UGI - UGI Corporation: Undervalued And A Long-Term Buy

2023-09-15 09:30:45 ET

Summary

- Utilities sector has declined nearly 8% in 2023, but many individual equities have fallen further.

- UGI Corporation is facing challenges in its business model, but efforts to improve performance in 2024 are expected.

- UGI Corporation is undervalued, has long-term dividend growth, and carries an above-average dividend yield.

Utilities are the worst-performing sector in 2023. They have declined nearly 8% in aggregate, but many individual equities have fallen further.

When interest rates rise, utility stock prices typically drop because investors prefer safer short-term United States Treasury bills and bonds. That said, many utilities are trading at their lowest valuation and highest dividend yields in a decade. Moreover, UGI Corporation ( UGI ) faces challenges specific to its business model, causing steeper share price declines. However, the utility is moving to exit underperforming businesses in Europe, raise its base rate for the regulated utilities, and lower costs. These efforts should improve performance in 2024. In the meantime, the equity is undervalued, has long-term dividend growth, and carries an above-average dividend yield. I view UGI Corporation as a long-term buy.

UGI Corporation Overview

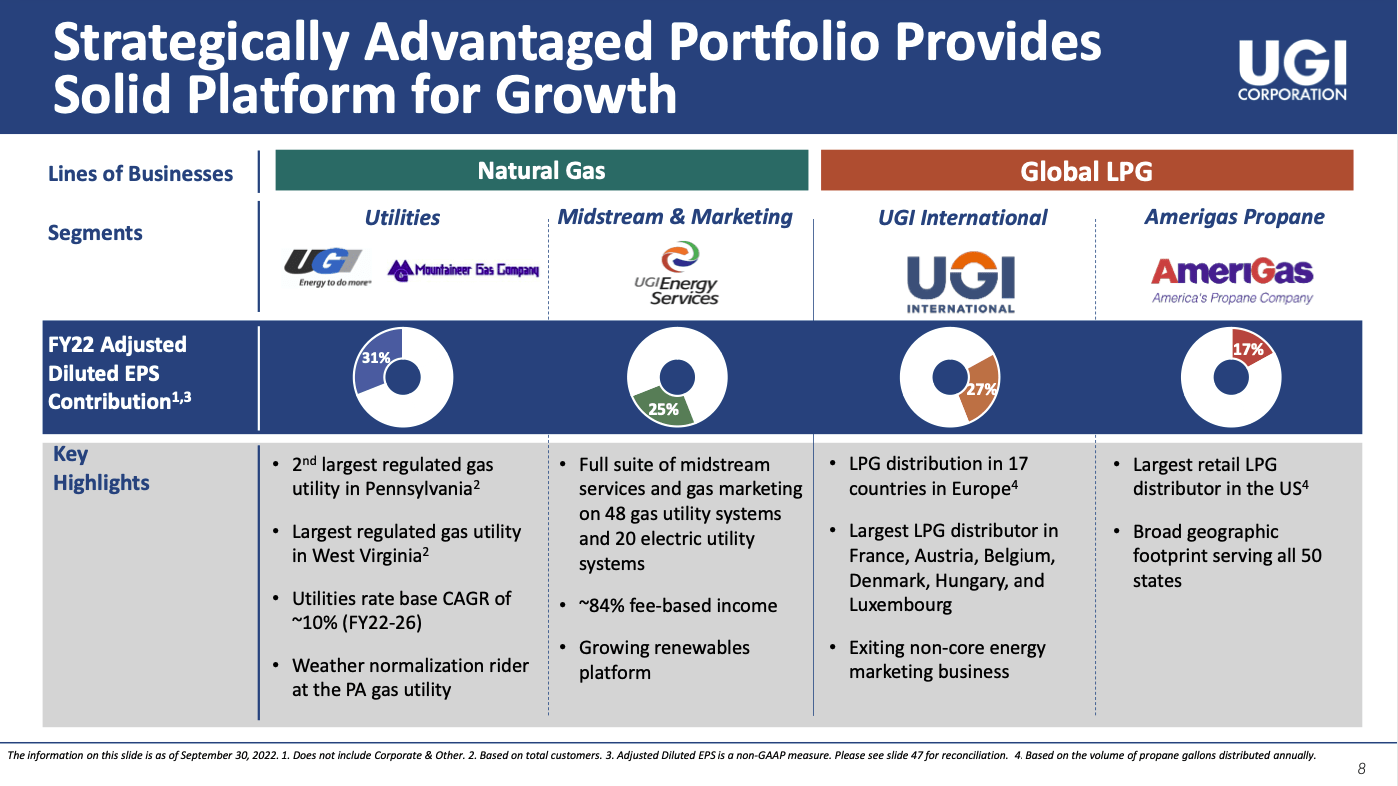

UGI Corporation is a diversified energy company with regulated and non-regulated businesses. The company reports four operating segments: AmeriGas Propane, UGI International, Midstream & Marketing, and UGI Utilities. Total revenue was $10,106 million in 2022 and $9,458 million in the last twelve months.

