UGI - UGI Corporation Has A Stable History And A Promising Future Business Outlook

2023-08-14 13:53:01 ET

Summary

- UGI Corporation is a leading energy products and services distributor with operations in the United States and Europe.

- The company's strategic investments and initiatives in various agreements will contribute to further operational improvements.

- UGI Corporation's stable history and promising future business outlook make it an attractive player in the energy distribution industry.

Introduction

UGI Corporation ( UGI ) is a company of multiple segments in the United States and Europe. It distributes, stores, and transports energy products and services through its business territories. UGI’s major operations are in four business segments: AmeriGas Propane, UGI International, Midstream & Marketing, and Utilities. Throughout the analysis, I have investigated UGI’s operations and outlook in each segment and concluded that based on the company’s several investments and initiatives in different agreements, their future operations should improve further and thus bring more benefits for investors. That is why I have upgraded my previous Hold rating to a Buy rating.

UGI business outlook

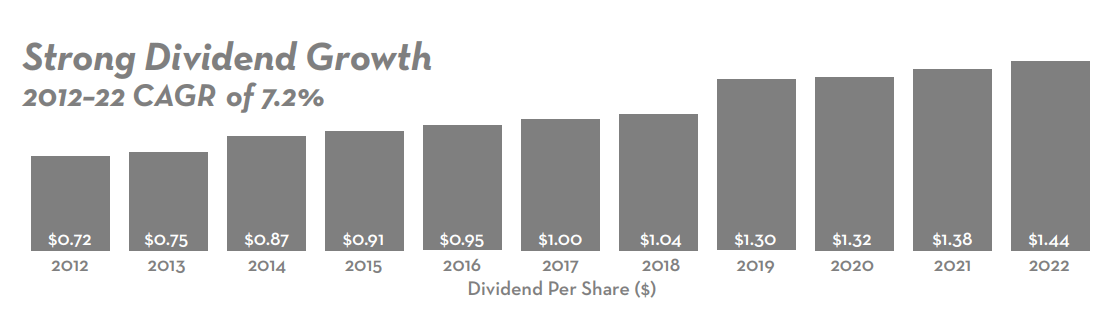

It has been 139 years that UGI has paid dividends, while it has been 36 years that they have consequently increased their dividend payment. Thus, in this uncertain period after the COVID-19 outbreak and the world’s current complicated geo-political landscape, I believe that UGI is a safe company to invest in on the basis of strong historical financials (see Figure 1).

