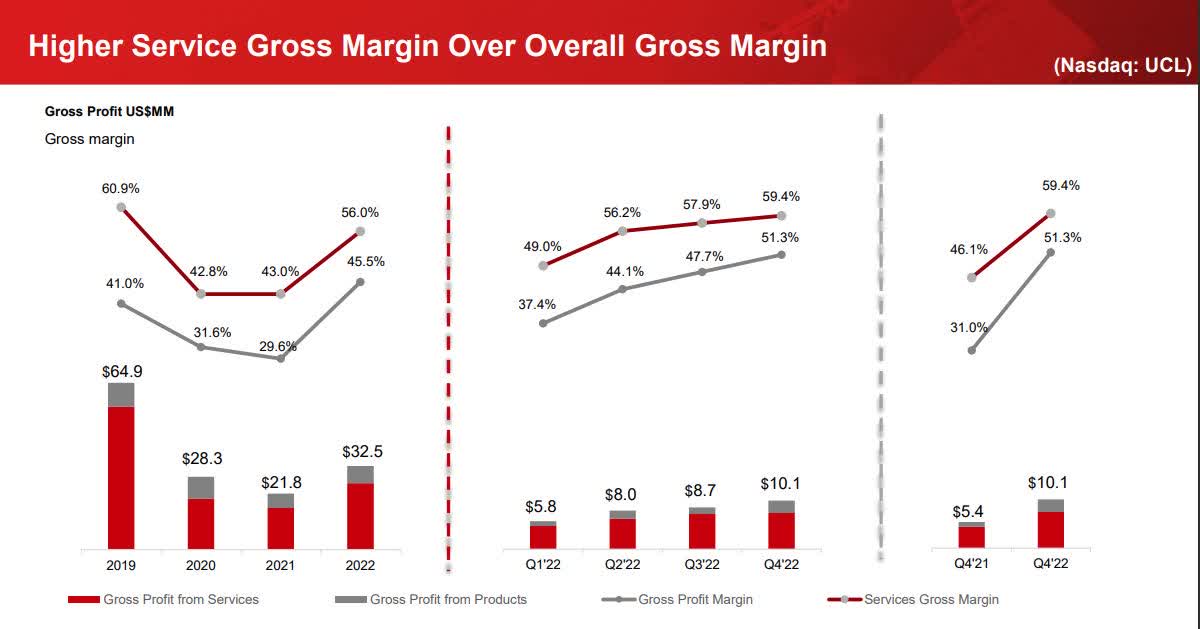

Revenue from services in the reporting period was $12.5 million, compared to revenue from services of $9.6 million in the fourth quarter of 2021. Revenue from products in the fourth quarter of 2022 was $7.08 million, compared to $7.95 million in the fourth quarter of 2021.

Full year 2022 revenue for services was $46.2 million, compared to $37.8 million for full year 2021. Full year 2022 sales from products were $25.2 million, compared to $36.00 million for full year 2021.

The decline in revenue for 2022 was attributed to a drop in sales of some terminal and data related products. That was reflected in the increase in service revenue as a percentage of overall sales from 31.2 percent in 2021 to 64.7 percent in 2022.

Revenue from international data for 2022 was $24.1 million, up 29.6 percent year-over-year, and revenue from local data connectivity was $7.4 million, up 35.5 percent year-over-year. The boost in data connectivity revenue came from the ongoing recovery of international travel, and the company rolling out more local services.

The significance of that is international data connectivity, overall, has higher margin, which was a major reason gross margin improved over the last year, from 29.6 percent in full year 2021 to 45.5 percent in full year 2022. Cost of overall revenue also improved from $52.00 million in full year 2021 to $39.00 million in full year 2022. Part of that appears to be from the decline in product revenue.