AmeriGas Propane is probably the crown jewel of the four businesses. Based on total annual volumes, it is the largest retailer of liquified petroleum gas [LPG] in America. The firm serves all 50 states through 1,400 distribution sites, reaching 1.3 million customers. The firm also distributes LPG in 17 European countries through UGI International. It is the market leader in France, Austria, Belgium, Denmark, Hungry, and Luxembourg and is one of the largest distributors in Poland, Slovakia, Norway, Czech Republic, Netherlands, and Sweden.

The regulated utilities are UGI Utilities and Mountaineer Gas Company, which have an attractive monopoly in their service area. The first firm provides natural gas and electricity services in Pennsylvania. It is the second largest regulated gas utility in Pennsylvania, serving 675,000+ customers in the eastern and central part of the state and a few hundred in one county of Maryland. UGI Utilities also delivers electricity to 62,500+ customers in northeastern Pennsylvania. Mountaineer Gas is the largest regulated gas utility in West Virginia, serving 214,000 customers.

UGI Energy Services is an unregulated midstream and marketing business. It provides natural gas to 12,400 residential, commercial, and industrial customers at 42,000+ sites in Pennsylvania and 21 other states.

{kind=link}

Near-Term Challenges

The utility had a challenging 2022 and early 2023 because of the Russo-Ukrainian War, warmer weather, and inflation. However, the firm has made moves to address some of the issues. As a result, the second half of 2023 and 2024 should show better results.

In Europe, the invasion of Ukraine disrupted the LPG market, leading to tight supply relative to demand. The response was to promote conservation efforts. As a result, demand dropped more than expected. According to the European Union, consumption was reduced by ~12% on average relative to the preceding few years. In 2023, demand is still below long-term trends. But UGI is exiting the non-core energy marketing business. According to the latest quarterly release , it “entered into definitive agreements to divest certain natural gas and power marketing portfolios in France and the wind and solar portfolio in the Netherlands.”

Next, warmer weather and heat waves in the western U.S. in the first half of 2023 caused lower sales for AmeriGas Propane and the regulated utilities, impacting margins. The Pennsylvania utility has implemented a weather normalization rider and higher base rates, which should improve revenue and margins. However, warm weather this winter may still affect AmeriGas Propane.

Lastly, inflation has pressured margins because labor and vehicle costs are higher. Inflationary pressures are declining, but the higher input costs are likely permanent. UGI Utilities will probably raise its base rate in the future to address higher expenses. However, the company is also focusing on operational efficiencies and cost controls.