Figure 1

{kind=link}

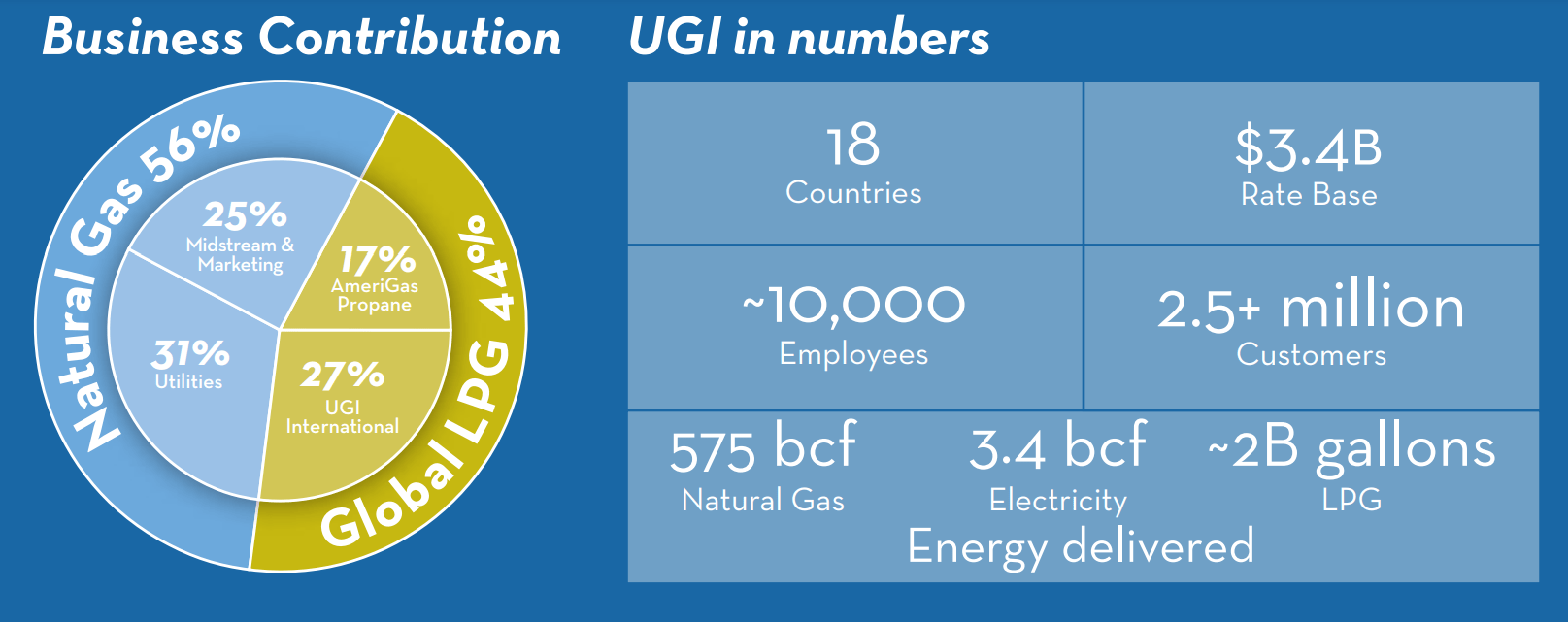

UGI is a well-performed blue-chip company that is the second-largest regulated gas utility in Pennsylvania and the largest in West Virginia. During 2022 , 56% of their EPS was from their natural gas business, and 44% was from global LPG business. It is worth noting that UGI has the largest retail LPG distributor in the United States based on the volume of propane gallons distributed annually. They also distribute LPG to 17 European countries (see Figure 2).

Figure 2 – UGI’s business contribution

{kind=link}

As mentioned, the largest business portion of UGI’ is associated with natural gas. The company has expanded its interest in natural gas gathering systems through the acquisitions of UGI Moraine East and Pennant Midstream, LLC. These investments brought high production volumes in 2022 and indicate the company’s capability of providing sustainable values for its shareholders. During 2022, the geopolitical situation in Europe, like the war between Russia and Ukraine, which led to severe fluctuations in natural gas and electricity prices, affected UGI’s cash flows to a great extent. However, it did not hurt the management’s strategy for shareholder returns because UGI benefited $150 million at AmeriGas and about $33 million at UGI International from their 3-year business transformation initiatives. These strategies helped the management to mostly offset the impact of the cost environment during the last year.

Furthermore, the company has invested and participated in several business strategies to produce renewable natural gas and bioLPG. Their total renewables commitment has been over $300 million, and they have a plan to invest approximately $1.25 billion in renewable energy solutions by 2025. The Net Zero Emissions by 2050 scenario sees a rapid increase in the use of bioenergy to displace fossil fuels by 2030. These investments, coupled with other project developments, make UGI well-positioned to develop investment opportunities in renewable energy markets and help the company to take advantage of the Inflation Reduction Act rules regarding tax credits for renewable energy projects and thus declining their costs while inclining their portfolio balance.

AmeriGas Propane segment

During the recent winter , heating degree days were about 4% higher than usual, while they were 16.5% higher than in the winter of 2022. Heating degree days measure the difference between the outside temperature and room temperature to help calculate the demand for energy needed to heat an area. The weather experienced a 9% higher warmth in the most recent quarter versus the same period of the prior year. Weather conditions have a paramount impact on the demand for propane. This is because the volume of propane used severely relies on the coldness of the winter weather. As a result, AmeriGas Propane’s retail sold dropped by 6% from 173 million in 3Q 2022 to 163 million in 3Q 2023. Although their total revenues declined by 14% to $514 million, the total margin of AmeriGas was boosted by $36 million. Thanks to higher LPG unit margins.