{kind=link}

Investor Presentation

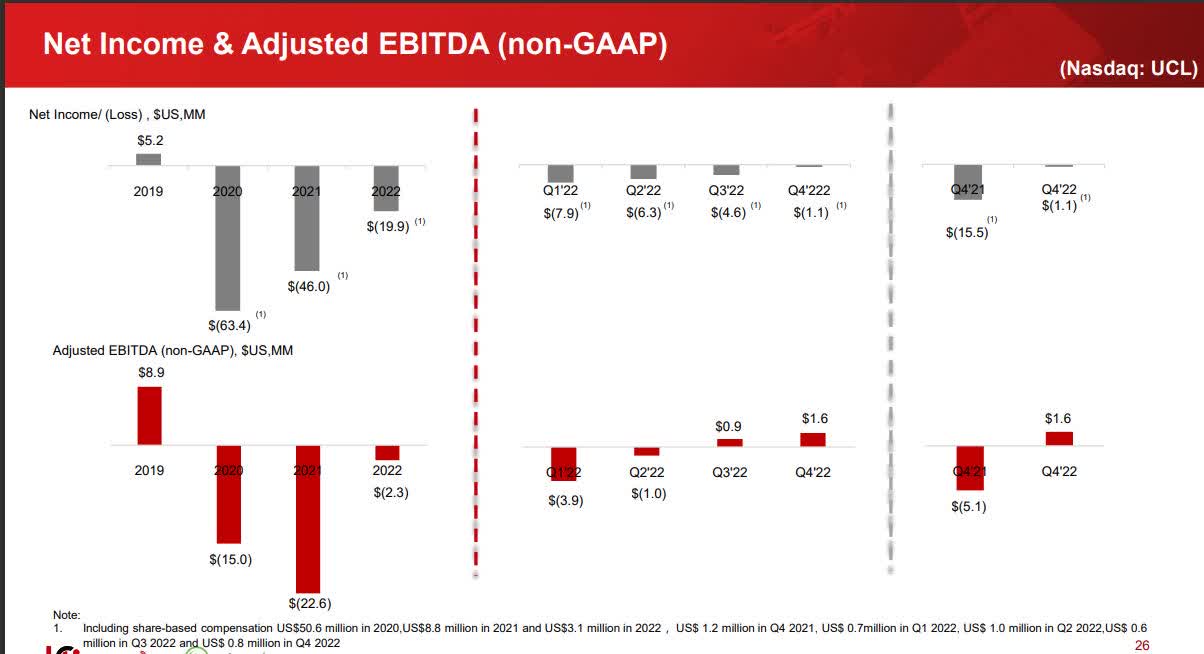

Adjusted EBITDA was $2.3 million for full year 2022, compared to adjusted EBITDA of -$(22.6) million for full year 2021.

Operating cash flow for full year 2022 was $4.4 million, compared to -$(21.7) million for full year 2021.

Net loss in the fourth quarter of 2022 was -$(1.05) million, or $0.00 per diluted share, compared to a net loss of -$(15.5) million, or -$(0.05) per diluted share for the fourth quarter of 2021. Net loss for full year 2022 was -($20.00) million, or -$(0.64) per diluted share, compared to a net loss of -$(46.00) million, or -$(1.61) per diluted share for full year 2021.

At the end of calendar 2022 the company had cash and cash equivalents of $15.00 million, compared to cash and cash equivalents of $7.9 million at the end of calendar 2021.

Taken together, the company is moving in the right direction. Overall improvement on its bottom line came from a more favorable product mix, led by growing international connectivity services, with a lot of that coming from PaaS and SaaS revenue, which commands higher margin within that segment.

While a lot of things are aligning right for the company as a number of its markets are opening up from the impact of COVID-19, it now faces another challenge if the global economy weakens going forward, which I think is the most likely scenario.

Management guides for total revenue for 2023 to be in a range of $85.00 million to $100.00 million.

Profitability metrics

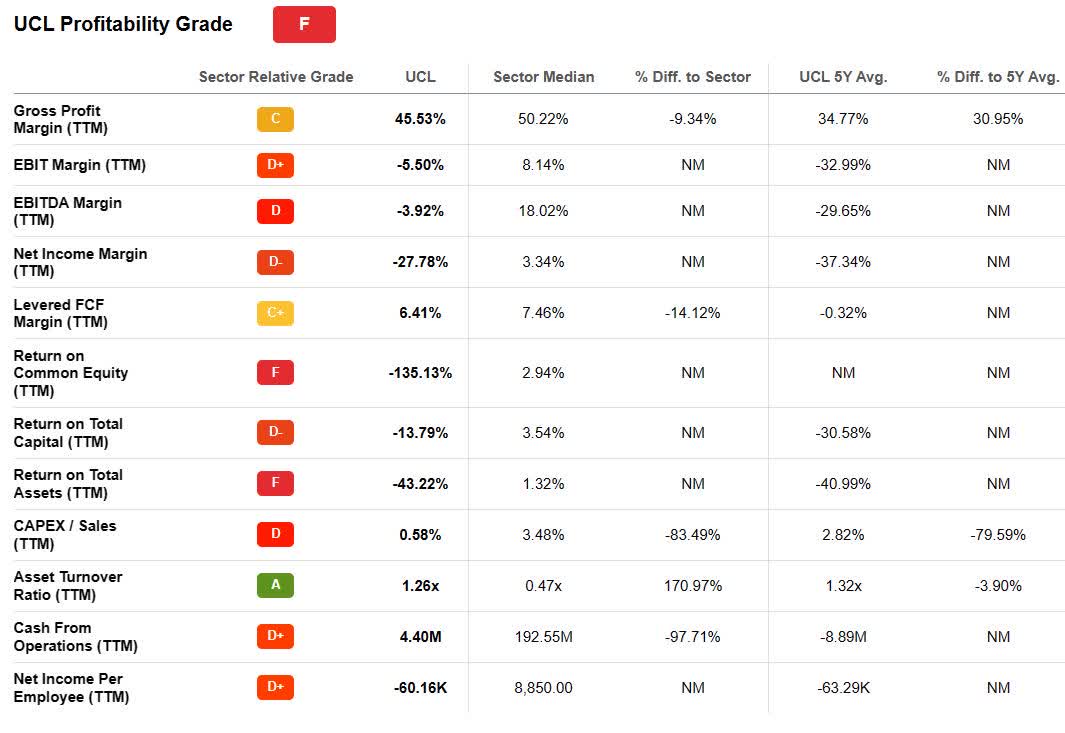

UCL is very weak in profitability, underperforming the sector median in most metrics. Gross margin (ttm) was one of its better performers, coming in at 45.53 percent, compared to the sector median of 50.22 percent, lower by -(9.34) percent.