Dividend Analysis

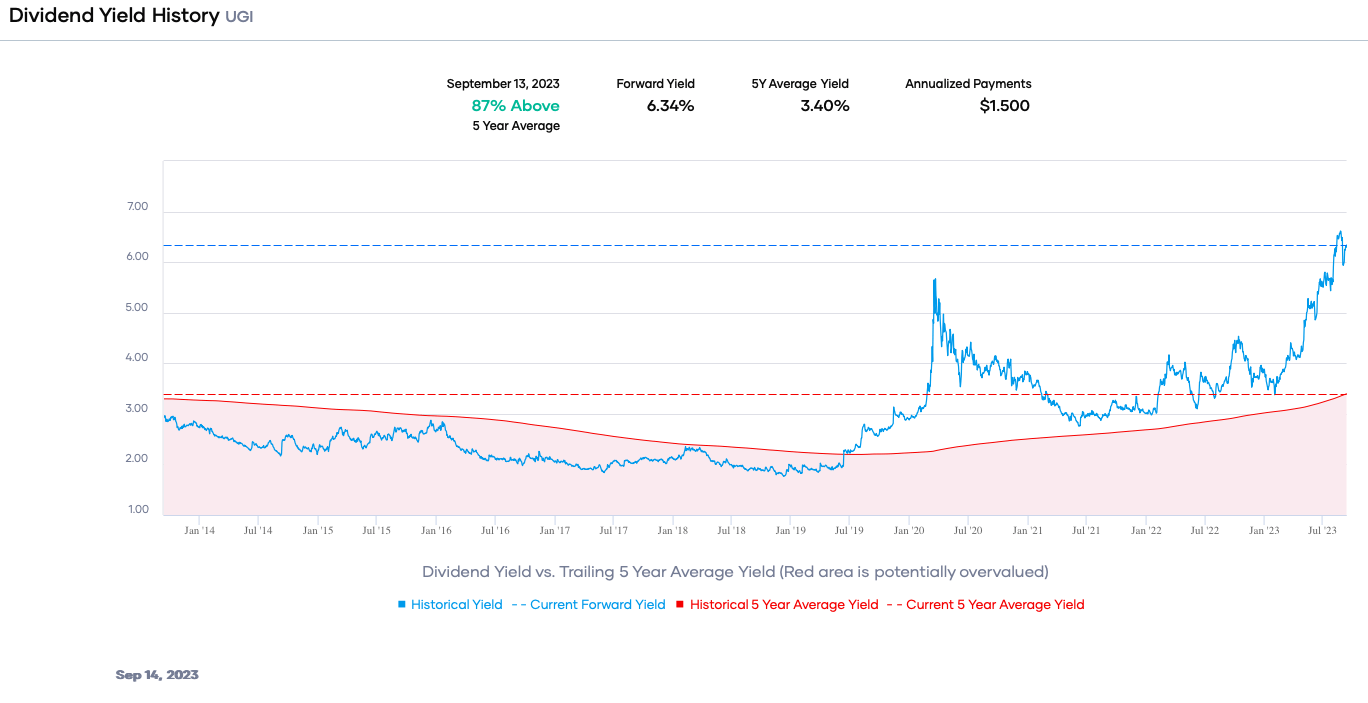

Like many utilities, UGI Corporation's dividend yield has risen almost to the highest in the past ten years. With an annualized forward dividend rate of $1.44, the forward dividend yield is around 6.34%, more than the 5-year average of 3.40%. The yield is attractive even with today’s higher short-term Treasury rates, and indicates the stock is considerably undervalued.