The management’s plans for operating multiple production facilities and expanding renewable production facilities have a crucial impact on their capability of providing solid financials in the long term. UGI has entered into a 15-year agreement to produce renewable fuels from renewable ethanol in the U.S. and Europe. Thereby, it will increase the supply of renewable propane in the future. Also, it is worth noting that the management has a target of constructing the first product facility onstream by the end of the Fiscal Year 2024. This will lead to an annual production of 50 million gallons of combined renewable fuels: a great outlook for the company’s renewable supplies.

UGI’s Midstream & Marketing segment

This segment is managed by UGI’s subsidiary called Energy Services. They provide energy marketing, electricity generation, and RNG production in the Mid-Atlantic region of the U.S. and California. At the end of the third quarter of 2023, the midstream segment’s revenue declined by 47% to $279 million versus $525 million at the same time in 2022. However, it is worth noting that this segment’s operating margin reached 14%, while it was 7% at the end of the third quarter of 2022. Similar to other business segments of UGI, warmer weather has negatively affected the midstream and marketing segments by declining their volumes. During the recent quarter, temperatures were 7% warmer than usual and 3% warmer than the prior-year period, thereby pushing total margins of $2 million down versus the same time in 2022. However, it is worth noting that Energy Services recently embarked on a project that includes the construction of a manure digester and gas upgrading equipment, which will produce 55 million cubic feet of RNG annually after being completed. Besides other similar projects, this segment will produce more than 200 million cubic feet of RNG annually, thereby bringing more stability for the business and gathering a well-amount of benefits for investors.

UGI International

In the recent quarter, albeit temperatures were 10% warmer than usual, they were 5% colder than the same time in 2022. As a result, retail volume increased by 2%, which thankfully could partially offset the effect of energy-related phenomena across Europe. Meanwhile, the company’s revenues from international activities fall by 17% to $611 million in the 3Q 2023 year-over-year compared with $783 million in 3Q 2022. It mainly stemmed from lower average propane wholesale selling prices across Europe, which were circa 41% lower than in the same period in 2022. Notwithstanding lower revenues, their operating margin of 2.9% in 3Q 2022 improved to 3.4% at the end of 3Q 2023.

Regarding the future potentials, the company has a plan to develop 6 plants to produce rDME, which will lead to a total production capacity of 300,000 tons of rDME per year by the end of 2027. rDME is a cost-effective and clean-burning fuel that is chemically similar to propane and butane. So, it behaves in the same way as LPG. Similar to LPG, rDME is easily and safely transported as a liquid in cylinders and tanks.