EBITDA margin (ttm) was -(3.92) percent, compared to the sector median of 18.02 percent.

The important net income margin ( ttm ) metric was -(27.78) percent, compared to the sector median of 3.34 percent.

Return on equity ( ttm ) was -(135.13) percent, compared to the sector median of 2.94 percent. Return on capital ( ttm ) w as -(13.79) percent, compared to the sector median of 3.54 percent. Return on asset s ( ttm ) was -(43.22) percent, compared to the sector median of 1.32 percent.

Cash from operations ( ttm ) was $4.40 million, compared to the sector median of $192.55 million.

Concerning valuation metrics , a couple I wanted to point out was first, EV/Sales ( ttm ), which was 1.62, compared to the sector median of 1.99 - lower by 18.57 percent, and EV/Sales (fwd), which was 1.33, compared to the sector median of 1.81 - lower by 26.60 percent. Second was Price/Sales (ttm), which was 1.86, compared to the sector median of 1.29 - up by 28.69 percent. Price/Sales (fwd) is 1.62, compared to the sector median of 1.22 - higher by 32.57 percent.

Revenue growth (fwd) looks much better for the company, with expectations it'll jump 18.8 percent, compared to the sector median of 5.31 percent - better by 255.55 percent.

Momentum for the company is also significantly better then the sector median.

{kind=link}

Seeking Alpha

The way forward

UCL operates as a mobile data traffic sharing marketplace at the local and international levels, with its fast-growing international connectivity business being important to its future performance because the segment generates higher margins, which is vital to it moving toward profitability.

There are two important things for investors to consider with UCL: its production mix and opening up of travel over the next couple of years. The opening up of travel represents the improved product mix, and as mentioned above, international business represents a more favorable margin for the company.

The company's uCloudlink 1.0 business is the one that targets demand in the international data roaming market.

Management said in its earnings report that the United Nations World Travel Organization projects international tourist travel to recover to a range of 80 percent to 95 percent of pre-pandemic levels, which offers a solid growth opportunity for the company.

On the other hand, China and Southeast Asia are expected to recover slower, with the company thinking China will recover only 40 percent in 2023 but expecting it to be fully recovered in 2024. Southeast Asia may recover a little higher than that, maybe coming in at 50 percent of recovery in 2023, and full recovery in 2024.

With national borders further opening up, the company is moving quickly to meet cross-border coverage demand. Consequently, it believes its uCloudlink 1.0 roaming business should provide increasing growth in 2023 and beyond. If the company is able to gain share in international connectivity, it has a good chance of outperforming over the next couple of years, especially in regard to the bottom line because of the widening of margins.

The company now provides international data connectivity services in over 140 countries.

{kind=link}

Investor Presentation

What could go wrong

UCL is moving in the right direction, and economic conditions within the sector it competes in are improving as borders continue to open up, providing significant growth opportunities for the company.

Even so, the general macroeconomic conditions are probably going to get worse before they get better in my opinion, and that would mean businesses and consumers reconsidering spending decisions, which would mean less travel, and less demand for UCL's services in the near term.

I believe the company has good products and services, but almost anything that could go wrong has gone wrong, and I don't think that's going to improve over the next year, primarily from economic conditions I believe are going to worsen.

So while the world is opening up more, there's a strong probability spending will cut back because of economic concerns and uncertainties. If that's how it plays out, it means the stock is likely to come under heavy pressure until economic headwinds abate.

What that suggests is the timeframe for the company to improve revenue and earnings will be pushed out further into the future. Under those conditions, it'll probably start to show stronger improvement in around mid-2024.

Conclusion

UCL operates in a market that has increasing demand, and over time, if it continues to grow share - especially in its international connectivity business, it should result in consistent, sustainable growth on the top and bottom lines.

In the near term I believe it's going to struggle because of a weakening economy that is likely to get worse as 2023 goes on and could remain subdued into the first quarter of 2024.

For that reason, even with other favorable tailwinds like borders opening up and improved margins, I think the headwinds are going to overwhelm the tailwinds from a cutback in spending at the corporate level and consumer level until confirmation the global economy is returning to meaningful growth mode.

My thesis is the company has a much stronger chance of having a significant correction in 2023, and that would be the time to take a serious look at taking a position in it.

Over time I think UCL has a high-percentage chance of rewarding patient shareholders, but I would wait until a much more favorable entry point in order to improve risk/reward.

One last thing to consider is, UCL stock is traded very thinly, so that should be considered in regard to position sizing.

For further details see:

uCloudlink Group: Not A Good Time To Get In