{kind=link}

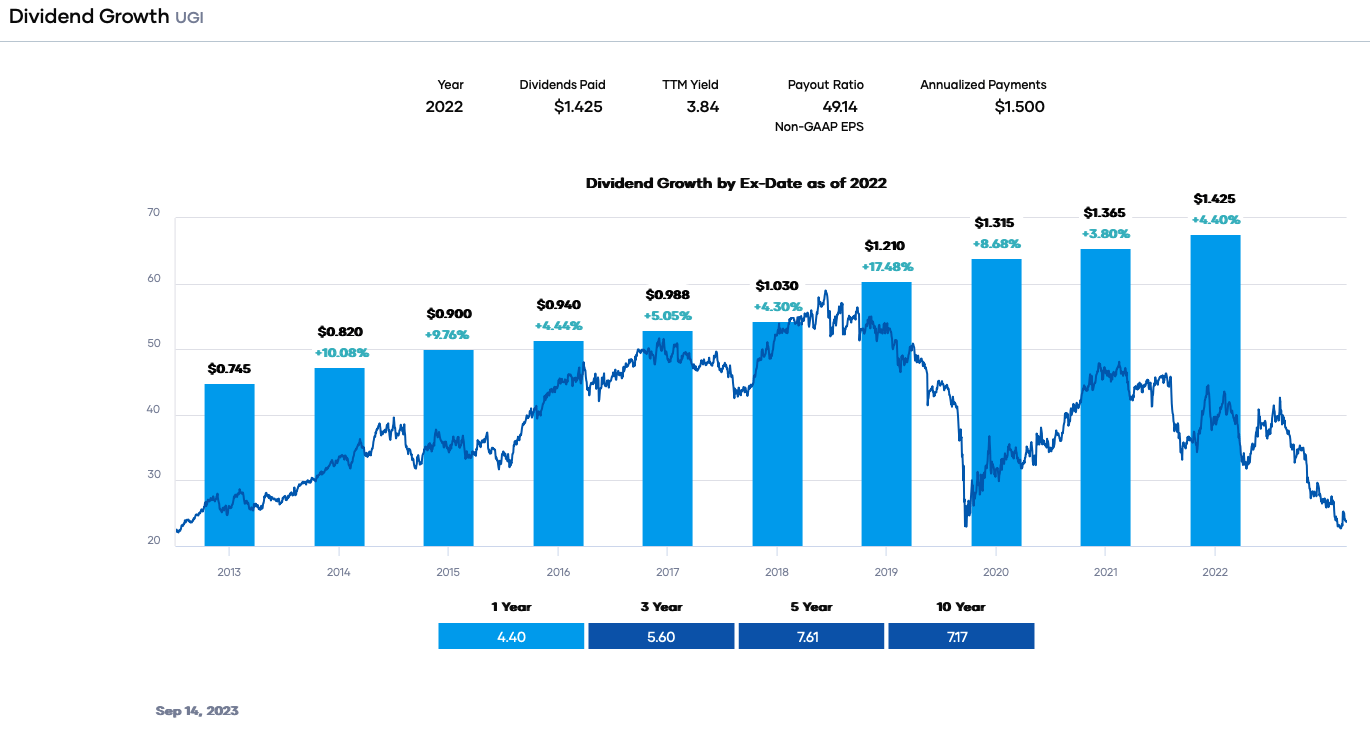

Besides the attractive yield, UGI Corporation is a dividend growth stock. It has 36 consecutive years of increases, placing it on the Dividend Champions list. The utility is also one of the few that have paid a dividend for a minimum of 100 years. The dividend growth rate is relatively consistent, at approximately 7.6% in the past five years and 7.2% in the trailing decade. The last quarterly dividend increase was to $0.375 per share from $0.360 in May 2023, and investors should expect another increase in May 2024.

{kind=link}

UGI Corporation has excellent dividend safety based on earnings per share, operating cash flow (OCF), and its balance sheet.

Earnings estimates for the fiscal year 2023 are $2.75 per share, and the dividend rate is $1.44 per share. These values result in a payout ratio of around 52%. This percentage is excellent for a utility and below our desired criterion of 65%. In addition, even with lower earnings than in fiscal year 2022, the dividend safety is still solid.

The utility generated $725 million in OCF in the last twelve months, an amount that covers the dividend requirement of $306 million. The dividend-to-OCF ratio is conservative at about 42%. This value is less than our target of 70% and points to excellent dividend safety.

Utilities usually carry an appreciable amount of debt because the business is capital-intensive. At the end of Q3 2023, short-term debt was $481 million, current long-term debt was $56 million, while long-term debt was $6,579 million. In addition, UGI Utilities has a BBB+/A3 lower-to-upper investment grade credit rating. However, the parent company's rating is lower because UGI International has a non-investment grade rating. However, UGI Corporation still has an investment grade rating; the total debt is not excessive, and the firm's balance sheet is sound.

Valuation

The share price has declined more than 36% year-to-date and in the past year. Simultaneously, the earnings multiple has fallen to 8.6X, considerably below the five- and ten-year ranges. The lower valuation is mainly because investors are gravitating to short-term bonds and the firm’s challenges related to the conflict in Ukraine, warmer-than-expected weather, and energy conservation efforts in Europe.

Analysts estimate earnings per share of $2.75 in fiscal 2023. We will use 14X as the fair value multiple near the mid-point of the 5-year range, and accounting for near-term challenges, market leadership of the LPG business, and the regulated utility monopoly. Thus, our fair value estimate is $38.50. The present share price is ~$24.09, implying UGI Corporation is undervalued.

Applying a sensitivity calculation using P/E ratios between 13X and 15X, we obtain a fair value range from $35.75 to $41.25. Hence, the stock price is approximately 58% to 67% of the fair value estimate.

Estimated Current Valuation Based On P/E Ratio

| P/E Ratio |

| 13 |

| 14 |

| 15 |

| Estimated Value |

| $35.75 |

| $38.50 |

| $41.25 |

| % of Estimated Value at Current Stock Price |

| 67% |

| 63% |

| 58% |

Source: Dividend Power Calculations

How does this calculation compare to other valuation models? Portfolio Insight’s blended fair value model combining the P/E ratio and dividend yield gives a fair value estimate of $41.58 per share. The Gordon Growth Model [GGM] provides a fair value of $36.00, assuming a discount rate of 10% and a conservative annual dividend growth rate of 6%.

The three-model average is ~$38.69, indicating that UGI Corporation is significantly undervalued at the current price.

Final Thoughts

Utilities are out of favor right now because interest rates are high, and tech stocks are gaining. Moreover, UGI Corporation faces challenges unique to its non-regulated business in Europe, weather, and inflation. However, the firm is exiting its non-core assets in Europe and making other moves to improve performance. In the meantime, the regulated utilities are performing well. Moreover, the stock is a Dividend Champion, has a safe dividend, and is undervalued. We view UGI Corporation as a long-term buy.

For further details see:

UGI Corporation: Undervalued And A Long-Term Buy