UGI’s Utility segment

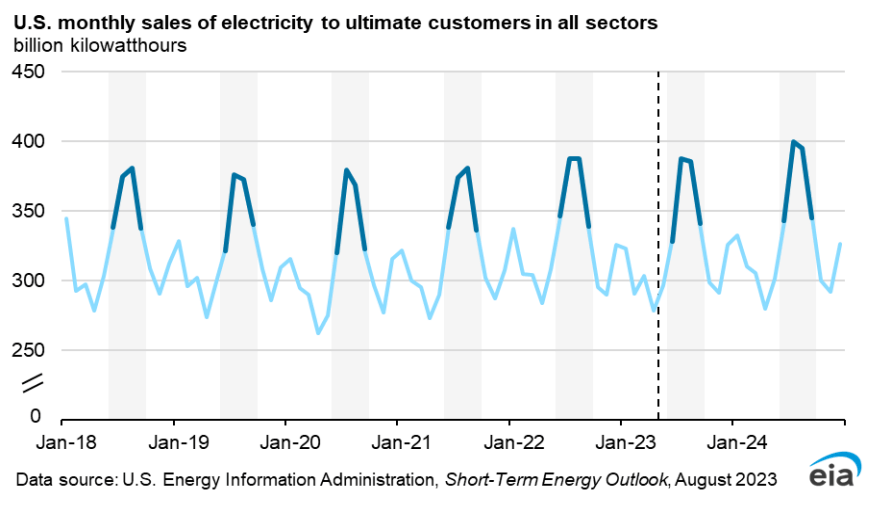

During the recent winter, the Gas Utility service territory experienced 8% lower core market throughput due to 11% warmer weather than normal and 8% warmer than the same time in the last year. As we know, winter weather strongly affects residential and commercial demand for natural gas. the higher temperatures caused lower volumes and thus lower 16% lower operating income of $32 million in 3Q 2023 versus $38 million in 3Q 2022. According to the EIA expectations, U.S. electricity sales will increase by 2% in 2024 based on the expectations of warmer summer next year, and thus, demand for electricity will increase in the industrial sector as the economic growth is recovering after the COVID-19 pandemic (see Figure 3).

Figure 3

{kind=link}

Moreover, renewables are increasing their share of electricity generation by passing time. By the end of 2023, 22% of U.S. total electricity generation will be by renewables, while that share will grow and reach 25% of total generation in the U.S. by 2024. Meanwhile, the share of natural gas in U.S. electricity generation will decline from 42% in 2023 to 40% in 2024. As a result, UGI’s vast investments in renewables pave the company’s path for energy transition and thus meet global needs.

The poor sentiment for UGI

Higher weather temperatures affected the financials of UGI to a great extent. Although higher margins caused AmeriGas to reach higher EBIT, the amount of EBIT in UGI International, Midstream and Marketing, and Utilities declined. Moreover, based on the last report, UGI holds over $7 billion of debt, which could become a concern for the company’s future stability. These results have led to lower fans for UGI stocks recently. However, we should bear in mind that in the utility industry, we need to accept the usual volatility. In my opinion, UGI Corporation is a wise decision for growth investors as the company is focusing on investment growth. In minutiae, the company has estimated to have approximately 25% higher capital expenditures of $1040 million by the end of Fiscal 2023 versus $835 million in Fiscal 2022. It is worth noting that these increases are mainly in Midstream and Marketing and UGI International for expanding natural gas infrastructures and investing in renewable energy projects in these segments. As a result, notwithstanding short-term capital-intensive activities that will lead to higher amounts of debt and costs, the management’s focus on growth investments should lead to benefits for shareholders in the future when renewables become the major source of electricity generation. Overall, I believe that now is a good time for investing in UGI because when the macroeconomic constraints pass, and interest rates fall in the future, the stock price will increase.

Risks

The primary risk associated with UGI's business is the demand for its products and services. As you know, UGI business is seasonal, and their demand decreases in warmer than usual heating seasons. It is because most of their customers use their services for heating their houses and businesses hence, warmer weather may adversely affect their operations and revenue generation. Moreover, during the last few years, the demand for LPG has declined in the U.S. and Europe, while there is no growing outlook in the near future. As a result, UGI requires to acquire other retail distributors to keep its ability to grow in the LPG industry. Additionally, UGI Corporation needs to grow its business through acquisitions, construction, and expansion. These developments and adjustments may lead to temporary higher costs and reduce their productivity. These risks may reversely affect their achievements and thus, cash flow operations.

Conclusion

UGI Corporation has a dividend yield of 6%, which is a great record for utility companies. The company has paid cash dividends for 139 years while has increased the dividend payment for 39 years in a row. During the last winter, UGI's revenues in different segments were greatly affected by warmer weather temperatures and thus, lower retail volumes. However, based on the management’s long-term plans and agreements in expanding renewable supply facilities, I conclude that UGI has a strong future financial outlook and is well capable of bringing benefits for its shareholders in the long term. Thus, I believe that a buy rating is appropriate for UGI stock.

For further details see:

UGI Corporation Has A Stable History And A Promising Future Business Outlook